Global Private Lte Market

Market Size in USD Billion

CAGR :

%

USD

4.34 Billion

USD

11.62 Billion

2025

2033

USD

4.34 Billion

USD

11.62 Billion

2025

2033

| 2026 –2033 | |

| USD 4.34 Billion | |

| USD 11.62 Billion | |

| % | |

|

What is the Global Private LTE Market Size and Growth Rate?

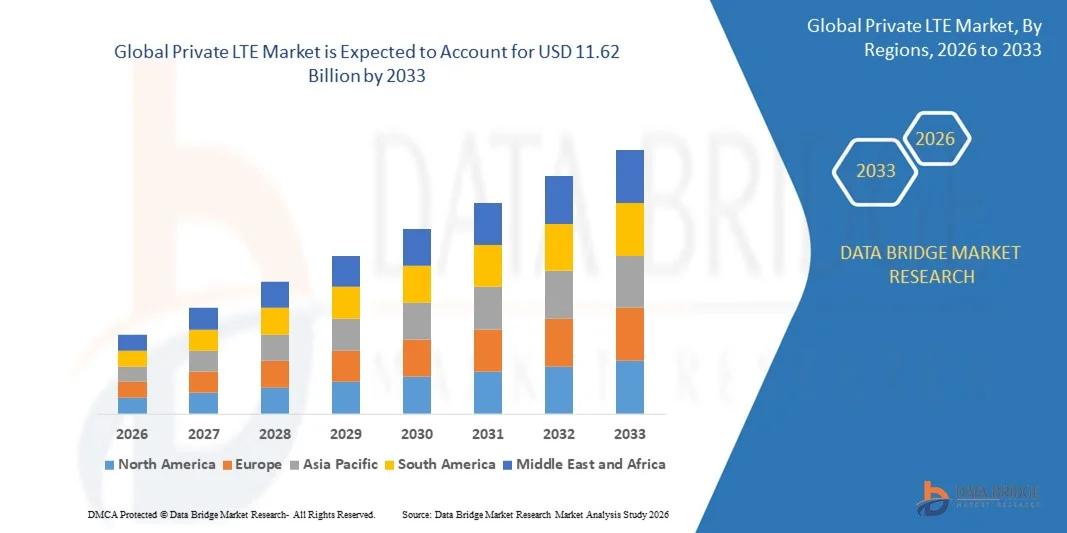

- The global Private LTE market size was valued at USD 4.34 billion in 2025 and is expected to reach USD 11.62 billion by 2033, at a CAGR of 13.10% during the forecast period

- The increase in the deployment of private LTE networks among public safety agencies acts as one of the major factors driving the growth of the private LTE market

- The rise in the adoption of private LTE networks allows the consumers to enhance situational awareness, obtain more accurate information, reduce response times and availability of unlicensed spectrums such as CBRS and MulteFire bands accelerate the market growth

What are the Major Takeaways of Private LTE Market?

- The increase in the deployment of private LTE networks by Emergency Service Provider Organizations (ESPOs) and public safety agencies to respond to emergencies effectively and deliver secure mission-critical voice, video, and data, and rise in demand for secured private networks with low latency and high operational efficiency at a reduced cost further influence the market

- In addition, an increase in the need for unique and defined network qualities, open networking model and infusion of the cloud and virtualization and digital transformation initiatives positively affect the private LTE market

- North America dominated the Private LTE market with a 43.2% revenue share in 2025, driven by early adoption of CBRS shared spectrum in the U.S., strong enterprise digital transformation initiatives, and rapid deployment of Industry 4.0 infrastructure across manufacturing, utilities, oil & gas, and logistics sectors

- Asia-Pacific is projected to register the fastest CAGR of 8.04% from 2026 to 2033, driven by rapid industrialization, expansion of smart manufacturing ecosystems, and strong telecom infrastructure development across China, Japan, India, South Korea, and Southeast Asia

- The Infrastructure segment dominated the market with a 68.5% share in 2025, driven by high investments in radio access networks (RAN), evolved packet core (EPC), small cells, routers, antennas, and edge computing hardware

Report Scope and Private LTE Market Segmentation

|

Attributes |

Private LTE Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

What is the Key Trend in the Private LTE Market?

Accelerating Adoption of Dedicated, Secure, and Industry-Specific Private LTE Networks

- The Private LTE market is witnessing strong adoption of dedicated cellular networks designed to provide secure, low-latency, and high-reliability connectivity for enterprises across manufacturing, energy, mining, ports, and smart campuses

- Vendors are introducing compact core network solutions, virtualized RAN architectures, and cloud-managed LTE platforms that enable flexible deployment and simplified network management

- Growing demand for mission-critical communication, industrial IoT connectivity, and real-time data transmission is transforming traditional Wi-Fi-dependent environments into LTE-based private networks

- For instance, companies such as Nokia, Telefonaktiebolaget LM Ericsson, Huawei Technologies Co., Ltd., and Samsung Electronics Co., Ltd. are expanding their private LTE portfolios with edge computing integration and industrial-grade network solutions

- Increasing spectrum allocation initiatives, including CBRS in the U.S., are accelerating enterprise-level LTE deployment

- As industries prioritize automation, predictive maintenance, and secure wireless infrastructure, Private LTE networks will remain vital for reliable and scalable enterprise connectivity

What are the Key Drivers of Private LTE Market?

- Rising demand for secure, high-bandwidth, and low-latency connectivity to support Industry 4.0, smart factories, autonomous vehicles, and remote asset monitoring is significantly driving market growth

- For instance, in 2025, leading companies such as Cisco Systems, Inc., ZTE Corporation, and NEC Corporation enhanced their private LTE offerings with cloud-native cores and edge computing capabilities

- Growing adoption of IoT devices, connected sensors, robotics, and automated guided vehicles (AGVs) across industrial environments is increasing the need for reliable cellular connectivity

- Advancements in virtualized network functions (VNF), software-defined networking (SDN), and open RAN technologies have strengthened deployment flexibility and cost efficiency

- Rising concerns over cybersecurity risks in public networks are encouraging enterprises to invest in dedicated private LTE infrastructure

- Supported by expanding enterprise digital transformation initiatives and favorable regulatory frameworks, the Private LTE market is expected to witness sustained long-term expansion

Which Factor is Challenging the Growth of the Private LTE Market?

- High costs associated with premium, high-bandwidth, and multi-channel logic analyzers restrict adoption among small engineering teams and academic institutions

- For instance, during 2024–2025, fluctuations in semiconductor component prices, specialized chip shortages, and longer lead times increased device manufacturing costs for several global vendors

- Complexity in analyzing high-speed digital protocols, mixed-signal systems, and advanced timing sequences increases the need for skilled engineers and training

- Limited awareness in emerging markets regarding logic analyzer capabilities, protocol support, and debugging best practices slows adoption

- Competition from digital oscilloscopes with built-in logic analyzer features (MSO), software debuggers, and protocol analyzers creates pricing pressure and reduces product differentiation

- To address these issues, companies are focusing on cost-optimized designs, training resources, cloud-based analytics, and higher software integration to increase global adoption of Private LTEs

How is the Private LTE Market Segmented?

The market is segmented on the basis of component, technology, deployment model, frequency band, and end user.

- By Component

On the basis of component, the Private LTE market is segmented into Infrastructure and Services. The Infrastructure segment dominated the market with a 68.5% share in 2025, driven by high investments in radio access networks (RAN), evolved packet core (EPC), small cells, routers, antennas, and edge computing hardware. Enterprises deploying private LTE prioritize ownership of dedicated physical infrastructure to ensure secure, low-latency, and high-reliability connectivity. Industrial facilities, ports, airports, and manufacturing plants are heavily investing in standalone LTE networks to support automation, IoT devices, and mission-critical communications.

The Services segment is expected to grow at the fastest CAGR from 2026 to 2033, supported by increasing demand for managed services, system integration, consulting, spectrum planning, and network maintenance. As private LTE networks become more complex, enterprises are increasingly outsourcing deployment and lifecycle management to specialized telecom solution providers.

- By Technology

On the basis of technology, the market is segmented into FDD and TDD. The FDD (Frequency Division Duplex) segment dominated the market with a 57.2% share in 2025, owing to its stable uplink and downlink separation, reliable coverage, and suitability for mission-critical industrial communication. FDD technology is widely deployed in utilities, oil & gas, and public safety networks where consistent performance is essential.

The TDD (Time Division Duplex) segment is projected to grow at the fastest CAGR from 2026 to 2033, driven by flexible spectrum utilization and higher data capacity advantages. Increasing deployment in smart manufacturing, high-density enterprise campuses, and shared spectrum environments is accelerating adoption of TDD-based private LTE solutions.

- By Deployment Model

On the basis of deployment model, the Private LTE market is segmented into Centralized and Distributed. The Centralized deployment segment dominated the market with a 60.4% share in 2025, supported by its simplified management, centralized core control, and cost-efficient architecture for large industrial sites and enterprise campuses. Organizations prefer centralized models for streamlined monitoring and secure data handling.

The Distributed deployment segment is expected to grow at the fastest CAGR from 2026 to 2033, driven by rising need for edge computing, ultra-low latency communication, and geographically dispersed industrial operations. Distributed architectures enable localized processing and enhanced network resilience in mining sites, smart cities, and logistics hubs.

- By Frequency Band

On the basis of frequency band, the market is segmented into Licensed, Unlicensed, and Shared Spectrum. The Licensed spectrum segment dominated the market with a 49.8% share in 2025, as enterprises prioritize secure and interference-free connectivity for mission-critical operations. Licensed bands provide higher reliability and predictable performance for utilities and defense applications.

The Shared spectrum segment is projected to grow at the fastest CAGR from 2026 to 2033, fueled by regulatory initiatives such as CBRS and increasing enterprise interest in cost-effective spectrum access models. Shared spectrum enables flexible deployment without full licensing costs.

- By End User

On the basis of end user, the Private LTE market is segmented into Utilities, Mining, Oil and Gas, Manufacturing, Transportation and Logistics, Government and Public Safety, Healthcare, and Others. The Manufacturing segment dominated the market with a 32.6% share in 2025, driven by Industry 4.0 adoption, robotics integration, predictive maintenance, and real-time asset tracking requirements.

The Government and Public Safety segment is expected to grow at the fastest CAGR from 2026 to 2033, propelled by rising demand for secure communication networks, disaster response coordination, and mission-critical connectivity solutions across smart city initiatives and national infrastructure projects.

Which Region Holds the Largest Share of the Private LTE Market?

- North America dominated the Private LTE market with a 43.2% revenue share in 2025, driven by early adoption of CBRS shared spectrum in the U.S., strong enterprise digital transformation initiatives, and rapid deployment of Industry 4.0 infrastructure across manufacturing, utilities, oil & gas, and logistics sectors. High demand for secure, low-latency wireless connectivity for mission-critical operations continues to accelerate private LTE adoption across industrial campuses and smart facilities

- Leading companies in North America are introducing cloud-native LTE cores, open RAN solutions, and edge-integrated private network platforms, strengthening the region’s technological leadership. Continuous investments in industrial IoT, smart grids, and autonomous systems further support long-term market growth

- Strong regulatory support, advanced telecom infrastructure, and high concentration of technology vendors reinforce North America’s dominant position in enterprise private LTE deployment

U.S. Private LTE Market Insight

The U.S. is the largest contributor in North America, supported by CBRS spectrum availability, expansion of smart manufacturing facilities, and increasing demand for secure wireless connectivity in defense and public safety networks. Enterprises across utilities, ports, airports, and large industrial campuses are deploying private LTE to ensure reliable communication, real-time monitoring, and enhanced cybersecurity. Growing adoption of edge computing, robotics, and automated guided vehicles further drives demand for dedicated LTE infrastructure nationwide.

Canada Private LTE Market Insight

Canada contributes significantly to regional growth, driven by rising investments in mining automation, energy infrastructure modernization, and remote industrial connectivity solutions. Enterprises are deploying private LTE networks to support IoT-based monitoring, predictive maintenance, and mission-critical communication in geographically dispersed locations. Government-backed digital innovation programs and expanding industrial automation initiatives further strengthen adoption across key sectors.

Asia-Pacific Private LTE Market

Asia-Pacific is projected to register the fastest CAGR of 8.04% from 2026 to 2033, driven by rapid industrialization, expansion of smart manufacturing ecosystems, and strong telecom infrastructure development across China, Japan, India, South Korea, and Southeast Asia. Increasing deployment of connected factories, autonomous transport systems, and smart city projects significantly boosts demand for secure private LTE networks. Rising spectrum reforms and enterprise mobility requirements further accelerate regional growth.

China Private LTE Market Insight

China is the largest contributor to Asia-Pacific due to extensive industrial automation initiatives, large-scale manufacturing hubs, and strong government support for digital infrastructure development. Rapid deployment of smart factories, logistics automation, and energy monitoring systems drives demand for high-capacity private LTE networks. Local telecom equipment manufacturers and competitive infrastructure costs further expand domestic adoption.

Japan Private LTE Market Insight

Japan demonstrates steady growth supported by advanced manufacturing systems, robotics integration, and modernization of industrial control networks. Enterprises prioritize secure and reliable wireless connectivity to enhance operational efficiency and real-time analytics capabilities. Strong focus on technological precision and industrial automation supports long-term private LTE expansion.

India Private LTE Market Insight

India is emerging as a key growth hub, driven by expanding smart manufacturing initiatives, digital transformation programs, and growing enterprise mobility requirements. Rising investments in industrial corridors, telecom infrastructure, and IoT-enabled operations accelerate private LTE adoption across manufacturing and logistics sectors. Government initiatives promoting digital infrastructure further strengthen market penetration.

South Korea Private LTE Market Insight

South Korea contributes significantly due to widespread 5G infrastructure development, strong semiconductor and electronics industries, and rapid industrial automation. Enterprises deploy private LTE to support robotics, AI-powered manufacturing systems, and smart logistics operations. Technological innovation and advanced digital ecosystems continue to drive sustained market growth.

Which are the Top Companies in Private LTE Market?

The Private LTE industry is primarily led by well-established companies, including:

- Nokia (Finland)

- Telefonaktiebolaget LM Ericsson (Sweden)

- Huawei Technologies Co., Ltd. (China)

- ZTE Corporation (China)

- NEC Corporation (Japan)

- Affirmed Networks (U.S.)

- Athonet srl (Italy)

- Redline Communications (Canada)

- Samsung Electronics Co., Ltd. (South Korea)

- Airspan Networks (U.S.)

- ASOCS (Israel)

- Boingo Wireless, Inc. (U.S.)

- Casa Systems (U.S.)

- Cisco Systems, Inc. (U.S.)

- Comba Telecom Systems Holdings Ltd. (Hong Kong)

- CommScope (U.S.)

- Druid Software (Ireland)

- ExteNet Systems (U.S.)

- FUJITSU (Japan)

- LEMKO Corporation (U.S.)

- Mavenir (U.S.)

- Quortus Limited (U.K.)

What are the Recent Developments in Global Private LTE Market?

- In April 2023, Nokia introduced an advanced private LTE solution tailored for the mining sector, delivering secure, high-reliability connectivity across remote and large-scale mining operations, thereby strengthening digital transformation and operational efficiency in isolated industrial environments

- In March 2023, Siemens acquired Industrial Communication Technologies (ICOM), a specialist in private LTE solutions for manufacturing applications, to expand its industrial networking portfolio and enhance its end-to-end automation and connectivity capabilities, reinforcing its position in smart factory infrastructure

- In January 2023, Verizon partnered with Microsoft to develop private LTE networks for manufacturing facilities, aiming to accelerate digital transformation initiatives and enable advanced automation use cases, ultimately supporting next-generation industrial innovation

- In August 2022, Cisco launched a private LTE solution designed for the transportation sector, enabling real-time fleet tracking and seamless vehicle-to-network communication, thereby improving operational visibility and transportation efficiency

- In June 2022, Honeywell unveiled a private LTE network solution for the oil and gas industry, ensuring secure and dependable connectivity for remote drilling and exploration sites, ultimately enhancing safety standards and operational reliability in energy infrastructure

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.