Global Pu Films Market

Market Size in USD Million

CAGR :

%

USD

827.75 Million

USD

1,723.39 Million

2025

2033

USD

827.75 Million

USD

1,723.39 Million

2025

2033

| 2026 –2033 | |

| USD 827.75 Million | |

| USD 1,723.39 Million | |

| % | |

|

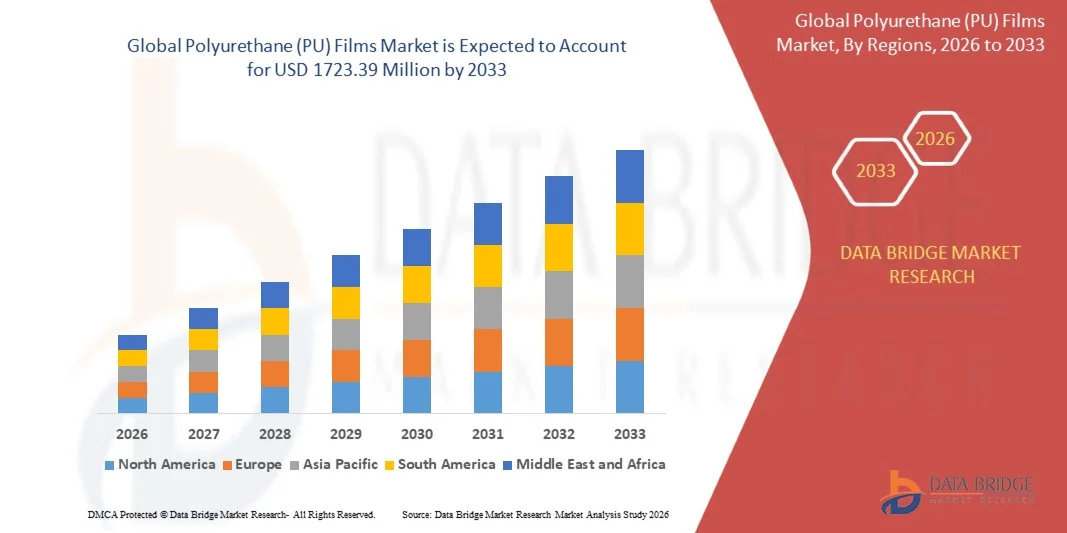

Polyurethane (PU) Films Market Size

- The global Polyurethane (PU) Films market size was valued at USD 827.75 million in 2025 and is expected to reach USD 1723.39 million by 2033, at a CAGR of 9.6% during the forecast period

- The market growth is largely fueled by rising demand for lightweight, durable, and high-performance polymer materials across automotive, aerospace, medical, and industrial applications, where polyurethane (PU) films offer superior abrasion resistance, flexibility, and protective functionality

- Furthermore, increasing adoption of advanced surface protection solutions, flexible packaging materials, and high-barrier films is strengthening demand, as industries prioritize enhanced product longevity, safety, and aesthetic appeal, thereby accelerating market expansion

Polyurethane (PU) Films Market Analysis

- Polyurethane (PU) films are flexible polymer-based materials known for their excellent elasticity, chemical resistance, transparency, and durability, making them suitable for protective coatings, medical applications, automotive interiors, and industrial uses

- The escalating demand for PU films is primarily driven by rapid expansion of automotive production, growing healthcare applications such as medical dressings and devices, and increasing use in protective and high-performance packaging solutions

- Asia-Pacific dominated the Polyurethane (PU) Films market with a share of 50.02% in 2025, due to rapid industrialization, strong manufacturing activity, and expanding demand from automotive, electronics, and healthcare sectors

- North America is expected to be the fastest growing region in the Polyurethane (PU) Films market during the forecast period due to strong demand from automotive, aerospace, and medical sectors, along with increasing use of high-performance protective materials

- Thermoplastic-based Polyurethane (PU) films segment dominated the market with a market share of 62.9% in 2025, due to its ease of processing, recyclability potential, and strong mechanical performance. These films are widely used in automotive interiors, consumer electronics, and packaging applications due to their versatility and cost-efficient production. Their ability to be reshaped under heat supports efficient manufacturing and design flexibility

Report Scope and Polyurethane (PU) Films Market Segmentation

|

Attributes |

Polyurethane (PU) Films Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Polyurethane (PU) Films Market Trends

“Growing Adoption of Sustainable and Bio-Based PU Films”

- A significant trend in the polyurethane (PU) films market is the rising shift toward sustainable and bio-based film solutions driven by increasing environmental regulations and the demand for low-carbon material alternatives across packaging, automotive, and consumer goods applications. Manufacturers are focusing on reducing dependency on petrochemical feedstocks while improving recyclability and lifecycle performance of PU films, which is strengthening the transition toward circular material systems in multiple industries

- For instance, Covestro has expanded its development of partially bio-based and CO₂-based polyurethane film materials used in coatings, automotive interiors, and flexible packaging applications. Similarly, BASF is advancing its biomass-balanced polyurethane portfolios that support reduced carbon footprint across industrial film applications, reinforcing the industry movement toward sustainable material innovation

- The adoption of eco-efficient PU films is increasing in packaging applications where brands are prioritizing reduced environmental impact without compromising barrier performance and flexibility. This is accelerating demand for advanced PU film formulations that maintain durability while supporting sustainability commitments across global supply chains

- The automotive sector is integrating sustainable PU films into interior surfaces, seating materials, and protective layers to align with emission reduction targets and green mobility initiatives. This is strengthening collaboration between material suppliers and automotive manufacturers to develop next-generation lightweight and environmentally responsible interior components

- Medical and hygiene industries are also adopting bio-based PU films for breathable and skin-compatible applications, supporting safer and more sustainable healthcare product development. This trend is encouraging innovation in biocompatible film structures with improved comfort and performance characteristics

- The market is witnessing continuous innovation in recyclable and solvent-free PU film production technologies that aim to reduce environmental impact during manufacturing and end-of-life disposal. This is reinforcing the long-term shift toward greener polyurethane material systems across global industrial sectors

Polyurethane (PU) Films Market Dynamics

Driver

“Rising Demand for Lightweight and Durable Materials”

- The increasing requirement for lightweight yet high-strength materials across automotive, electronics, packaging, and industrial sectors is driving the adoption of polyurethane films due to their superior flexibility, abrasion resistance, and mechanical durability. These properties enable manufacturers to reduce overall product weight while maintaining performance efficiency and structural integrity across diverse applications

- For instance, The Lubrizol Corporation supplies advanced TPU-based film materials widely used in automotive interiors, protective coatings, and consumer electronics applications where durability and lightweight performance are critical. These materials help manufacturers enhance product lifespan while improving design flexibility and functional efficiency

- The expansion of electric vehicle production is further strengthening demand for PU films as automakers prioritize weight reduction to improve battery efficiency and driving range. This is increasing the use of polyurethane films in interior trim, seating systems, and surface protection layers

- The packaging industry is adopting lightweight PU films to enhance material efficiency and reduce transportation costs while maintaining strong barrier properties. This is supporting the transition toward high-performance flexible packaging solutions across food, medical, and industrial packaging segments

- The growing need for multifunctional materials that combine strength, elasticity, and chemical resistance continues to strengthen this driver. This sustained demand is positioning polyurethane films as essential materials in next-generation lightweight engineering solutions across global industries

Restraint/Challenge

“High Raw Material Cost Volatility and Recyclability Limits”

- The polyurethane (PU) films market faces significant challenges due to fluctuations in raw material prices, particularly isocyanates such as MDI and TDI, which are derived from petrochemical feedstocks and are highly sensitive to crude oil price variations. This volatility increases production uncertainty and impacts cost stability for manufacturers across the supply chain

- For instance, Covestro and BASF, which are major producers of polyurethane intermediates, have experienced cost pressures linked to fluctuating feedstock prices and supply chain disruptions in global petrochemical markets. These variations directly affect pricing structures and profitability across downstream PU film applications

- The recyclability of polyurethane films remains limited due to complex polymer structures that are difficult to separate and reprocess efficiently, creating challenges for circular economy implementation. This restricts large-scale adoption of closed-loop recycling systems across PU film applications

- The disposal of PU-based materials continues to raise environmental concerns, particularly in regions with strict regulatory frameworks focused on plastic waste reduction. This is increasing pressure on manufacturers to develop alternative formulations and recycling-compatible material systems

- The combined impact of raw material volatility and recycling constraints continues to challenge market scalability. This is reinforcing the need for technological advancements in bio-based chemistry, process efficiency, and circular material development within the polyurethane films industry

Polyurethane (PU) Films Market Scope

The market is segmented on the basis of material, function, and end-user.

• By Material

On the basis of material, the polyurethane (PU) films market is segmented into polyester polyurethane (PU) films and polyether polyurethane (PU) films. The polyester polyurethane films segment dominated the largest market revenue share in 2025, driven by its superior mechanical strength, abrasion resistance, and high durability under demanding operating conditions. These films are widely preferred in applications requiring long-term structural stability, such as industrial coatings, automotive interiors, and protective layers. Strong resistance to wear and tear further supports their widespread adoption across end-use industries. The segment continues to lead due to its cost-effectiveness in high-volume manufacturing and consistent performance across diverse environments.

The polyether polyurethane films segment is anticipated to witness the fastest growth rate from 2026 to 2033, supported by its excellent hydrolysis resistance and flexibility in moisture-prone environments. This makes it highly suitable for medical applications, packaging solutions, and outdoor usage conditions where stability under humidity is critical. Growing demand for advanced medical-grade materials and high-performance protective films is accelerating adoption. In addition, increasing use in automotive and electronic applications requiring enhanced elasticity and environmental resistance is strengthening market expansion. The segment’s growth is further driven by its suitability for long-term performance in variable climatic conditions.

• By Function

On the basis of function, the polyurethane (PU) films market is segmented into thermoplastic-based polyurethane (PU) films and thermoset-based polyurethane (PU) films. The thermoplastic-based polyurethane films segment dominated the largest market revenue share of 62.9% in 2025, driven by its ease of processing, recyclability potential, and strong mechanical performance. These films are widely used in automotive interiors, consumer electronics, and packaging applications due to their versatility and cost-efficient production. Their ability to be reshaped under heat supports efficient manufacturing and design flexibility. The segment also benefits from increasing industrial demand for sustainable and high-performance material solutions.

The thermoset-based polyurethane films segment is expected to witness the fastest growth rate from 2026 to 2033, supported by its superior thermal stability and chemical resistance in extreme operating conditions. These films are increasingly used in aerospace, defense, and heavy industrial applications requiring long-term durability and structural integrity. Rising demand for advanced protective coatings and high-performance insulation materials is further accelerating adoption. In addition, their ability to maintain properties under continuous stress conditions supports their growing industrial relevance. The segment is expanding due to increasing investment in specialized engineering-grade materials.

• By End-User

On the basis of end-user, the polyurethane (PU) films market is segmented into automotive and aerospace, textile and leisure, medical, and others. The automotive and aerospace segment dominated the largest market revenue share in 2025, driven by strong demand for lightweight, durable, and protective materials used in interiors, coatings, and insulation systems. PU films are widely adopted in vehicle interiors and aircraft components due to their abrasion resistance and aesthetic finish. Growing emphasis on fuel efficiency and weight reduction further supports material substitution trends. The segment continues to lead due to expanding production of electric vehicles and advanced aerospace components.

The medical segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by increasing use of PU films in wound care products, surgical drapes, and medical device coverings. Rising demand for hygienic, flexible, and biocompatible materials is strengthening adoption in healthcare applications. In addition, the expansion of healthcare infrastructure and increasing surgical procedures are accelerating consumption of advanced medical films. Their breathability, comfort, and protective barrier properties enhance their suitability for clinical use. The segment’s growth is further supported by ongoing innovation in medical-grade polymer technologies.

Polyurethane (PU) Films Market Regional Analysis

- Asia-Pacific dominated the Polyurethane (PU) Films market with the largest revenue share of 50.02% in 2025, driven by rapid industrialization, strong manufacturing activity, and expanding demand from automotive, electronics, and healthcare sectors

- The region benefits from large-scale production capabilities, cost-efficient manufacturing ecosystems, and rising adoption of high-performance polymer materials

- Increasing investments in packaging, medical supplies, and industrial applications are further accelerating market expansion

China Polyurethane (PU) Films Market Insight

China held the largest share in the Asia-Pacific polyurethane (PU) films market in 2025, supported by its strong chemical manufacturing base, extensive automotive production, and large-scale industrial output. The country’s dominance is reinforced by high domestic demand for protective films in electronics, packaging, and automotive interiors. Continuous expansion of advanced manufacturing facilities and strong export capabilities are further strengthening market leadership.

India Polyurethane (PU) Films Market Insight

India is witnessing the fastest growth in the Asia-Pacific region, driven by rapid expansion in automotive manufacturing, increasing healthcare investments, and rising demand for flexible packaging solutions. Growth in domestic industrial production and supportive government initiatives for manufacturing and infrastructure development are further boosting consumption of PU films. Expanding medical device production and packaging industries are also contributing significantly to market acceleration.

Europe Polyurethane (PU) Films Market Insight

The Europe polyurethane (PU) films market is expanding steadily, supported by strong demand from automotive, aerospace, and medical applications, along with strict regulatory emphasis on high-performance and sustainable materials. The region benefits from advanced material innovation, well-established industrial infrastructure, and increasing adoption of specialty films in high-value applications. Growing focus on lightweight materials and environmental compliance is further supporting market growth.

Germany Polyurethane (PU) Films Market Insight

Germany accounted for the largest share in the Europe polyurethane (PU) films market in 2025, driven by its leadership in automotive manufacturing, advanced engineering capabilities, and strong industrial base. High demand for durable and high-performance films in vehicle interiors, machinery, and industrial coatings is supporting growth. Continuous innovation in material science and strong R&D investments further reinforce Germany’s dominant position.

U.K. Polyurethane (PU) Films Market Insight

The U.K. market is expanding steadily due to growing demand from medical, aerospace, and packaging industries, along with increasing focus on advanced polymer applications. Rising investments in healthcare infrastructure and sustainable material development are supporting adoption of PU films. Strong presence of research institutions and innovation-driven manufacturing is further contributing to market growth.

North America Polyurethane (PU) Films Market Insight

North America is projected to grow at the fastest CAGR from 2026 to 2033, driven by strong demand from automotive, aerospace, and medical sectors, along with increasing use of high-performance protective materials. Rising focus on lightweight materials, advanced manufacturing, and sustainable polymer solutions is further accelerating growth. Expansion of healthcare applications and packaging innovations is also strengthening market demand.

U.S. Polyurethane (PU) Films Market Insight

The U.S. held the largest share in the North America polyurethane (PU) films market in 2025, supported by its strong automotive and aerospace industries, advanced healthcare sector, and high adoption of innovative materials. The country’s leadership is reinforced by strong R&D capabilities, large-scale industrial production, and continuous investment in high-performance polymer technologies. Increasing demand for medical-grade films and protective industrial applications further supports its dominant position.

Polyurethane (PU) Films Market Share

The Polyurethane (PU) Films industry is primarily led by well-established companies, including:

- 3M (U.S.)

- Avery Dennison Corporation (U.S.)

- DingZing Advanced Materials Inc. (Taiwan)

- American Polyfilm Inc. (U.S.)

- SK Global Chemical Co. Ltd. (South Korea)

- TotalEnergies (France)

- GS Caltex India (India)

- Galp (Portugal)

- Marathon Petroleum Corporation (U.S.)

- Shell (U.K.)

- RTP Company (U.S.)

- Scorpion Coatings (U.S.)

- CITGO Petroleum Corporation (U.S.)

- Valero (U.S.)

Latest Developments in Global Polyurethane (PU) Films Market

- In December 2025, BASF expanded its thermoplastic polyurethane (TPU) film portfolio to support specialty industrial applications requiring superior chemical resistance and mechanical stability. This expansion reinforces BASF’s position in the PU films market by addressing growing industrial demand for durable films used in harsh operating conditions such as machinery protection, industrial coatings, and engineering applications. The improved performance characteristics enable broader substitution of conventional materials with TPU films, enhancing operational efficiency and product reliability. It also supports increasing industrial automation trends where long-lasting protective materials are essential for reducing maintenance costs and downtime

- In December 2025, BASF introduced new TPU film solutions targeting advanced apparel and protective applications with enhanced durability, elasticity, and processing efficiency. This launch strengthens the polyurethane (PU) films market by accelerating adoption in high-performance textiles, sportswear, and protective clothing where comfort and mechanical strength are critical. The improved elasticity and flexibility support better wearer comfort while maintaining protective functionality, making these films suitable for next-generation functional garments. Rising consumer preference for performance-oriented and durable apparel is further boosting demand, encouraging manufacturers to integrate TPU films into innovative textile designs

- In October 2025, Avery Dennison launched the Neo Matte Black polyurethane paint protection film, an 8.5-mil self-healing matte solution designed for premium automotive surface protection and long-term stain resistance. This development significantly enhances the polyurethane (PU) films market by expanding the application scope of high-performance films in the luxury automotive segment, where aesthetic appeal and durability are key purchasing factors. The self-healing functionality improves scratch resistance and extends product lifespan, increasing replacement cycles and value-added demand. It also strengthens the trend toward advanced surface protection systems in premium vehicles, supporting higher-margin product adoption among manufacturers and aftermarket service providers

- In May 2025, Covestro AG broadened its portfolio by introducing specialty thermoplastic polyurethane (TPU) films designed for enhanced security glazing applications. These films enable strong adhesion between multiple layers of glass, polycarbonate, or acrylic, resulting in highly durable and transparent laminates used in automotive and architectural safety systems. This development strengthens the PU films market by increasing demand for advanced safety and impact-resistant glazing solutions in both construction and transportation sectors. The improved structural integrity and optical clarity also support adoption in high-security environments, where resistance to breakage and transparency are equally important

- In January 2025, ADNOC completed its acquisition of Covestro AG, integrating upstream isocyanate production with downstream polyurethane film manufacturing to establish a vertically integrated value chain. This strategic move strengthens the polyurethane (PU) films market by improving supply chain stability, reducing dependency on external raw material pricing, and enhancing cost efficiency across production processes. The integration enables better control over feedstock availability, minimizing volatility risks and supporting consistent product output. It also positions the combined entity to accelerate innovation in PU film technologies through closer alignment between raw material development and downstream application needs

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Pu Films Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Pu Films Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Pu Films Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.