Global Scoliosis Treatment Market

Market Size in USD Billion

CAGR :

%

USD

191.50 Billion

USD

454.20 Billion

2025

2033

USD

191.50 Billion

USD

454.20 Billion

2025

2033

| 2026 –2033 | |

| USD 191.50 Billion | |

| USD 454.20 Billion | |

| % | |

|

Scoliosis Treatment Market Size

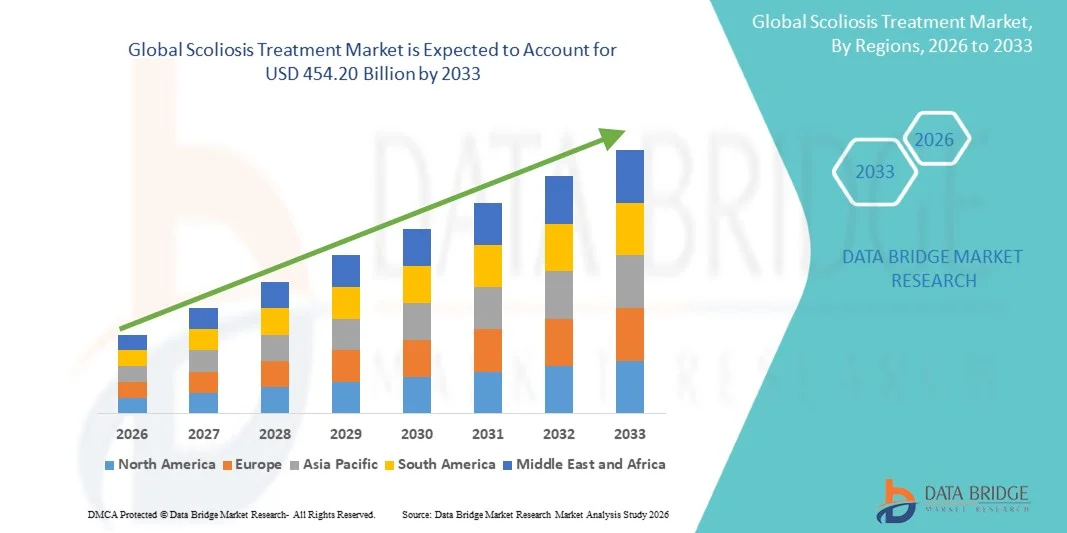

- The global scoliosis treatment market size was valued at USD 191.5 billion in 2025 and is expected to reach USD 454.20 billion by 2033, at a CAGR of 11.40% during the forecast period

- The market growth is largely fueled by the increasing prevalence of spinal deformities such as scoliosis, along with advancements in medical imaging, bracing technologies, and minimally invasive surgical procedures, leading to improved diagnosis and treatment outcomes

- Furthermore, rising awareness about early detection, growing adoption of non-surgical and corrective treatment options, and increasing healthcare expenditure are establishing scoliosis treatment as a critical component of orthopedic care. These converging factors are accelerating the uptake of Scoliosis Treatment solutions, thereby significantly boosting the industry's growth

Scoliosis Treatment Market Analysis

- Scoliosis treatment, involving bracing, physical therapy, and surgical correction procedures, is increasingly vital in modern orthopedic care due to the rising prevalence of spinal deformities, especially among adolescents, and growing awareness about early diagnosis and intervention

- The escalating demand for scoliosis treatment is primarily fueled by advancements in orthopedic surgery techniques, increasing adoption of minimally invasive procedures, and rising awareness regarding posture-related spinal disorders

- North America dominated the scoliosis treatment market with the largest revenue share of approximately 38.9% in 2025, characterized by advanced healthcare infrastructure, high adoption of corrective surgeries and bracing systems, and strong presence of specialized orthopedic centers, with the U.S. witnessing substantial growth driven by early screening programs and improved treatment accessibility

- Asia-Pacific is expected to be the fastest growing region in the scoliosis treatment market during the forecast period, with a projected CAGR of around 9.6%, due to rising healthcare expenditure, increasing awareness of spinal disorders, expanding pediatric population, and improving access to orthopedic care

- The oral segment held the largest market revenue share of 63.2% in 2025, driven by widespread use of oral medications for pain management and supportive therapy in scoliosis patients

Report Scope and Scoliosis Treatment Market Segmentation

|

Attributes |

Scoliosis Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Scoliosis Treatment Market Trends

“Advancements in Non-Invasive Therapies and Personalized Spine Care”

- A significant and accelerating trend in the global scoliosis treatment market is the increasing adoption of non-invasive treatment approaches and personalized spine care solutions aimed at improving patient outcomes and reducing surgical interventions

- For instance, leading healthcare institutions such as Mayo Clinic and Johns Hopkins Medicine are actively involved in developing advanced scoliosis management protocols, including bracing systems and minimally invasive surgical techniques

- The growing use of modern scoliosis braces, such as 3D-printed and custom-fitted orthotic devices, is significantly improving treatment compliance and effectiveness, especially in adolescent patients

- In addition, advancements in imaging technologies such as EOS imaging systems and AI-assisted radiological assessment (clinical use) are enabling earlier and more precise diagnosis of spinal curvature progression

- The integration of physiotherapy-based interventions, including Schroth method exercises and rehabilitation programs, is gaining strong clinical acceptance for mild to moderate scoliosis cases

- This shift toward conservative, patient-specific, and technology-supported treatment approaches is reshaping the Scoliosis Treatment market and improving long-term clinical outcomes

Scoliosis Treatment Market Dynamics

Driver

“Rising Prevalence of Spinal Disorders and Increasing Awareness of Early Diagnosis”

- The increasing prevalence of scoliosis across pediatric and adolescent populations is a major driver fueling the growth of the scoliosis treatment market globally

- For instance, organizations such as World Health Organization highlight the growing burden of musculoskeletal disorders, including spinal deformities, which require early intervention and long-term management

- Rising awareness among parents, schools, and healthcare providers regarding early detection of spinal curvature is leading to increased diagnosis rates

- In addition, improvements in screening programs in schools and pediatric healthcare settings are supporting earlier identification of scoliosis cases

- The growing availability of advanced bracing systems and improved surgical outcomes is further encouraging treatment adoption

- Furthermore, increasing healthcare expenditure and better access to orthopedic care are contributing significantly to market growth

Restraint/Challenge

“High Cost of Advanced Treatments and Limited Access to Specialized Care”

- One of the major challenges in the Scoliosis Treatment market is the high cost associated with advanced surgical procedures and custom orthopedic devices

- The affordability of long-term treatment, including bracing, physiotherapy, and surgical correction, remains a concern, particularly in low- and middle-income regions

- For instance, In addition, limited access to specialized orthopedic surgeons and spine care centers in rural areas restricts timely diagnosis and treatment

- Delayed diagnosis can lead to disease progression, increasing the complexity and cost of intervention

- Variability in treatment outcomes and the need for long-term follow-up care also add to the overall treatment burden

- Addressing these challenges through improved healthcare infrastructure, expanded screening programs, and affordable treatment solutions will be essential for sustained growth in the Scoliosis Treatment market

Scoliosis Treatment Market Scope

The market is segmented on the basis of product, types, treatment, route of administration, and end-users.

• By Product

On the basis of product, the Scoliosis Treatment market is segmented into Cervical Thoracic Lumbar Sacral Orthosis (CTLSO), Thoracolumbosacral Orthosis (TLSO), and Lumbosacral Orthosis (LSO). The TLSO segment dominated the largest market revenue share of 46.8% in 2025, driven by its widespread use in treating thoracic and lumbar spinal curvature, which represents the most common form of scoliosis. TLSO braces are highly effective in controlling curve progression in adolescents, particularly during growth phases. Their non-invasive nature and strong clinical acceptance support adoption. Increasing awareness of early scoliosis screening further drives demand. Advancements in lightweight and custom-fitted braces enhance patient compliance. Hospitals and orthopedic clinics widely recommend TLSO devices. Rising prevalence of adolescent idiopathic scoliosis strengthens market growth. Improved materials and 3D printing technologies enhance comfort and effectiveness. Insurance coverage in developed markets further supports usage. These factors collectively reinforce TLSO dominance.

The CTLSO segment is expected to witness the fastest CAGR of 8.9% from 2026 to 2033, driven by its use in severe spinal deformities requiring full spinal immobilization. CTLSO braces provide comprehensive support from cervical to sacral regions. Increasing cases of complex scoliosis conditions support demand. The segment benefits from advancements in adjustable and patient-friendly designs. Growing pediatric and neuromuscular scoliosis cases further boost adoption. Improved rehabilitation outcomes enhance clinical preference. Rising surgical alternatives avoidance supports non-invasive treatments. Technological innovation in orthotic manufacturing improves usability. Expanding orthopedic care infrastructure strengthens accessibility. These factors position CTLSO as the fastest-growing product segment.

• By Types

On the basis of types, the Scoliosis Treatment market is segmented into structural, non-structural, and others. The structural segment held the largest market revenue share of 57.4% in 2025, driven by the high prevalence of structural scoliosis cases caused by spinal deformities and vertebral abnormalities. Structural scoliosis requires long-term treatment strategies such as bracing, surgery, and physiotherapy. Increasing diagnosis rates through advanced imaging technologies support early detection. The segment benefits from strong clinical focus on curve progression management. Rising adolescent idiopathic scoliosis cases further drive demand. Hospitals prioritize structured treatment protocols for better outcomes. Growing awareness of spinal health enhances patient screening. Expanding orthopedic care facilities support treatment access. Continuous innovation in surgical techniques improves recovery rates. These factors ensure dominance of the structural segment.

The non-structural segment is expected to witness the fastest CAGR of 7.6% from 2026 to 2033, driven by increasing cases of functional scoliosis caused by posture, inflammation, or muscle imbalance. Non-structural scoliosis is often reversible with early intervention. Rising sedentary lifestyles and poor posture habits contribute to growth. Increasing physiotherapy and rehabilitation adoption supports demand. Awareness programs on spinal health improve early diagnosis. The segment benefits from non-invasive treatment preference. Growth in sports-related spinal injuries also contributes. Expanding outpatient care services enhance accessibility. Cost-effective treatment options support wider adoption. These factors position non-structural scoliosis as the fastest-growing type segment.

• By Treatment

On the basis of treatment, the scoliosis treatment market is segmented into braces, surgery, physical exercises, drugs, and others. The braces segment dominated the largest market revenue share of 41.9% in 2025, driven by its effectiveness in preventing curve progression in mild to moderate scoliosis cases. Bracing is widely recommended for adolescents during growth spurts. Non-invasive nature and high safety profile support adoption. Increasing availability of custom-fit and 3D-printed braces enhances compliance. Orthopedic specialists strongly prefer bracing as first-line therapy. Rising awareness of early scoliosis screening boosts usage. Expanding pediatric orthopedic care supports demand. Insurance coverage for bracing devices increases accessibility. Technological advancements improve comfort and durability. These factors ensure dominance of the braces segment.

The surgery segment is expected to witness the fastest CAGR of 9.3% from 2026 to 2033, driven by increasing cases of severe spinal curvature requiring corrective procedures. Surgical interventions such as spinal fusion provide long-term correction. Advancements in minimally invasive spine surgery improve outcomes. Rising healthcare infrastructure supports surgical access. Increasing prevalence of complex scoliosis cases fuels demand. Improved postoperative recovery techniques enhance adoption. Growing success rates of surgical correction boost confidence. Expanding specialist surgeon availability supports procedures. Rising patient preference for definitive correction drives growth. These factors position surgery as the fastest-growing treatment segment.

• By Route of Administration

On the basis of route of administration, the scoliosis treatment market is segmented into oral, parenteral, and others. The oral segment held the largest market revenue share of 63.2% in 2025, driven by widespread use of oral medications for pain management and supportive therapy in scoliosis patients. Oral drugs are preferred for ease of administration and high patient compliance. They are commonly used alongside bracing and physiotherapy. Increasing outpatient treatment trends support demand. Availability of anti-inflammatory and muscle relaxant drugs enhances usage. Cost-effectiveness further strengthens adoption. Expanding pharmaceutical access in developing regions boosts growth. Rising awareness of long-term symptom management supports usage. Physicians prefer oral route for mild cases. These factors ensure dominance of the oral segment.

The parenteral segment is expected to witness the fastest CAGR of 8.1% from 2026 to 2033, driven by its use in severe postoperative pain management and advanced therapeutic care. Parenteral administration ensures faster drug action and higher bioavailability. Increasing scoliosis surgeries support demand. Hospitals adopt injectable therapies for critical care cases. Advancements in injectable formulations improve safety and effectiveness. Growing inpatient care infrastructure enhances availability. Rising cases of severe spinal deformities further support growth. Improved clinical protocols boost adoption rates. Expanding orthopedic surgical centers contribute to demand. These factors position parenteral route as the fastest-growing segment.

• By End-Users

On the basis of end-users, the scoliosis treatment market is segmented into hospitals, specialty clinics, and others. The hospitals segment accounted for the largest market revenue share of 49.6% in 2025, driven by high patient inflow for diagnosis, bracing, and surgical treatments. Hospitals offer advanced imaging and orthopedic care facilities. Availability of multidisciplinary teams supports comprehensive treatment. Rising scoliosis surgeries increase hospital utilization. Strong reimbursement systems enhance affordability. Increasing pediatric scoliosis screening programs support early detection. Hospitals are primary centers for complex case management. Expanding healthcare infrastructure boosts accessibility. Integration of rehabilitation services improves outcomes. These factors ensure dominance of the hospitals segment.

The specialty clinics segment is expected to witness the fastest CAGR of 9.0% from 2026 to 2033, driven by growing preference for specialized orthopedic and spine care. Specialty clinics offer personalized treatment and faster diagnosis. Increasing awareness of spinal health supports clinic visits. Rising demand for non-surgical treatments boosts growth. Clinics provide focused bracing and physiotherapy services. Advancements in outpatient care improve efficiency. Expanding urban healthcare facilities enhance accessibility. Patients prefer clinics for regular follow-ups. Growing use of digital health tools supports engagement. These factors position specialty clinics as the fastest-growing end-user segment.

Scoliosis Treatment Market Regional Analysis

- North America dominated the scoliosis treatment market with the largest revenue share of approximately 38.9% in 2025, characterized by advanced healthcare infrastructure, high adoption of corrective surgeries and bracing systems, and a strong presence of specialized orthopedic center

- The region benefits from well-established clinical pathways, early screening programs, and improved access to specialized spine care, which collectively support timely diagnosis and effective treatment outcomes

- In particular, the U.S. contributes significantly to regional growth due to strong healthcare expenditure, high awareness of spinal deformities, and widespread availability of pediatric orthopedic services

U.S. Scoliosis Treatment Market Insight

The U.S. scoliosis treatment market accounts for a substantial share within North America, driven by early screening initiatives, advanced surgical techniques, and increasing adoption of non-surgical treatment options such as bracing and physiotherapy. Growing awareness of adolescent idiopathic scoliosis, along with improved access to specialized spine care centers, continues to support early intervention and better long-term patient outcomes. In addition, the presence of highly skilled orthopedic specialists and strong healthcare infrastructure further strengthens treatment accessibility across the country.

Europe Scoliosis Treatment Market Insight

The Europe scoliosis treatment market is projected to expand at a steady CAGR during the forecast period, supported by well-established healthcare systems, increasing awareness of spinal disorders, and rising adoption of conservative treatment approaches. The region is witnessing growing use of advanced bracing technologies and minimally invasive surgical procedures, which are improving patient recovery and outcomes. In addition, structured pediatric screening programs in several European countries are enabling early diagnosis and timely treatment.

U.K. Scoliosis Treatment Market Insight

The U.K. scoliosis treatment market is expected to grow steadily due to rising awareness of spinal health, strong public healthcare infrastructure, and improved access to orthopedic specialists. Increasing cases of adolescent scoliosis and enhanced diagnostic capabilities are supporting early intervention. Furthermore, the availability of rehabilitation programs and growing preference for non-surgical management approaches are contributing to market growth.

Germany Scoliosis Treatment Market Insight

The Germany scoliosis treatment market is expanding due to strong healthcare infrastructure, high emphasis on medical innovation, and widespread adoption of evidence-based orthopedic treatment methods. Increasing focus on early diagnosis and screening programs is improving clinical outcomes. In addition, Germany’s well-developed physiotherapy and rehabilitation ecosystem plays a key role in post-treatment recovery and long-term patient management.

Asia-Pacific Scoliosis Treatment Market Insight

Asia-Pacific scoliosis treatment market is expected to be the fastest-growing region in the Scoliosis Treatment market during the forecast period, with a projected CAGR of approximately 9.6%, driven by rising healthcare expenditure, increasing awareness of spinal disorders, expanding pediatric population, and improving access to orthopedic care. Growing healthcare infrastructure, coupled with government initiatives promoting early diagnosis and treatment, is further supporting regional growth.

Japan Scoliosis Treatment Market Insight

The Japan scoliosis treatment market is witnessing steady growth due to advanced medical technology adoption, strong healthcare infrastructure, and a high focus on precision-based treatment. Early diagnosis practices, widespread use of minimally invasive procedures, and strong rehabilitation support systems are enhancing patient outcomes. In addition, Japan’s aging population is increasing demand for effective and less invasive spinal care solutions.

China Scoliosis Treatment Market Insight

China scoliosis treatment market accounted for a major share of the Asia-Pacific Scoliosis Treatment market in 2025, driven by rapid urbanization, large patient population, and continuous improvements in healthcare infrastructure. Increasing awareness of spinal deformities, expanding hospital networks, and rising availability of orthopedic specialists are supporting early diagnosis and treatment adoption. Government initiatives focused on healthcare modernization and improved screening programs are further strengthening market growth.

Scoliosis Treatment Market Share

The Scoliosis Treatment industry is primarily led by well-established companies, including:

- Medtronic plc (Ireland)

- Johnson & Johnson (U.S.)

- Stryker Corporation (U.S.)

- Zimmer Biomet Holdings, Inc. (U.S.)

- NuVasive, Inc. (U.S.)

- Globus Medical, Inc. (U.S.)

- Boston Scientific Corporation (U.S.)

- Abbott Laboratories (U.S.)

- Orthofix Medical Inc. (U.S.)

- Smith+Nephew plc (U.K.)

- B. Braun Melsungen AG (Germany)

- Siemens Healthineers AG (Germany)

- GE HealthCare (U.S.)

- Arthrex, Inc. (U.S.)

- Medacta Group SA (Switzerland)

- K2M Group Holdings (U.S.)

- Aesculap, Inc. (Germany)

- RTI Surgical Holdings (U.S.)

- Alphatec Holdings, Inc. (U.S.)

- SeaSpine Orthopedics Corporation (U.S.)

Latest Developments in Global Scoliosis Treatment Market

- In June 2021, Spinologics Inc. announced that the U.S. Food and Drug Administration (FDA) granted Breakthrough Device Designation to its MIScoli™ vertebral body tethering system, an innovative non-fusion scoliosis treatment aimed at improving outcomes for adolescent patients. This designation supports accelerated development and priority review for devices that address unmet medical needs in scoliosis care

- In August 2021, Auctus Surgical revealed that the FDA had granted Breakthrough Device Designation to its dynamic vertebral body tethering system, recognizing its potential to provide a non-fusion surgical option for pediatric scoliosis patients. The designation enables more interactive communication with regulators and expedited review pathways for this emerging treatment technology

- In March 2023, research and clinical adoption of advanced scoliosis treatments such as vertebral body tethering (VBT) and 3D-printed custom bracing expanded globally, with medical centers reporting improved flexibility and patient outcomes compared with traditional spinal fusion. These trends reflect the broader shift toward motion-preserving and personalized treatment approaches in scoliosis care

- In July 2025, robotic-assisted spine surgery and 3D-printed bracing technologies were increasingly reported as mainstream innovations in scoliosis treatment, enabling more precise surgical correction and customized orthotic support for patients. These technologies aim to improve accuracy, reduce complications, and enhance patient comfort in both surgical and non-surgical scoliosis management

- In September 2025, a retrospective FDA Investigational Device Exemption (IDE) study published clinical follow-up data on anterior vertebral body tethering for adolescent idiopathic scoliosis, providing up to 10-year outcome insights that support long-term effectiveness of non-fusion treatment strategies. These results contribute to evidence-based decision-making for scoliosis treatment planning

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.