Global Ready Drink Tea Ready Drink Coffee Market

Market Size in USD Billion

CAGR :

%

USD

125.90 Billion

USD

211.69 Billion

2025

2033

USD

125.90 Billion

USD

211.69 Billion

2025

2033

| 2026 –2033 | |

| USD 125.90 Billion | |

| USD 211.69 Billion | |

| % | |

|

Ready to Drink Tea and Ready to Drink Coffee Market Size

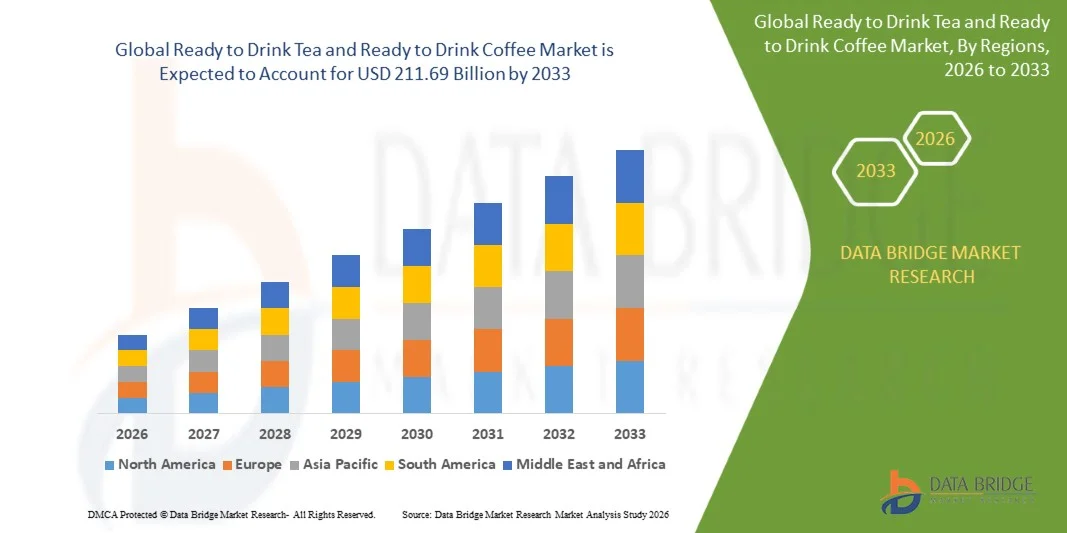

- The global ready to drink tea and ready to drink coffee market size was valued at USD 125.90 billion in 2025 and is expected to reach USD 211.69 billion by 2033, at a CAGR of 6.71% during the forecast period

- The market growth is largely fuelled by the rising demand for ready-to-consume beverages that offer convenience, taste, and functional benefits

- In addition, busy lifestyles and increasing working populations are driving the shift from traditional beverage preparation to packaged ready-to-drink alternatives

Ready to Drink Tea and Ready to Drink Coffee Market Analysis

- The market is witnessing consistent growth due to changing consumer preferences toward convenience, health-conscious consumption, and premium beverage experiences

- In addition, companies are investing in product diversification and sustainable packaging solutions to align with evolving consumer expectations and regulatory requirements

- Asia-Pacific dominated the ready to drink tea and ready to drink coffee market with the largest revenue share of 43.3% in 2025, driven by rapid urbanization, increasing disposable incomes, and changing consumer lifestyles

- North America region is expected to witness the highest growth rate in the global ready to drink tea and ready to drink coffee market, driven by rising consumer preference for convenience beverages, expanding distribution channels, and increasing adoption of health-oriented drink options

- The flavours segment held the largest market revenue share in 2025 driven by increasing consumer preference for diverse and innovative taste profiles. Flavored beverages enhance product appeal and encourage repeat purchases, making them a key focus area for manufacturers aiming to attract a broad consumer base. In addition, continuous innovation in exotic and region-specific flavors is helping brands differentiate their offerings and strengthen market positioning

Report Scope and Ready to Drink Tea and Ready to Drink Coffee Market Segmentation

|

Attributes |

Ready to Drink Tea and Ready to Drink Coffee Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

• Asahi Group Holdings Ltd. (Japan) |

|

Market Opportunities |

• Rising Demand For Functional And Health-Oriented Beverages |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Ready to Drink Tea and Ready to Drink Coffee Market Trends

“Rising Demand for Convenient and Functional Beverages”

• The increasing preference for on-the-go consumption is significantly shaping the ready to drink tea and coffee market, as consumers seek convenient beverage options that fit into busy lifestyles. These products are gaining traction due to their ease of use, consistent taste, and wide availability across retail channels. This trend is strengthening their adoption among urban consumers, encouraging manufacturers to introduce innovative and ready-to-consume beverage format

• Growing awareness around health, wellness, and functional nutrition has accelerated the demand for ready to drink tea and coffee with added benefits such as antioxidants, energy enhancement, and low sugar content. Health-conscious consumers are actively seeking beverages that offer both refreshment and nutritional value, prompting brands to develop functional and fortified variants. This has also led to increased collaboration between beverage companies and ingredient suppliers to enhance product offerings

• Premiumization and flavor innovation are influencing purchasing decisions, with manufacturers focusing on unique flavors, organic ingredients, and sustainable packaging solutions. These factors are helping brands differentiate their products in a competitive market while attracting a broader consumer base. In addition, the introduction of cold brew coffee and specialty tea variants is further enhancing consumer interest and driving repeat purchases

• For instance, in 2024, Nestlé and PepsiCo expanded their ready to drink beverage portfolios with new functional and low-sugar variants. These launches were introduced in response to increasing demand for healthier and convenient beverages, with distribution across supermarkets, convenience stores, and online platforms. The products were also marketed as premium and health-focused options, strengthening brand positioning and consumer loyalty

• While demand for ready to drink tea and coffee is rising, sustained market growth depends on continuous product innovation, cost management, and maintaining quality standards. Manufacturers are also focusing on improving shelf life, expanding distribution networks, and developing sustainable packaging solutions to support long-term adoption

Ready to Drink Tea and Ready to Drink Coffee Market Dynamics

Driver

“Growing Preference for Convenient and Functional Beverages”

• Rising consumer demand for ready-to-consume beverages is a major driver for the market, as individuals increasingly seek convenience without compromising on taste and quality. Manufacturers are expanding their product lines to include functional ingredients, organic options, and low-calorie variants to meet evolving consumer preferences. This trend is also encouraging the development of innovative formulations to enhance product appeal

• Expanding applications across daily consumption, energy drinks, and refreshment beverages are influencing market growth. Ready to drink tea and coffee provide convenience, portability, and consistent flavor, enabling manufacturers to cater to a wide range of consumer needs. The increasing adoption of busy and on-the-go lifestyles further reinforces demand for these beverages globally

• Beverage companies are actively promoting ready to drink tea and coffee through product innovation, branding strategies, and strategic partnerships. These efforts are supported by growing consumer interest in premium and health-oriented beverages, encouraging collaboration between manufacturers and distributors to improve product reach and performance

• For instance, in 2023, The Coca-Cola Company and Starbucks Corporation increased their focus on ready to drink coffee and tea offerings through new product launches and expanded distribution. This expansion followed rising consumer demand for convenient and premium beverages, driving repeat purchases and strengthening market presence. Both companies also emphasized sustainability and innovative packaging in their strategies

• Although rising demand for convenience and functionality supports growth, wider adoption depends on pricing strategies, product differentiation, and supply chain efficiency. Investment in sustainable sourcing, advanced processing technologies, and strong distribution networks will be critical for maintaining competitiveness

Restraint/Challenge

“Health Concerns and High Sugar Content in Packaged Beverages”

• The presence of added sugars and preservatives in many ready to drink tea and coffee products remains a key challenge, limiting adoption among health-conscious consumers. Concerns regarding calorie intake and long-term health effects are influencing purchasing decisions. In addition, regulatory scrutiny on sugar content and labeling requirements is impacting product formulation and marketing strategies

• Consumer awareness regarding healthier beverage alternatives remains uneven, particularly in developing markets where education on nutritional content is still evolving. Limited understanding of ingredient composition can affect demand for premium and functional products. This also slows the transition from traditional beverages to ready to drink options in certain regions

• Supply chain and storage challenges also impact market growth, as ready to drink beverages require efficient distribution, temperature control, and shelf life management. Logistical complexities and packaging requirements increase operational costs for manufacturers. Companies must invest in advanced packaging technologies and distribution infrastructure to maintain product quality

• For instance, in 2024, distributors in Southeast Asia supplying beverage brands reported slower adoption of certain ready to drink products due to concerns over sugar content and pricing. Regulatory compliance and labeling requirements were additional barriers, influencing product availability and consumer trust. These factors also affected shelf placement and promotional strategies in retail environment

• Overcoming these challenges will require reformulation of products, expansion of low-sugar and natural variants, and improved consumer awareness. Collaboration with regulatory bodies, retailers, and health organizations can help support long-term market growth, while innovation in packaging and ingredient sourcing will be essential for broader adoption

Ready to Drink Tea and Ready to Drink Coffee Market Scope

The market is segmented on the basis of additives, type, packaging, price, and distribution channel.

•By Additives

On the basis of additives, the ready to drink tea and ready to drink coffee market is segmented into flavours, artificial sweeteners, acidulates, nutraceuticals, preservatives, and others. The flavours segment held the largest market revenue share in 2025 driven by increasing consumer preference for diverse and innovative taste profiles. Flavored beverages enhance product appeal and encourage repeat purchases, making them a key focus area for manufacturers aiming to attract a broad consumer base. In addition, continuous innovation in exotic and region-specific flavors is helping brands differentiate their offerings and strengthen market positioning.

The nutraceuticals segment is expected to witness the fastest growth rate from 2026 to 2033, driven by rising demand for functional beverages offering added health benefits. Nutraceutical-infused drinks are gaining popularity among health-conscious consumers seeking energy, immunity, and wellness support. Ingredients such as vitamins, minerals, and herbal extracts are increasingly incorporated to enhance product value. This trend is further supported by the growing shift toward preventive healthcare and functional nutrition, encouraging manufacturers to expand their nutraceutical portfolios.

• By Type

On the basis of type, the market is segmented into black tea, green tea, oolong tea, fruit & herbal based tea, taurine, guarana, vitamin B, ginseng, yerba mate, and acai berry. The black tea segment held the largest market revenue share in 2025 driven by its widespread consumption, strong flavor profile, and established consumer base across global markets. Its familiarity and versatility make it a dominant choice in ready to drink formats. In addition, black tea-based beverages are widely accepted across different age groups, supporting consistent demand and large-scale production.

The green tea segment is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing awareness of its antioxidant properties and health benefits. Consumers are increasingly shifting toward healthier beverage options, making green tea a preferred choice among wellness-focused individuals. The demand for organic and low-calorie green tea variants is also rising. In addition, product innovation in flavors and packaging is further enhancing its appeal among younger consumers.

• By Packaging

On the basis of packaging, the market is segmented into glass bottle, canned, PET bottle, sachets, fountain/aseptic/cartons, and others. The PET bottle segment held the largest market revenue share in 2025 driven by its convenience, lightweight nature, and cost-effectiveness. PET bottles are widely used for their durability and ease of transportation, supporting large-scale distribution. In addition, their compatibility with various beverage types and sizes makes them a preferred packaging option for manufacturers.

The canned segment is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing demand for portable and recyclable packaging solutions. Cans offer longer shelf life and are gaining popularity among consumers seeking sustainable and convenient beverage options. Their ability to preserve freshness and flavor is also contributing to their growing adoption. Furthermore, rising environmental concerns are encouraging brands to adopt recyclable packaging formats such as aluminum cans.

• By Price

On the basis of price, the market is segmented into premium, regular, and super premium. The regular segment held the largest market revenue share in 2025 driven by its affordability and mass-market appeal. These products cater to a wide consumer base, ensuring consistent demand across various demographics. In addition, strong presence in supermarkets and convenience stores supports high sales volumes for regular-priced beverages.

The premium segment is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing consumer inclination toward high-quality ingredients, unique flavors, and branded experiences. Premium beverages are gaining traction among urban and high-income consumers seeking differentiated products. The inclusion of organic, artisanal, and specialty ingredients is further enhancing their appeal. In addition, attractive packaging and branding strategies are supporting premium segment growth.

• By Distribution Channel

On the basis of distribution channel, the market is segmented into off-trade and on-trade. The off-trade segment held the largest market revenue share in 2025 driven by the widespread availability of ready to drink beverages through supermarkets, convenience stores, and online platforms. This channel offers easy accessibility and a wide product variety, supporting high sales volumes. In addition, promotional offers and discounts in retail outlets are encouraging consumer purchases.

The on-trade segment is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing consumption in cafes, restaurants, and foodservice outlets. Growing urbanization and changing consumer lifestyles are encouraging out-of-home consumption, boosting demand through on-trade channels. In addition, the expansion of café culture and quick-service restaurants is further supporting segment growth. This trend is also driving partnerships between beverage brands and foodservice providers to expand market reach.

Ready to Drink Tea and Ready to Drink Coffee Market Regional Analysis

- Asia-Pacific dominated the ready to drink tea and ready to drink coffee market with the largest revenue share of 43.3% in 2025, driven by rapid urbanization, increasing disposable incomes, and changing consumer lifestyles

- The region’s strong tea and coffee consumption culture, combined with growing demand for convenient beverage options, is encouraging market expansion

- In addition, increasing investments in product innovation and distribution channels are improving accessibility across emerging economies

Japan Ready to Drink Tea and Ready to Drink Coffee Market Insight

The Japan ready to drink tea and ready to drink coffee market is expected to witness the fastest growth rate from 2026 to 2033 due to the country’s well-established ready to drink beverage culture and high demand for convenience. Consumers prefer high-quality, innovative, and functional beverage options, driving continuous product development. The widespread availability of vending machines and convenience stores is further supporting market growth.

China Ready to Drink Tea and Ready to Drink Coffee Market Insight

The China ready to drink tea and ready to drink coffee market accounted for the largest market revenue share in Asia Pacific in 2025, attributed to the country’s large consumer base, rapid urbanization, and increasing adoption of packaged beverages. China is one of the fastest-growing markets for ready to drink beverages, with strong demand across both urban and semi-urban areas. The availability of affordable products and expanding retail infrastructure are key factors driving market growth.

North America Ready to Drink Tea and Ready to Drink Coffee Market Insight

North America ready to drink tea and ready to drink coffee market is expected to witness the fastest growth rate from 2026 to 2033, driven by strong consumer demand for convenient beverage options and increasing preference for on-the-go consumption. Consumers in the region highly value the variety of flavors, functional benefits, and premium quality offered by ready to drink tea and coffee products across retail channels. This widespread adoption is further supported by high disposable incomes, a fast-paced lifestyle, and well-established distribution networks, establishing these beverages as a popular choice among both young and working populations

U.S. Ready to Drink Tea and Ready to Drink Coffee Market Insight

The U.S. ready to drink tea and ready to drink coffee market is expected to witness the fastest growth rate from 2026 to 2033, fueled by increasing demand for convenient, ready-to-consume beverages and strong presence of leading beverage brands. Consumers are increasingly prioritizing premium, functional, and low-sugar drink options that align with health and wellness trends. The growing popularity of cold brew coffee and specialty tea variants, combined with high penetration of retail and e-commerce channels, further propels market growth.

Europe Ready to Drink Tea and Ready to Drink Coffee Market Insight

The Europe ready to drink tea and ready to drink coffee market is expected to witness the fastest growth rate from 2026 to 2033, primarily driven by increasing demand for healthier beverage alternatives and sustainable packaging solutions. The rising trend of organic and clean-label products is fostering the adoption of ready to drink beverages. Consumers in the region are also drawn to premium offerings and innovative flavors, supporting market expansion across various consumption segments.

U.K. Ready to Drink Tea and Ready to Drink Coffee Market Insight

The U.K. ready to drink tea and ready to drink coffee market is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing consumer inclination toward convenient and functional beverages. In addition, the growing café culture and demand for premium ready to drink coffee products are supporting market growth. The country’s strong retail infrastructure and increasing preference for healthier beverage choices are expected to further accelerate adoption.

Germany Ready to Drink Tea and Ready to Drink Coffee Market Insight

The Germany ready to drink tea and ready to drink coffee market is expected to witness the fastest growth rate from 2026 to 2033, fueled by rising awareness of health and wellness and increasing demand for organic and low-calorie beverages. Germany’s well-developed retail sector and focus on sustainability are promoting the adoption of eco-friendly packaging and premium beverage options. The growing popularity of functional drinks is also contributing to market growth.

Ready to Drink Tea and Ready to Drink Coffee Market Share

The Ready to Drink Tea and Ready to Drink Coffee industry is primarily led by well-established companies, including:

• Asahi Group Holdings Ltd. (Japan)

• The Coca-Cola Company (U.S.)

• Unilever (U.K.)

• PepsiCo (U.S.)

• Suntory Holdings Limited (Japan)

• JBD Group (China)

• Ting Hsin (Taiwan)

• Amul Dairy, Anand (India)

• Arizona Beverages Company (U.S.)

• TradeWinds Beverage Company (U.S.)

• F&N Foods Pte Ltd (Singapore)

• Argo Tea (U.S.)

• Sweet Leaf Tea (U.S.)

• Xing Tea (U.S.)

• Kirin Beverage Company (Japan)

• Malaysia Dairy Industries (Malaysia)

Latest Developments in Global Ready to Drink Tea and Ready to Drink Coffee Market

- In December 2022, MatchaKo, product innovation, launched a premium ready to drink matcha beverage certified as organic, vegan, and non-GMO, offering a healthier alternative with lower calorie content compared to traditional sugary drinks. The product utilizes high-quality ceremonial-grade matcha sourced from Japan, enhancing its premium positioning. Its shelf-stable formulation improves convenience and accessibility for consumers. This development is expected to strengthen the demand for clean-label and functional beverages while encouraging innovation in premium RTD segments

- In April 2022, Red Diamond Coffee & Tea, product expansion, introduced a new 11-oz ready to drink tea bottle to diversify its product portfolio and address packaging size gaps. The formulation focuses on simplicity, using minimal ingredients without concentrates or preservatives, aligning with clean-label trends. This initiative enhances product transparency and consumer trust while catering to convenience-driven consumption. The launch is likely to support brand differentiation and increase market competitiveness

- In July 2021, Bottleshot Cold Brew, distribution expansion, expanded its presence in the U.K. by securing listings with Ocado and WHSmith Travel stores to strengthen its online and travel retail reach. This move improves product accessibility across key consumer touchpoints and supports brand visibility in a competitive market. The expansion aligns with the growing demand for premium ready to drink coffee options. It is expected to drive sales growth and encourage further expansion of RTD coffee brands across international markets

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Ready Drink Tea Ready Drink Coffee Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Ready Drink Tea Ready Drink Coffee Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Ready Drink Tea Ready Drink Coffee Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.