Global Rapid Diagnostic Tests Rdt Market

Market Size in USD Billion

CAGR :

%

USD

54.75 Billion

USD

111.51 Billion

2025

2033

USD

54.75 Billion

USD

111.51 Billion

2025

2033

| 2026 –2033 | |

| USD 54.75 Billion | |

| USD 111.51 Billion | |

| % | |

|

Rapid Diagnostic Tests (RDT) Market Size

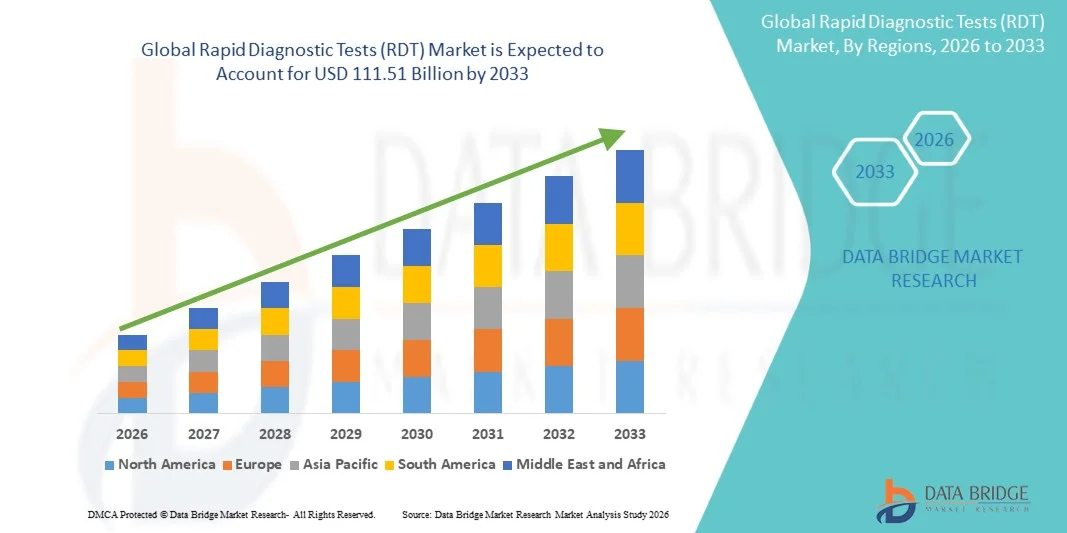

- The global Rapid Diagnostic Tests (RDT) market size was valued at USD 54.75 billion in 2025 and is expected to reach USD 111.51 billion by 2033, at a CAGR of 9.30% during the forecast period

- The market growth is largely fueled by the increasing demand for quick, accurate, and point-of-care diagnostic solutions, alongside advancements in immunoassay, molecular, and lateral flow technologies

- Furthermore, rising prevalence of infectious diseases, growing awareness of early disease detection, and the expansion of healthcare infrastructure in emerging markets are driving the adoption of RDTs across hospitals, clinics, and home-care settings. These converging factors are accelerating the uptake of rapid diagnostic solutions, thereby significantly boosting the industry's growth

Rapid Diagnostic Tests (RDT) Market Analysis

- Rapid Diagnostic Tests (RDT), providing quick and accurate detection of infectious diseases at point-of-care, are increasingly critical in both clinical and home settings due to their speed, ease of use, and minimal requirement for specialized equipment

- The growing demand for Rapid Diagnostic Tests (RDT) is primarily driven by rising prevalence of infectious diseases, increased focus on early diagnosis, and the need for cost-effective, decentralized testing solutions in hospitals, clinics, and remote areas

- North America dominated the Rapid Diagnostic Tests (RDT) market with the largest revenue share of 40.7% in 2025, supported by well-established healthcare infrastructure, high adoption of advanced diagnostic technologies, and strong presence of leading diagnostic companies, with the U.S. witnessing significant uptake in both hospital and at-home testing driven by innovations in multiplex assays and digital reporting

- Asia-Pacific is expected to be the fastest growing region in the Rapid Diagnostic Tests (RDT) market during the forecast period due to rising healthcare expenditure, expanding access to primary care, and increased government initiatives for infectious disease control

- Consumables and kits segment dominated the Rapid Diagnostic Tests (RDT) market with a market share of 47.3% in 2025, driven by their widespread use in infectious disease testing, glucose monitoring, pregnancy & fertility testing, and serological testing across hospitals, clinics, and home care settings

Report Scope and Rapid Diagnostic Tests (RDT) Market Segmentation

|

Attributes |

Rapid Diagnostic Tests (RDT) Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Rapid Diagnostic Tests (RDT) Market Trends

“Increasing Adoption of AI-Enabled and Digital Health-Integrated RDTs”

- A significant and accelerating trend in the global Rapid Diagnostic Tests (RDT) market is the integration with artificial intelligence (AI) and digital health platforms for enhanced accuracy, real-time reporting, and remote monitoring of test results

- For instance, Abbott’s BinaxNOW COVID-19 RDT integrates with mobile apps to deliver immediate results and track infection trends, enabling faster decision-making for patients and healthcare providers

- AI-powered RDT platforms enable predictive analytics, such as identifying disease hotspots and suggesting optimized testing strategies based on historical data. For instance, some Quidel Sofia RDTs use AI to enhance interpretation of test strips and reduce human error

- The integration with electronic health records (EHRs) and telemedicine platforms allows healthcare professionals to monitor patient results remotely, manage outbreaks, and provide timely guidance, creating a more connected and efficient diagnostic ecosystem

- This trend toward intelligent, digitally connected RDT solutions is reshaping user expectations for rapid, accurate, and actionable diagnostic results. Consequently, companies such as Roche Diagnostics are developing AI-enabled RDTs with cloud-based reporting and mobile app integration

- The demand for RDTs with AI and digital health integration is growing rapidly across hospitals, clinics, and home-care settings as healthcare providers and consumers prioritize speed, convenience, and data-driven decision-making

- There is also a growing trend toward multiplex RDTs capable of simultaneously detecting multiple pathogens, reducing testing time and improving diagnostic efficiency

Rapid Diagnostic Tests (RDT) Market Dynamics

Driver

“Rising Need for Quick and Accurate Point-of-Care Diagnostics”

- The increasing prevalence of infectious diseases and demand for rapid detection in hospitals, clinics, and remote locations is a significant driver for the adoption of Rapid Diagnostic Tests (RDT)

- For instance, in March 2025, Abbott Laboratories launched an expanded portfolio of RDTs for malaria and influenza to support timely diagnosis in high-burden regions, accelerating market growth

- RDTs provide rapid results, reduce laboratory dependence, and allow immediate treatment decisions, making them a preferred solution over conventional lab-based testing

- Furthermore, government screening programs, increased awareness of early detection, and initiatives for disease surveillance are boosting adoption across both public and private healthcare sectors

- The ease of use, portability, and low requirement for specialized training are key factors driving the widespread uptake of RDTs, especially in resource-limited settings, ensuring rapid and accurate disease management

- Technological advancements such as paper-based microfluidics and smartphone-enabled readouts are expanding accessibility and usability of RDTs in remote or low-resource areas

- For instance, LumiraDx’s portable RDT platform allows rapid detection of infectious diseases with digital readout capabilities, supporting on-the-go testing in clinics and field settings

Restraint/Challenge

“Regulatory Hurdles and Accuracy Limitations”

- Stringent regulatory approvals and quality control requirements for RDTs can slow down product launches and limit market penetration, posing a significant challenge for manufacturers

- For instance, delays in obtaining FDA or CE marking for new RDTs have impacted timely introduction of diagnostic solutions in key markets

- Variability in test sensitivity and specificity across different RDTs raises concerns about accuracy, particularly for low pathogen concentrations, which can limit clinician and consumer trust

- Addressing these challenges requires continuous validation, adherence to regulatory standards, and transparent reporting of test performance metrics to build confidence among healthcare providers and patients

- In addition, relatively high costs for multiplex or AI-integrated RDTs compared to basic rapid tests can hinder adoption in cost-sensitive regions, necessitating the development of affordable yet reliable diagnostic options for broader market growth

- Limited awareness and training among healthcare workers in some regions may reduce the effective utilization of RDTs, impacting market growth potential

- For instance, in rural areas of Southeast Asia and Africa, inadequate training on proper sample collection and test interpretation has occasionally led to inaccurate results, highlighting the need for educational initiatives alongside product deployment

Rapid Diagnostic Tests (RDT) Market Scope

The market is segmented on the basis of product type, mode, technology, modality, age group, test type, approach, specimen, application, end user, and distribution channel.

- By Product Type

On the basis of product type, the Rapid Diagnostic Tests (RDT) market is segmented into consumables and kits, instruments, and others. The consumables and kits segment dominated the market with the largest revenue share of 47.3% in 2025, driven by the extensive usage of test kits and reagents in hospitals, clinics, and home care settings. Consumables, including test strips, reagents, and sample collection devices, are crucial for the proper functioning of RDTs and are often required in repeated quantities, creating a consistent demand. The segment benefits from broad application across infectious disease testing, glucose monitoring, and pregnancy & fertility testing. Moreover, ease of distribution, affordability, and compatibility with multiple technologies such as lateral flow assays and PCR contribute to its dominance. Regulatory approvals and government initiatives for public health screening also reinforce the strong market position of consumables and kits.

The instruments segment is anticipated to witness the fastest growth from 2026 to 2033, driven by technological advancements in portable and automated diagnostic devices. Modern instruments enhance test accuracy, enable multiplexing, and integrate with digital health platforms for real-time reporting. Hospitals, diagnostic laboratories, and research institutes are increasingly adopting sophisticated RDT instruments to improve diagnostic efficiency and reduce turnaround times. The rising demand for point-of-care diagnostics and laboratory automation supports this growth. Instruments that support multiple specimen types, including blood, saliva, and swabs, further expand their utility across different test applications.

- By Mode

On the basis of mode, the RDT market is segmented into professional rapid diagnostic test products and over-the-counter (OTC) rapid diagnostic test products. The professional RDT product segment dominated the market in 2025 due to widespread use in hospitals, diagnostic laboratories, and clinics. Professional RDTs are preferred for their higher accuracy, comprehensive reporting, and ability to handle a wide range of specimens including blood, swabs, and urine. Healthcare providers rely on these products for timely decision-making, especially during infectious disease outbreaks. The professional segment also benefits from strong regulatory compliance and integration with electronic medical records (EMR) for streamlined patient management.

The OTC RDT product segment is expected to witness the fastest growth from 2026 to 2033, fueled by the rising trend of self-testing and home diagnostics. OTC products provide consumers with convenient, quick, and easy-to-use solutions for common infections, glucose monitoring, and pregnancy tests. Increasing awareness about early disease detection, coupled with smartphone-enabled digital result reporting, drives the popularity of OTC tests. Regulatory support for self-testing initiatives and growing e-commerce penetration further enhance market adoption.

- By Technology

On the basis of technology, the RDT market is segmented into PCR-based, flow-through assays, lateral flow immunochromatographic assays, agglutination assay, microfluidics, substrate technology, and others. The lateral flow immunochromatographic assay segment dominated the market in 2025 due to its simplicity, cost-effectiveness, and rapid results. This technology is widely used for infectious disease testing, pregnancy tests, and viral detection, offering portability and minimal equipment requirements. Its compatibility with home-based and point-of-care testing makes it a preferred choice across end users. Governments and healthcare programs favor lateral flow assays for large-scale screening due to ease of deployment and quick turnaround.

The microfluidics segment is expected to witness the fastest CAGR from 2026 to 2033, driven by innovations in lab-on-a-chip devices that provide high sensitivity, multiplex testing, and integration with digital platforms. Microfluidic RDTs allow miniaturization of sample handling, reduced reagent consumption, and faster diagnostics. Hospitals, research institutes, and advanced home-care settings increasingly adopt these devices for complex testing, including viral detection and serological studies. Advances in AI-enabled result interpretation and portable microfluidic devices further support rapid adoption.

- By Modality

On the basis of modality, the RDT market is segmented into laboratory-based tests and non-laboratory-based tests. The laboratory-based test segment dominated the market in 2025 due to the high accuracy, reproducibility, and extensive capabilities offered by centralized testing in hospitals and diagnostic laboratories. Laboratory-based RDTs support complex assays such as PCR, viral sequencing, and serological testing, which require controlled environments and specialized equipment. Hospitals and research institutes prefer this segment for large-scale testing and detailed diagnostic reporting. The integration of laboratory information systems (LIS) further streamlines data management and patient monitoring, reinforcing the dominance of this segment.

The non-laboratory-based test segment is expected to witness the fastest growth from 2026 to 2033, driven by the increasing adoption of point-of-care and home-based diagnostics. These tests provide rapid results for infectious disease detection, glucose monitoring, and pregnancy testing, enabling timely intervention outside traditional healthcare facilities. The convenience, portability, and user-friendliness of non-laboratory tests cater to self-testing trends and telemedicine adoption. Technological improvements in mobile-connected RDTs and miniaturized devices further accelerate growth in this segment.

- By Age Group

On the basis of age group, the RDT market is segmented into adult and pediatric. The adult segment dominated the market in 2025, owing to higher disease prevalence, routine health screenings, and workplace health monitoring. Adults often undergo infectious disease testing, glucose monitoring, and cardiometabolic evaluations, driving consistent demand for RDTs. Hospitals and clinics primarily target adult populations for preventive health programs and early disease detection initiatives. Moreover, regulatory approvals for adult RDTs are often faster, facilitating wider adoption.

The pediatric segment is expected to witness the fastest CAGR from 2026 to 2033, fueled by growing awareness for early diagnosis of infections and congenital conditions. Pediatric RDTs are increasingly used in hospitals, pediatric clinics, and community healthcare programs for diseases such as influenza, malaria, and RSV. Technological advancements have improved the accuracy of pediatric-friendly RDT devices, which require smaller sample volumes and less invasive specimen collection. Parental awareness and government immunization and screening programs further drive market growth.

- By Test Type

On the basis of test type, the RDT market is segmented into determining confirmation, serological testing, and viral sequencing. The determining confirmation segment dominated the market in 2025 due to widespread use in infectious disease diagnosis, including COVID-19, malaria, and HIV. These tests provide rapid, accurate results that guide treatment decisions, helping healthcare providers manage outbreaks effectively. The segment benefits from strong adoption in hospitals, diagnostic labs, and public health initiatives.

The viral sequencing segment is expected to witness the fastest growth from 2026 to 2033, driven by the rising need for pathogen surveillance, mutation tracking, and outbreak monitoring. Advanced RDT platforms now integrate viral sequencing capabilities to detect variants and inform epidemiological studies. Research institutes, hospitals, and government labs increasingly rely on viral sequencing for disease control strategies. Technological integration with AI and bioinformatics tools enhances the speed and accuracy of results, fueling adoption globally.

- By Approach

On the basis of approach, the RDT market is segmented into in-vitro diagnostics (IVD) and molecular diagnostics. The in-vitro diagnostics segment dominated the market in 2025 due to widespread application in hospitals, clinics, and home-care settings. IVD RDTs are commonly used for infectious disease detection, pregnancy testing, and glucose monitoring, offering rapid results with minimal infrastructure. The segment benefits from regulatory support and strong adoption in public health screening programs.

The molecular diagnostics segment is expected to witness the fastest CAGR from 2026 to 2033, driven by rising demand for highly accurate, PCR-based, and gene-targeted diagnostic tests. Molecular RDTs detect pathogens at very low concentrations, enabling early intervention and monitoring of disease outbreaks. The growing need for precision medicine, laboratory automation, and pathogen surveillance fuels market expansion in this segment.

- By Specimen

On the basis of specimen, the RDT market is segmented into swab, blood, urine, saliva, sputum, and others. The blood specimen segment dominated the market in 2025 due to its extensive application in infectious disease testing, glucose monitoring, serological assays, and cardiometabolic evaluations. Blood samples provide high accuracy, reliability, and versatility across multiple test types, making them the preferred choice in hospitals, clinics, and diagnostic laboratories. The segment benefits from standardized collection methods, widespread healthcare professional familiarity, and compatibility with both laboratory-based and point-of-care devices.

The swab specimen segment is expected to witness the fastest growth from 2026 to 2033, driven by the increasing prevalence of respiratory infections, COVID-19 testing, and other viral disease diagnostics. Swab-based RDTs allow rapid, minimally invasive collection for point-of-care testing and over-the-counter kits. Innovations in swab collection methods, integration with lateral flow assays, and real-time digital result reporting are boosting adoption. Rising awareness about self-testing and home diagnostics further fuels growth in this segment.

- By Application

On the basis of application, the RDT market is segmented into infectious disease testing, glucose monitoring, cardiology testing, oncology testing, cardiometabolic testing, drugs-of-abuse testing, pregnancy & fertility testing, toxicology testing, and others. The infectious disease testing segment dominated the market in 2025 due to high global demand for rapid detection of COVID-19, HIV, malaria, influenza, and other viral and bacterial infections. Hospitals, clinics, and public health organizations rely heavily on RDTs for quick diagnosis, outbreak management, and screening programs. Government initiatives and large-scale immunization and testing drives reinforce adoption in this segment.

The glucose monitoring segment is expected to witness the fastest growth from 2026 to 2033, fueled by increasing prevalence of diabetes, rising awareness about glycemic control, and adoption of home-care self-testing solutions. Glucose monitoring RDTs are convenient, portable, and compatible with digital health platforms for continuous monitoring and remote healthcare management. Technological advancements, affordability, and integration with smartphones and wearables further enhance segment growth.

- By End User

On the basis of end user, the RDT market is segmented into hospitals & clinics, diagnostic laboratories, home care settings, research and academic institutes, and others. The hospitals & clinics segment dominated the market in 2025 due to their high volume of diagnostic testing, wide access to trained personnel, and ability to handle laboratory-based and professional RDT products. Hospitals utilize RDTs for rapid disease confirmation, outbreak management, and patient triage. The segment is further supported by public health programs and partnerships with diagnostic companies for continuous supply of RDTs.

The home care settings segment is expected to witness the fastest growth from 2026 to 2033, driven by increasing consumer preference for self-testing, telemedicine adoption, and convenience of point-of-care testing. Home care RDTs enable early detection and monitoring of diseases such as diabetes, pregnancy, and common infections. Improved usability, digital integration, and awareness campaigns regarding self-care and preventive health are key factors supporting the rapid growth of this segment.

- By Distribution Channel

On the basis of distribution channel, the RDT market is segmented into direct tender, retail sales, and others. The direct tender segment dominated the market in 2025 due to bulk procurement by hospitals, government organizations, and diagnostic laboratories for large-scale testing and public health programs. Direct tender agreements ensure consistent supply, regulatory compliance, and often preferential pricing, making them the preferred channel for professional RDT products.

The retail sales segment is expected to witness the fastest growth from 2026 to 2033, fueled by the increasing availability of over-the-counter RDT products, rising e-commerce penetration, and growing consumer inclination toward self-testing. Retail sales channels provide easy access to pregnancy tests, glucose monitoring kits, and infectious disease RDTs for home use. Enhanced awareness of preventive health, coupled with digital platforms for ordering and result tracking, accelerates adoption through retail channels globally.

Rapid Diagnostic Tests (RDT) Market Regional Analysis

- North America dominated the Rapid Diagnostic Tests (RDT) market with the largest revenue share of 40.7% in 2025, supported by well-established healthcare infrastructure, high adoption of advanced diagnostic technologies, and strong presence of leading diagnostic companies

- Healthcare providers and consumers in the region highly value the speed, accuracy, and ease of use offered by RDTs, alongside seamless integration with digital health platforms and electronic medical records

- This widespread adoption is further supported by high healthcare expenditure, strong regulatory frameworks, and growing government initiatives for disease surveillance and early detection, establishing RDTs as a preferred diagnostic solution across hospitals, clinics, and home-care settings

U.S. Rapid Diagnostic Tests (RDT) Market Insight

The U.S. Rapid Diagnostic Tests (RDT) market captured the largest revenue share of 42% in 2025 within North America, fueled by the increasing demand for rapid, point-of-care diagnostics and well-established healthcare infrastructure. Healthcare providers and consumers are prioritizing faster disease detection, early intervention, and convenient testing solutions to manage both endemic and emerging diseases. The growing adoption of digital health platforms, telemedicine, and smartphone-enabled RDT devices further propels the market by enabling real-time result reporting and remote patient monitoring. Moreover, government initiatives for infectious disease surveillance, large-scale screening programs, and public awareness campaigns are significantly contributing to the market’s expansion, making RDTs an essential tool in the U.S. healthcare system.

Europe Rapid Diagnostic Tests (RDT) Market Insight

The Europe Rapid Diagnostic Tests (RDT) market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by rising incidence of infectious diseases and government-led screening programs. Increasing urbanization, modernization of healthcare facilities, and growing demand for efficient diagnostic tools are fostering the adoption of RDTs. European healthcare providers and laboratories are increasingly drawn to the convenience, speed, and accuracy of RDTs, which allow for rapid triage, patient management, and outbreak containment. The region is experiencing significant growth across hospitals, clinics, laboratories, and home-care settings, with RDTs being incorporated into both routine screenings and emergency diagnostics, further strengthening healthcare preparedness.

U.K. Rapid Diagnostic Tests (RDT) Market Insight

The U.K. Rapid Diagnostic Tests (RDT) market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by rising awareness of early disease detection, the need for efficient point-of-care diagnostics, and proactive public health initiatives. Increasing prevalence of infectious diseases and emphasis on reducing diagnostic turnaround times are encouraging widespread RDT adoption. The U.K.’s strong healthcare infrastructure, well-established laboratory networks, and digital health integration, alongside advancements in home-based testing solutions, are expected to continue stimulating market growth. In addition, government support for mass screening programs and early detection campaigns is further accelerating the adoption of RDTs in both clinical and community settings.

Germany Rapid Diagnostic Tests (RDT) Market Insight

The Germany Rapid Diagnostic Tests (RDT) market is expected to expand at a considerable CAGR during the forecast period, fueled by technological advancements and growing demand for accurate, rapid diagnostics across hospitals, clinics, and laboratories. Germany’s well-developed healthcare infrastructure, focus on preventive care, and strict regulatory standards ensure high-quality diagnostic practices, promoting the adoption of RDTs. Integration with electronic health records, telemedicine platforms, and AI-assisted diagnostic tools is becoming increasingly prevalent, with a strong preference for reliable, precise, and fast diagnostic solutions. In addition, Germany’s increasing investment in healthcare digitalization is further driving market growth by facilitating efficient testing workflows and rapid data-driven decision-making.

Asia-Pacific Rapid Diagnostic Tests (RDT) Market Insight

The Asia-Pacific Rapid Diagnostic Tests (RDT) market is poised to grow at the fastest CAGR of 23% during the forecast period of 2026 to 2033, driven by increasing urbanization, rising disposable incomes, expanding healthcare access, and technological advancements in countries such as China, Japan, and India. The region’s growing emphasis on point-of-care diagnostics, supported by government health initiatives, insurance coverage, and awareness campaigns, is driving the adoption of RDTs. Furthermore, APAC’s emergence as a manufacturing hub for diagnostic devices is enhancing the affordability and accessibility of RDTs to a wider population, including remote and underserved areas. The increasing penetration of mobile-based and portable RDT devices is further enabling timely diagnosis and treatment, significantly boosting market expansion.

Japan Rapid Diagnostic Tests (RDT) Market Insight

The Japan Rapid Diagnostic Tests (RDT) market is gaining momentum due to the country’s high healthcare standards, advanced technology adoption, and strong focus on preventive care. The Japanese market emphasizes rapid, reliable diagnostics, with RDT adoption driven by hospitals, clinics, and home-care services for both infectious and chronic diseases. Integration with digital health platforms, telemedicine, and smartphone-enabled testing is fueling growth by enabling seamless reporting and real-time monitoring. Moreover, Japan’s aging population is likely to spur demand for easy-to-use, accurate RDT solutions in residential, assisted-living, and clinical settings, creating opportunities for manufacturers to develop user-friendly and accessible devices tailored to senior citizens.

India Rapid Diagnostic Tests (RDT) Market Insight

The India Rapid Diagnostic Tests (RDT) market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to the country’s expanding healthcare infrastructure, rising disease awareness, and increasing adoption of point-of-care diagnostics. India is one of the largest markets for RDTs, with growing usage in hospitals, clinics, mobile testing units, and remote healthcare settings. Government initiatives promoting early disease detection, widespread health campaigns, and investment in smart health technologies are key factors propelling the market. In addition, the rise of domestic manufacturers offering affordable and reliable RDTs, along with increasing private-sector participation, is making rapid diagnostics more accessible to urban and rural populations alike, thereby significantly driving market growth.

Rapid Diagnostic Tests (RDT) Market Share

The Rapid Diagnostic Tests (RDT) industry is primarily led by well-established companies, including:

- Abbott (U.S.)

- Bio Rad Laboratories, Inc. (U.S.)

- BD (U.S.)

- F. Hoffmann La Roche Ltd (Switzerland)

- BIOMÉRIEUX (France)

- QIAGEN (Netherlands)

- Quidel Corporation (U.S.)

- Cepheid Inc (U.S.)

- Hologic Inc (U.S.)

- OraSure Technologies Inc (U.S.)

- Sekisui Diagnostics (U.S.)

- Trinity Biotech plc (Ireland)

- Siemens Healthineers AG (Germany)

- PerkinElmer Inc (U.S.)

- Nova Biomedical Corporation (U.S.)

- Access Bio Inc (U.S.)

- Chembio Diagnostics Systems Inc (U.S.)

- PTS Diagnostics (U.S.)

- Luminex Corporation (U.S.)

- Danaher (U.S.)

What are the Recent Developments in Global Rapid Diagnostic Tests (RDT) Market?

- In October 2025, the World Health Organization (WHO) launched the “Rapid diagnostic test accessibility considerations” publication to improve accessibility and equitable use of RDTs for both professional and self‑testing globally, emphasizing inclusion for persons with disabilities and marginalized populations

- In May 2025, WHO and Medicines Patent Pool (MPP) signed a sublicensing agreement enabling local production of RDT technology in Africa, with Nigerian firm Codix Bio to manufacture tests (starting with HIV RDTs) using technology transferred from SD Biosensor, expanding local diagnostic capacity

- In April 2024, a global deployment of more than 1.2 million cholera rapid diagnostic test kits was launched, coordinated by Gavi, WHO, UNICEF, and partners, to strengthen outbreak detection, surveillance, and response in 14 high‑risk countries

- In October 2021, the U.S. National Institutes of Health (NIH) expanded its RADx initiative by awarding contracts totaling USD 77.7 million for the development and manufacturing of 12 new rapid SARS‑CoV‑2 diagnostic tests (home and point‑of‑care), supporting innovation in multiplex and rapid detection

- In May 2021, DiaSorin launched new point‑of‑care rapid diagnostic tests on its LIAISON IQ platform, including both antibody and antigen tests for SARS‑CoV‑2, later receiving U.S. FDA Emergency Use Authorization for the antigen assay, broadening the range of rapid diagnostics available globally

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.