Global Pyoderma Gangrenosum Treatment Market

Market Size in USD Million

CAGR :

%

USD

312.62 Million

USD

472.55 Million

2025

2033

USD

312.62 Million

USD

472.55 Million

2025

2033

| 2026 - 2033 | |

| USD 312.62 Million | |

| USD 472.55 Million | |

| % | |

|

Pyoderma Gangrenosum Treatment Market Overview

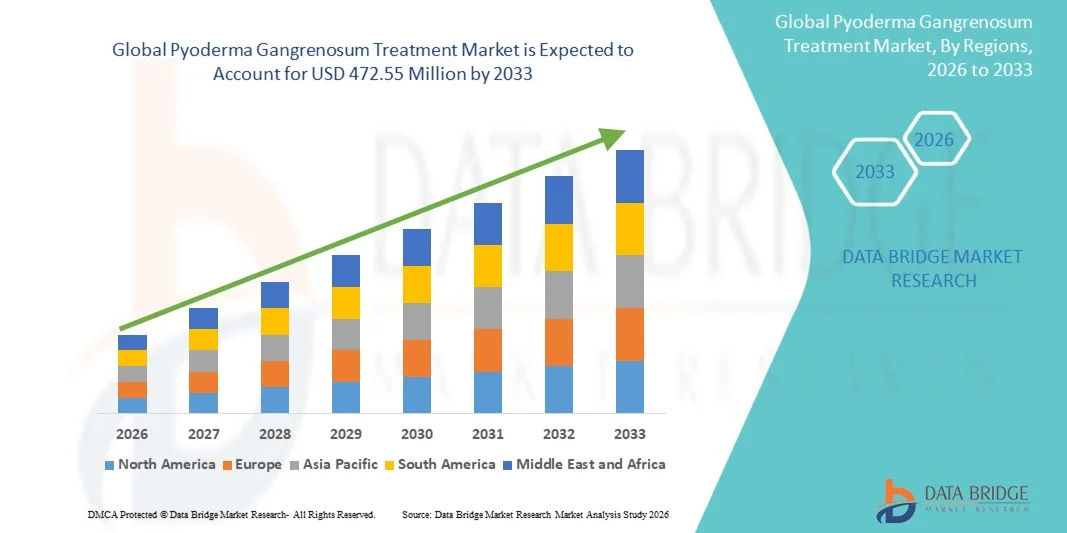

The Pyoderma Gangrenosum Treatment Market was valued at USD 312.62 million in 2025 and is projected to reach USD 472.55 million by 2033, growing at a CAGR of 5.30% from 2026 to 2033. The market is experiencing steady growth driven by rising prevalence of autoimmune and inflammatory conditions, increasing healthcare expenditure, and rapid advancements in biologic therapies. Growing awareness of rare dermatological disorders and rising initiatives by public and private organizations to improve diagnosis are further fueling expansion. The increasing adoption of targeted immunotherapies, rising demand for effective wound management solutions, and growing R&D activities focused on launching novel biologics are creating beneficial opportunities. In addition, the high unmet need for effective treatments and continuous developments in precision medicine are expected to escalate market growth over the forecast period.

The increasing prevalence of autoimmune conditions and immune system dysregulation, causing the body's defense mechanisms to attack healthy skin tissues, is primarily driving the pyoderma gangrenosum treatment market.

Key Market Trends & Insights

- North America dominated the Pyoderma Gangrenosum Treatment Market in 2025 with the largest revenue share of 41.84% in 2025, supported by advanced dermatology infrastructure, high healthcare expenditure, strong presence of specialized wound care centers, and robust government funding for autoimmune disorder research.

- Asia-Pacific is expected to be the fastest-growing regional market during the forecast period, driven by improving healthcare access, increasing awareness of rare inflammatory skin disorders, and expanding diagnostic capabilities.

- The Systemic Therapy segment led the market in 2025, accounting for 50.9% market share, owing to the frequent requirement for corticosteroids, immunosuppressants, and biologic therapies in severe cases.

- The Tumor Necrosis Factor Inhibitors segment is anticipated to be the fastest-growing drug class category, driven by rising adoption of targeted biologics and increasing emphasis on steroid-sparing treatment approaches.

- The Biopsy segment dominated the diagnosis category in 2025 with 45% market share, supported by its role as the primary method for ruling out other conditions and confirming inflammatory characteristics.

- The Pain segment accounted for the largest share of the symptoms category with approximately 35% market share, driven by the high prevalence of painful ulcerative lesions among patients with pyoderma gangrenosum.

- The Injection segment led the dosage category in 2025 with 40% market share, owing to widespread use of injectable corticosteroids and biologic therapies for managing severe manifestations.

- The Parenteral segment dominated the route of administration category with 42% market share, supported by its effectiveness in delivering systemic therapies for acute and refractory cases.

- The Hospital segment accounted for the largest share of the end-user category in 2025 with 55% market share, driven by multidisciplinary management requirements and access to specialized dermatology and wound care professionals.

Market Size & Forecast

- Global Market Value (2025): USD 312.62 Million

- Expected Market Value (2033): USD 472.55 Million

- Forecast CAGR (2026–2033): 5.30%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Pyoderma Gangrenosum Treatment Market Segmentation

|

Attributes |

Pyoderma Gangrenosum Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Johnson & Johnson Private Limited (U.S.) · AbbVie Inc. (U.S.) · Novartis AG (Switzerland) · Pfizer Inc. (U.S.) · Merck & Co., Inc. (U.S.) · GlaxoSmithKline plc (U.K.) · UCB S.A. (Belgium) · Amgen Inc. (U.S.) · Takeda Pharmaceutical Company Limited (Japan) · F. Hoffmann-La Roche Ltd. (Switzerland) · Aurobindo Pharma (India) · Apotex Inc. (Canada) · Cipla Inc. (India) · Sun Pharmaceutical Industries Ltd. (India) · AstraZeneca (U.K.) · Sanofi (France) · LEO Pharma A/S (Denmark) · Alexion Pharmaceuticals, Inc. (U.S.) · Swedish Orphan Biovitrum AB (Sweden) · Sumitomo Dainippon Pharma Co., Ltd. (Japan) |

|

Market Opportunities |

· Advancements in biologic therapies and precision medicine approaches for rare inflammatory skin disorders · Increasing investment in orphan drug development and autoimmune disease research programs |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Pyoderma Gangrenosum Treatment Market Trends

Trend: Growing Adoption of Biologic Therapies and Targeted Immunomodulators for Treatment

The increasing adoption of biologic therapies and targeted immunomodulators is emerging as a major trend in the Pyoderma Gangrenosum Treatment Market. Healthcare providers are increasingly utilizing advanced biologic agents to enable more effective disease control, reduce reliance on high-dose corticosteroids, and support personalized treatment strategies for patients with refractory or severe disease. The growing availability of tumor necrosis factor (TNF) inhibitors, interleukin inhibitors, and novel complement-targeting therapies is helping clinicians achieve better clinical outcomes while minimizing systemic side effects.

For instance,

In February 2025, IMARC Group reported that advancements in TNF inhibitors (adalimumab, infliximab), IL-1 and IL-17 inhibitors, and new complement inhibitors such as IFX-1 (vilobelimab) are changing treatment patterns towards precision medicine strategies, enhancing patient outcomes and minimizing reliance on high-dose corticosteroids.

In addition, the integration of artificial intelligence-based diagnostic tools, advanced wound care technologies, multimodal treatment protocols, and coordinated multispecialty care is enhancing treatment efficiency and supporting personalized care pathways for pyoderma gangrenosum. These advancements are improving clinical decision-making, accelerating wound healing, and strengthening the overall rare dermatological disease management ecosystem.

Pyoderma Gangrenosum Treatment Market Dynamics

Key Market Driver: Increasing Adoption of Targeted Biologic Therapies and Immunosuppressive Agents

The growing adoption of targeted biologic therapies and immunosuppressive agents is significantly driving the Pyoderma Gangrenosum Treatment Market. Healthcare providers are increasingly utilizing TNF inhibitors, calcineurin inhibitors, and other steroid-sparing medications to enable effective disease control, reduce corticosteroid-related side effects, and support long-term disease management. Rising awareness of autoimmune skin disorders, expanding access to specialty dermatology services, and increasing investments in precision medicine are further supporting market growth.

For instance,

In 2025, multiple pharmaceutical companies expanded their pipeline activities for biologic treatments targeting pyoderma gangrenosum, highlighting the increasing global focus on improving treatment outcomes through advanced immunotherapy approaches.

Key Restraint/Challenge: Limited Diagnostic Biomarkers and High Treatment Costs

A major challenge in the Pyoderma Gangrenosum Treatment Market is the absence of definitive diagnostic biomarkers and the high cost of advanced biologic therapies required for effective management. Limited disease awareness among healthcare providers and delayed diagnosis further restrict treatment adoption and market growth.

For instance,

In 2025, clinical guidelines continued to emphasize the diagnostic challenges associated with pyoderma gangrenosum, highlighting the persistent need for improved diagnostic criteria and broader access to specialized dermatological services.

Key Market Opportunity: Advancements in Wound Care Technologies and Multimodal Treatment Protocols

The growing adoption of advanced wound care technologies, negative pressure wound therapy, and multimodal treatment protocols presents significant opportunities for the market. Increasing investments in autoimmune disease research and coordinated multispecialty care approaches are expected to improve wound healing, personalized treatment strategies, and long-term patient management worldwide.

For instance,

In 2025, a case report published in Foot & Ankle Surgery: Techniques, Reports & Cases demonstrated that a structured multimodal protocol integrating patient education, coordinated multispecialty care, conservative debridement, split-thickness skin grafting, and negative pressure wound therapy achieved complete healing in a decade-long refractory case of pyoderma gangrenosum.

Pyoderma Gangrenosum Treatment Market Scope

The pyoderma gangrenosum treatment market is segmented on the basis of treatment, drug class, diagnosis, symptoms, dosage, route of administration, end-users, and distribution channel.

By Treatment

On the basis of treatment, the Pyoderma Gangrenosum Treatment Market is segmented into systemic therapy, topical therapy, surgery, and others. The systemic therapy segment dominated the market in 2025 with 50.9% market share due to the frequent requirement for corticosteroids, immunosuppressants, and biologic therapies in severe and refractory cases. The widespread use of oral and injectable systemic agents for managing acute flare-ups and preventing disease progression further supports segment dominance.

The topical therapy segment is expected to witness steady growth from 2026 to 2033, driven by increasing use of topical corticosteroids and calcineurin inhibitors for localized or mild disease. Rising patient preference for non-invasive treatment options and expanding availability of advanced topical formulations are further contributing to segment growth.

By Drug Class

On the basis of drug class, the Pyoderma Gangrenosum Treatment Market is segmented into immunosuppressive drugs, tumor necrosis factor inhibitors, and antibacterial agents. The immunosuppressive drugs segment dominated the market in 2025 with 45% market share due to widespread use of cyclosporine, mycophenolate, and dapsone as first-line or steroid-sparing therapies.

The tumor necrosis factor inhibitors segment is expected to witness the fastest growth from 2026 to 2033, driven by rising adoption of infliximab, adalimumab, and other biologic agents for treatment-resistant cases. Increasing clinical evidence supporting biologic efficacy, expanding indications, and growing emphasis on precision medicine approaches are further supporting segment growth.

By Diagnosis

On the basis of diagnosis, the Pyoderma Gangrenosum Treatment Market is segmented into biopsy, blood test, swab test, and others. The biopsy segment dominated the market in 2025 with 45% market share due to its role as the primary method for ruling out other conditions and confirming the inflammatory nature of the disease.

The blood test segment is expected to witness steady growth from 2026 to 2033, driven by increasing utilization of laboratory investigations to identify underlying associated conditions and support differential diagnosis. Growing integration of comprehensive diagnostic workups and improved access to specialized dermatology services are further accelerating adoption.

By Symptoms

On the basis of symptoms, the Pyoderma Gangrenosum Treatment Market is segmented into tenderness, fever, pain, blisters, and others. The pain segment dominated the market in 2025 with 35% market share due to the high prevalence of painful ulcerative lesions among affected patients and the continued need for effective pain management during wound care.

The blisters segment is expected to witness steady growth from 2026 to 2033, driven by increasing emphasis on early intervention and wound healing optimization. Growing awareness of disease progression patterns and improved access to specialized wound care services are further supporting segment growth.

By Dosage

On the basis of dosage, the Pyoderma Gangrenosum Treatment Market is segmented into injection, tablets, ointments, and others. The injection segment dominated the market in 2025 with 40% market share due to widespread use of injectable corticosteroids and biologic therapies for managing severe and refractory manifestations. Their rapid onset of action and systemic therapeutic effect have contributed to widespread adoption among healthcare providers.

The tablets segment is expected to witness steady growth from 2026 to 2033, driven by increasing use of oral corticosteroids and immunosuppressants for long-term disease management. Rising patient preference for convenient oral administration and expanding availability of steroid-sparing oral therapies are further contributing to segment growth.

By Route of Administration

On the basis of route of administration, the Pyoderma Gangrenosum Treatment Market is segmented into oral, parenteral, topical, and others. The parenteral segment dominated the market in 2025 with 42% market share owing to its effectiveness in delivering systemic therapies for acute and refractory cases. Injectable formulations, including intravenous and subcutaneous biologics, are widely used to manage severe ulcerative manifestations associated with pyoderma gangrenosum.

The oral segment is expected to witness steady growth from 2026 to 2033, driven by increasing adoption of oral corticosteroids and immunosuppressive agents in hospital and outpatient settings. Growing use of oral therapies for long-term maintenance and improving patient compliance are expected to support segment growth.

By End-Users

On the basis of end-users, the Pyoderma Gangrenosum Treatment Market is segmented into clinic, hospital, and others. The hospital segment dominated the market in 2025 with 55% market share due to the multidisciplinary care requirements associated with the disease and the availability of specialized dermatologists, wound care professionals, and advanced diagnostic facilities. Hospitals play a critical role in the diagnosis, treatment, and long-term management of pyoderma gangrenosum by providing access to comprehensive care for complex and severe cases.

The clinic segment is expected to witness the fastest growth from 2026 to 2033, driven by improving access to outpatient dermatology and wound care services. Increasing availability of specialized dermatology clinics, shorter waiting times, cost-effective treatment options, and growing patient preference for convenient outpatient care are expected to support strong segment expansion during the forecast period.

By Distribution Channel

On the basis of distribution channel, the Pyoderma Gangrenosum Treatment Market is segmented into hospital pharmacy, retail pharmacy, and online pharmacy. The hospital pharmacy segment dominated the market in 2025 with 50% market share due to the concentration of specialist-prescribed treatments within hospital settings. Hospital pharmacies serve as the primary distribution channel for medications used in the management of pyoderma gangrenosum, particularly for patients requiring specialized care and continuous medical supervision.

The online pharmacy segment is expected to witness the fastest growth from 2026 to 2033, driven by expanding digital healthcare platforms and increasing patient preference for convenient medication access. Growing internet penetration, rising adoption of e-pharmacy services, home delivery options, and improved availability of prescription medications through online channels are expected to support significant growth in this segment throughout the forecast period.

Pyoderma Gangrenosum Treatment Market Regional Analysis

North America dominated the pyoderma gangrenosum treatment market in 2025 with 40% market share, supported by advanced healthcare infrastructure, widespread availability of biologic therapies, strong dermatology and wound care research activities, and the presence of leading pharmaceutical and biotechnology companies. The region also benefits from high awareness of autoimmune skin disorders, favorable reimbursement frameworks, and increasing adoption of precision medicine approaches. Growing investments in targeted therapy research, specialty dermatology services, and specialized treatment centers continue to strengthen North America's leadership position in the global market.

U.S. Pyoderma Gangrenosum Treatment Market Insight

The U.S. pyoderma gangrenosum treatment market is witnessing steady growth due to increasing adoption of biologic therapies, rising awareness of rare inflammatory skin disorders, and expanding investments in precision medicine. The country's well-established healthcare system, strong research ecosystem, and availability of specialized dermatology and wound care treatment centers are supporting market expansion. In addition, growing focus on early diagnosis and personalized treatment strategies is improving patient outcomes and driving demand for advanced diagnostic and therapeutic solutions.

Europe Pyoderma Gangrenosum Treatment Market Insight

The Europe pyoderma gangrenosum treatment market remains a major contributor to global revenue with approximately 30% market share, driven by strong healthcare systems, increasing government support for rare disease management, and growing adoption of biologic therapies. The presence of specialized research institutions and collaborative rare disease networks is supporting advancements in diagnosis and treatment. Furthermore, favorable regulatory initiatives and increasing investments in immunology research continue to enhance market growth across the region.

U.K. Pyoderma Gangrenosum Treatment Market Insight

The U.K. pyoderma gangrenosum treatment market is experiencing steady growth, supported by increasing awareness of rare inflammatory skin disorders, expanding access to specialty dermatology services, and rising investments in autoimmune disease research programs. Growing integration of advanced biologic therapies and multidisciplinary treatment approaches is improving disease identification and management. In addition, ongoing research initiatives and support from healthcare organizations are contributing to market development.

Germany Pyoderma Gangrenosum Treatment Market Insight

The Germany pyoderma gangrenosum treatment market is expanding steadily due to the country's advanced healthcare infrastructure, strong focus on autoimmune disease research, and increasing adoption of targeted immunotherapy technologies. Healthcare providers are increasingly utilizing biologic agents and multidisciplinary treatment approaches to improve patient care. Continuous advancements in precision medicine and growing investments in specialized healthcare services are further supporting market growth in Germany.

Asia-Pacific Pyoderma Gangrenosum Treatment Market Insight

The Asia-Pacific pyoderma gangrenosum treatment market is expected to witness rapid growth with a projected CAGR of 13.1%, driven by improving healthcare infrastructure, increasing awareness of rare inflammatory skin disorders, and expanding access to diagnostic and specialty dermatology services across countries such as China, India, and Japan. Growing investments in precision medicine, rising adoption of biologic therapies, and increasing government initiatives aimed at improving rare disease management are supporting regional market expansion.

Japan Pyoderma Gangrenosum Treatment Market Insight

The Japan pyoderma gangrenosum treatment market is witnessing consistent growth due to increasing investments in autoimmune disease research, advanced healthcare technologies, and rare dermatological disorder diagnostics. Healthcare institutions are increasingly adopting biologic therapies and personalized treatment approaches to improve disease management. Moreover, strong government support for rare disease research and innovation is further contributing to market growth.

China Pyoderma Gangrenosum Treatment Market Insight

The China pyoderma gangrenosum treatment market is growing rapidly, driven by expanding healthcare infrastructure, increasing adoption of biologic therapies, and rising awareness of rare inflammatory skin conditions. Growing investments in biotechnology research, precision medicine initiatives, and advanced diagnostic capabilities are significantly boosting market development. In addition, supportive healthcare reforms and increasing access to specialized medical services are positioning China as one of the fastest-growing markets for rare dermatological disease diagnostics and treatment.

Pyoderma Gangrenosum Treatment Market Share

The Pyoderma Gangrenosum Treatment industry is primarily led by well-established companies, including:

- Johnson & Johnson Private Limited (U.S.)

- AbbVie Inc. (U.S.)

- Novartis AG (Switzerland)

- Pfizer Inc. (U.S.)

- Merck & Co., Inc. (U.S.)

- GlaxoSmithKline plc (U.K.)

- UCB S.A. (Belgium)

- Amgen Inc. (U.S.)

- Takeda Pharmaceutical Company Limited (Japan)

- F. Hoffmann-La Roche Ltd. (Switzerland)

- Aurobindo Pharma (India)

- Apotex Inc. (Canada)

- Cipla Inc. (India)

- Sun Pharmaceutical Industries Ltd. (India)

- AstraZeneca (U.K.)

- Sanofi (France)

- LEO Pharma A/S (Denmark)

- Alexion Pharmaceuticals, Inc. (U.S.)

- Swedish Orphan Biovitrum AB (Sweden)

- Sumitomo Dainippon Pharma Co., Ltd. (Japan)

Latest Developments in Pyoderma Gangrenosum Treatment Market

- In 2025, a case report published in Foot & Ankle Surgery: Techniques, Reports & Cases demonstrated that a structured multimodal protocol—the Pyoderma Gangrenosum Precision Care Initiative—integrating patient education, coordinated multispecialty care, conservative debridement, split-thickness skin grafting, and negative pressure wound therapy achieved complete healing in a decade-long refractory case of pyoderma gangrenosum.

- In December 2024, Mayo Clinic updated its clinical guidance on pyoderma gangrenosum treatment, emphasizing the importance of early and correct diagnosis and the use of steroid-sparing immunosuppressive therapies including cyclosporine, mycophenolate, infliximab, and tacrolimus to minimize long-term corticosteroid side effects.

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.