Global Regulatory Technology Regtech Market

Market Size in USD Billion

CAGR :

%

USD

16.57 Billion

USD

491.38 Billion

2025

2033

USD

16.57 Billion

USD

491.38 Billion

2025

2033

| 2026 –2033 | |

| USD 16.57 Billion | |

| USD 491.38 Billion | |

| % | |

|

Regulatory Technology (Regtech) Market Size

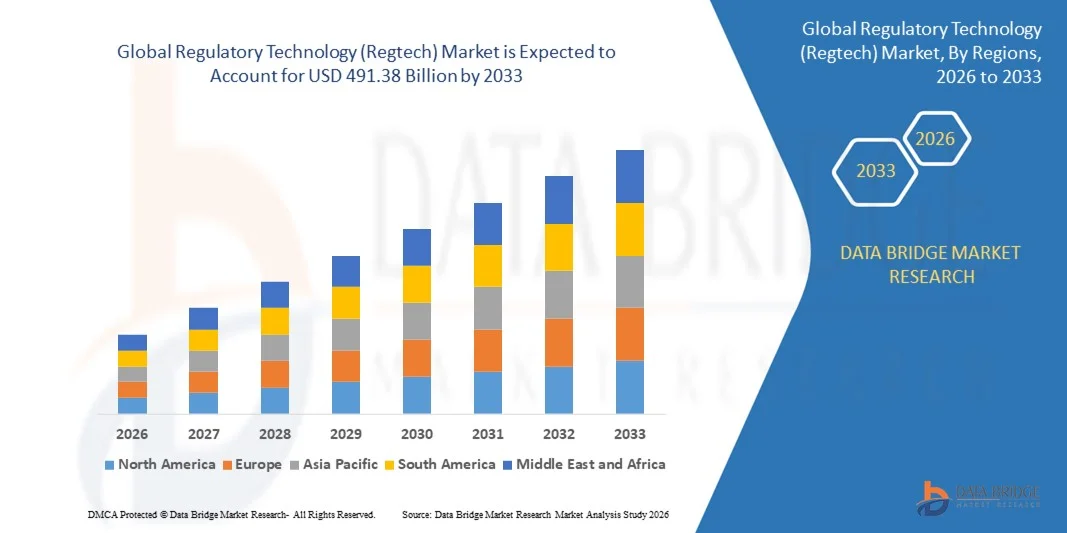

- The global regulatory technology (Regtech) market size was valued at USD 16.57 billion in 2025 and is expected to reach USD 491.38 billion by 2033, at a CAGR of 52.75% during the forecast period

- The market growth is largely fuelled by the increasing complexity of regulatory frameworks across financial institutions and other heavily regulated industries

- Growing demand for automated compliance solutions, real-time monitoring, and risk management tools is further accelerating market adoption

Regulatory Technology (Regtech) Market Analysis

- Financial institutions and enterprises are increasingly adopting Regtech solutions to reduce compliance costs, improve efficiency, and minimize regulatory penalties

- The market is witnessing rapid innovation, with AI, machine learning, and blockchain technologies being leveraged to enhance regulatory monitoring, reporting, and analytics capabilities

- North America dominated the regulatory technology (Regtech) market with the largest revenue share of 42.15% in 2025, driven by rapid digitization of financial services, stringent compliance regulations, and a growing focus on risk management across banking and insurance sectors

- Asia-Pacific region is expected to witness the highest growth rate in the global regulatory technology (Regtech) market, driven by expansion of fintech, increasing investments in digital compliance technologies, and supportive government policies encouraging regulatory automation

- The solutions segment held the largest market revenue share in 2025, driven by the increasing adoption of AI-powered platforms, automated compliance tools, and real-time monitoring systems across financial institutions. Regtech solutions help streamline regulatory reporting, enhance operational efficiency, and reduce compliance costs, making them a preferred choice for enterprises. In addition, solutions provide predictive insights and risk assessment capabilities, enabling proactive compliance management. The growing complexity of financial regulations globally further supports the demand for comprehensive Regtech solutions

Report Scope and Regulatory Technology (Regtech) Market Segmentation

|

Attributes |

Regulatory Technology (Regtech) Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

Regulatory Technology (Regtech) Market Trends

Rising Adoption Of AI And Automation In Compliance Solutions

- The growing emphasis on regulatory compliance and risk management is significantly shaping the global Regtech market, as financial institutions and enterprises increasingly prefer automated, technology-driven solutions. Regtech platforms are gaining traction due to their ability to enhance regulatory reporting, monitor transactions in real time, and reduce compliance costs. This trend strengthens their adoption across banking, insurance, and capital markets, encouraging providers to develop innovative solutions that address evolving regulatory requirements

- Increasing awareness around data security, fraud prevention, and operational efficiency has accelerated the demand for Regtech solutions in anti-money laundering (AML), know-your-customer (KYC), and risk management processes. Organizations are actively seeking platforms that leverage AI, machine learning, and cloud computing to ensure compliance, prompting solution providers to focus on scalable and intelligent offerings

- Automation and digitalization trends are influencing purchasing decisions, with enterprises prioritizing platforms that reduce manual effort, minimize human error, and ensure real-time compliance. These factors help organizations strengthen governance, reduce penalties, and improve operational efficiency, while also encouraging adoption of advanced analytics and blockchain-enabled solutions

- For instance, in 2024, Deloitte in the U.S. and PwC in the U.K. expanded their Regtech service portfolios by incorporating AI-driven compliance monitoring and real-time risk analytics. These initiatives were introduced in response to increasing regulatory scrutiny and the growing need for faster, more reliable compliance solutions, distributed across enterprise, financial, and governmental clients

- While demand for Regtech solutions is rising, sustained market expansion depends on integration capabilities, regulatory alignment across regions, and continuous innovation. Providers are also focusing on improving platform scalability, data security, and user experience to achieve broader adoption

Regulatory Technology (Regtech) Market Dynamics

Driver

Rising Need For Efficient Compliance And Risk Management

- The increasing complexity of global regulations is a major driver for the Regtech market. Enterprises are adopting digital solutions to streamline compliance processes, enhance transparency, and minimize risk exposure. This trend is also pushing development of AI-powered and cloud-based platforms that can quickly adapt to regulatory changes

- Expanding applications across banking, insurance, capital markets, and financial services are influencing market growth. Regtech solutions help improve reporting accuracy, enable real-time monitoring, and reduce operational costs, meeting enterprise expectations for compliance efficiency

- Service providers are actively promoting Regtech adoption through partnerships, platform integrations, and customized solutions. These efforts are supported by rising demand for automated risk assessment, regulatory reporting, and fraud detection, encouraging collaboration between technology vendors and financial institutions to improve operational resilience

- For instance, in 2023, KPMG in the U.S. and EY in the U.K. reported increased deployment of AI-enabled compliance solutions for corporate clients. This expansion followed higher regulatory scrutiny and a need for efficient risk management, driving repeat adoption and customer loyalty. Both firms also highlighted the role of predictive analytics and real-time monitoring in marketing campaigns to strengthen client confidence

- Although increasing regulatory complexity supports growth, wider adoption depends on platform integration, regional compliance alignment, and cost-effective implementation. Investment in cloud infrastructure, AI capabilities, and robust cybersecurity will be critical for meeting global demand and maintaining competitive advantage

Restraint/Challenge

Data Security Concerns And Integration Complexity

- Concerns around sensitive data security and privacy remain a key challenge for Regtech adoption, as enterprises must comply with multiple regulations across jurisdictions. Any data breach or system vulnerability can lead to severe penalties, limiting adoption among risk-averse organizations

- Uneven awareness and understanding of Regtech benefits restrict adoption, particularly among small and medium-sized enterprises in developing markets. Limited technical expertise can hinder implementation and slow the uptake of advanced compliance solutions

- Integration challenges also impact market growth, as Regtech platforms must be compatible with existing enterprise systems, financial databases, and reporting infrastructure. Complex integration processes, high implementation costs, and legacy system constraints can reduce operational efficiency

- For instance, in 2024, financial institutions in Singapore and India reported slower adoption of automated compliance platforms due to security concerns, integration hurdles, and limited regulatory clarity. These factors prompted some enterprises to continue relying on manual compliance processes, affecting market penetration

- Overcoming these challenges will require secure, flexible, and easily integrable solutions, along with focused educational initiatives for clients. Collaboration between technology providers, regulators, and enterprise stakeholders can help unlock long-term growth potential. Furthermore, developing cost-effective, scalable, and secure platforms will be essential for widespread adoption of Regtech solutions

Regulatory Technology (Regtech) Market Scope

The regulatory technology (Regtech) market is segmented on the basis of component, deployment model, organization size, application, and end-users.

- By Component

On the basis of component, the market is segmented into solutions and services. The solutions segment held the largest market revenue share in 2025, driven by the increasing adoption of AI-powered platforms, automated compliance tools, and real-time monitoring systems across financial institutions. Regtech solutions help streamline regulatory reporting, enhance operational efficiency, and reduce compliance costs, making them a preferred choice for enterprises. In addition, solutions provide predictive insights and risk assessment capabilities, enabling proactive compliance management. The growing complexity of financial regulations globally further supports the demand for comprehensive Regtech solutions.

The services segment is expected to witness the fastest growth rate from 2026 to 2033, fueled by the rising demand for managed compliance services, consulting, and system integration. Services offerings enable organizations to implement Regtech platforms more efficiently, customize solutions based on regulatory requirements, and ensure continuous support, boosting adoption among enterprises with limited in-house technical expertise. Moreover, service providers assist in training staff, ensuring smooth platform adoption, and maintaining compliance in a dynamically changing regulatory landscape. This is particularly valuable for SMEs and non-financial firms entering regulated markets.

- By Deployment Model

On the basis of deployment model, the market is segmented into cloud and on-premises. The cloud segment dominated in 2025 due to its scalability, cost-effectiveness, and ease of integration with existing enterprise systems. Cloud-based Regtech platforms allow real-time monitoring, centralized reporting, and secure data management, enhancing operational efficiency. In addition, cloud deployments enable multi-location organizations to standardize compliance processes and quickly adapt to new regulatory changes without extensive infrastructure investments. The adoption of hybrid cloud models is also gaining traction, combining flexibility with enhanced security.

The on-premises segment is expected to witness the fastest growth rate from 2026 to 2033, driven by enterprises prioritizing data privacy, regulatory compliance, and control over sensitive information. On-premises solutions appeal to large financial organizations with stringent internal governance and data security policies. These deployments offer full control over data storage, configuration, and access management, which is crucial for handling confidential financial and customer information. Regulatory audits and compliance verification processes are easier to manage with on-premises solutions for highly regulated sectors.

- By Organization Size

On the basis of organization size, the market is segmented into large enterprises and small and medium-sized enterprises (SMEs). Large enterprises held the largest market share in 2025, owing to their complex regulatory requirements, higher adoption of advanced compliance platforms, and ability to invest in AI-driven and analytics-enabled Regtech solutions. They also benefit from automated reporting, risk analytics, and centralized compliance dashboards to manage multiple jurisdictions efficiently. Large enterprises are increasingly using Regtech for operational resilience, fraud prevention, and regulatory intelligence to stay competitive.

SMEs is expected to witness the fastest growth rate from 2026 to 2033, as these organizations increasingly seek cost-effective, cloud-based, and scalable Regtech platforms to comply with evolving regulations and reduce operational risks. SMEs are adopting subscription-based Regtech solutions to avoid high upfront costs and benefit from continuous updates aligned with regulatory changes. The rising number of fintech startups and small financial service providers globally further drives adoption. Regtech enables SMEs to maintain compliance without building extensive in-house infrastructure or expertise.

- By Application

On the basis of application, the market is segmented into risk and compliance management, identity management, regulatory reporting, anti-money laundering and fraud management, and regulatory intelligence. Regulatory reporting dominated in 2025, driven by the need for accurate, timely, and automated reporting to meet stringent financial regulations. Automated reporting minimizes human errors, reduces compliance time, and ensures adherence to multiple regional regulations. Financial institutions leverage these tools to maintain transparency, avoid penalties, and optimize internal resources.

The anti-money laundering and fraud management segment is expected to witness the fastest growth rate from 2026 to 2033, fueled by rising regulatory scrutiny, financial crime risks, and increasing adoption of AI and machine learning technologies to detect and prevent fraudulent activities. Advanced analytics, pattern recognition, and real-time monitoring allow organizations to identify suspicious transactions faster. This segment is expanding across banking, insurance, and investment firms to mitigate financial losses and reputational risks. Continuous regulatory updates and cross-border compliance requirements further strengthen demand.

- By End Users

On the basis of end-users, the market is segmented into banking and capital markets, insurance, and non-finance sectors. Banking and capital markets held the largest share in 2025, driven by strict compliance requirements, risk management needs, and large-scale deployment of Regtech platforms for reporting, monitoring, and fraud detection. Banks are increasingly adopting integrated platforms that combine identity verification, risk assessment, and compliance monitoring. The growing digitalization of financial services and adoption of open banking also support Regtech adoption in this sector.

The insurance segment is expected to witness the fastest growth from 2026 to 2033, as insurers increasingly adopt Regtech solutions for underwriting compliance, claims monitoring, and anti-fraud measures, enhancing operational efficiency and regulatory adherence. Regtech platforms help insurance providers automate reporting, monitor policy compliance, and detect fraudulent claims in real-time. The sector is also leveraging Regtech to manage cross-border regulations and improve customer trust through transparent compliance practices. Rising digitization and IoT integration in insurance further accelerate market growth.

Regulatory Technology (Regtech) Market Regional Analysis

- North America dominated the regulatory technology (Regtech) market with the largest revenue share of 42.15% in 2025, driven by rapid digitization of financial services, stringent compliance regulations, and a growing focus on risk management across banking and insurance sectors

- Organizations in the region are increasingly adopting advanced Regtech solutions to automate compliance, reduce operational risks, and ensure real-time regulatory reporting. The availability of cloud infrastructure and robust IT ecosystems further supports market penetration

- High investment capacity, technological readiness, and an expanding base of fintech startups are accelerating Regtech adoption, establishing North America as a key hub for regulatory innovation and digital compliance solutions

U.S. Regtech Market Insight

The U.S. Regtech market captured the largest revenue share in 2025 within North America, fueled by growing regulatory pressure and the need for efficient compliance management in banking, insurance, and capital markets. Financial institutions are leveraging AI, blockchain, and cloud-based solutions to streamline identity verification, anti-money laundering (AML), and fraud detection processes. The increasing emphasis on digital reporting and real-time risk management is driving the demand for automated Regtech platforms, while government initiatives promoting digital compliance further reinforce market growth.

Europe Regtech Market Insight

The Europe Regtech market is expected to witness the fastest growth rate from 2026 to 2033, primarily driven by stringent data protection regulations such as GDPR, increasing cross-border transactions, and rising regulatory complexity. Enterprises are increasingly adopting cloud-based Regtech solutions for risk management, regulatory reporting, and identity verification. The growing digital transformation initiatives in banking and insurance sectors are fostering rapid Regtech adoption across the region.

U.K. Regtech Market Insight

The U.K. Regtech market is expected to witness the fastest growth rate from 2026 to 2033, supported by strong fintech presence, government-backed digital initiatives, and heightened focus on AML and fraud prevention. Financial institutions are deploying AI-driven solutions to improve compliance efficiency, automate reporting, and reduce operational risks. The robust regulatory environment and the country’s well-developed fintech ecosystem continue to stimulate market expansion.

Germany Regtech Market Insight

The Germany Regtech market is expected to witness significant growth from 2026 to 2033, fueled by increasing regulatory complexity, financial sector digitization, and a growing demand for automated compliance solutions. German banks and insurers are adopting AI- and blockchain-based platforms for risk assessment, regulatory reporting, and fraud detection. The integration of Regtech with enterprise IT systems is becoming widespread, enabling organizations to reduce manual compliance efforts and operational costs.

Asia-Pacific Regtech Market Insight

The Asia-Pacific Regtech market is expected to witness the highest growth rate from 2026 to 2033, driven by rising fintech adoption, digital banking expansion, and increasing regulatory scrutiny in countries such as China, India, and Singapore. The region’s growing emphasis on financial inclusion, real-time reporting, and risk management solutions is accelerating Regtech deployment. Emerging economies are adopting cloud-based Regtech platforms to ensure scalable and cost-effective compliance solutions.

China Regtech Market Insight

The China Regtech market accounted for the largest revenue share in Asia-Pacific in 2025, attributed to the country’s rapidly expanding banking and insurance sectors, stringent local regulatory frameworks, and strong government support for digital transformation. Chinese financial institutions are implementing AI, machine learning, and cloud-based solutions to enhance compliance efficiency, automate reporting, and mitigate fraud risks. The increasing integration of Regtech solutions with fintech platforms and digital payment systems is propelling the market forward.

Regulatory Technology (Regtech) Market Share

The Regulatory Technology (Regtech) industry is primarily led by well-established companies, including:

- ACTICO GmbH (Germany)

- Broadridge Financial Solutions, Inc. (U.S.)

- Deloitte (U.K.)

- London Stock Exchange Group plc (U.K.)

- IBM (U.S.)

- Jumio (U.S.)

- MetricStream Inc. (U.S.)

- Nice Actimize (U.S.)

- PwC (U.K.)

- REGIS-TR (U.K.)

- InfrasoftTech (U.S.)

- Thomson Reuters (U.S.)

- VERMEG (Belgium)

- Trulioo (Canada)

- Fenergo (Ireland)

- ComplyAdvantage (U.K.)

- Acuant, Inc. (U.S.)

- Ascent (U.S.)

- Ayasdi AI LLC (U.S.)

- Pole Star Space Applications (U.K.)

Latest Developments in Global Regulatory Technology (Regtech) Market

- In May 2024, CUBE (U.K.) executed a strategic acquisition of Thomson Reuters’ RegTech business, expanding its portfolio in Automated Regulatory Intelligence (ARI). This development aims to broaden CUBE’s customer base, strengthen its talent pool, and enhance its technological capabilities. The acquisition is expected to improve service offerings, accelerate innovation in regulatory compliance solutions, and reinforce CUBE’s competitive position in the global RegTech market, driving growth and market influence

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.