Global Retinal Implant Market

Market Size in USD Billion

CAGR :

%

USD

47.40 Billion

USD

110.81 Billion

2025

2033

USD

47.40 Billion

USD

110.81 Billion

2025

2033

| 2026 - 2033 | |

| USD 47.40 Billion | |

| USD 110.81 Billion | |

| % | |

|

Retinal Implant Market Overview

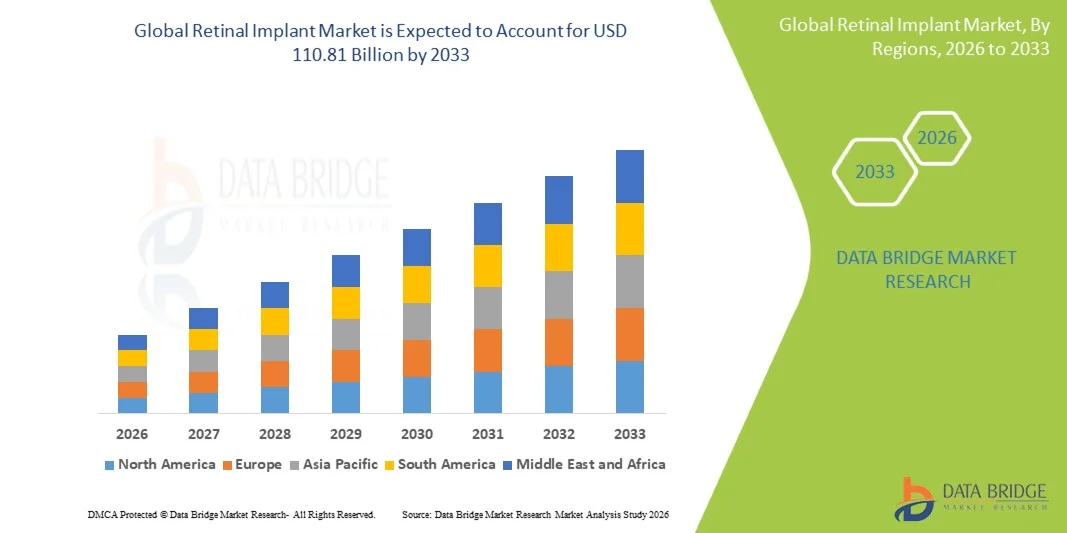

The Retinal Implant Market was valued at USD 47.40 billion in 2025 and is projected to reach USD 110.81 billion by 2033, growing at a CAGR of 11.20% from 2026 to 2033. The market is witnessing steady growth driven by increasing prevalence of retinal degenerative diseases, rising geriatric population, and rapid advancements in neuroprosthetic and bioelectronic vision restoration technologies.

The growing incidence of conditions such as retinitis pigmentosa and age-related macular degeneration, combined with unmet clinical needs in severe vision loss cases, is encouraging adoption of retinal prosthetic devices and implantable vision restoration systems. Continuous improvements in microelectronics, biocompatible materials, and wireless retinal stimulation technologies are enhancing device performance and patient outcomes. In addition, increasing investments in ophthalmic research and regulatory support for breakthrough medical devices are accelerating clinical trials and commercialization of next-generation retinal implants.

Key Market Trends & Insights

- North America dominated the Retinal Implant Market with the largest revenue share of 38.6% in 2025, supported by advanced ophthalmic healthcare infrastructure, strong reimbursement frameworks, and early adoption of neuroprosthetic vision restoration technologies.

- The Argus II segment led the market with a 42.6% share in 2025, driven by its status as one of the earliest commercially approved retinal prosthesis systems for severe vision loss treatment.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 9.1% from 2026 to 2033, fueled by rising prevalence of retinal disorders, expanding geriatric population, improving healthcare infrastructure, and increasing access to advanced ophthalmic treatments in countries such as China, India, Japan, and South Korea.

- Retina Implant Alpha AMS are the fastest-growing product type, projected to register a CAGR of 10.8%, reflecting the surge in advancements in subretinal stimulation technology and improved visual resolution outcomes.

- The epiretinal implants segment dominated the implant type category with a 46.3% revenue share in 2025, led by early commercialization and widespread clinical use of devices such as Argus II.

- Retinitis pigmentosa accounted for 51.7% of the market, preferred by the primary approved indication for most retinal prosthesis systems.

- The age-related macular degeneration (AMD) segment is the fastest-growing indication category, with a CAGR of 9.6%, driven by the rapidly increasing elderly population worldwide.

Market Size & Forecast

- Global Market Value (2025): USD 47.40 Billion

- Expected Market Value (2033): USD 110.81 Billion

- Forecast CAGR (2026–2033): 11.20%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia Pacific

Report Scope and Retinal Implant Market Segmentation

|

Attributes |

Retinal Implant Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Cortigent (U.S.) · Science Corporation (U.S.) · Pixium Vision (France) · VisionCare Ophthalmic Technologies (U.S.) · Nano Retina (Israel) · Retina Implant AG (Germany) · Bionic Vision Technologies (Australia) · Monash Vision Group (Australia) · iBionics Inc. (Canada) · Second Sight Medical Products (U.S.) · Shanghai Artificial Vision Technology Co., Ltd. (China) · Shenzhen SiBionic Technology Co., Ltd. (China) · Kyoto University (Japan) · Osaka University (Japan) · Stanford University (U.S.) · Harvard Medical School (U.S.) · University College London (U.K.) · University of Oxford (U.K.) · EPFL – Swiss Federal Institute of Technology (Switzerland) · Seoul National University Hospital (South Korea) |

|

Market Opportunities |

· Development of next-generation high-resolution wireless retinal implants · Expansion of clinical applications beyond retinitis pigmentosa into age-related macular degeneration · Growing integration of minimally invasive surgical techniques and biocompatible microelectrode materials |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Retinal Implant Market Trends

Trend: Advancement in Bioelectronic Vision Restoration Technologies

Retinal implant systems are increasingly incorporating high-density microelectrode arrays, wireless power transmission, and photovoltaic stimulation technologies to improve visual resolution and long-term implant stability. Continuous progress in neural interface engineering is enabling more precise stimulation of retinal ganglion cells, improving image perception quality in patients with severe vision loss. Research institutions and medical device companies are also focusing on miniaturized, fully implantable systems that reduce surgical complexity and enhance patient comfort, while AI-assisted image preprocessing is improving real-time visual signal interpretation in next-generation devices. For instance, PRIMA photovoltaic retinal implant systems and advanced subretinal microchip platforms are being developed to enhance wireless vision restoration capabilities.

Retinal Implant Market Dynamics

Key Market Driver: Rising Prevalence of Degenerative Retinal Diseases and Aging Population

The increasing global incidence of age-related macular degeneration, retinitis pigmentosa, and diabetic retinopathy is significantly driving demand for retinal implant solutions as conventional treatments offer limited efficacy in advanced-stage vision loss. The growing geriatric population worldwide is further accelerating the patient pool requiring vision restoration technologies, particularly in developed and emerging healthcare markets. Healthcare systems and ophthalmology centers are increasingly adopting retinal prostheses as a last-line treatment option for restoring partial visual function and improving patient quality of life. For instance, Argus II and Alpha AMS implant systems have been clinically utilized in patients with severe retinitis pigmentosa to restore basic visual perception.

Key Restraint/Challenge: High Cost, Surgical Complexity, and Limited Accessibility

A major restraint in the retinal implant market is the extremely high cost of devices and surgical procedures combined with the complexity of implantation and post-operative rehabilitation requirements. These systems require highly specialized surgical expertise, advanced hospital infrastructure, and long-term patient training, which limits adoption to select advanced healthcare centers. In addition, limited reimbursement coverage in several countries and the experimental nature of many devices restrict large-scale commercialization and accessibility for patients in low- and middle-income regions. For instance, implantation procedures for devices such as Argus II require multi-stage surgery and intensive rehabilitation, making widespread adoption challenging outside specialized ophthalmic centers.

Key Market Opportunity: Expansion of Next-Generation Wireless and AI-Assisted Vision Restoration Systems

The integration of wireless retinal stimulation technologies, artificial intelligence-based image processing, and cloud-connected neuroprosthetic platforms presents a major growth opportunity for the retinal implant market. These advancements are expected to improve visual clarity, enable real-time adaptive signal modulation, and reduce dependency on bulky external hardware, thereby enhancing patient comfort and usability. Increasing collaboration between biotech firms, AI developers, and ophthalmic device manufacturers is accelerating innovation in fully implantable, minimally invasive retinal prostheses. For instance, emerging photovoltaic implant systems and AI-enhanced retinal decoding platforms are being developed to enable more natural and adaptive vision restoration outcomes.

Retinal Implant Market Scope

The retinal implant market is segmented on the basis of product type, implant type, indication, and end user.

- By Product Type

On the basis of product type, the Retinal Implant Market is segmented into Retina Implant Alpha AMS, Implantable Miniature Telescope (IMT), Argus II, and Others. The Argus II segment dominated the market with the highest share of 42.6% in 2025, owing to its status as one of the earliest commercially approved retinal prosthesis systems for severe vision loss treatment. It has been widely adopted in clinical research and specialized ophthalmic centers for patients with advanced retinitis pigmentosa. Strong clinical validation and long-term patient outcome data have reinforced its dominance. The system’s established surgical protocols and global awareness among ophthalmologists also contribute to sustained usage. However, its availability is limited due to discontinuation and replacement by next-generation technologies. Despite this, its legacy adoption base continues to maintain market leadership in installed systems.

The Retina Implant Alpha AMS segment is expected to witness the fastest growth at a CAGR of 10.8% from 2026 to 2033, driven by advancements in subretinal stimulation technology and improved visual resolution outcomes. It offers better biocompatibility and more natural signal processing compared to earlier devices. Increasing clinical trials in Europe and expanding regulatory approvals are supporting adoption. The system’s ability to restore partial functional vision in low-light conditions is further enhancing demand. Rising investment in next-generation neuroprosthetic research is accelerating product development. Growing focus on wireless and minimally invasive implantation techniques is also strengthening its growth trajectory.

- By Implant Type

On the basis of implant type, the Retinal Implant Market is segmented into epiretinal implants, subretinal implants, suprachoroidal implants, and optic nerve implants. The epiretinal implants segment dominated the market with a 46.3% share in 2025, primarily due to early commercialization and widespread clinical use of devices such as Argus II. These implants are positioned on the inner retinal surface, allowing direct stimulation of retinal ganglion cells for basic visual perception. Their established surgical procedures and clinical familiarity among ophthalmic surgeons have supported widespread adoption. Strong historical usage in retinitis pigmentosa patients has reinforced dominance. However, limitations in image resolution and dependency on external hardware restrict advanced performance. Despite technological evolution, epiretinal implants remain the most clinically deployed category globally.

The subretinal implants segment is expected to be the fastest growing at a CAGR of 11.2% from 2026 to 2033, driven by superior anatomical alignment with photoreceptor layers and improved visual fidelity. These implants mimic natural retinal processing more closely, leading to enhanced image perception. Advancements in photovoltaic microchip technology are enabling fully wireless operation. Increasing clinical trials and regulatory approvals in Europe and Asia-Pacific are accelerating adoption. Growing demand for next-generation vision restoration systems is further boosting research funding. The segment is also benefiting from innovations in ultra-miniaturized implant designs and biocompatible materials.

- By Indication

On the basis of indication, the Retinal Implant Market is segmented into retinitis pigmentosa, age-related macular degeneration (AMD), diabetic retinopathy, blindness, and other retinal degenerative disorders. The retinitis pigmentosa segment dominated the market with a 51.7% share in 2025, as it represents the primary approved indication for most retinal prosthesis systems. Patients with advanced RP experience severe photoreceptor degeneration, making them ideal candidates for electronic vision restoration. Established clinical trial history and regulatory approvals for RP-specific devices have strengthened its dominance. High unmet medical need in late-stage disease further supports demand. Continuous research into genetic therapies combined with implants is expanding treatment pathways. However, the limited patient population compared to AMD restricts long-term volume expansion.

The age-related macular degeneration (AMD) segment is expected to be the fastest growing at a CAGR of 9.6% from 2026 to 2033, driven by the rapidly increasing elderly population worldwide. AMD leads to central vision loss, creating strong demand for assistive visual restoration technologies. Advancements in high-resolution implant systems are improving suitability for AMD patients. Expanding clinical research into hybrid implant-photovoltaic systems is supporting adoption. Rising healthcare spending and improved diagnosis rates are further accelerating demand. Growing focus on restoring functional vision in aging populations is positioning AMD as a key future growth indication.

- By End User

On the basis of end user, the Retinal Implant Market is segmented into hospitals and eye care centers. The hospitals segment dominated the market with a 63.9% share in 2025, due to the requirement for highly complex surgical implantation procedures and multidisciplinary postoperative care. Hospitals are equipped with advanced ophthalmic surgical infrastructure and trained retinal specialists, making them the primary centers for implantation procedures. Availability of rehabilitation services and long-term patient monitoring further strengthens their dominance. Strong referral networks for severe vision loss cases also contribute to higher patient inflow. However, high treatment costs and limited accessibility restrict widespread adoption outside specialized centers. Despite this, hospitals remain the central hub for retinal implant procedures globally.

The eye care centers segment is expected to be the fastest growing at a CAGR of 10.1% from 2026 to 2033, driven by increasing decentralization of ophthalmic care and expansion of specialized vision restoration clinics. These centers are becoming more capable of handling advanced diagnostic and follow-up care for implant patients. Rising investments in outpatient ophthalmic infrastructure are supporting growth. Increasing awareness of vision restoration technologies is driving patient visits to specialized clinics. Partnerships between device manufacturers and eye care networks are improving accessibility. Growing focus on minimally invasive procedures and outpatient-based care models is further accelerating adoption.

Retinal Implant Market Regional Analysis

North America dominated the Retinal Implant Market with the largest revenue share of 38.6% in 2025, supported by advanced ophthalmic healthcare infrastructure, strong reimbursement frameworks, and early adoption of neuroprosthetic vision restoration technologies. The region benefits from high healthcare expenditure, strong presence of leading medical device companies, and favorable reimbursement frameworks for advanced surgical procedures. Increasing prevalence of retinal degenerative diseases and a growing geriatric population are further driving demand for retinal implant systems. The presence of well-established ophthalmology centers and specialized vision rehabilitation facilities continues to strengthen market leadership. Continuous investment in AI-integrated vision restoration devices and ongoing clinical trials further supports regional dominance. Growing adoption of next-generation subretinal and photovoltaic implant technologies is also accelerating market expansion in the region.

U.S. Retinal Implant Market Insight

The U.S. retinal implant market is witnessing steady growth due to strong investments in advanced ophthalmic research, increasing prevalence of retinal degenerative diseases, and early adoption of neuroprosthetic vision restoration technologies. The country’s well-established healthcare infrastructure, along with the presence of leading medical device companies and research institutions, is driving demand for retinal implant systems. Rising focus on clinical trials for next-generation subretinal and photovoltaic implants is further accelerating innovation. In addition, favorable reimbursement frameworks and growing awareness of vision restoration solutions are supporting patient access and adoption. Increasing collaboration between biotech firms and academic centers continues to strengthen market development across the U.S.

Europe Retinal Implant Market Insight

The Europe retinal implant market remains a major contributor to global revenue, driven by strong clinical research activity, supportive regulatory pathways, and high investment in neuroengineering technologies. The region benefits from well-established ophthalmology networks and active participation in medical device innovation programs. Increasing use of retinal prostheses in clinical trials for retinitis pigmentosa and age-related macular degeneration is supporting market expansion. In addition, strong government funding for bioelectronic medicine and vision restoration research is accelerating technological advancement. The presence of leading academic research institutes and medtech companies continues to reinforce Europe’s position in the global market.

U.K. Retinal Implant Market Insight

The U.K. retinal implant market is experiencing gradual growth, supported by increasing adoption of advanced ophthalmic technologies and strong focus on clinical research in vision restoration. Growing investments in NHS-supported ophthalmology services and academic research programs are contributing to market development. The country’s emphasis on early diagnosis and treatment of retinal diseases is driving demand for innovative implantable solutions. Furthermore, collaboration between universities, biotech firms, and healthcare providers is enhancing clinical trial activity. Rising awareness of neuroprosthetic vision restoration is positioning the U.K. as an important contributor to European market growth.

Germany Retinal Implant Market Insight

The Germany retinal implant market is expanding steadily due to strong medical device manufacturing capabilities, advanced research infrastructure, and increasing focus on neuroprosthetic innovation. The country is actively involved in the development and clinical testing of subretinal implant technologies. Strong collaboration between engineering institutes and ophthalmic research centers is supporting technological advancements. Increasing prevalence of age-related eye diseases is further driving demand for vision restoration solutions. In addition, government support for medtech innovation and high-quality healthcare services is strengthening Germany’s role in the European retinal implant landscape.

Asia-Pacific Retinal Implant Market Insight

The Asia-Pacific retinal implant market is expected to witness rapid growth, driven by rising prevalence of retinal disorders, expanding geriatric population, and improving access to advanced ophthalmic care. Increasing investments in healthcare infrastructure and growing adoption of cutting-edge medical technologies are supporting regional expansion. Countries such as China, Japan, and India are increasingly focusing on clinical research and awareness programs for vision impairment treatment. In addition, rising collaboration with global medtech companies is accelerating technology transfer and adoption. The region’s growing patient pool and improving reimbursement systems are positioning Asia-Pacific as a high-growth market globally.

Japan Retinal Implant Market Insight

The Japan retinal implant market is witnessing consistent growth due to strong emphasis on advanced healthcare innovation, aging population, and increasing cases of age-related macular degeneration. The country’s highly developed medical technology ecosystem is supporting research in neuroprosthetic vision restoration systems. Japanese universities and research institutes are actively involved in retinal implant development and clinical trials. In addition, integration of robotics, AI, and precision medicine into ophthalmology is enhancing treatment outcomes. Government support for regenerative medicine and assistive vision technologies continues to strengthen market growth in Japan.

China Retinal Implant Market Insight

The China retinal implant market is growing rapidly, driven by increasing prevalence of retinal diseases, expanding elderly population, and rising investments in advanced healthcare technologies. Government initiatives to improve ophthalmic care infrastructure and promote medical innovation are significantly supporting market expansion. Increasing participation in clinical research and collaborations with global medtech companies are accelerating adoption of retinal implant technologies. In addition, growing awareness of vision restoration solutions among patients is boosting demand. Rapid advancements in biotechnology and AI-enabled medical devices are positioning China as one of the fastest-growing markets globally.

Retinal Implant Market Share

The retinal implant industry is primarily led by well-established companies, including:

- Cortigent (U.S.)

- Science Corporation (U.S.)

- Pixium Vision (France)

- VisionCare Ophthalmic Technologies (U.S.)

- Nano Retina (Israel)

- Retina Implant AG (Germany)

- Bionic Vision Technologies (Australia)

- Monash Vision Group (Australia)

- iBionics Inc. (Canada)

- Second Sight Medical Products (U.S.)

- Shanghai Artificial Vision Technology Co., Ltd. (China)

- Shenzhen SiBionic Technology Co., Ltd. (China)

- Kyoto University (Japan)

- Osaka University (Japan)

- Stanford University (U.S.)

- Harvard Medical School (U.S.)

- University College London (U.K.)

- University of Oxford (U.K.)

- EPFL – Swiss Federal Institute of Technology (Switzerland)

- Seoul National University Hospital (South Korea)

Latest Developments in Retinal Implant Market

- In June 2024, Science Corporation and academic partners continued advancing clinical development of next-generation PRIMA-based retinal implant systems, focusing on improving visual resolution and expanding patient eligibility. Ongoing studies demonstrated enhanced image processing capabilities through improved stimulation algorithms and upgraded implant hardware. The development reflects the shift toward AI-assisted, high-density photovoltaic retinal implants for more natural vision restoration. It also highlights increasing integration of computational vision decoding into implantable ophthalmic devices

- In May 2023, Pixium Vision, a key developer of subretinal implant technologies including PRIMA-based systems, entered insolvency proceedings due to financial constraints and delayed commercialization timelines. Despite strong clinical progress in retinal prosthesis development, the company struggled with funding challenges and long regulatory pathways. This development reflected the high-cost, long-gestation nature of retinal implant commercialization. It also led to increased acquisition interest in its neuroprosthetic vision technologies by other medtech players

- In February 2022, Second Sight Medical Products, the developer of the Argus II retinal prosthesis system, announced bankruptcy proceedings and restructuring, marking a major transition in the retinal implant industry. The company later transferred its assets into Cortigent while continuing development in cortical visual prosthesis technologies. This event highlighted the commercialization challenges, high costs, and limited adoption of first-generation retinal implants despite earlier clinical success. It also marked a strategic shift from retinal implants toward brain-based vision restoration systems

- In April 2021, researchers from Stanford University and collaborators published clinical results of the PRIMA wireless photovoltaic subretinal retinal implant, demonstrating partial vision restoration in patients with atrophic macular degeneration. The study confirmed that wireless microchip-based stimulation can restore form vision without external wired power systems, marking a major breakthrough in next-generation retinal prosthesis technology. This development significantly advanced the shift toward fully implantable, high-resolution vision restoration systems and strengthened confidence in photovoltaic retinal implant scalability

- In March 2021, UCLA and clinical collaborators reported advancement in the Orion cortical visual prosthesis system, achieving first-in-human implantation that enabled basic light perception in blind patients. The device bypasses damaged retinal structures and directly stimulates the visual cortex, expanding the vision restoration ecosystem beyond retinal implants. This development demonstrated feasibility for cortical-level prosthetic vision in cases where retinal implantation is not viable. It represented a significant breakthrough in neuroprosthetic vision research and opened new pathways for treating total blindness

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.