Global Proppant Market

Market Size in USD Billion

CAGR :

%

USD

10.95 Billion

USD

18.77 Billion

2025

2033

USD

10.95 Billion

USD

18.77 Billion

2025

2033

| 2026 –2033 | |

| USD 10.95 Billion | |

| USD 18.77 Billion | |

| % | |

|

Proppant Market Size

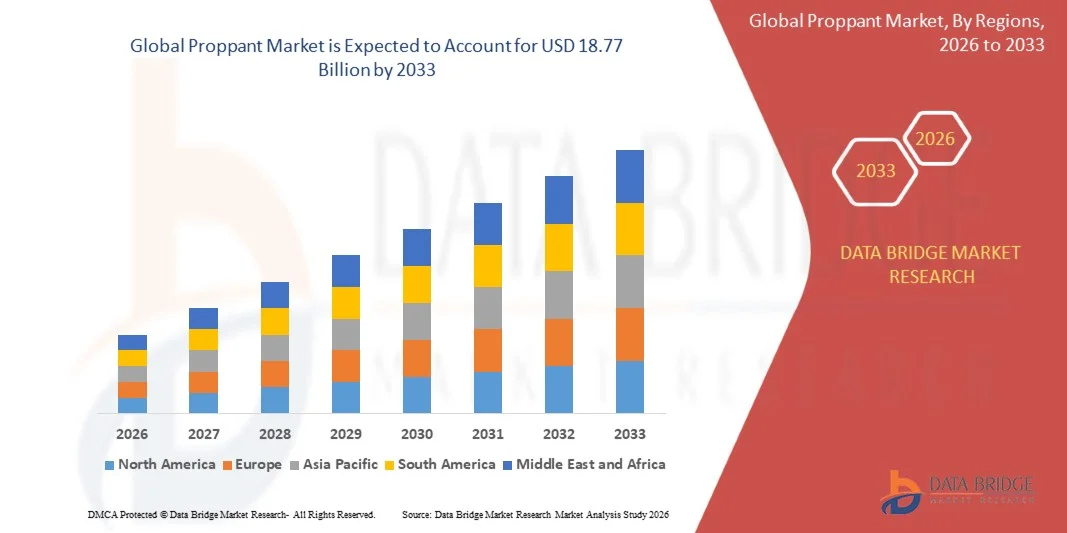

- The global proppant market size was valued at USD 10.95 billion in 2025 and is expected to reach USD 18.77 billion by 2033, at a CAGR of 6.97% during the forecast period

- The proppant market growth is largely driven by rising shale gas and tight oil exploration activities, where hydraulic fracturing techniques require large volumes of high-performance proppants to maintain fracture conductivity and improve hydrocarbon recovery efficiency

- Furthermore, increasing global energy demand and the shift toward unconventional oil and gas resources are accelerating drilling intensity, leading to higher consumption of silica sand, ceramic, and resin-coated proppants across major producing regions

Proppant Market Analysis

- Proppants, which are specialized materials such as silica sand, ceramic, and resin-coated particles used to keep induced fractures open in underground formations, are essential in hydraulic fracturing operations for enhancing oil and gas production from tight reservoirs

- The growing reliance on unconventional resource extraction, combined with continuous advancements in drilling technologies and well stimulation techniques, is significantly boosting the demand for high-strength and cost-efficient proppant materials across upstream oilfield operations

- North America dominated the proppant market with a share of 46% in 2025, due to extensive shale gas exploration and strong hydraulic fracturing activity across major basins such as Permian and Eagle Ford

- Asia-Pacific is expected to be the fastest growing region in the proppant market during the forecast period due to rising oil and gas exploration in China, India, and Australia. Expanding energy demand, rapid industrialization, and increasing investment in unconventional hydrocarbon resources are accelerating hydraulic fracturing activities

- Frac sand proppant segment dominated the market with a market share of 77.5% in 2025, due to its cost-effectiveness and widespread availability across major hydraulic fracturing operations. Its strong performance in maintaining fracture conductivity makes it highly preferred in shale and tight reservoir development. Oil and gas operators continue to rely on frac sand due to its established supply chain and ease of transportation

Report Scope and Proppant Market Segmentation

|

Attributes |

Proppant Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· CARBO Ceramics Inc. (U.S.) · Saint-Gobain (France) · U.S. Silica Holdings Inc. (U.S.) · JSC Borovichi Refractories Plant (Russia) · Superior Silica Sands (U.S.) · Hexion Inc. (U.S.) · Fores LTD (Russia) · Badger Mining Corporation (U.S.) · Smart Sand Inc. (U.S.) · ChangQing Proppant (China) · Eagle Materials Inc. (U.S.) · Baker Hughes (U.S.) · Halliburton (U.S.) · Wanli Proppant (China) · Momentive (U.S.) |

|

Market Opportunities |

· Expansion of Unconventional Oil and Gas Exploration in Emerging Economies · Development of Environmentally Sustainable and Recyclable Proppant Materials |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Proppant Market Trends

“Increasing Adoption of High-Performance Ceramic and Resin-Coated Proppants”

- A significant trend in the proppant market is the rising adoption of high-performance ceramic and resin-coated proppants, driven by the need to enhance fracture conductivity and improve hydrocarbon recovery in deep and ultra-deep unconventional reservoirs. This shift is strengthening the use of advanced proppant materials in complex hydraulic fracturing operations where durability and pressure resistance are critical

- For instance, CARBO Ceramics Inc. supplies engineered ceramic proppants that are widely used in high-pressure shale formations to improve long-term well productivity. Such products enhance fracture stability and support efficient extraction in challenging geological conditions

- The increasing focus on longer horizontal wells and multi-stage fracturing is accelerating demand for proppants that can withstand extreme downhole stress and maintain conductivity over extended production cycles. This is reinforcing the preference for premium-grade materials over conventional frac sand in several mature shale basins.

- Oilfield operators are increasingly integrating resin-coated proppants in applications requiring controlled flowback and improved sand control, which is enhancing operational efficiency and well integrity. This adoption is particularly relevant in reservoirs with high closure stress conditions

- Technological advancements in proppant design, including improved size uniformity and strength optimization, are supporting better placement within fracture networks. This is improving stimulation efficiency and increasing overall well performance across unconventional resources

- The trend is also being reinforced by growing investment in unconventional oil and gas development, where operators are prioritizing enhanced recovery techniques and maximizing reservoir contact. This is driving sustained demand for advanced proppant solutions globally

Proppant Market Dynamics

Driver

“Rising Hydraulic Fracturing Activities in Shale and Tight Oil Reservoirs”

- The proppant market is strongly driven by increasing hydraulic fracturing activities in shale and tight oil reservoirs, where proppants are essential for maintaining fracture openness and enabling efficient hydrocarbon flow. Expanding unconventional resource development is significantly boosting demand for both silica sand and advanced ceramic proppants

- For instance, Halliburton Company utilizes large-scale proppant volumes in hydraulic fracturing operations across major U.S. shale basins such as the Permian Basin to enhance production efficiency. These operations demonstrate the critical role of proppants in boosting well output from low-permeability formations

- The rising number of drilling and completion activities in unconventional reservoirs is increasing proppant intensity per well, particularly in multi-stage fracturing operations. This is resulting in sustained consumption growth across upstream oilfield services

- Growing energy demand and the shift toward domestic oil and gas production in several countries are encouraging operators to expand shale development programs. This is directly increasing hydraulic fracturing activity and supporting proppant market expansion

- The continuous expansion of shale gas production and tight oil extraction remains a key structural driver of the market, ensuring long-term demand for proppant materials across global energy markets

Restraint/Challenge

“Volatility in Raw Material Supply and Transportation Costs”

- The proppant market faces significant challenges due to volatility in raw material availability and transportation costs, particularly for silica sand and resin-coated materials used in hydraulic fracturing operations. These fluctuations directly impact production economics and supply chain stability

- For instance, U.S. Silica Holdings Inc. has experienced cost pressures due to fluctuating mining inputs and rising logistics expenses associated with transporting frac sand to major shale basins. These cost variations affect pricing stability across the proppant supply chain

- Dependence on region-specific raw materials creates supply bottlenecks, especially when demand surges in active drilling regions such as the Permian Basin. This leads to capacity constraints and increases procurement uncertainty for operators

- Transportation-intensive distribution models for proppants significantly raise operational costs, as large volumes of sand must be moved over long distances from production sites to well locations. This makes logistics a major cost component in overall project economics

- Overall, the combination of raw material price instability and high logistics dependency continues to constrain market profitability, requiring companies to optimize supply chains and enhance regional production strategies to maintain competitiveness

Proppant Market Scope

The market is segmented on the basis of type and application.

- By Type

On the basis of type, the proppant market is segmented into frac sand proppant, resin-coated proppant, and ceramic proppant. The frac sand segment dominated the market with the largest revenue share of 77.5% in 2025, driven by its cost-effectiveness and widespread availability across major hydraulic fracturing operations. Its strong performance in maintaining fracture conductivity makes it highly preferred in shale and tight reservoir development. Oil and gas operators continue to rely on frac sand due to its established supply chain and ease of transportation. Growing drilling activities in North America and other shale-rich regions further strengthen its dominant position in the market.

The ceramic proppant segment is anticipated to witness the fastest growth rate from 2026 to 2033, supported by increasing demand for high-strength materials in deep and ultra-deep well applications. Ceramic proppants offer superior crush resistance and conductivity under extreme pressure conditions compared to conventional alternatives. Their ability to enhance hydrocarbon recovery efficiency makes them highly suitable for complex geological formations. Rising investments in unconventional oil and gas exploration further support adoption. Continuous technological improvements in lightweight and high-performance ceramics are also accelerating segment expansion.

- By Application

On the basis of application, the proppant market is segmented into shale gas, tight gas, coal bed methane, and others. The shale gas segment dominated the market with the largest revenue share in 2025, driven by extensive hydraulic fracturing activities and high production output from shale reserves. Strong drilling investments in North America and expanding exploration projects in emerging regions reinforce its leadership. Shale formations require significant proppant volumes to maintain fracture networks and maximize gas recovery. The maturity of shale gas extraction technologies further supports sustained demand for proppants. Continuous development of horizontal drilling techniques also strengthens this segment’s dominance.

The coal bed methane segment is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing focus on cleaner energy sources and lower-carbon natural gas alternatives. CBM extraction requires specialized fracturing techniques that rely on efficient proppant placement for sustained gas flow. Expanding utilization of coal reserves for methane recovery in Asia-Pacific is contributing to rapid adoption. Government initiatives supporting unconventional gas development further enhance growth prospects. Advancements in extraction efficiency and reservoir management are also accelerating segment expansion.

Proppant Market Regional Analysis

- North America dominated the proppant market with the largest revenue share of 46% in 2025, driven by extensive shale gas exploration and strong hydraulic fracturing activity across major basins such as Permian and Eagle Ford

- The region benefits from high drilling intensity, advanced well completion technologies, and strong presence of oilfield service providers supporting large-scale proppant consumption in unconventional reservoirs

- Continuous investments in shale production, along with rising energy demand and well productivity optimization strategies, further strengthen proppant usage across both silica and resin-coated categories, reinforcing regional dominance

U.S. Proppant Market Insight

The U.S. proppant market captured the largest revenue share in North America in 2025, supported by its leadership in shale oil and gas production and extensive hydraulic fracturing operations. Operators increasingly rely on high-performance proppants to improve fracture conductivity and maximize hydrocarbon recovery from tight formations. The growing focus on longer lateral wells and multi-stage fracturing has significantly increased proppant intensity per well. In addition, technological advancements in frac design and increasing domestic energy production continue to drive strong market expansion.

Europe Proppant Market Insight

The Europe proppant market is projected to expand at a steady CAGR during the forecast period, driven by limited but technologically advanced shale and tight gas development activities. The region’s focus on energy security and reducing import dependence is encouraging selective exploration projects in countries with favorable geology. Environmental regulations remain strict, influencing controlled adoption of proppant-intensive extraction techniques. However, ongoing research in efficient drilling technologies and enhanced recovery methods supports gradual market growth across the region.

U.K. Proppant Market Insight

The U.K. proppant market is anticipated to grow at a moderate CAGR during the forecast period, supported by offshore oil and gas development activities in the North Sea. Operators are increasingly adopting hydraulic fracturing and well stimulation techniques to extend the life of mature fields. The demand for high-strength proppants is rising as drilling moves toward deeper and more complex reservoirs. Moreover, ongoing energy transition efforts are encouraging optimized extraction from existing assets, supporting steady proppant consumption.

Germany Proppant Market Insight

The Germany proppant market is expected to expand at a considerable CAGR during the forecast period, influenced by limited shale potential but strong emphasis on industrial energy efficiency and engineering innovation. While large-scale hydraulic fracturing remains restricted, proppant demand is supported through research-driven applications and adjacent well stimulation technologies. The country’s focus on advanced materials and precision drilling techniques is contributing to niche adoption. In addition, increasing demand for secure domestic energy solutions is supporting controlled exploration activities.

Asia-Pacific Proppant Market Insight

The Asia-Pacific proppant market is poised to grow at the fastest CAGR during the forecast period of 2026 to 2033, driven by rising oil and gas exploration in China, India, and Australia. Expanding energy demand, rapid industrialization, and increasing investment in unconventional hydrocarbon resources are accelerating hydraulic fracturing activities. The region is also witnessing growing domestic manufacturing of proppants, improving cost efficiency and availability. Furthermore, government initiatives to enhance energy self-sufficiency are supporting large-scale adoption across emerging economies.

China Proppant Market Insight

The China proppant market accounted for the largest revenue share in Asia Pacific in 2025, driven by aggressive shale gas development and strong government-backed energy expansion programs. Large-scale drilling projects in basins such as Sichuan and Tarim are significantly increasing proppant consumption. Domestic manufacturers are enhancing production capacity for high-quality silica and ceramic proppants to support growing demand. In addition, the country’s focus on energy independence and unconventional resource development continues to strengthen market growth.

Proppant Market Share

The proppant industry is primarily led by well-established companies, including:

- CARBO Ceramics Inc. (U.S.)

- Saint-Gobain (France)

- U.S. Silica Holdings Inc. (U.S.)

- JSC Borovichi Refractories Plant (Russia)

- Superior Silica Sands (U.S.)

- Hexion Inc. (U.S.)

- Fores LTD (Russia)

- Badger Mining Corporation (U.S.)

- Smart Sand Inc. (U.S.)

- ChangQing Proppant (China)

- Eagle Materials Inc. (U.S.)

- Baker Hughes (U.S.)

- Halliburton (U.S.)

- Wanli Proppant (China)

- Momentive (U.S.)

Latest Developments in Global Proppant Market

- In January 2025, CARBO Ceramics Inc. focused on expanding its advanced ceramic proppant portfolio to support high-pressure and deep shale formations, improving fracture conductivity and long-term well performance. The development strengthened the company’s position in high-value unconventional reservoirs by enabling more efficient hydrocarbon recovery and increasing adoption of premium proppant solutions among operators targeting complex geological formations.

- In October 2024, U.S. Silica Holdings Inc. enhanced its frac sand production and processing capabilities through targeted capacity optimization initiatives across its key manufacturing sites. This development improved operational efficiency, ensured a more consistent supply of high-quality silica sand proppants, and reduced dependency on long-haul logistics, thereby strengthening its competitiveness in major U.S. shale basins such as the Permian and Eagle Ford.

- In June 2024, Hi-Crush Inc. advanced its integrated logistics infrastructure by expanding in-basin storage terminals and streamlining proppant delivery systems for hydraulic fracturing operations. This improvement reduced transportation delays and operational downtime for oilfield service providers, while also lowering overall supply chain costs and enhancing real-time responsiveness to fluctuating proppant demand in active drilling regions.

- In February 2024, Atlas Energy Solutions Inc., a company specializing in renewable energy solutions, entered into an agreement with Hi Crush Inc. to acquire the latter’s North American logistics operations and proppant production assets, strengthening its supply chain control and expanding its market presence in proppant distribution, which significantly improved its ability to integrate production and logistics under a unified operating structure

- In May 2022, CARBO Ceramics Inc. announced the acquisition of Pinnacle Technologies Inc., which provides fracture diagnostic services, fracture mapping services, and fracture simulation models, enhancing its technical capabilities and strengthening its integrated offering in the proppants market by enabling better fracture design optimization and improved decision-making for hydraulic fracturing operations

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Proppant Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Proppant Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Proppant Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.