Global Rheumatoid Arthritis Drugs Market

Market Size in USD Billion

CAGR :

%

USD

60.02 Billion

USD

284.10 Billion

2025

2033

USD

60.02 Billion

USD

284.10 Billion

2025

2033

| 2026 - 2033 | |

| USD 60.02 Billion | |

| USD 284.10 Billion | |

| % | |

|

Rheumatoid Arthritis Drugs Market Overview

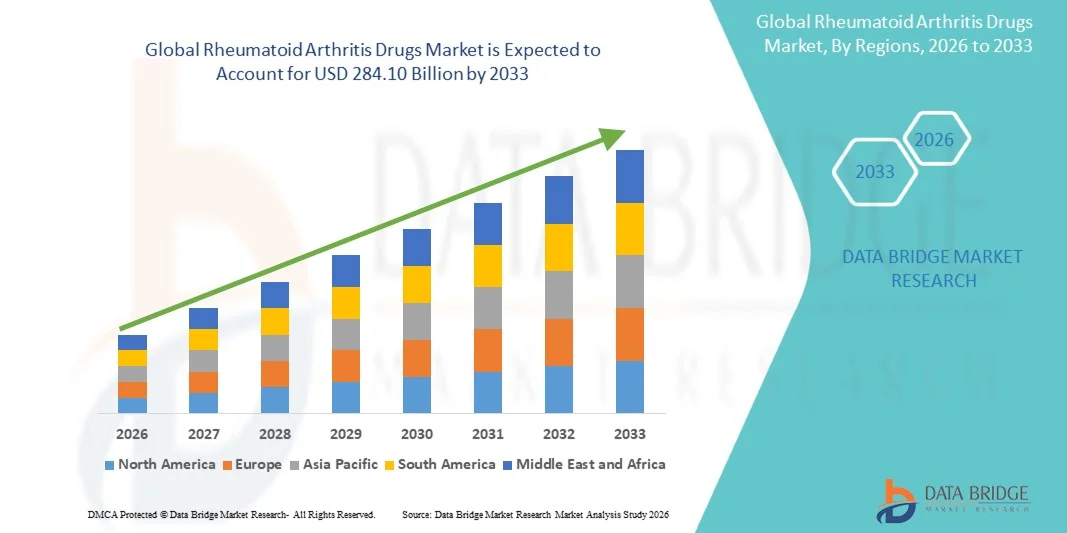

The Rheumatoid Arthritis Drugs Market was valued at USD 60.02 billion in 2025 and is projected to reach USD 284.10 billion by 2033, growing at a CAGR of 21.45% from 2026 to 2033. The market is experiencing steady growth driven by the rising global prevalence of rheumatoid arthritis, increasing aging population, and growing awareness regarding early diagnosis and long-term disease management. Expanding adoption of biologics and targeted synthetic disease-modifying antirheumatic drugs (DMARDs) is significantly improving treatment outcomes by slowing disease progression and reducing joint damage.

The increasing burden of autoimmune disorders, combined with improved access to healthcare and advancements in immunology-based research, is encouraging healthcare providers and pharmaceutical companies to develop more effective and personalized treatment options. The shift from conventional synthetic DMARDs to biologics and Janus kinase (JAK) inhibitors is transforming the treatment landscape, offering better efficacy for patients with moderate to severe rheumatoid arthritis. In addition, rising healthcare expenditure, ongoing drug pipeline developments, and increasing approvals of biosimilars are further accelerating market expansion across both developed and emerging regions.

Key Market Trends & Insights

- North America dominated the Rheumatoid Arthritis Drugs Market with the largest revenue share of 39.64% in 2025, driven by a high prevalence of rheumatoid arthritis, advanced healthcare infrastructure, strong adoption of biologics and targeted therapies, favorable reimbursement policies, and the presence of leading pharmaceutical companies. Increasing diagnosis rates and expanding access to advanced treatment options such as JAK inhibitors and biologic DMARDs further support regional market growth.

- The Oral segment dominated the market with a share of 44.18% in 2025, driven by the widespread use of DMARDs and JAK inhibitors in oral formulations.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 8.3% from 2026 to 2033, fueled by rising healthcare expenditure, increasing awareness of autoimmune diseases, expanding patient access to advanced therapies, and improving healthcare infrastructure across China, India, Japan, and Southeast Asia.

- JAK Inhibitors are projected to be the fastest-growing drug class, registering a CAGR of 8.0%, due to their oral administration benefits, rapid onset of action, and increasing preference for targeted synthetic DMARDs in patients with inadequate response to conventional therapies.

- The DMARDs segment dominated the drug class category with a 52.37% revenue share in 2025, driven by their central role in slowing disease progression and their widespread use as first-line and combination therapy options in rheumatoid arthritis management.

- The Oral route of administration accounted for 57.18% of the market in 2025, supported by higher patient compliance, convenience, and increasing availability of oral DMARDs and JAK inhibitors.

- The Specialty Clinics segment held a 46.85% revenue share in 2025, driven by increasing patient preference for specialized rheumatology care, advanced diagnostic capabilities, and personalized treatment approaches offered in these settings.

Market Size & Forecast

- Global Market Value (2025): USD 60.02 Billion

- Expected Market Value (2033): USD 284.10 Billion

- Forecast CAGR (2026–2033): 21.45%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Rheumatoid Arthritis Drugs Market Segmentation

|

Attributes |

Rheumatoid Arthritis Drugs Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· AbbVie Inc. (U.S.) · Pfizer Inc. (U.S.) · Amgen Inc. (U.S.) · Johnson & Johnson (U.S.) · Bristol Myers Squibb (U.S.) · Novartis AG (Switzerland) · Roche Holding AG (Switzerland) · Eli Lilly and Company (U.S.) · Sanofi S.A. (France) · Merck & Co., Inc. (U.S.) · UCB S.A. (Belgium) · AstraZeneca plc (U.K.) · GlaxoSmithKline plc (U.K.) · Biogen Inc. (U.S.) · Gilead Sciences, Inc. (U.S.) · Teva Pharmaceutical Industries Ltd. (Israel) · Samsung Bioepis Co., Ltd. (South Korea) · Celltrion Inc. (South Korea) · Fresenius Kabi AG (Germany) · Boehringer Ingelheim (Germany) · Sun Pharmaceutical Industries Ltd. (India) · Lupin Limited (India) · Dr. Reddy’s Laboratories Ltd. (India) · Cipla Ltd. (India) · Almirall S.A. (Spain) · Sandoz (Novartis Division) (Switzerland) · Horizon Therapeutics plc (Ireland/U.S.) · Astellas Pharma Inc. (Japan) · Takeda Pharmaceutical Company Limited (Japan) · Mitsubishi Tanabe Pharma Corporation (Japan) · Regeneron Pharmaceuticals, Inc. (U.S.) |

|

Market Opportunities |

· Rising Adoption of Biologics and Targeted Therapies · Expanding Biosimilars Market and Cost-Effective Treatment Access · Growing Demand for Personalized and Early-Stage Treatment Approaches |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Rheumatoid Arthritis Drugs Market Trends

Trend: Increasing Shift Toward Biologics and Targeted Synthetic Therapies

The Rheumatoid Arthritis (RA) Drugs market is witnessing a strong shift toward biologic agents and targeted synthetic DMARDs, driven by their superior efficacy in controlling disease progression and improving long-term patient outcomes. Biologics such as TNF inhibitors, IL-6 inhibitors, and B-cell targeted therapies are increasingly being used for moderate-to-severe RA cases, particularly in patients who show inadequate response to conventional DMARDs like methotrexate.

In addition, the adoption of Janus Kinase (JAK) inhibitors is accelerating due to their oral administration convenience and rapid onset of action. According to clinical rheumatology studies, early biologic intervention has been associated with improved remission rates and reduced joint damage progression, further supporting their growing adoption. Increasing prevalence of autoimmune diseases globally—affecting nearly 18–20 million people with rheumatoid arthritis worldwide—continues to drive demand for advanced treatment options.

Rheumatoid Arthritis Drugs Market Dynamics

Key Market Driver: Rising Prevalence of Autoimmune and Chronic Inflammatory Disorders

The increasing global burden of rheumatoid arthritis and other autoimmune diseases is a major driver of market growth. RA affects approximately 0.5–1% of the global population, with higher prevalence observed in women and aging populations. Factors such as genetic susceptibility, environmental triggers, smoking, and obesity contribute to disease development and progression.

Growing awareness, earlier diagnosis, and improved access to rheumatology care have significantly increased treatment uptake. In addition, the expansion of reimbursement coverage for biologics and targeted therapies in developed markets such as North America and Europe is improving patient access. Pharmaceutical advancements and continuous pipeline development by major companies such as AbbVie, Amgen, Pfizer, and Roche are further accelerating innovation and market expansion.

Key Restraint/Challenge: High Cost and Limited Accessibility of Advanced Therapies

A major challenge in the Rheumatoid Arthritis Drugs market is the high cost of biologics and JAK inhibitors, which limits accessibility, especially in low- and middle-income countries. Biologic therapies often require long-term administration and can cost several thousand dollars annually per patient, creating a significant financial burden on healthcare systems and individuals.

In addition, biosimilar competition, regulatory complexities, and variations in reimbursement policies across regions impact market penetration. Side effects associated with long-term immunosuppression, such as increased infection risk, also require careful patient monitoring, further increasing treatment complexity and healthcare costs.

Key Market Opportunity: Expansion of Biosimilars and Personalized Medicine Approaches

The growing adoption of biosimilars presents a major opportunity for improving affordability and expanding access to rheumatoid arthritis treatments. Biosimilars for key biologics such as adalimumab and infliximab are gaining traction, particularly in Europe and emerging markets, significantly reducing treatment costs.

At the same time, advancements in precision medicine and biomarker-driven therapy selection are enabling more personalized treatment approaches. Pharmaceutical companies are increasingly investing in targeted drug development, combination therapies, and patient stratification strategies to improve clinical outcomes. Expanding healthcare infrastructure in Asia-Pacific, along with rising healthcare expenditure and government support for chronic disease management, is expected to further accelerate market growth globally.

Rheumatoid Arthritis Drugs Market Scope

The Rheumatoid Arthritis Drugs market is segmented on the basis of Drugs, Route of Administration, End-Users, and Distribution Channel.

- By Drugs

On the basis of drugs, the Rheumatoid Arthritis Drugs Market is segmented into Nonsteroidal Anti-Inflammatory Drugs (NSAIDs), Corticosteroids, Disease-Modifying Antirheumatic Drugs (DMARDs), Janus Kinase (JAK) Inhibitors, Biologic Agents, and Others. The DMARDs segment dominated the market with a share of 38.62% in 2025, driven by their strong efficacy in slowing disease progression and reducing long-term joint damage. These drugs remain the first-line treatment option in most clinical guidelines for rheumatoid arthritis management. The increasing adoption of methotrexate-based combination therapies is further strengthening segment dominance. Rising awareness of early diagnosis and long-term disease control is boosting demand for DMARDs globally. Biologic agents are increasingly used in moderate-to-severe cases where conventional therapies fail. JAK inhibitors are gaining traction due to oral administration convenience and rapid symptom relief. NSAIDs continue to be widely used for pain and inflammation management in early-stage patients. Corticosteroids are frequently used for short-term flare control. Increasing R&D investment is leading to next-generation targeted therapies. Expanding biologics pipeline is improving treatment outcomes. Growing physician preference for personalized treatment is supporting segment expansion. Overall, rising disease burden is driving sustained demand across all drug classes.

The Biologic Agents segment is projected to register the fastest growth with a CAGR of 8.4% from 2026 to 2033, driven by increasing adoption of targeted immunotherapy approaches. These drugs offer high efficacy in patients resistant to conventional DMARDs. Rising approvals of biosimilars are improving affordability and accessibility. Expanding use in combination therapy is enhancing treatment response rates. Increasing prevalence of moderate-to-severe rheumatoid arthritis is supporting demand growth. Pharmaceutical companies are investing heavily in monoclonal antibody development. Advancements in TNF inhibitors, IL inhibitors, and B-cell therapies are expanding treatment options. Growing physician preference for precision medicine is accelerating adoption. Strong clinical trial pipeline is expected to introduce next-generation biologics. Improved patient compliance due to reduced dosing frequency is boosting usage. Expanding healthcare infrastructure in emerging economies is increasing penetration. Overall, biologics are expected to remain the most dynamic segment.

- By Route of Administration

On the basis of route of administration, the market is segmented into Oral, Parenteral, Topical, and Others. The Oral segment dominated the market with a share of 44.18% in 2025, driven by the widespread use of DMARDs and JAK inhibitors in oral formulations. Oral administration remains the most preferred route due to ease of use and better patient compliance. It reduces the need for hospital visits compared to injectable therapies. Increasing adoption of methotrexate tablets and JAK inhibitors is strengthening growth. Parenteral therapies, especially biologics, are widely used in hospital settings. Topical formulations are used for localized symptom relief but have limited systemic efficacy. Growing preference for home-based treatment is supporting oral drug adoption. Rising elderly population is increasing demand for convenient therapies. Improved drug formulations are enhancing absorption and efficacy. Physicians prefer oral therapies for long-term maintenance treatment. Expanding pharmacy distribution networks are supporting accessibility. Overall, oral therapies remain the backbone of rheumatoid arthritis management.

The Parenteral segment is expected to witness the fastest growth with a CAGR of 8.1% from 2026 to 2033, driven by increasing adoption of biologic injections and infusion therapies. These treatments provide high efficacy in moderate-to-severe rheumatoid arthritis cases. Rising hospital-based biologic administration is supporting growth. Development of subcutaneous self-injectable formulations is improving patient convenience. Increasing approval of biosimilars is expanding treatment access. Growth in hospital infusion centers is further accelerating adoption. Strong clinical efficacy compared to oral drugs is driving physician preference. Expanding insurance coverage for biologics is improving affordability. Advances in drug delivery systems are enhancing safety and compliance. Increasing prevalence of refractory rheumatoid arthritis cases is boosting demand. Pharmaceutical innovations are expanding injectable portfolios. Overall, parenteral therapies are gaining strong clinical acceptance.

- By End-Users

On the basis of end-users, the market is segmented into Hospitals, Specialty Clinics, and Others. The Hospitals segment dominated the market with a share of 52.36% in 2025, driven by high patient inflow and availability of advanced diagnostic and treatment facilities. Hospitals serve as primary centers for biologic infusion and advanced RA management. Presence of rheumatology specialists supports accurate disease monitoring. Increasing hospitalization rates for severe RA cases is driving demand. Hospitals also manage complex combination therapy cases. Availability of reimbursement support is boosting patient access. Growing use of infusion-based biologics is strengthening hospital dominance. Integration of electronic health records improves treatment tracking. Strong pharmaceutical supply chains support drug availability. Hospitals are key centers for clinical trials and advanced therapies. Rising healthcare infrastructure investment is further enhancing capacity. Overall, hospitals remain the primary treatment hub.

The Specialty Clinics segment is projected to grow at the fastest CAGR of 8.6% from 2026 to 2033, driven by increasing preference for specialized rheumatology care. These clinics offer personalized and long-term disease management. Rising patient preference for outpatient care is supporting growth. Improved access to specialist physicians is enhancing treatment outcomes. Growing adoption of biologics in outpatient settings is accelerating demand. Lower treatment costs compared to hospitals are boosting adoption. Expansion of private healthcare networks is supporting clinic growth. Increasing awareness of early diagnosis is driving patient visits. Advanced diagnostic capabilities in clinics are improving care efficiency. Shorter waiting times compared to hospitals are attracting patients. Rising urban healthcare infrastructure is further supporting expansion. Overall, specialty clinics are becoming key outpatient treatment centers.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into Hospital Pharmacy, Retail Pharmacy, and Others. The Hospital Pharmacy segment dominated the market with a share of 55.14% in 2025, driven by high distribution of biologics and injectable therapies through hospital networks. Hospital pharmacies ensure proper storage and handling of temperature-sensitive drugs. Increasing inpatient treatments support strong demand. Direct linkage with infusion centers enhances drug availability. Bulk procurement by hospitals improves supply efficiency. Strong reimbursement frameworks support hospital pharmacy dominance. Growing use of specialty drugs is increasing hospital dispensing. Centralized procurement systems improve cost control. Hospital pharmacies also support clinical trial drug distribution. Increasing biologic usage strengthens this channel further. Regulatory compliance requirements favor hospital-based dispensing. Overall, hospital pharmacies remain the key distribution channel.

The Retail Pharmacy segment is expected to register the fastest growth with a CAGR of 8.2% from 2026 to 2033, driven by increasing adoption of oral DMARDs and JAK inhibitors. Rising preference for home-based treatment is supporting retail expansion. Improved drug accessibility through pharmacy chains is boosting sales. Growth of e-pharmacy platforms is further accelerating distribution. Increasing patient awareness is driving self-managed treatment adoption. Expanding insurance coverage is improving affordability. Convenience of repeat prescription refills is supporting demand. Rising chronic disease management trends are boosting long-term drug sales. Expansion of retail healthcare infrastructure in emerging markets is driving growth. Digital health integration is improving prescription fulfillment. Strong growth in generic drug availability is enhancing affordability. Overall, retail pharmacies are becoming increasingly important in outpatient drug distribution.

Rheumatoid Arthritis Drugs Market Regional Analysis

North America dominated the Rheumatoid Arthritis Drugs Market and accounted for the largest revenue share of 39.64% in 2025, driven by a high prevalence of rheumatoid arthritis, advanced healthcare infrastructure, strong adoption of biologics and targeted therapies, favorable reimbursement policies, and the presence of leading pharmaceutical companies. The region benefits from early diagnosis rates, widespread access to rheumatology care, and strong integration of advanced treatment options such as biologic DMARDs and JAK inhibitors. Increasing healthcare expenditure and continuous drug innovation further support sustained market growth across North America.

U.S. Rheumatoid Arthritis Drugs Market Insight

The U.S. Rheumatoid Arthritis Drugs market is witnessing strong growth due to rising prevalence of autoimmune disorders and increasing adoption of advanced biologic and targeted synthetic therapies. The country’s robust pharmaceutical ecosystem, strong clinical research activity, and extensive insurance coverage for chronic disease management are supporting market expansion. In addition, continuous drug approvals by regulatory bodies and strong pipeline development by major players such as AbbVie, Pfizer, Amgen, and Johnson & Johnson are accelerating treatment innovation and patient access.

Europe Rheumatoid Arthritis Drugs Market Insight

The Europe Rheumatoid Arthritis Drugs market remains a major contributor to global revenue, driven by strong public healthcare systems, increasing geriatric population, and growing adoption of advanced immunotherapies. The region benefits from structured reimbursement frameworks and strong clinical guidelines promoting early treatment initiation. Rising awareness of autoimmune diseases and expanding access to biologics and biosimilars continue to support market growth across hospitals and specialty care centers.

U.K. Rheumatoid Arthritis Drugs Market Insight

The U.K. Rheumatoid Arthritis Drugs market is experiencing steady growth, supported by the National Health Service (NHS) framework, increasing incidence of rheumatoid arthritis, and rising use of biologic therapies and JAK inhibitors. Expanded access to biosimilars has improved treatment affordability, while growing emphasis on early diagnosis and long-term disease management is strengthening adoption of advanced therapies across rheumatology centers.

Germany Rheumatoid Arthritis Drugs Market Insight

The Germany Rheumatoid Arthritis Drugs market is expanding steadily due to strong healthcare infrastructure, high awareness of autoimmune diseases, and increasing use of biologics and biosimilars. The country’s well-established pharmaceutical manufacturing base and strong focus on clinical innovation are supporting drug accessibility and development. In addition, rising adoption of precision medicine approaches is improving treatment outcomes for rheumatoid arthritis patients.

Asia-Pacific Rheumatoid Arthritis Drugs Market Insight

The Asia-Pacific Rheumatoid Arthritis Drugs market is expected to witness the fastest growth, registering a CAGR of 8.3% from 2026 to 2033, fueled by rising healthcare expenditure, increasing awareness of autoimmune diseases, expanding access to advanced therapies, and improving healthcare infrastructure across China, India, Japan, and Southeast Asia. Growing patient population, improving diagnostic rates, and increasing availability of biologics and biosimilars are further driving regional market expansion.

Japan Rheumatoid Arthritis Drugs Market Insight

The Japan Rheumatoid Arthritis Drugs market is witnessing consistent growth due to a rapidly aging population and high prevalence of autoimmune disorders. The country’s advanced healthcare system, strong adoption of biologic therapies, and increasing use of JAK inhibitors are supporting treatment innovation. In addition, strong clinical research activity and government support for chronic disease management are further enhancing market growth.

China Rheumatoid Arthritis Drugs Market Insight

The China Rheumatoid Arthritis Drugs market is growing rapidly, driven by increasing prevalence of autoimmune diseases, improving healthcare infrastructure, and rising adoption of advanced treatment options. Expanding access to biologics and biosimilars, along with growing government support for chronic disease management, is significantly boosting market demand. In addition, rising pharmaceutical investments and increasing awareness of early diagnosis are positioning China as a key growth market in the region.

Rheumatoid Arthritis Drugs Market Share

The Rheumatoid Arthritis Drugs industry is primarily led by well-established companies, including:

- AbbVie Inc. (U.S.)

- Pfizer Inc. (U.S.)

- Amgen Inc. (U.S.)

- Johnson & Johnson (U.S.)

- Bristol Myers Squibb (U.S.)

- Novartis AG (Switzerland)

- Roche Holding AG (Switzerland)

- Eli Lilly and Company (U.S.)

- Sanofi S.A. (France)

- Merck & Co., Inc. (U.S.)

- UCB S.A. (Belgium)

- AstraZeneca plc (U.K.)

- GlaxoSmithKline plc (U.K.)

- Biogen Inc. (U.S.)

- Gilead Sciences, Inc. (U.S.)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Samsung Bioepis Co., Ltd. (South Korea)

- Celltrion Inc. (South Korea)

- Fresenius Kabi AG (Germany)

- Boehringer Ingelheim (Germany)

- Sun Pharmaceutical Industries Ltd. (India)

- Lupin Limited (India)

- Dr. Reddy’s Laboratories Ltd. (India)

- Cipla Ltd. (India)

- Almirall S.A. (Spain)

- Sandoz (Novartis Division) (Switzerland)

- Horizon Therapeutics plc (Ireland/U.S.)

- Astellas Pharma Inc. (Japan)

- Takeda Pharmaceutical Company Limited (Japan)

- Mitsubishi Tanabe Pharma Corporation (Japan)

- Regeneron Pharmaceuticals, Inc. (U.S.)

Latest Developments in Rheumatoid Arthritis Drugs Market

- In September 2021, the U.S. Food and Drug Administration (FDA) announced a class-wide boxed warning update for Janus Kinase (JAK) inhibitors, including tofacitinib (Xeljanz), baricitinib (Olumiant), and upadacitinib (Rinvoq), highlighting increased risks of serious heart-related events, cancer, blood clots, and death. This regulatory action significantly impacted prescribing patterns and strengthened pharmacovigilance requirements across rheumatoid arthritis therapies

- In January 2022, the European Medicines Agency’s Pharmacovigilance Risk Assessment Committee (PRAC) recommended restrictions on the use of JAK inhibitors for chronic inflammatory disorders, including rheumatoid arthritis. The recommendation limited their use to patients who had inadequate response or intolerance to at least one disease-modifying antirheumatic drug (DMARD), reshaping treatment guidelines across Europe

- In January 2023, Amgen announced the U.S. launch of Amjevita (adalimumab-atto), the first biosimilar of AbbVie’s Humira to enter the U.S. market. This marked a major milestone in the rheumatoid arthritis biologics segment, introducing cost-effective competition and accelerating biosimilar penetration in autoimmune disease treatment

- In July 2023, Boehringer Ingelheim launched Cyltezo (adalimumab-adbm) in the United States as an interchangeable biosimilar to Humira following FDA approval. The launch strengthened biosimilar competition and expanded access to affordable anti-TNF biologic therapy for rheumatoid arthritis patients

- In October 2023, Sandoz announced the U.S. launch of Hyrimoz (adalimumab-adaz), further expanding the wave of Humira biosimilars entering the market after patent exclusivity loss. This development significantly increased pricing pressure in the biologics segment and improved treatment accessibility for chronic autoimmune conditions

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.