Global Retinal Vein Occlusion Market

Market Size in USD Billion

CAGR :

%

USD

18.17 Billion

USD

40.97 Billion

2025

2033

USD

18.17 Billion

USD

40.97 Billion

2025

2033

| 2026 –2033 | |

| USD 18.17 Billion | |

| USD 40.97 Billion | |

| % | |

|

Retinal Vein Occlusion Market Size

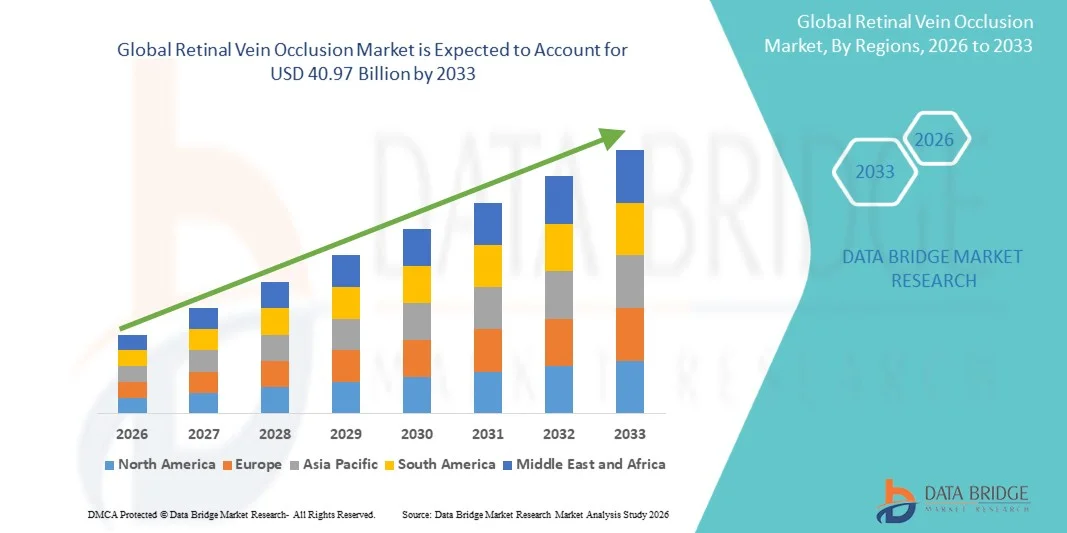

- The global retinal vein occlusion market size was valued at USD 18.17 billion in 2025and is expected to reach USD 40.97 billion by 2033, at a CAGR of 10.70% during the forecast period

- The market growth is largely fueled by the rising prevalence of diabetes, hypertension, and age-related eye disorders, along with continuous advancements in ophthalmic diagnostics and treatment technologies, leading to greater adoption of vision care solutions across healthcare settings

- Furthermore, growing patient awareness regarding early detection of retinal diseases, increasing demand for effective anti-VEGF therapies and corticosteroid treatments, and expanding access to specialized ophthalmology care are establishing Retinal Vein Occlusion solutions as an essential component of modern retinal disease management. These converging factors are accelerating the uptake of Retinal Vein Occlusion solutions, thereby significantly boosting the industry's growth

Retinal Vein Occlusion Market Analysis

- Retinal vein occlusion solutions, including anti-VEGF therapies, corticosteroid implants, laser photocoagulation, and diagnostic imaging technologies, are increasingly vital components of modern ophthalmic care due to their role in preserving vision, reducing macular edema, and preventing long-term retinal complications

- The escalating demand for retinal vein occlusion solutions is primarily fueled by the rising prevalence of diabetes, hypertension, glaucoma, and aging-related vascular eye disorders, along with increasing awareness regarding early diagnosis and treatment of retinal diseases

- North America dominated the retinal vein occlusion market with the largest revenue share of approximately 42.8% in 2025, characterized by advanced ophthalmology healthcare infrastructure, strong adoption of innovative retinal therapies, favorable reimbursement systems, and high awareness regarding vision preservation treatments across the U.S. and Canada

- Asia-Pacific is expected to be the fastest growing region in the retinal vein occlusion market during the forecast period due to increasing diabetic population, improving eye care infrastructure, rising healthcare expenditure, growing awareness of retinal disorders, and expanding access to advanced ophthalmic therapies across China, Japan, India, and Southeast Asia

- The Non-Ischemic segment held the largest market revenue share of 64.3% in 2025, driven by its higher prevalence compared with ischemic forms and better prognosis with timely intervention

Report Scope and Retinal Vein Occlusion Market Segmentation

|

Attributes |

Retinal Vein Occlusion Key Market Insights |

|

Segments Covered |

· By Type: Branch Retinal Artery Occlusion and Central Retinal Vein Occlusion · By Condition: Non-Ischemic and Ischemic · By Diagnosis: Optical Coherence Tomography (OCT), Fundoscopic Examination, Fluorescein Angiography, and Others · By Treatment: Anti-Vascular Endothelial Growth Factor, Corticosteroid Drugs, Laser Retinal Photocoagulation, and Others · By End User: Hospitals and Clinics, Research and Academics, and Others |

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· F. Hoffmann-La Roche Ltd. (Switzerland) · Regeneron Pharmaceuticals, Inc. (U.S.) · Bayer AG (Germany) · Novartis AG (Switzerland) · AbbVie Inc. (U.S.) · Pfizer Inc. (U.S.) · Bausch + Lomb Corporation (Canada) · Alimera Sciences, Inc. (U.S.) · Ocular Therapeutix, Inc. (U.S.) · Kodiak Sciences Inc. (U.S.) · Apellis Pharmaceuticals, Inc. (U.S.) · Oxurion NV (Belgium) · Santen Pharmaceutical Co., Ltd. (Japan) · Samsung Bioepis Co., Ltd. (South Korea) · Biocon Biologics Ltd. (India) · Teva Pharmaceutical Industries Ltd. (Israel) · Coherus BioSciences, Inc. (U.S.) · Adverum Biotechnologies, Inc. (U.S.) · Outlook Therapeutics, Inc. (U.S.) · Chengdu Kanghong Pharmaceutical Group Co., Ltd. (China) |

|

Market Opportunities |

· Rising Prevalence of Diabetes and Hypertension Creating Larger Patient Pool · Advancements in Biologics, Sustained-Release Therapies, and Emerging Market Access |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Retinal Vein Occlusion Market Trends

“Rising Adoption of Anti-VEGF Therapies and Advanced Retinal Imaging for Vision Preservation”

- A significant and accelerating trend in the global Retinal Vein Occlusion market is the increasing adoption of targeted therapies and modern retinal diagnostics for the management of branch retinal vein occlusion (BRVO) and central retinal vein occlusion (CRVO). Growing awareness regarding early intervention is helping improve visual outcomes and reduce long-term complications

- For instance, Regeneron Pharmaceuticals and F. Hoffmann-La Roche Ltd. have strengthened the market through anti-VEGF therapies such as Eylea and Lucentis, widely used for macular edema associated with retinal vein occlusion

- Increasing use of optical coherence tomography (OCT), fluorescein angiography, and AI-assisted retinal screening tools is improving diagnostic accuracy and enabling better treatment planning

- Physicians are increasingly favoring personalized treatment regimens, including treat-and-extend dosing schedules, to balance efficacy, patient convenience, and healthcare resource utilization

- Rising demand for long-acting formulations, sustained drug delivery implants, and combination therapies is further supporting innovation in this therapeutic area

- The trend toward earlier diagnosis, targeted biologic treatment, and technology-enabled monitoring is reshaping the Retinal Vein Occlusion market globally across hospitals, ophthalmology clinics, and ambulatory eye centers

Retinal Vein Occlusion Market Dynamics

Driver

“Growing Prevalence of Diabetes, Hypertension, and Age-Related Vascular Eye Disorders”

- The increasing global burden of diabetes, hypertension, atherosclerosis, and other cardiovascular disorders is a major driver for the Retinal Vein Occlusion market, as these conditions are key risk factors for retinal vascular blockage

- For instance, World Health Organization and International Diabetes Federation continue to highlight rising diabetes prevalence worldwide, contributing to higher demand for retinal disease diagnosis and treatment

- Aging populations in North America, Europe, Japan, and other developed regions are increasing the number of individuals at risk for retinal vein occlusion and associated macular edema

- Improved access to ophthalmic screening and specialist eye care is enabling earlier detection, resulting in faster treatment initiation and better preservation of vision

- Expanding healthcare expenditure and increasing patient awareness regarding preventable blindness are further supporting market growth in emerging economies

- In addition, strong clinical evidence supporting anti-VEGF injections and corticosteroid implants is encouraging physician confidence and wider therapeutic adoption

Restraint/Challenge

“High Treatment Burden, Repeated Injection Requirements, and Limited Access in Emerging Regions”

- Frequent intravitreal injections, regular follow-up visits, and long-term monitoring create a significant treatment burden for patients and healthcare providers, especially elderly populations

- For instance, many patients in lower-income regions face delayed access to premium anti-VEGF drugs due to affordability constraints, limited reimbursement coverage, or shortage of retinal specialists

- High therapy costs associated with branded biologics and advanced diagnostic imaging systems remain a barrier in cost-sensitive healthcare markets

- Fear of eye injections, transportation difficulties, and inconsistent adherence to follow-up schedules may reduce treatment continuity and affect clinical outcomes

- In some patients, incomplete response or recurrence of macular edema may require switching therapies or combining treatment approaches, increasing overall management complexity

- Overcoming these challenges through broader reimbursement access, long-acting therapies, improved patient education, and expansion of ophthalmic infrastructure will be essential for sustained market growth

Retinal Vein Occlusion Market Scope

The market is segmented on the basis of type, condition, diagnosis, treatment, and end user.

- By Type

On the basis of type, the Retinal Vein Occlusion market is segmented into Branch Retinal Artery Occlusion and Central Retinal Vein Occlusion. The Central Retinal Vein Occlusion segment dominated the largest market revenue share of 58.6% in 2025, driven by its higher disease severity, greater risk of vision loss, and increased requirement for long-term treatment. Patients with central retinal vein occlusion often need repeated anti-VEGF injections, imaging diagnostics, and close ophthalmic monitoring. Rising prevalence of hypertension, diabetes, and cardiovascular disorders is supporting segment growth. Increasing aging population globally further boosts diagnosis rates. Higher complication risk such as macular edema reinforces treatment demand. Strong availability of approved therapies supports continued market leadership.

The Branch Retinal Artery Occlusion segment is expected to witness the fastest growth rate of 22.4% from 2026 to 2033, driven by improving early diagnosis through retinal imaging and increased awareness of vascular eye diseases. Better management of milder and localized cases is expanding treatment volumes. Growing adoption of outpatient ophthalmology services supports growth. Rising screening among diabetic and elderly populations accelerates detection rates. Advances in minimally invasive retinal therapies further strengthen uptake. Increasing physician focus on preserving vision quality boosts demand. Continuous expansion of specialty eye care centers supports rapid growth.

- By Condition

On the basis of condition, the Retinal Vein Occlusion market is segmented into Non-Ischemic and Ischemic. The Non-Ischemic segment held the largest market revenue share of 64.3% in 2025, driven by its higher prevalence compared with ischemic forms and better prognosis with timely intervention. Many diagnosed patients present initially with non-ischemic disease requiring imaging follow-up and pharmacological management. Greater treatment responsiveness to anti-VEGF therapy supports segment dominance. Rising awareness of early visual symptoms is increasing consultations. Improved access to retinal specialists further strengthens demand. Lower complication rates encourage sustained treatment adherence.

The Ischemic segment is expected to witness the fastest CAGR of 24.1% from 2026 to 2033, driven by higher unmet medical need and severe complications requiring aggressive management. Ischemic cases are associated with retinal non-perfusion, neovascularization, and profound vision impairment. Growing use of advanced diagnostics is improving identification rates. Increasing need for combination therapies supports market growth. Expanding research into next-generation retinal treatments accelerates adoption. Rising elderly population with vascular comorbidities further boosts incidence. Enhanced specialist care pathways continue to drive expansion.

- By Diagnosis

On the basis of diagnosis, the Retinal Vein Occlusion market is segmented into Optical Coherence Tomography (OCT), Fundoscopic Examination, Fluorescein Angiography, and Others. The Optical Coherence Tomography (OCT) segment accounted for the largest market revenue share of 46.8% in 2025, driven by its non-invasive nature and high precision in detecting macular edema and retinal structural changes. OCT has become the standard monitoring tool for retinal vein occlusion patients undergoing therapy. Rapid image acquisition and detailed cross-sectional scans support strong adoption. Growing installation of OCT systems in eye clinics reinforces dominance. Increasing repeat imaging needs further boost utilization. Strong physician preference for real-time monitoring sustains leadership.

The Fluorescein Angiography segment is expected to witness the fastest growth rate of 23.6% from 2026 to 2033, driven by increasing need to assess retinal blood flow, leakage, and ischemic damage. It remains highly valuable for treatment planning in complex cases. Rising use in specialized retina centers supports growth. Improved digital angiography systems enhance efficiency and safety. Growing demand for accurate vascular mapping boosts adoption. Increasing severe retinal cases further support utilization. Continuous diagnostic innovation accelerates segment expansion.

- By Treatment

On the basis of treatment, the Retinal Vein Occlusion market is segmented into Antivascular Endothelial Growth Factor, Corticosteroid Drugs, Laser Retinal Photocoagulation, and Others. The Antivascular Endothelial Growth Factor segment dominated the largest market revenue share of 61.5% in 2025, driven by its strong efficacy in reducing macular edema and improving visual acuity. Anti-VEGF injections are considered the frontline treatment for many retinal vein occlusion patients. Frequent clinical adoption of branded biologics supports segment leadership. Strong physician confidence in evidence-based outcomes reinforces demand. Expanding reimbursement access in developed markets boosts treatment volumes. Ongoing innovation in longer-acting agents further strengthens dominance.

The Corticosteroid Drugs segment is expected to witness the fastest CAGR of 25.2% from 2026 to 2033, driven by increasing use in patients unresponsive to anti-VEGF therapy or requiring alternative management. Sustained-release steroid implants are gaining popularity in retinal practice. Rising preference for reduced injection frequency supports growth. Improved patient outcomes in chronic edema cases strengthen adoption. Expanding availability of ophthalmic steroid products accelerates uptake. Increasing specialist familiarity with adjunct treatment options boosts demand. Continued product development supports rapid expansion.

- By End User

On the basis of end user, the Retinal Vein Occlusion market is segmented into Hospitals and Clinics, Research and Academics, and Others. The Hospitals and Clinics segment held the largest market revenue share of 78.4% in 2025, driven by high patient dependence on ophthalmology departments for diagnosis, injections, laser treatment, and follow-up care. Most retinal vein occlusion cases are managed in clinical settings with specialized imaging equipment. Availability of retina specialists supports segment leadership. Rising outpatient ophthalmology visits further boost demand. Access to reimbursement-backed treatment pathways reinforces dominance. Growing eye disease burden supports continued revenue growth.

The Research and Academics segment is expected to witness the fastest CAGR of 21.8% from 2026 to 2033, driven by increasing clinical trials, retinal disease research, and innovation in imaging technologies. Academic centers are actively studying novel biologics, gene therapies, and precision diagnostics. Rising funding for ophthalmic research supports expansion. Collaboration between universities and pharmaceutical companies accelerates development. Growing interest in vision restoration therapies boosts activity levels. Increasing publication output and translational studies further strengthen growth. Continuous innovation pipelines support long-term segment momentum.

Retinal Vein Occlusion Market Regional Analysis

- North America dominated the retinal vein occlusion market with the largest revenue share of approximately 42.8% in 2025, characterized by advanced ophthalmology healthcare infrastructure, strong adoption of innovative retinal therapies, favorable reimbursement systems, and high awareness regarding vision preservation treatments across the U.S. and Canada. The region has also witnessed increasing use of anti-VEGF therapies, corticosteroid implants, and laser-based interventions for managing retinal vein occlusion and associated macular edema

- Ophthalmologists and healthcare providers in the region highly value the improved visual outcomes, minimally invasive treatment approaches, and early intervention strategies offered by modern retinal therapies. Growing preference for timely diagnosis and long-term retinal disease monitoring continues to strengthen market demand

- This widespread adoption is further supported by high healthcare expenditure, strong specialist retina care networks, increasing aging population, and rising prevalence of hypertension and diabetes-related eye complications, establishing North America as a leading market for retinal vein occlusion treatment solutions

U.S. Retinal Vein Occlusion Market Insight

The U.S. retinal vein occlusion market captured the largest revenue share in 2025 within North America, fueled by strong adoption of advanced retinal therapeutics, widespread access to ophthalmology specialists, and increasing awareness regarding early vision-saving treatment. Physicians are increasingly prioritizing intravitreal anti-VEGF injections and corticosteroid therapies to manage retinal edema and preserve visual acuity. The growing preference for outpatient ophthalmic procedures, combined with robust demand across retina clinics, hospitals, and ambulatory surgery centers, further propels the market. Moreover, increasing integration of OCT imaging and AI-supported retinal diagnostics is significantly contributing to market expansion.

Europe Retinal Vein Occlusion Market Insight

The Europe retinal vein occlusion market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by rising prevalence of retinal vascular disorders, increasing aging population, and strong healthcare support for vision care services. The region’s advanced ophthalmology care systems and structured treatment pathways are fostering adoption of retinal therapies. European healthcare providers are also focused on reducing preventable vision loss through early diagnosis and effective treatment strategies. The market is experiencing significant growth across hospitals, specialty eye clinics, and academic medical centers.

U.K. Retinal Vein Occlusion Market Insight

The U.K. retinal vein occlusion market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by increasing awareness of retinal disorders and growing NHS investment in ophthalmic services. In addition, rising demand for anti-VEGF therapy and advanced retinal imaging is encouraging broader treatment adoption. The UK’s expanding specialist eye care network and emphasis on preserving patient quality of life are expected to continue stimulating market growth.

Germany Retinal Vein Occlusion Market Insight

The Germany retinal vein occlusion market is expected to expand at a considerable CAGR during the forecast period, fueled by strong healthcare infrastructure, rising burden of age-related retinal disease, and increasing demand for advanced ophthalmic treatment solutions. Germany’s well-developed specialist care systems and emphasis on evidence-based retinal management promote the adoption of innovative therapies. Integration of high-resolution imaging systems and outpatient retinal treatment centers is also becoming increasingly prevalent.

Asia-Pacific Retinal Vein Occlusion Market Insight

The Asia-Pacific retinal vein occlusion market is poised to grow at the fastest CAGR during the forecast period of 2026 to 2033, driven by increasing diabetic population, improving eye care infrastructure, rising healthcare expenditure, growing awareness of retinal disorders, and expanding access to advanced ophthalmic therapies across China, Japan, India, and Southeast Asia. The region’s growing elderly population and increasing incidence of vascular disorders are accelerating demand for retinal treatment services. Furthermore, expanding hospital networks and government vision care initiatives are improving patient access to advanced therapies.

Japan Retinal Vein Occlusion Market Insight

The Japan retinal vein occlusion market is gaining momentum due to the country’s aging population, advanced healthcare system, and strong focus on preserving vision health among elderly patients. Japanese ophthalmologists place significant emphasis on early diagnosis and minimally invasive retinal treatments, driving adoption of anti-VEGF therapies and precision imaging systems. Integration of advanced ophthalmic diagnostics is fueling market growth.

China Retinal Vein Occlusion Market Insight

The China retinal vein occlusion market accounted for the largest market revenue share in Asia Pacific in 2025, attributed to the country’s expanding eye care infrastructure, increasing diabetic and hypertensive patient population, rising healthcare expenditure, and growing adoption of advanced retinal therapies. China is witnessing increasing use of intravitreal therapies and modern retinal imaging technologies in major urban hospitals. Government healthcare reforms, rising awareness of preventable blindness, and improving access to specialty ophthalmology care are key factors propelling market growth in China.

Retinal Vein Occlusion Market Share

The Retinal Vein Occlusion industry is primarily led by well-established companies, including:

- F. Hoffmann-La Roche Ltd. (Switzerland)

- Regeneron Pharmaceuticals, Inc. (U.S.)

- Bayer AG (Germany)

- Novartis AG (Switzerland)

- AbbVie Inc. (U.S.)

- Pfizer Inc. (U.S.)

- Bausch + Lomb Corporation (Canada)

- Alimera Sciences, Inc. (U.S.)

- Ocular Therapeutix, Inc. (U.S.)

- Kodiak Sciences Inc. (U.S.)

- Apellis Pharmaceuticals, Inc. (U.S.)

- Oxurion NV (Belgium)

- Santen Pharmaceutical Co., Ltd. (Japan)

- Samsung Bioepis Co., Ltd. (South Korea)

- Biocon Biologics Ltd. (India)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Coherus BioSciences, Inc. (U.S.)

- Adverum Biotechnologies, Inc. (U.S.)

- Outlook Therapeutics, Inc. (U.S.)

- Chengdu Kanghong Pharmaceutical Group Co., Ltd. (China)

Latest Developments in Global Retinal Vein Occlusion Market

- In July 2021, clinical ophthalmology studies continued to support anti-VEGF therapies such as Eylea (aflibercept) and Lucentis (ranibizumab) as first-line treatment options for macular edema secondary to retinal vein occlusion, reinforcing their dominant role in preserving and improving vision outcomes globally

- In May 2023, Roche announced that the U.S. Food and Drug Administration accepted the supplemental Biologics License Application for Vabysmo (faricimab) for the treatment of macular edema following retinal vein occlusion. The filing was supported by positive Phase III BALATON and COMINO trial data showing non-inferior visual acuity gains versus aflibercept

- In October 2023, the U.S. Food and Drug Administration approved Roche’s Vabysmo (faricimab) for the treatment of macular edema following retinal vein occlusion. The approval marked the third indication for Vabysmo and introduced the first bispecific antibody therapy for patients with retinal vein occlusion

- In July 2024, the European Commission approved Vabysmo for visual impairment due to macular edema secondary to branch retinal vein occlusion and central retinal vein occlusion. The approval expanded access across Europe and strengthened Roche’s position in the retinal vascular disease market

- In March 2025, published market and clinical reviews highlighted growing momentum for dual-pathway biologics and next-generation retinal therapeutics in retinal vein occlusion management, with faricimab receiving strong attention for efficacy and extended dosing potential

- In October 2025, peer-reviewed reviews emphasized that retinal vein occlusion remained the second most common retinal vascular cause of vision loss after diabetic retinopathy, sustaining strong commercial focus on innovative injectable therapies, sustained-release systems, and pipeline biologics

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.