Global Pressure Relief Devices Market

Market Size in USD Billion

CAGR :

%

USD

3.97 Billion

USD

7.08 Billion

2025

2033

USD

3.97 Billion

USD

7.08 Billion

2025

2033

| 2026 –2033 | |

| USD 3.97 Billion | |

| USD 7.08 Billion | |

| % | |

|

Pressure Relief Devices Market Size

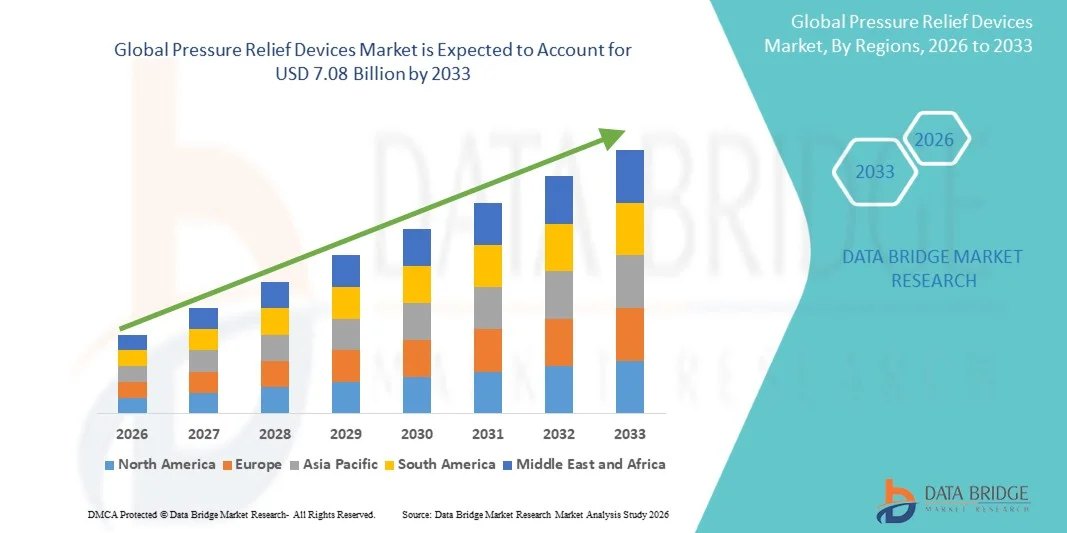

- The global pressure relief devices market size was valued at USD 3.97 billion in 2025and is expected to reach USD 7.08 billion by 2033, at a CAGR of 7.50% during the forecast period

- The market growth is largely fueled by the increasing prevalence of pressure ulcers (bedsores) among aging and immobile patient populations, along with rising hospital admissions and long-term care requirements, leading to greater demand for advanced wound care and pressure redistribution solutions

- Furthermore, growing emphasis on patient safety, hospital-acquired condition prevention, and improved critical care infrastructure, along with rising adoption of specialized mattresses, cushions, and support surfaces, is establishing Pressure Relief Devices as a key component of modern healthcare delivery. These converging factors are accelerating the uptake of Pressure Relief Devices solutions, thereby significantly boosting the industry's growth

Pressure Relief Devices Market Analysis

- Pressure relief devices, including alternating pressure mattresses, static air mattresses, gel cushions, foam-based support surfaces, and specialized heel protectors, are increasingly vital in modern healthcare settings such as hospitals, long-term care facilities, and home care environments due to their ability to reduce prolonged pressure, prevent pressure ulcers, and improve patient comfort and recovery outcomes

- The escalating demand for pressure relief devices is primarily fueled by the rising prevalence of chronic illnesses, growing geriatric population, increased ICU admissions, and heightened awareness regarding hospital-acquired pressure injuries, along with strong emphasis on improving patient safety and quality of care

- North America dominated the pressure relief devices market with the largest revenue share of 39.6% in 2025, driven by advanced healthcare infrastructure, high healthcare spending, strong adoption of preventive care technologies, and stringent patient safety regulations, with the U.S. accounting for the majority of product utilization across hospitals and long-term care facilities

- Asia-Pacific is expected to be the fastest growing region in the pressure relief devices market during the forecast period due to rapid aging population growth, expanding healthcare infrastructure, increasing hospital bed capacity, and rising awareness of pressure ulcer prevention across emerging economies such as China and India

- The Low-Tech Devices segment dominated the largest market revenue share of 57.6% in 2025, driven by their widespread use in cost-sensitive healthcare settings

Report Scope and Pressure Relief Devices Market Segmentation

|

Attributes |

Pressure Relief Devices Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

• Hill-Rom Holdings, Inc. (U.S.) |

|

Market Opportunities |

· Rising Demand from Aging Population and Long-Term Care Facilities · Technological Advancements in Smart and Dynamic Pressure Redistribution Systems |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Pressure Relief Devices Market Trends

“Enhanced Clinical Precision and Smart Patient Monitoring Integration”

- A significant and accelerating trend in the global Pressure Relief Devices market is the integration of digital health technologies, including AI-enabled pressure monitoring systems and smart hospital beds that support continuous patient data tracking. This convergence is significantly improving patient comfort, early risk detection, and clinical decision-making in long-term care settings

- For instance, hospitals in the U.S. and Europe are increasingly deploying smart pressure redistribution mattresses equipped with embedded sensors that continuously monitor patient movement and automatically adjust pressure distribution to reduce the risk of pressure ulcers in intensive care units

- AI integration in pressure relief devices enables predictive analytics that can identify patients at high risk of developing pressure injuries based on mobility patterns, hydration status, and historical clinical data. For instance, advanced hospital-grade support surfaces used in critical care units can now trigger early alerts to nursing staff when prolonged immobility is detected

- Furthermore, connected pressure relief systems are increasingly being integrated with hospital information systems (HIS) and electronic health records (EHR), allowing clinicians to track patient repositioning schedules and device performance in real time. This improves workflow efficiency and ensures adherence to pressure injury prevention protocols

- The growing adoption of smart hospital infrastructure is also enabling centralized monitoring of multiple beds across wards, allowing healthcare staff to remotely monitor patient risk levels and intervene proactively, thereby improving overall patient safety outcomes

Pressure Relief Devices Market Dynamics

Driver

“Rising Prevalence of Chronic Illnesses, Aging Population, and Hospital-Acquired Pressure Injury Prevention”

- The increasing global aging population, combined with a rising prevalence of chronic conditions such as diabetes, cardiovascular disease, and mobility impairments, is a major driver for the demand for pressure relief devices. Elderly and immobile patients are particularly vulnerable to pressure ulcers, necessitating advanced preventive care solutions

- For instance, long-term care facilities in Japan and Western Europe are increasingly adopting advanced alternating pressure mattresses and dynamic support surfaces to manage the growing elderly patient population requiring extended bed rest care

- Growing clinical emphasis on preventing hospital-acquired pressure injuries (HAPIs) is also driving adoption, as healthcare systems aim to reduce treatment costs and improve patient outcomes. For instance, hospitals participating in value-based care programs in the U.S. are increasingly investing in pressure-relieving beds to reduce penalty risks associated with preventable pressure ulcers

- In addition, rising awareness among healthcare providers regarding early-stage pressure injury prevention is encouraging the use of proactive support surfaces in ICUs, post-surgical wards, and long-term rehabilitation centers. For instance, rehabilitation hospitals are increasingly integrating pressure redistribution systems into standard post-operative recovery protocols to minimize complications

- Expansion of home healthcare services is further contributing to market growth, as patients requiring long-term immobility care are increasingly managed in home settings using advanced pressure relief mattresses and cushions designed for continuous use outside hospitals

Restraint/Challenge

“High Equipment Costs and Limited Accessibility in Resource-Constrained Healthcare Settings”

- Despite strong clinical benefits, the high cost of advanced pressure relief devices remains a significant barrier to adoption, particularly in low- and middle-income healthcare systems where budget allocation for supportive care equipment is limited

- For instance, smaller community hospitals and nursing homes in developing regions often continue using basic foam mattresses due to budget constraints, despite the availability of advanced alternating pressure systems

- Limited reimbursement coverage in several healthcare systems also restricts adoption, as pressure relief technologies are not uniformly classified under reimbursable medical equipment categories in many regions. For instance, patients in some healthcare systems must bear out-of-pocket expenses for specialized pressure-relieving support surfaces, limiting accessibility

- In addition, maintenance requirements, replacement of air pumps or sensor components, and training needs for caregivers increase the total cost of ownership, making advanced systems less attractive for smaller healthcare facilities

- Furthermore, lack of standardized procurement policies and unequal distribution of advanced medical infrastructure across rural and urban healthcare centers further restricts widespread deployment, slowing overall market penetration despite strong clinical demand

Pressure Relief Devices Market Scope

The market is segmented on the basis of devices, product, and end-users.

- By Devices

On the basis of devices, the Pressure Relief Devices market is segmented into Low-Tech Devices and High-Tech Devices. The Low-Tech Devices segment dominated the largest market revenue share of 57.6% in 2025, driven by their widespread use in cost-sensitive healthcare settings. These devices are extensively used in hospitals and long-term care facilities for preventing pressure ulcers in immobile patients. Their affordability and easy availability make them highly preferred in developing regions. Increasing geriatric population is further boosting demand. Hospitals prefer low-tech solutions for basic pressure redistribution needs. Growing awareness of hospital-acquired pressure injuries supports adoption. Ease of maintenance and low operational complexity enhance usage. These devices are widely used in home-care settings as well. Government healthcare programs in emerging economies are supporting procurement. Continuous demand from long-term care centers sustains dominance. Overall, they remain the most widely used segment globally.

The High-Tech Devices segment is expected to witness the fastest growth rate of 8.9% CAGR from 2026 to 2033, driven by increasing adoption of advanced patient care technologies. These devices offer dynamic pressure redistribution systems for improved clinical outcomes. Rising ICU admissions and critical care cases are boosting demand. Integration with smart monitoring systems enhances adoption in hospitals. Increasing healthcare infrastructure modernization supports growth. Higher effectiveness in preventing pressure ulcers drives clinical preference. Growing investments in advanced medical beds are accelerating adoption. Technological advancements are improving device efficiency and comfort. Rising awareness among healthcare providers is expanding usage. Demand is increasing in developed healthcare systems. Expansion of premium care facilities supports segment growth. Overall, it is the fastest-growing device category.

- By Product

On the basis of product, the Pressure Relief Devices market is segmented into Mattresses, Specialty Beds, and Mattress Overlays. The Mattresses segment dominated the largest market revenue share of 48.3% in 2025, driven by its extensive use in hospitals and long-term care facilities. Pressure-relief mattresses are widely used for bedridden patients to prevent pressure ulcers. Increasing hospital admissions and aging population are key demand drivers. Hospitals prefer mattresses due to cost-effectiveness and ease of use. Growing awareness of patient safety standards supports adoption. Rising cases of immobility-related complications boost usage. Availability of both foam and air-pressure variants expands application. Government healthcare guidelines encourage usage in critical care. Expanding home healthcare sector also supports demand. Continuous innovation in materials improves effectiveness. Strong procurement in public hospitals sustains dominance. Overall, mattresses remain the core revenue-generating product segment.

The Specialty Beds segment is expected to witness the fastest growth rate of 9.4% CAGR from 2026 to 2033, driven by increasing demand for advanced critical care solutions. These beds offer automated pressure redistribution and patient repositioning features. Rising ICU and emergency care admissions are boosting adoption. Hospitals are increasingly upgrading to intelligent bed systems. Higher effectiveness in preventing pressure ulcers is driving demand. Integration with digital monitoring systems supports clinical efficiency. Expanding healthcare infrastructure in developed regions supports growth. Increasing surgical procedures contribute to demand. Growing focus on patient comfort and safety enhances adoption. Technological advancements are improving product capabilities. Rising healthcare expenditure supports premium bed adoption. Overall, specialty beds represent the fastest-growing product segment.

- By End-Users

On the basis of end-users, the Pressure Relief Devices market is segmented into Hospitals, Long-Term Care Centers, Rehabilitation Centers, Geriatric Care Centers, Home-Based Centers, and Others. The Hospitals segment dominated the largest market revenue share of 44.1% in 2025, driven by high patient inflow and critical care requirements. Hospitals are the primary users of pressure relief devices for immobile and surgical patients. Rising incidence of pressure ulcers in acute care settings supports demand. Strong institutional procurement systems enhance adoption. Increasing ICU admissions globally drive usage. Government hospital funding supports large-scale deployment. Growing emphasis on patient safety standards boosts demand. Availability of advanced healthcare infrastructure strengthens usage. Continuous monitoring requirements increase device utilization. Training of healthcare professionals improves adoption rates. Expansion of hospital networks supports growth. Overall, hospitals remain the dominant end-user segment.

The Home-Based Centers segment is expected to witness the fastest growth rate of 9.1% CAGR from 2026 to 2033, driven by the rising trend of home healthcare services. Increasing aging population is boosting demand for home-based patient care. Growing preference for post-hospital recovery at home supports adoption. Technological advancements are making devices more user-friendly. Rising healthcare costs are shifting care toward home settings. Availability of portable pressure relief devices supports growth. Increasing caregiver support systems enhance usage. Government support for home healthcare is expanding access. Rising chronic disease prevalence increases demand. Growing awareness of pressure ulcer prevention at home boosts adoption. E-commerce distribution channels are improving accessibility. Overall, home-based care is emerging as a high-growth segment.

Pressure Relief Devices Market Regional Analysis

- North America dominated the pressure relief devices market with the largest revenue share of 39.6% in 2025, driven by advanced healthcare infrastructure, high healthcare expenditure, strong adoption of preventive care technologies, and stringent patient safety regulations. The region benefits from widespread use of pressure relief solutions across hospitals, long-term care facilities, and home healthcare settings, supported by increasing focus on reducing hospital-acquired pressure injuries and improving patient outcomes

- The growing prevalence of chronic illnesses, aging patient populations, and extended hospital stays has significantly increased the demand for advanced pressure relief systems, including specialized mattresses, cushions, and support surfaces designed to prevent pressure ulcers

- This widespread adoption is further supported by continuous product innovation, rising investments in hospital infrastructure, and increasing emphasis on patient-centric care models, establishing pressure relief devices as a critical component of modern healthcare delivery systems

U.S. Pressure Relief Devices Market Insight

The U.S. pressure relief devices market captured the largest revenue share within North America in 2025, driven by high hospitalization rates, strong healthcare spending, and widespread implementation of patient safety protocols across acute care and long-term care facilities. The country demonstrates strong adoption of advanced pressure redistribution technologies in hospitals, nursing homes, and rehabilitation centers. In addition, increasing regulatory focus on reducing hospital-acquired pressure injuries and improving quality of care metrics is further accelerating market growth in the U.S.

Europe Pressure Relief Devices Market Insight

The Europe pressure relief devices market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by rising geriatric population, increasing incidence of chronic diseases, and strong emphasis on improving hospital care quality standards. The region is witnessing growing adoption of pressure relief solutions across public and private healthcare facilities, supported by government initiatives focused on patient safety and long-term care improvements.

U.K. Pressure Relief Devices Market Insight

The U.K. pressure relief devices market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by increasing demand for long-term care services, rising elderly population, and strong focus on reducing pressure ulcer incidence within the National Health Service (NHS). The country is also witnessing growing investment in healthcare infrastructure and assistive medical technologies to improve patient mobility and comfort.

Germany Pressure Relief Devices Market Insight

The Germany pressure relief devices market is expected to expand at a considerable CAGR during the forecast period, fueled by strong hospital infrastructure, increasing elderly population, and high adoption of advanced medical support systems. Germany’s healthcare system emphasizes quality of inpatient care and prevention of secondary complications, supporting widespread use of pressure relief mattresses and support surfaces across healthcare facilities.

Asia-Pacific Pressure Relief Devices Market Insight

The Asia-Pacific pressure relief devices market is poised to grow at the fastest CAGR during the forecast period of 2026 to 2033, driven by rapid aging population growth, expanding healthcare infrastructure, increasing hospital bed capacity, and rising awareness of pressure ulcer prevention across emerging economies such as China and India. The region is also experiencing improvements in healthcare access and growing investments in hospital modernization, supporting broader adoption of pressure relief technologies.

Japan Pressure Relief Devices Market Insight

The Japan pressure relief devices market is gaining momentum due to the country’s rapidly aging population, advanced healthcare system, and strong focus on elderly care. Japan’s long-term care facilities and hospitals are increasingly adopting specialized pressure relief solutions to prevent bedsores and improve patient comfort, particularly among geriatric patients requiring prolonged care.

China Pressure Relief Devices Market Insight

The China pressure relief devices market accounted for the largest market revenue share in Asia Pacific in 2025, attributed to the country’s expanding healthcare infrastructure, rising hospitalization rates, and increasing awareness of patient safety and pressure ulcer prevention. China is witnessing strong adoption of advanced medical support surfaces in hospitals and elder care facilities, supported by healthcare system expansion and growing investments in clinical care quality improvements.

Pressure Relief Devices Market Share

The Pressure Relief Devices industry is primarily led by well-established companies, including:

• Hill-Rom Holdings, Inc. (U.S.)

• Stryker Corporation (U.S.)

• Invacare Corporation (U.S.)

• Arjo AB (Sweden)

• Drive DeVilbiss Healthcare (U.S.)

• EHOB, Inc. (U.S.)

• Talley Group Ltd (U.K.)

• Span-America Medical Systems (U.S.)

• Joerns Healthcare (U.S.)

• Mölnlycke Health Care (Sweden)

• Smith & Nephew plc (U.K.)

• Medline Industries, LP (U.S.)

• Baxter International Inc. (U.S.)

• Getinge AB (Sweden)

• Aircast Inc. (U.S.)

• Allegro Medical (U.S.)

• Cardinal Health, Inc. (U.S.)

• Ossur (Iceland)

• KCI Licensing, Inc. (Acelity) (U.S.)

• Paramount Bed Holdings Co., Ltd. (Japan)

Latest Developments in Global Pressure Relief Devices Market

- In March 2021, Arjo announced a strategic investment and partnership expansion with Bruin Biometrics, strengthening its portfolio in early pressure injury detection technologies such as the SEM Scanner, used for identifying tissue damage before visible pressure ulcers develop. This development reinforced the shift toward preventive, sensor-based pressure relief solutions in acute and long-term care settings

- In March 2021, Direct Healthcare Group completed the acquisition of Talley Group Ltd, expanding its portfolio of alternating pressure mattresses and therapeutic support surfaces designed for pressure ulcer prevention in hospitals, nursing homes, and homecare environments. This strengthened consolidation in the pressure relief devices market

- In September 2021, Dassiet introduced the UCAST splint system, an innovation aimed at improving immobilization outcomes while reducing localized pressure complications in orthopedic care. The system contributed to advancements in pressure redistribution during patient immobilization

- In August 2022, Arjo expanded its pressure injury prevention portfolio through continued integration of hospital bed systems and advanced therapeutic mattress technologies, strengthening its position in acute and critical care pressure relief solutions

- In August 2023, Arjo launched expanded deployment of its Citadel™ patient care system in U.S. healthcare facilities, combining integrated bed systems with pressure redistribution surfaces and patient monitoring capabilities to reduce hospital-acquired pressure injuries

- In March 2024, Getinge advanced its hospital infection control and sterile processing systems with next-generation washer-disinfectors, supporting improved patient safety workflows that indirectly enhance pressure injury prevention outcomes in clinical environments

- In June 2024, the global healthcare industry reported increased adoption of smart pressure-relieving mattresses and sensor-enabled hospital beds, integrating real-time pressure mapping and automated adjustment features to reduce pressure ulcer risks in immobile patients

- In September 2024, leading medical device manufacturers accelerated development of AI-enabled pressure injury prevention systems, combining sensor data, predictive analytics, and hospital monitoring platforms to proactively reduce pressure ulcer incidence in ICU and long-term care patient

- In May 2025, healthcare providers increasingly adopted connected smart beds and digital pressure monitoring systems, enabling continuous tracking of patient positioning and pressure distribution to reduce hospital-acquired pressure injuries and improve patient outcomes in critical care units

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.