Global Sound Sensors Market

Market Size in USD Billion

CAGR :

%

USD

1.84 Billion

USD

2.80 Billion

2025

2033

USD

1.84 Billion

USD

2.80 Billion

2025

2033

| 2026 - 2033 | |

| USD 1.84 Billion | |

| USD 2.80 Billion | |

| % | |

|

Sound Sensors Market Overview

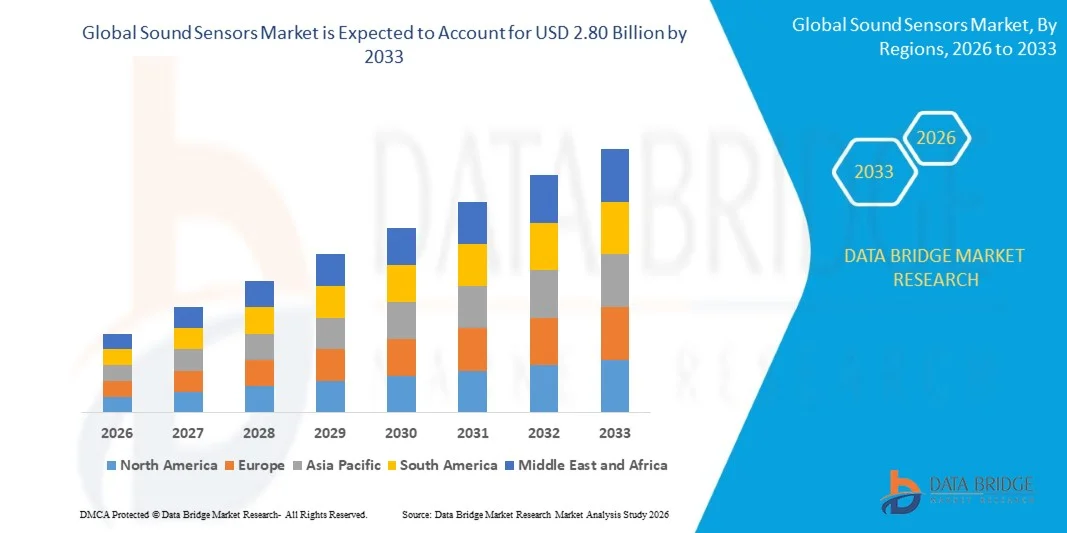

The Sound Sensors Market was valued at USD 1.84 billion in 2025 and is projected to reach USD 2.80 billion by 2033, growing at a CAGR of 5.40% from 2026 to 2033. The market is experiencing steady growth driven by increasing adoption of smart consumer electronics, rising integration of voice recognition and audio-based sensing technologies, and expanding use of sound sensors in industrial monitoring, automotive safety systems, and healthcare applications.

The growing penetration of IoT-enabled devices and smart home systems is significantly boosting demand for sound sensors, as they enable voice activation, noise detection, and real-time audio-based control functions. In addition, advancements in MEMS (Micro-Electro-Mechanical Systems) technology are enhancing sensor sensitivity, accuracy, and miniaturization, further supporting their adoption across smartphones, wearable devices, surveillance systems, and industrial automation platforms.

Key Market Trends & Insights

- North America dominated the sound sensors market with the largest revenue share of approximately 38.9% in 2025, supported by strong penetration of smart devices, advanced industrial infrastructure, high adoption of AI-based voice assistants, and widespread use of acoustic sensing in automotive and industrial applications.

- Asia-Pacific is expected to be the fastest-growing region, recording a CAGR of around 7–8% from 2026 to 2033. Growth is driven by rapid urbanization, expanding consumer electronics manufacturing base, increasing adoption of smart home ecosystems, rising automotive production, and strong government investments in IoT and smart city infrastructure across China, Japan, and India.

- The Pressure segment held the largest market revenue share of approximately 27.9% in 2025 driven by strong demand for vibration and pressure-based acoustic monitoring in industrial machinery and automotive systems. Pressure-based acoustic sensing is widely used in predictive maintenance and structural health monitoring applications. The segment is further supported by increasing adoption of Industry 4.0 technologies and real-time condition monitoring systems across manufacturing facilities. Industrial automation plants are integrating acoustic pressure sensors into motors, turbines, and compressors for improved efficiency. Growing focus on reducing equipment downtime is strengthening adoption across developed economies.

- The Chemical Vapour segment is projected to register the fastest growth at a CAGR of 9.8% from 2026 to 2033, driven by increasing adoption in environmental monitoring, industrial safety systems, and hazardous gas detection applications where acoustic signal variation helps identify chemical leaks. Rising environmental compliance requirements and stricter emission regulations are boosting deployment of chemical vapour sensing systems. Oil and gas refineries and chemical plants are increasingly using acoustic detection for early hazard identification. Smart city pollution monitoring networks are further supporting demand growth.

- The SAW Sensor segment held the largest market revenue share of approximately 58.6% in 2025 driven by its high sensitivity, low power consumption, and widespread use in consumer electronics and wireless communication devices. SAW sensors are widely used in smartphones, IoT devices, and wearable electronics due to compact size and cost efficiency. Their stable frequency performance makes them suitable for mass deployment. Growing adoption of smart consumer devices is further strengthening segment dominance.

- The BAW Sensor segment is projected to register the fastest growth at a CAGR of 8.7% from 2026 to 2033, driven by increasing adoption in high-frequency industrial sensing, automotive radar systems, and advanced communication applications requiring higher performance and stability. BAW sensors offer superior thermal stability and high-frequency performance, making them suitable for 5G infrastructure and automotive electronics. Increasing deployment in aerospace and defense applications is also accelerating demand. Expansion of next-generation communication networks is further supporting growth.

- The Consumer Electronics segment held the largest market revenue share of approximately 41.3% in 2025 driven by strong demand for smartphones, smart speakers, and wearable devices integrated with voice recognition and audio sensing technologies. Rising adoption of smart assistants and voice-enabled devices is driving segment growth. Integration of sound sensors in home automation and entertainment systems is further increasing demand. Continuous innovation in consumer electronics is strengthening market expansion.

- The Automotive segment is projected to register the fastest growth at a CAGR of 9.2% from 2026 to 2033, driven by increasing adoption of ADAS systems, in-cabin monitoring, and acoustic-based safety applications in electric and autonomous vehicles. Sound sensors are increasingly used for driver monitoring, collision warning, and voice control systems. Expansion of electric vehicles is boosting integration of acoustic technologies. Rising focus on vehicle safety regulations is further accelerating adoption.

- The Low Frequency Detection segment held the largest market revenue share of approximately 62.4% in 2025 driven by its widespread use in consumer devices, industrial monitoring, and voice recognition systems. Low frequency sensors are widely used for human voice detection and smart assistant applications. Their integration into smartphones and smart home devices is increasing rapidly. Industrial applications also rely on low-frequency detection for basic condition monitoring.

- The High Frequency Detection segment is projected to register the fastest growth at a CAGR of 8.9% from 2026 to 2033, driven by increasing use in ultrasonic sensing, medical diagnostics, and advanced industrial inspection systems requiring high precision acoustic analysis. High-frequency sensors are used in ultrasound imaging and non-destructive testing applications. Growing robotics and automation deployment is boosting demand. Healthcare diagnostics advancements are further supporting segment expansion.

- The Acoustic Sensors segment held the largest market revenue share of approximately 66.8% in 2025 driven by widespread adoption in smartphones, smart homes, and industrial monitoring systems. Acoustic sensors are extensively used for voice recognition and environmental sound detection. Their integration in consumer electronics and security systems is driving adoption. Increasing demand for smart home ecosystems is strengthening segment dominance.

- The Ultrasonic Sensors segment is projected to register the fastest growth at a CAGR of 9.5% from 2026 to 2033, driven by increasing use in automotive parking systems, robotics, and medical imaging applications requiring high-precision distance and object detection. Ultrasonic sensors are widely used in autonomous vehicles and robotics for navigation and obstacle detection. Healthcare imaging applications are also supporting growth. Rising investment in smart mobility solutions is further accelerating demand.

Market Size & Forecast

- Global Market Value (2025): USD 1.84 Billion

- Expected Market Value (2033): USD 2.80 Billion

- Forecast CAGR (2026–2033): 5.40%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Sound Sensors Market Segmentation

|

Attributes |

Sound Sensors Key Market Insights |

|

Segments Covered |

· By Sensing Parameter: Temperature, Torque, Pressure, Mass, Humidity, Viscosity, and Chemical Vapour · By Type: Surface Acoustic Wave (SAW) Sensor, and Bulk Acoustic Wave (BAW) Sensor · By End-User: Automotive, Healthcare, Aerospace and Defense, Industrial, and Consumer Electronics · By Specification: Low Frequency Detection (<20,000 Hz), and High Frequency Detection (>20,000 Hz) · By Application: Ultrasonic Sensors and Acoustic Sensors |

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

• Honeywell International Inc. (U.S.) |

|

Market Opportunities |

· Expansion Of Smart Home And IoT Devices · Growth In Automotive Voice Recognition Systems |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Sound Sensors Market Trends

Trend: Rising Adoption Of Acoustic-Based Sensing In Smart And Industrial Applications

The Sound Sensors Market is witnessing strong growth driven by increasing integration of acoustic sensing technologies in smart devices, industrial automation systems, and safety monitoring applications. Rising demand for real-time sound detection, voice recognition, and vibration analysis across automotive, healthcare, and consumer electronics sectors is significantly boosting adoption. In addition, advancements in MEMS-based microphones and ultrasonic sensing technologies are improving accuracy, sensitivity, and miniaturization of sound sensors.

In modern automotive systems, manufacturers are increasingly integrating sound sensors, For instance in advanced driver assistance systems (ADAS) and in-cabin voice control modules, to enhance safety and improve user interaction. In industrial environments, acoustic sensors are being deployed for predictive maintenance by detecting abnormal machine vibrations and sound signatures, helping reduce equipment failure and downtime.

The rapid expansion of smart homes and IoT ecosystems is also increasing demand for voice-enabled devices such as smart speakers, security systems, and wearable electronics. In addition, healthcare applications such as respiratory monitoring and diagnostic imaging are increasingly adopting acoustic sensing technologies. Industry deployments in 2025 across North America smart manufacturing facilities reported up to 12–18% reduction in unplanned equipment downtime after integrating acoustic-based predictive monitoring systems.

Sound Sensors Market Dynamics

Key Market Driver: Rising Adoption Of IoT And Voice-Enabled Smart Devices

The increasing penetration of IoT-enabled devices and voice-controlled systems is a major driver of the sound sensors market, as consumers and industries shift toward hands-free and intelligent interaction technologies. Growing demand for smart assistants, automated security systems, and connected appliances is driving large-scale deployment of acoustic sensing solutions.

Consumer electronics companies are increasingly integrating high-precision microphones and sound sensors into smartphones, smart speakers, and wearables, For instance in voice assistant platforms such as Alexa, Google Assistant, and Siri-based ecosystems, to enable seamless user interaction and real-time voice processing. Industrial sectors are also leveraging sound sensors for equipment monitoring and quality control applications.

Global shipments of smart speakers exceeded 150 million units in 2024, highlighting strong adoption of voice-enabled technologies, particularly in North America and Asia-Pacific, where smart home penetration continues to rise rapidly.

Key Restraint/Challenge: Environmental Noise Interference And Signal Accuracy Limitations

The performance of sound sensors is often affected by environmental noise interference, signal distortion, and sensitivity limitations in complex acoustic environments. These challenges reduce accuracy in applications requiring precise sound detection, particularly in industrial and outdoor settings where background noise levels are high.

In addition, high-precision sound sensors require advanced signal processing algorithms and calibration systems, increasing overall system complexity and cost. Limited performance consistency across varying temperature and humidity conditions further restricts adoption in mission-critical applications.

Technical studies indicate that ambient industrial noise levels can exceed 85 dB in manufacturing environments, significantly impacting the accuracy of standard acoustic sensors without advanced noise filtering systems.

Key Market Opportunity: Expansion In Automotive Safety And Healthcare Monitoring Applications

The growing use of sound sensors in automotive safety systems and healthcare monitoring solutions is creating significant market opportunities. Increasing focus on driver safety, in-cabin monitoring, and predictive vehicle diagnostics is driving demand for advanced acoustic sensing technologies in modern vehicles.

Automotive companies are increasingly deploying sound sensors, For instance in fatigue detection systems and emergency alert monitoring, to enhance passenger safety and improve real-time decision-making capabilities. In healthcare, sound sensors are being used for respiratory monitoring, heartbeat analysis, and non-invasive diagnostic applications, particularly in remote patient monitoring systems.

In addition, advancements in AI-based acoustic analytics and machine learning algorithms are improving sound classification accuracy, opening opportunities across aerospace, defense, and industrial automation sectors. In 2025, pilot healthcare programs in Japan and Germany reported improved early detection accuracy of respiratory anomalies by nearly 15–20% using AI-enabled acoustic monitoring systems.

Sound Sensors Market Scope

The market is segmented on the basis of sensing parameter, type, end-user, specification, and application.

- By Sensing Parameter

On the basis of sensing parameter, the sound sensors market is segmented into Temperature, Torque, Pressure, Mass, Humidity, Viscosity, and Chemical Vapour. The Pressure segment held the largest market revenue share of approximately 27.9% in 2025 driven by strong demand for vibration and pressure-based acoustic monitoring in industrial machinery and automotive systems. Pressure-based acoustic sensing is widely used in predictive maintenance and structural health monitoring applications. The segment is further supported by increasing adoption of Industry 4.0 technologies and real-time condition monitoring systems across manufacturing facilities. Industrial automation plants are integrating acoustic pressure sensors into motors, turbines, and compressors for improved efficiency. Growing focus on reducing equipment downtime is strengthening adoption across developed economies.

The Chemical Vapour segment is projected to register the fastest growth at a CAGR of 9.8% from 2026 to 2033, driven by increasing adoption in environmental monitoring, industrial safety systems, and hazardous gas detection applications where acoustic signal variation helps identify chemical leaks. Rising environmental compliance requirements and stricter emission regulations are boosting deployment of chemical vapour sensing systems. Oil and gas refineries and chemical plants are increasingly using acoustic detection for early hazard identification. Smart city pollution monitoring networks are further supporting demand growth.

- By Type

On the basis of type, the market is segmented into Surface Acoustic Wave (SAW) Sensor and Bulk Acoustic Wave (BAW) Sensor. The SAW Sensor segment held the largest market revenue share of approximately 58.6% in 2025 driven by its high sensitivity, low power consumption, and widespread use in consumer electronics and wireless communication devices. SAW sensors are widely used in smartphones, IoT devices, and wearable electronics due to compact size and cost efficiency. Their stable frequency performance makes them suitable for mass deployment. Growing adoption of smart consumer devices is further strengthening segment dominance.

The BAW Sensor segment is projected to register the fastest growth at a CAGR of 8.7% from 2026 to 2033, driven by increasing adoption in high-frequency industrial sensing, automotive radar systems, and advanced communication applications requiring higher performance and stability. BAW sensors offer superior thermal stability and high-frequency performance, making them suitable for 5G infrastructure and automotive electronics. Increasing deployment in aerospace and defense applications is also accelerating demand. Expansion of next-generation communication networks is further supporting growth.

- By End-User

On the basis of end-user, the market is segmented into Automotive, Healthcare, Aerospace and Defense, Industrial, and Consumer Electronics. The Consumer Electronics segment held the largest market revenue share of approximately 41.3% in 2025 driven by strong demand for smartphones, smart speakers, and wearable devices integrated with voice recognition and audio sensing technologies. Rising adoption of smart assistants and voice-enabled devices is driving segment growth. Integration of sound sensors in home automation and entertainment systems is further increasing demand. Continuous innovation in consumer electronics is strengthening market expansion.

The Automotive segment is projected to register the fastest growth at a CAGR of 9.2% from 2026 to 2033, driven by increasing adoption of ADAS systems, in-cabin monitoring, and acoustic-based safety applications in electric and autonomous vehicles. Sound sensors are increasingly used for driver monitoring, collision warning, and voice control systems. Expansion of electric vehicles is boosting integration of acoustic technologies. Rising focus on vehicle safety regulations is further accelerating adoption.

- By Specification

On the basis of specification, the market is segmented into Low Frequency Detection (<20,000 Hz) and High Frequency Detection (>20,000 Hz). The Low Frequency Detection segment held the largest market revenue share of approximately 62.4% in 2025 driven by its widespread use in consumer devices, industrial monitoring, and voice recognition systems. Low frequency sensors are widely used for human voice detection and smart assistant applications. Their integration into smartphones and smart home devices is increasing rapidly. Industrial applications also rely on low-frequency detection for basic condition monitoring.

The High Frequency Detection segment is projected to register the fastest growth at a CAGR of 8.9% from 2026 to 2033, driven by increasing use in ultrasonic sensing, medical diagnostics, and advanced industrial inspection systems requiring high precision acoustic analysis. High-frequency sensors are used in ultrasound imaging and non-destructive testing applications. Growing robotics and automation deployment is boosting demand. Healthcare diagnostics advancements are further supporting segment expansion.

- By Application

On the basis of application, the market is segmented into Ultrasonic Sensors and Acoustic Sensors. The Acoustic Sensors segment held the largest market revenue share of approximately 66.8% in 2025 driven by widespread adoption in smartphones, smart homes, and industrial monitoring systems. Acoustic sensors are extensively used for voice recognition and environmental sound detection. Their integration in consumer electronics and security systems is driving adoption. Increasing demand for smart home ecosystems is strengthening segment dominance.

The Ultrasonic Sensors segment is projected to register the fastest growth at a CAGR of 9.5% from 2026 to 2033, driven by increasing use in automotive parking systems, robotics, and medical imaging applications requiring high-precision distance and object detection. Ultrasonic sensors are widely used in autonomous vehicles and robotics for navigation and obstacle detection. Healthcare imaging applications are also supporting growth. Rising investment in smart mobility solutions is further accelerating demand.

Sound Sensors Market Regional Analysis

North America Sound Sensors Market Insight

North America dominated the sound sensors market with the largest revenue share of 38.9% in 2025, supported by strong adoption of smart consumer electronics, advanced industrial automation systems, and high penetration of IoT-enabled devices. The region benefits from strong technological infrastructure and high demand for voice-enabled systems, predictive maintenance solutions, and smart home applications. Increasing integration of AI-based acoustic analytics in automotive and industrial sectors is further strengthening market expansion across the region.

U.S. Sound Sensors Market Insight

The U.S. sound sensors market captured the largest revenue share in 2025 within North America, driven by rapid adoption of smart speakers, smartphones, and wearable devices integrated with advanced voice recognition technologies. Growing demand for in-cabin automotive voice control systems and ADAS applications is further accelerating adoption. Strong presence of leading technology companies and continuous innovation in MEMS microphone technologies are significantly contributing to market growth.

Europe Sound Sensors Market Insight

The Europe sound sensors market is expected to witness the fastest growth rate from 2026 to 2033, primarily driven by rising demand for industrial automation, smart manufacturing, and energy-efficient monitoring systems. Strict regulatory frameworks focused on workplace safety and environmental monitoring are encouraging adoption of acoustic sensing technologies. Increasing deployment in automotive safety systems and smart building applications is further boosting regional growth across residential and industrial sectors.

U.K. Sound Sensors Market Insight

The U.K. sound sensors market is expected to witness strong growth from 2026 to 2033, driven by increasing adoption of smart home devices, security systems, and voice-controlled consumer electronics. Rising concerns regarding public safety and building security are supporting deployment of acoustic monitoring systems. In addition, growth in e-commerce, smart infrastructure projects, and IoT integration across residential applications is accelerating market expansion.

Germany Sound Sensors Market Insight

The Germany sound sensors market is expected to witness robust growth from 2026 to 2033, fueled by strong industrial automation, advanced automotive manufacturing, and increasing focus on predictive maintenance technologies. Germany’s emphasis on Industry 4.0 is driving adoption of acoustic sensing systems in machinery monitoring and smart factories. Growing integration in electric vehicles and energy-efficient industrial systems is further supporting market development.

Asia-Pacific Sound Sensors Market Insight

The Asia-Pacific sound sensors market is expected to witness the fastest growth rate from 2026 to 2033, supported by rapid urbanization, expanding consumer electronics manufacturing, and increasing adoption of smart home technologies in countries such as China, Japan, and India. Strong growth in automotive production and industrial automation is further boosting demand. The region’s position as a global electronics manufacturing hub is also enhancing affordability and large-scale adoption of sound sensor technologies.

Japan Sound Sensors Market Insight

The Japan sound sensors market is expected to witness steady growth from 2026 to 2033 due to high technological adoption, aging population needs, and strong demand for smart healthcare and assisted living systems. Increasing integration of acoustic sensors in robotics, automotive systems, and healthcare monitoring devices is driving growth. Japan’s focus on precision electronics and advanced industrial automation is further strengthening market expansion.

China Sound Sensors Market Insight

The China sound sensors market accounted for the largest market revenue share in Asia Pacific in 2025, attributed to rapid expansion of consumer electronics manufacturing, strong adoption of smart home devices, and growing automotive production. Increasing government support for smart city development and IoT infrastructure is further boosting demand. Rising integration of sound sensors in industrial monitoring and voice-enabled devices is strengthening China’s dominance in the regional market.

Sound Sensors Market Share

The Sound Sensors industry is primarily led by well-established companies, including:

• Honeywell International Inc. (U.S.)

• Seiko Epson Corporation (Japan)

• CTS Corporation (U.S.)

• GENERAL ELECTRIC (U.S.)

• MaxBotix Inc. (U.S.)

• Rockwell Automation, Inc. (U.S.)

• Siemens (Germany)

• STMicroelectronics (Switzerland)

• Teledyne Technologies Incorporated (U.S.)

• API Technologies (U.K.)

• Emerson Electric Co. (U.S.)

• BOSTON PIEZO-OPTICS INC. (U.S.)

• Panasonic Corporation (Japan)

• Robert Bosch GmbH (Germany)

• NXP Semiconductors (Netherlands)

• Infineon Technologies AG (Germany)

• DENSO CORPORATION (Japan)

• Brüel & Kjær (Denmark)

• CeramTec GmbH (Germany)

• Microchip Technologies (U.S.)

Latest Developments in Sound Sensors Market

- In May 2026, SensiBel, in collaboration with Silex Microsystems, advanced the commercialization of the SBM100B optical MEMS microphone through a production-scale manufacturing partnership, enabling laser-interferometry-based acoustic sensing to move closer to high-volume industrial deployment and reducing manufacturing scalability barriers that previously restricted market adoption.

- In March 2026, Trident IoT and Syntiant introduced a low-power audio AI sensor platform integrating neural decision processing with IoT connectivity, designed for always-on safety, security, and industrial monitoring applications, expanding edge-AI sensing capabilities and strengthening demand for intelligent acoustic edge devices across smart infrastructure markets.

- In March 2026, Ocean Sonics secured USD 4.1 million funding from Canada’s Ocean Supercluster to advance hydrophone technologies for passive acoustic monitoring of marine ecosystems, supporting environmental sensing innovation and driving growth in underwater acoustic data solutions for research and conservation applications.

- In January 2026, Syntiant launched an AI-powered smart frame reference design at CES 2026 featuring a MEMS microphone array combined with its neural decision processor, enabling always-on audio event detection in smart home environments and accelerating adoption of edge AI-driven consumer audio sensing systems.

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Sound Sensors Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Sound Sensors Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Sound Sensors Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.