Global Preimplantation Genetic Screening Pgs Technology Market

Market Size in USD Million

CAGR :

%

USD

823.72 Million

USD

1,830.95 Million

2025

2033

USD

823.72 Million

USD

1,830.95 Million

2025

2033

| 2026 –2033 | |

| USD 823.72 Million | |

| USD 1,830.95 Million | |

| % | |

|

Preimplantation Genetic Screening (PGS) Technology Market Size

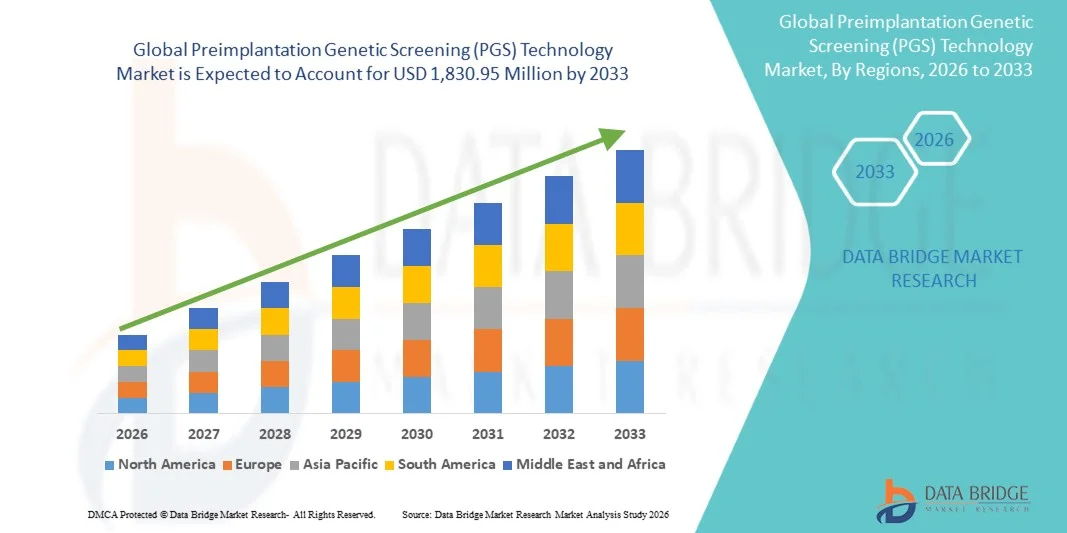

- The global Preimplantation Genetic Screening (PGS) technology market size was valued at USD 823.72 million in 2025and is expected to reach USD 1,830.95 million by 2033, at a CAGR of 10.50% during the forecast period

- The market growth is largely fueled by the increasing adoption of assisted reproductive technologies (ART) and rapid advancements in embryo screening techniques, including next-generation sequencing (NGS) and comprehensive chromosomal screening, which are improving implantation success rates and reducing genetic disorder risks

- Furthermore, rising incidence of infertility, growing maternal age trends, and increasing awareness of genetic disease prevention are driving demand for accurate and early-stage embryo selection solutions, positioning PGS technology as a critical component in modern fertility treatments, thereby significantly accelerating industry expansion

Preimplantation Genetic Screening (PGS) Technology Market Analysis

- Preimplantation Genetic Screening (PGS) technology, enabling chromosomal analysis of embryos prior to implantation in IVF procedures, is increasingly becoming a critical tool in reproductive medicine due to its ability to enhance implantation success rates and reduce the risk of genetic abnormalities in newborns

- The rising demand for Preimplantation Genetic Screening (PGS) technology is primarily driven by increasing infertility rates, delayed childbearing, and growing awareness regarding genetic disorder prevention, along with rapid advancements in embryo biopsy methods and next-generation sequencing (NGS) that are improving diagnostic accuracy and clinical outcomes

- North America dominated the Preimplantation Genetic Screening (PGS) technology market with the largest revenue share of 41.6% in 2025, supported by advanced fertility clinic infrastructure, high adoption of IVF procedures, strong clinical expertise, and the presence of leading reproductive genetics providers, with the U.S. witnessing significant uptake of advanced embryo screening technologies

- Asia-Pacific is expected to be the fastest growing region in the Preimplantation Genetic Screening (PGS) technology market during the forecast period due to rising infertility prevalence, expanding fertility treatment accessibility, increasing medical tourism, and improving healthcare infrastructure across emerging economies

- The next-generation sequencing (NGS)-based screening segment dominated the Preimplantation Genetic Screening (PGS) technology market with a share of 46.8% in 2025, driven by its high-resolution chromosomal detection capability, improved embryo selection accuracy, and growing preference among fertility specialists for comprehensive genetic screening solutions

Report Scope and Preimplantation Genetic Screening (PGS) Technology Market Segmentation

|

Attributes |

Preimplantation Genetic Screening (PGS) Technology Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

|

|

Market Opportunities |

· Expansion of Preimplantation Genetic Screening (PGS) technology into emerging fertility markets · Increasing integration of AI-powered embryo selection algorithms with Preimplantation Genetic Screening (PGS) technology |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Preimplantation Genetic Screening (PGS) Technology Market Trends

“Rising Adoption of NGS-Based Comprehensive Embryo Screening”

- A significant and accelerating trend in the global Preimplantation Genetic Screening (PGS) technology market is the widespread shift toward next-generation sequencing (NGS)-based platforms, which are improving chromosomal detection accuracy and enabling more comprehensive embryo evaluation in IVF procedures

- For instance, Illumina-based PGS workflows are increasingly being used in IVF laboratories to detect aneuploidies with higher resolution compared to traditional array-based methods, supporting improved implantation outcomes

- The integration of artificial intelligence (AI) and advanced bioinformatics tools in Preimplantation Genetic Screening (PGS) technology is enhancing embryo grading, enabling predictive analysis of implantation potential and reducing subjectivity in clinical decision-making

- The growing adoption of non-invasive or minimally invasive embryo assessment techniques is facilitating safer genetic screening processes, improving embryo viability while reducing procedural risks associated with traditional biopsy methods

- The expansion of personalized reproductive medicine is driving the use of Preimplantation Genetic Screening (PGS) technology to tailor embryo selection strategies based on patient-specific genetic and clinical profiles

- Increasing collaboration between fertility clinics and genomics companies is accelerating innovation in Preimplantation Genetic Screening (PGS) technology, enabling faster test turnaround times and improved diagnostic precision

- This trend toward more precise, data-driven, and less invasive Preimplantation Genetic Screening (PGS) technology is transforming IVF workflows, leading to higher success rates and more personalized reproductive treatment strategies

Preimplantation Genetic Screening (PGS) Technology Market Dynamics

Driver

“Rising Infertility Rates and Expanding IVF Treatment Adoption”

- The increasing prevalence of infertility and delayed pregnancies is a major driver fueling the demand for Preimplantation Genetic Screening (PGS) technology, as couples increasingly rely on IVF procedures to achieve successful pregnancies

- For instance, in 2025, fertility clinics across major healthcare systems reported rising utilization of PGS technology to improve embryo selection success rates and reduce genetic disorder risks in high-risk pregnancies

- Growing awareness of genetic diseases and the benefits of early embryo screening is encouraging wider adoption of Preimplantation Genetic Screening (PGS) technology among patients undergoing assisted reproductive treatments

- Furthermore, increasing accessibility of IVF services in emerging economies and expanding fertility clinic infrastructure are making Preimplantation Genetic Screening (PGS) technology more widely available

- The ability of Preimplantation Genetic Screening (PGS) technology to significantly improve implantation success rates and reduce miscarriage risk is a key factor propelling its integration into standard IVF protocols

- Rising investments in fertility research and reproductive genetics are accelerating technological advancements in Preimplantation Genetic Screening (PGS) technology, improving efficiency and clinical outcomes

- The growing trend of elective fertility preservation and delayed parenthood is further increasing reliance on Preimplantation Genetic Screening (PGS) technology for healthier pregnancy outcomes

- The rising acceptance of assisted reproductive technologies globally is expected to further strengthen demand for Preimplantation Genetic Screening (PGS) technology across healthcare systems

Restraint/Challenge

“High Cost of Advanced Genetic Screening and Ethical Complexity”

- Concerns regarding the high cost of Preimplantation Genetic Screening (PGS) technology and associated IVF procedures pose a significant challenge to widespread adoption, particularly in cost-sensitive and developing healthcare markets

- For instance, in 2025, several fertility centers highlighted that advanced NGS-based PGS testing significantly increases overall IVF cycle costs, limiting accessibility for middle-income patients

- Ethical concerns surrounding embryo selection and genetic screening practices also present regulatory and societal challenges, affecting the acceptance of Preimplantation Genetic Screening (PGS) technology in certain regions

- Furthermore, variations in regulatory frameworks across countries create inconsistencies in the approval and usage of Preimplantation Genetic Screening (PGS) technology, slowing standardized adoption

- Limited reimbursement coverage for fertility treatments and genetic screening procedures further restricts patient access to Preimplantation Genetic Screening (PGS) technology in several healthcare systems

- Shortage of highly skilled embryologists and genetic specialists in emerging regions is also limiting the efficient implementation of Preimplantation Genetic Screening (PGS) technology in clinical practice

- Data privacy concerns related to genetic information storage and sharing are emerging as an additional barrier to broader adoption of Preimplantation Genetic Screening (PGS) technology

- Addressing affordability issues, improving regulatory harmonization, and strengthening ethical guidelines will be crucial for the sustained and equitable growth of the Preimplantation Genetic Screening (PGS) technology market

Preimplantation Genetic Screening (PGS) Technology Market Scope

The market is segmented on the basis of procedure type, technology, product and services, end user, test type, and application.

- By Procedure Type

On the basis of procedure type, the Preimplantation Genetic Screening (PGS) Technology market is segmented into Preimplantation Genetic Screening (PGS) and Preimplantation Genetic Diagnosis (PGD). The Preimplantation Genetic Screening (PGS) segment dominated the market with the largest revenue share of 58.4% in 2025, driven by its widespread use in IVF procedures to identify chromosomal abnormalities in embryos before implantation. Clinics prefer PGS due to its ability to significantly improve implantation success rates and reduce miscarriage risks associated with aneuploid embryos. The segment also benefits from increasing adoption of NGS-based screening, which enhances accuracy and reliability in embryo selection. Rising maternal age and infertility cases further support strong demand for Preimplantation Genetic Screening (PGS) technology in routine fertility treatments. In addition, improved clinical guidelines recommending embryo screening in high-risk pregnancies continue to strengthen its dominance across fertility centers globally.

The Preimplantation Genetic Diagnosis (PGD) segment is expected to witness the fastest growth rate of 18.9% from 2026 to 2033, fueled by increasing demand for detection of specific inherited genetic disorders before embryo implantation. PGD is gaining traction among couples with known genetic conditions seeking to prevent transmission to offspring. Advances in molecular diagnostics and sequencing technologies are enhancing the accuracy of PGD testing. Rising awareness of single-gene disorders and expanding access to genetic counseling services are also driving adoption. Furthermore, growing integration of PGD with IVF cycles in specialized fertility clinics is accelerating segment growth across developed and emerging markets.

- By Technology

On the basis of technology, the Preimplantation Genetic Screening (PGS) Technology market is segmented into Next-Generation Sequencing (NGS), Polymerase Chain Reaction (PCR), Fluorescence In Situ Hybridization (FISH), Comparative Genomic Hybridization (CGH), and Single-Nucleotide Polymorphism (SNP). The Next-Generation Sequencing (NGS) segment dominated the market with the largest revenue share of 46.8% in 2025, driven by its superior accuracy, high-throughput capability, and ability to detect comprehensive chromosomal abnormalities. NGS has become the preferred technology in modern IVF laboratories due to its ability to provide detailed genomic insights from minimal embryo samples. Increasing automation in sequencing workflows and declining sequencing costs are further supporting adoption. Fertility clinics increasingly rely on NGS for improved embryo selection and higher implantation success rates. Its compatibility with AI-based analysis tools also enhances clinical decision-making efficiency.

The Polymerase Chain Reaction (PCR) segment is expected to witness the fastest growth rate of 17.6% from 2026 to 2033, driven by its cost-effectiveness and rapid amplification capabilities for targeted genetic analysis. PCR remains widely used in smaller fertility centers due to its simplicity and lower infrastructure requirements. Continuous improvements in real-time PCR techniques are enhancing diagnostic accuracy in embryo screening applications. The method is also gaining traction in emerging markets where affordability is a key consideration. In addition, its integration with multiplex testing formats is expanding its utility in routine Preimplantation Genetic Screening (PGS) workflows.

- By Product and Services

On the basis of product and services, the Preimplantation Genetic Screening (PGS) Technology market is segmented into reagents and consumables, instruments, and software and services. The Reagents and Consumables segment dominated the market with the largest revenue share of 49.3% in 2025, driven by repeated usage requirements in every IVF and genetic screening cycle. These include biopsy kits, amplification reagents, and sequencing consumables essential for embryo testing procedures. Rising IVF cycle volumes globally are directly increasing demand for consumables. The segment also benefits from continuous technological upgrades requiring compatible reagent systems. Strong recurring revenue models for manufacturers further strengthen dominance in this segment.

The Software and Services segment is expected to witness the fastest growth rate of 20.4% from 2026 to 2033, driven by increasing adoption of AI-based embryo analysis platforms and cloud-based genetic data interpretation tools. Fertility clinics are increasingly relying on software solutions for embryo grading, data management, and predictive analytics. Integration of machine learning algorithms is improving accuracy in implantation outcome predictions. Growing outsourcing of genetic analysis to specialized service providers is also boosting segment growth. In addition, rising demand for digitalized IVF workflows is accelerating the adoption of advanced software and service platforms.

- By End User

On the basis of end user, the Preimplantation Genetic Screening (PGS) Technology market is segmented into maternity centers and fertility clinics, hospitals, diagnostic labs and service providers, and research laboratories and academic institutes. The Maternity Centers and Fertility Clinics segment dominated the market with the largest revenue share of 61.7% in 2025, driven by their primary role in performing IVF procedures and embryo screening services. These centers are increasingly integrating advanced genetic testing platforms to improve pregnancy success rates. High patient inflow for infertility treatments significantly supports segment dominance. Clinics also benefit from specialized infrastructure and trained embryologists for handling PGS workflows. Rising global IVF adoption further strengthens their leading position in the market.

The Diagnostic Labs and Service Providers segment is expected to witness the fastest growth rate of 19.2% from 2026 to 2033, driven by increasing outsourcing of genetic testing services by fertility clinics. Independent diagnostic laboratories offer cost-efficient and high-throughput screening solutions. Advancements in centralized testing models are improving turnaround times and scalability. Growing demand for specialized genomic interpretation services is also fueling expansion. In addition, increasing collaborations between IVF clinics and third-party genetic labs are accelerating segment growth.

- By Test Type

On the basis of test type, the Preimplantation Genetic Screening (PGS) Technology market is segmented into Chromosomal Abnormalities, X-linked Diseases, Embryo Testing, Aneuploidy Screening, HLA Typing, and Other PGT Types. The Aneuploidy Screening segment dominated the market with the largest revenue share of 52.6% in 2025, driven by its critical role in identifying embryos with abnormal chromosome numbers that often lead to implantation failure or miscarriage. This test type is widely adopted as a standard screening procedure in IVF clinics. Increasing maternal age and associated chromosomal risks are further boosting demand. Advancements in NGS technology have significantly improved detection accuracy. Its strong clinical relevance in improving live birth rates reinforces segment dominance.

The HLA Typing segment is expected to witness the fastest growth rate of 18.1% from 2026 to 2033, driven by its application in selecting embryos compatible for stem cell therapy in treating genetic and blood disorders. Growing interest in personalized regenerative medicine is supporting adoption. Increasing awareness of sibling donor compatibility for therapeutic purposes is also contributing to demand. Technological advancements in high-resolution genetic matching are improving feasibility. Furthermore, expanding clinical research in immunogenetics is accelerating segment growth globally.

- By Application

On the basis of application, the Preimplantation Genetic Screening (PGS) Technology market is segmented into Embryo HLA Typing for Stem Cell Therapy, IVF prognosis, late onset genetic disorders, inherited genetic disease, and others. The IVF Prognosis segment dominated the market with the largest revenue share of 45.9% in 2025, driven by the increasing use of Preimplantation Genetic Screening (PGS) technology to improve implantation success rates and predict embryo viability. Fertility clinics widely use PGS to enhance IVF outcomes and reduce treatment failures. Rising infertility rates globally are further strengthening demand. The segment benefits from integration of advanced sequencing technologies for better embryo selection. Continuous improvements in predictive genetic analysis are reinforcing its dominance.

The Inherited Genetic Disease segment is expected to witness the fastest growth rate of 20.1% from 2026 to 2033, driven by increasing demand for prevention of hereditary disorders before implantation. Couples with known genetic risks are increasingly opting for Preimplantation Genetic Screening (PGS) technology to ensure healthy offspring. Expanding genetic counseling services are supporting awareness and adoption. Advances in molecular diagnostics are improving detection of single-gene disorders. In addition, growing emphasis on preventive reproductive healthcare is accelerating segment growth globally.

Preimplantation Genetic Screening (PGS) Technology Market Regional Analysis

- North America dominated the Preimplantation Genetic Screening (PGS) technology market with the largest revenue share of 41.6% in 2025, supported by advanced fertility clinic infrastructure, high adoption of IVF procedures, strong clinical expertise, and the presence of leading reproductive genetics providers

- Consumers and healthcare providers in the region highly value the clinical accuracy, improved implantation success rates, and reduced risk of genetic disorders offered by Preimplantation Genetic Screening (PGS) technology in assisted reproduction

- This widespread adoption is further supported by well-established fertility clinic infrastructure, strong presence of leading genetic testing companies, and high healthcare expenditure, making PGS a standard component of advanced reproductive care in both residential and clinical fertility services

U.S. Preimplantation Genetic Screening (PGS) Technology Market Insight

The U.S. Preimplantation Genetic Screening (PGS) Technology market captured the largest revenue share of 81% within North America in 2025, driven by rapid adoption of advanced IVF procedures and strong demand for genetic screening in fertility treatments. Consumers and healthcare providers increasingly prioritize improved embryo selection outcomes, reduced genetic disorder risks, and higher implantation success rates. The market is further supported by widespread availability of advanced fertility clinics, strong reimbursement frameworks in select cases, and high healthcare spending. In addition, growing integration of AI-based embryo analysis and NGS technologies into IVF workflows is significantly accelerating market expansion across the country.

Europe Preimplantation Genetic Screening (PGS) Technology Market Insight

The Europe Preimplantation Genetic Screening (PGS) Technology market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by strong regulatory frameworks supporting reproductive health and increasing awareness of genetic disorder prevention. The rising prevalence of delayed pregnancies and infertility is further accelerating demand for PGS-enabled IVF treatments. European consumers and healthcare providers are increasingly adopting advanced genomic screening methods to improve embryo selection outcomes. In addition, the region’s emphasis on ethical medical practices and precision medicine is fostering structured adoption of Preimplantation Genetic Screening (PGS) technology across fertility clinics and hospitals.

U.K. Preimplantation Genetic Screening (PGS) Technology Market Insight

The U.K. Preimplantation Genetic Screening (PGS) Technology market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by increasing demand for assisted reproductive technologies and rising awareness of genetic disease prevention. Concerns related to infertility and delayed parenthood are encouraging greater use of IVF procedures supported by PGS testing. The country’s strong private fertility clinic network and advanced healthcare infrastructure are facilitating wider adoption. Furthermore, growing integration of genomic testing into fertility treatment pathways is enhancing clinical outcomes, supporting sustained market growth in both public and private healthcare sectors.

Germany Preimplantation Genetic Screening (PGS) Technology Market Insight

The Germany Preimplantation Genetic Screening (PGS) Technology market is expected to expand at a considerable CAGR during the forecast period, fueled by strong focus on precision medicine and increasing awareness of reproductive genetic health. Germany’s advanced healthcare infrastructure and high investment in biotechnology are supporting adoption of sophisticated embryo screening techniques. The demand for ethically guided and highly accurate reproductive solutions is encouraging the use of Preimplantation Genetic Screening (PGS) technology in fertility centers. In addition, integration of NGS-based screening platforms with IVF workflows is further strengthening market growth across clinical applications.

Asia-Pacific Preimplantation Genetic Screening (PGS) Technology Market Insight

The Asia-Pacific Preimplantation Genetic Screening (PGS) Technology market is poised to grow at the fastest CAGR of 23.8% during the forecast period of 2026 to 2033, driven by rising infertility rates, increasing disposable incomes, and expanding access to IVF treatments in countries such as China, India, and Japan. The region’s growing preference for advanced reproductive healthcare solutions is significantly boosting adoption of genetic screening technologies. Government initiatives supporting healthcare modernization and fertility treatments are further accelerating market penetration. In addition, the expansion of fertility clinics and medical tourism is making Preimplantation Genetic Screening (PGS) technology more accessible and affordable across the region.

Japan Preimplantation Genetic Screening (PGS) Technology Market Insight

The Japan Preimplantation Genetic Screening (PGS) Technology market is gaining momentum due to its highly advanced healthcare system, aging population, and increasing demand for fertility treatments. The country’s strong emphasis on technological innovation is driving adoption of NGS-based embryo screening methods. Rising cases of late pregnancies are further increasing reliance on IVF procedures supported by genetic screening. In addition, integration of Preimplantation Genetic Screening (PGS) technology with AI-enabled reproductive platforms is improving embryo selection accuracy, supporting better clinical outcomes in both hospital and specialized fertility clinic settings.

India Preimplantation Genetic Screening (PGS) Technology Market Insight

The India Preimplantation Genetic Screening (PGS) Technology market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to rapid urbanization, growing infertility awareness, and expanding access to affordable IVF treatments. India is emerging as a key hub for fertility tourism, significantly increasing demand for advanced genetic screening solutions. Rising middle-class income levels and improving healthcare infrastructure are further supporting adoption. In addition, the presence of cost-effective domestic fertility clinics and increasing awareness of genetic disorder prevention are driving strong growth of Preimplantation Genetic Screening (PGS) technology across the country.

Preimplantation Genetic Screening (PGS) Technology Market Share

The Preimplantation Genetic Screening (PGS) Technology industry is primarily led by well-established companies, including:

- Illumina, Inc. (U.S.)

- Thermo Fisher Scientific Inc. (U.S.)

- F. Hoffmann-La Roche AG (Switzerland)

- Agilent Technologies, Inc. (U.S.)

- Natera, Inc. (U.S.)

- CooperSurgical, Inc. (U.S.)

- PerkinElmer Inc. (U.S.)

- Quest Diagnostics Incorporated (U.S.)

- Labcorp (U.S.)

- Genea Limited (Australia)

- Igenomix S.L. (Spain)

- Igenomix USA LLC (U.S.)

- BGI Genomics Co., Ltd. (China)

- Fulgent Genetics, Inc. (U.S.)

- Invitae Corporation (U.S.)

- Reprogenetics LLC (U.S.)

- Genesis Genetics (U.S.)

- CooperGenomics (U.S.)

- Juno Genetics (U.S.)

- Genomic Prediction Inc. (U.S.)

What are the Recent Developments in Global Preimplantation Genetic Screening (PGS) Technology Market?

- In April 2026, GenEmbryomics and Genomic Prediction announced the launch of XGEN PGT-X™, a low-cost clinical-grade embryo genome sequencing platform for Preimplantation Genetic Screening (PGS) technology, aimed at making comprehensive embryo genetic testing more accessible for IVF patients globally. The platform significantly reduces per-embryo testing costs while enabling high-resolution chromosomal screening, expanding the clinical reach of advanced reproductive genetics

- In February 2026, Illumina launched TruPath Genome, an advanced sequencing system designed to enhance genomic analysis accuracy, supporting reproductive genetics workflows including Preimplantation Genetic Screening (PGS) technology applications. The platform improves detection of rare and complex genetic variations, strengthening embryo evaluation precision in IVF laboratories

- In October 2025, GeneDx began piloting Illumina’s Constellation mapped read technology, which improves structural variant detection and genomic resolution in complex DNA analysis, indirectly enhancing Preimplantation Genetic Screening (PGS) technology workflows used in reproductive genetics. This advancement supports better embryo assessment by increasing sensitivity in identifying clinically relevant genomic changes

- In June 2025, Juniper Genomics officially launched its whole-genome and transcriptome embryo screening platform for Preimplantation Genetic Screening (PGS) technology, introducing a new clinical standard for IVF genetic testing aimed at improving embryo selection accuracy and reducing IVF cycles. The platform integrates advanced genomic sequencing with reproductive medicine to deliver deeper embryo-level insights and improve reproductive decision-making outcomes

- In January 2025, Bionano Genomics reported a successful clinical application of optical genome mapping (OGM) in preimplantation genetic testing for structural rearrangements (PGT-SR), contributing to a healthy live birth outcome. This milestone demonstrated improved detection of chromosomal abnormalities that may be missed by conventional methods, strengthening the accuracy of Preimplantation Genetic Screening (PGS) technology in IVF procedures

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.