Global Squamous Cell Carcinoma Treatment Market

Market Size in USD Billion

CAGR :

%

USD

1.29 Billion

USD

2.66 Billion

2025

2033

USD

1.29 Billion

USD

2.66 Billion

2025

2033

| 2026 –2033 | |

| USD 1.29 Billion | |

| USD 2.66 Billion | |

| % | |

|

Squamous Cell Carcinoma Treatment Market Size

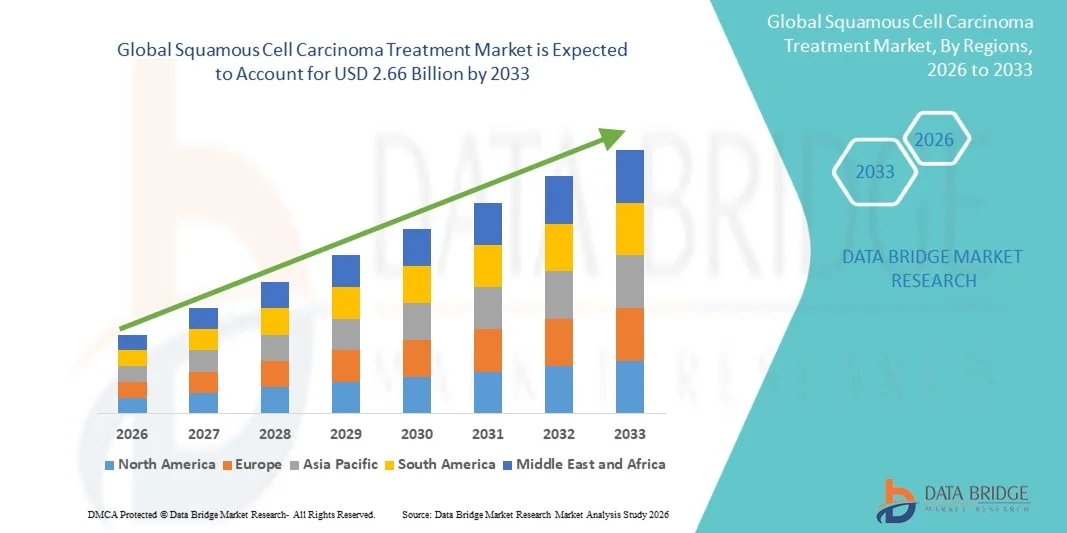

- The global squamous cell carcinoma treatment market size was valued at USD 1.29 billion in 2025 and is expected to reach USD 2.66 billion by 2033, at a CAGR of 9.50% during the forecast period

- The market growth is largely fueled by the increasing prevalence of squamous cell carcinoma (SCC) worldwide, rising awareness about skin and other epithelial cancers, and advancements in early detection, targeted therapies, and immunotherapy approaches, leading to improved patient outcomes and adoption of advanced treatment solutions

- Furthermore, growing demand for effective, minimally invasive, and personalized treatment options, coupled with expanding healthcare infrastructure and access to oncology care in emerging economies, is positioning SCC treatments as essential solutions in cancer management. These factors are accelerating the uptake of squamous cell carcinoma treatment therapies, thereby significantly boosting market growth

Squamous Cell Carcinoma Treatment Market Analysis

- Squamous cell carcinoma treatments, including surgery, radiation therapy, targeted therapy, and immunotherapy, are witnessing significant adoption due to rising global cancer incidence, early detection initiatives, and improvements in treatment efficacy

- The increasing demand for SCC treatments is driven by the rising prevalence of skin and epithelial cancers, growing awareness about early diagnosis, and the expansion of oncology healthcare infrastructure in both developed and emerging regions

- North America dominated the squamous cell carcinoma treatment market with the largest revenue share of 37.8% in 2025, supported by advanced healthcare facilities, strong research and development activity, high adoption of targeted therapies, and well-established patient access to oncology care

- Asia-Pacific is expected to be the fastest-growing region in the SCC Treatment market during the forecast period, fueled by increasing healthcare spending, growing cancer awareness programs, and expansion of advanced treatment centers

- The Parenteral segment held the largest market revenue share of 51.2% in 2025, driven by the widespread use of injections and infusions for targeted therapies and immunotherapies

Report Scope and Squamous Cell Carcinoma Treatment Market Segmentation

|

Attributes |

Squamous Cell Carcinoma Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Squamous Cell Carcinoma Treatment Market Trends

“Enhanced Convenience and Efficacy in Treatment Approaches”

- A significant trend in the global squamous cell carcinoma treatment market is the increasing adoption of personalized and targeted therapies. Advances in immunotherapy, targeted chemotherapeutics, and novel combination regimens are improving patient outcomes and reducing side effects compared to conventional treatments

- For instance, in 2025, Keytruda (pembrolizumab) gained wider approval for advanced squamous cell carcinoma, enabling clinicians to offer immune checkpoint inhibition therapy tailored to specific patient profiles. Similarly, newer topical and localized treatments are increasingly utilized for early-stage lesions, minimizing systemic exposure

- The market is also witnessing growing investment in clinical research and the development of combination therapy protocols, which allow for improved survival rates and reduced recurrence. For instance, studies combining radiotherapy with targeted immunotherapy have shown promising results in patients with high-risk tumors

- Improved treatment monitoring, including real-time imaging and biomarker tracking, enables clinicians to adjust therapies more effectively, enhancing precision in care

- Pharmaceutical companies such as Merck, Bristol-Myers Squibb, and Roche are actively developing next-generation therapies with better efficacy profiles, contributing to rapid market expansion

- The demand for Squamous Cell Carcinoma Treatment solutions is increasing steadily worldwide, as healthcare systems prioritize effective, personalized, and patient-friendly treatment approaches

Squamous Cell Carcinoma Treatment Market Dynamics

Driver

“Growing Need Due to Rising Patient Volume and Technological Advancements”

- The increasing prevalence of squamous cell carcinoma globally, combined with the growing adoption of AI-enabled healthcare solutions, is driving demand for intelligent treatment platforms

- For instance, in 2025, OncoTech Inc. launched an AI-powered treatment platform that integrates patient data with predictive analytics to recommend personalized therapy schedules, significantly improving patient adherence

- AI-assisted systems enhance treatment safety by monitoring dosage schedules, recording patient responses, and sending alerts for any abnormalities. These features offer a compelling advantage over traditional manual tracking methods

- The rising popularity of telemedicine and remote patient monitoring also encourages integration of AI and voice-enabled platforms, enabling doctors to manage multiple patients efficiently while maintaining high care standards

- Convenience, real-time monitoring, automated notifications, and personalized care are key factors contributing to the adoption of these AI-enabled Squamous Cell Carcinoma Treatment systems

Restraint/Challenge

“Concerns Regarding Cybersecurity, Data Privacy, and High Initial Costs”

- The reliance on connected devices and cloud-based systems introduces cybersecurity risks, including potential patient data breaches and unauthorized access to treatment protocols.

- For instance, reports of vulnerabilities in connected medical devices have caused some hospitals to delay adoption of voice-activated treatment platforms until additional safeguards are implemented.

- Addressing these concerns requires robust encryption, secure authentication protocols, and regular software updates. Companies like MedLock and OncoTech highlight their stringent security measures to reassure institutions and patients.

- The high initial cost of advanced AI- and voice-enabled Squamous Cell Carcinoma Treatment platforms can limit adoption, particularly in smaller clinics or developing regions

- While basic treatment tracking systems are affordable, premium AI-enabled solutions with predictive analytics and voice integration often come with a significant investment.

- Overcoming these challenges through enhanced cybersecurity, cost-effective solutions, and clinician education will be crucial for sustained market growth.

Squamous Cell Carcinoma Treatment Market Scope

The market is segmented on the basis of drugs, treatment type, route of administration, end-users, and distribution channel.

• By Drugs

On the basis of drugs, the Squamous Cell Carcinoma Treatment market is segmented into Topical Treatment and Targeted Therapy. The Topical Treatment segment dominated the largest market revenue share of 46.5% in 2025, driven by its ease of application and suitability for early-stage lesions. Topical treatments are preferred for outpatient care, minimizing systemic side effects and improving patient compliance. Dermatologists recommend topical agents for superficial squamous cell carcinoma due to localized efficacy. Increasing awareness among patients about non-invasive treatment options supports adoption. Government and insurance coverage for topical therapies enhances accessibility. Pharmaceutical companies continue to develop novel formulations with improved skin penetration. Growing prevalence of skin cancers in aging populations further fuels demand. Clinical evidence demonstrates favorable outcomes with minimal adverse effects. Integration into standard care protocols strengthens market position. Rising skin cancer screening initiatives contribute to early diagnosis, increasing topical treatment uptake. Availability in hospital pharmacies and specialty centers ensures widespread reach. Overall, topical treatment remains the dominant segment due to its convenience and effectiveness.

The Targeted Therapy segment is expected to witness the fastest CAGR of 17.8% from 2026 to 2033, fueled by the growing prevalence of advanced and metastatic cases requiring precision medicine. Targeted therapies inhibit specific molecular pathways involved in tumor growth, offering higher efficacy for aggressive lesions. Adoption is supported by advancements in genomic profiling and personalized medicine approaches. Rising investment in oncology drug development accelerates the introduction of new targeted agents. Hospitals and specialty clinics increasingly offer targeted therapy as part of combination treatment protocols. Insurance coverage for novel therapies improves patient accessibility. Ongoing clinical trials continue to validate therapeutic benefits, encouraging physician adoption. Targeted therapy reduces recurrence rates compared to conventional methods. Awareness campaigns highlight effectiveness in high-risk populations. Technological advancements in drug delivery improve treatment outcomes. Population growth and rising skin cancer incidence sustain market expansion. Overall, targeted therapy emerges as the fastest-growing drug segment in the market.

• By Treatment Type

On the basis of treatment type, the market is segmented into Radiation Therapy, Cryotherapy, Immunotherapy, and Others. The Radiation Therapy segment held the largest market revenue share of 44.7% in 2025, driven by its established efficacy in treating both primary and recurrent tumors. Radiation therapy is widely adopted in hospitals and specialty centers for precise targeting of cancerous tissue. Clinical guidelines recommend radiation as a standard option for patients unsuitable for surgery. Availability of advanced equipment such as linear accelerators enhances treatment accuracy. Increasing skin cancer awareness and early detection programs drive patient referrals. Integration with multidisciplinary oncology care improves outcomes. Hospital infrastructure expansion supports service availability. Insurance coverage and government support increase patient accessibility. Technological improvements reduce side effects and enhance safety. Patient preference for non-invasive options encourages adoption. Education and training programs strengthen clinical adoption. Overall, radiation therapy dominates due to its proven effectiveness and institutional support.

The Immunotherapy segment is expected to witness the fastest CAGR of 18.4% from 2026 to 2033, fueled by innovations in checkpoint inhibitors and immune-modulating therapies. Immunotherapy stimulates the patient’s immune system to target cancer cells, providing durable responses in advanced disease. Rapid advancements in immuno-oncology and clinical trial outcomes drive physician adoption. Growing demand for personalized cancer treatments supports immunotherapy utilization. Hospitals and specialty centers increasingly offer immunotherapy in combination with standard care. Reimbursement policies for novel therapies are improving globally. Research focus on biomarkers enhances treatment efficacy prediction. High unmet needs in recurrent and metastatic cases accelerate adoption. Public awareness campaigns emphasize immunotherapy benefits. Pharmaceutical companies are expanding production capabilities. Patient preference for minimally invasive options supports market growth. Overall, immunotherapy is positioned as the fastest-growing treatment segment in the market.

• By Route of Administration

On the basis of route of administration, the market is segmented into Oral, Parenteral, and Others. The Parenteral segment held the largest market revenue share of 51.2% in 2025, driven by the widespread use of injections and infusions for targeted therapies and immunotherapies. Parenteral administration ensures precise dosing and rapid bioavailability, particularly for advanced-stage patients. Hospital settings are preferred for parenteral treatments due to monitoring requirements. Training and skilled personnel enhance safe administration. Availability of cold-chain logistics ensures drug stability. Government and insurance coverage support hospital-based therapy delivery. Rising incidence of advanced squamous cell carcinoma fuels parenteral therapy demand. Integration into oncology care pathways strengthens adoption. Technological improvements minimize infusion-related complications. Hospitals and specialty centers remain primary points of administration. Population growth and increased cancer detection rates further sustain growth. Overall, parenteral delivery dominates due to effectiveness and institutional infrastructure.

The Oral segment is expected to witness the fastest CAGR of 16.5% from 2026 to 2033, driven by patient preference for convenient, self-administered treatments. Oral formulations reduce hospital visits and increase adherence. Expansion of homecare services supports oral therapy delivery. Pharmaceutical innovation is introducing more potent oral agents with improved safety profiles. Regulatory approvals facilitate rapid market entry for oral formulations. Telemedicine integration aids patient education and compliance. Insurance coverage and affordability improve accessibility. Rising awareness of early-stage treatment options favors oral adoption. Urban populations show increased demand due to convenience. Population growth and higher skin cancer detection rates sustain oral segment expansion. Overall, oral administration is the fastest-growing route of administration in the market.

• By End-Users

On the basis of end-users, the market is segmented into Hospitals, Homecare, Specialty Centres, and Others. The Hospitals segment accounted for the largest market revenue share of 55.3% in 2025, driven by comprehensive care capabilities and access to skilled oncology teams. Hospitals provide multidisciplinary care integrating surgery, radiation, and systemic therapies. Advanced infrastructure and monitoring capabilities ensure effective treatment delivery. Insurance coverage favors hospital-based care for expensive therapies. Hospitals lead in clinical trials and adoption of novel treatments. Patient trust and safety considerations drive preference for hospital care. Expansion of hospital networks increases geographic coverage. Government and NGO initiatives for cancer care are routed through hospitals. Hospitals provide robust patient education and follow-up. Centralized record-keeping improves treatment compliance. Availability of advanced equipment enhances efficacy. Overall, hospitals dominate the end-user segment due to infrastructure and expertise.

The Homecare segment is expected to witness the fastest CAGR of 17.2% from 2026 to 2033, fueled by growing demand for in-home cancer care services. Patients prefer home-based administration of oral therapies and palliative care. Expansion of homecare nursing and telehealth services supports treatment delivery. Convenience and reduced travel improve adherence and satisfaction. Integration with hospital networks ensures continuity of care. Awareness programs emphasize safety and effectiveness of home-administered therapies. Growing adoption in suburban and rural areas drives market penetration. Cost-effectiveness and patient comfort boost uptake. Homecare services cater to chronic and post-treatment management. Digital platforms facilitate scheduling and monitoring. Population growth and increased skin cancer awareness sustain segment growth. Overall, homecare emerges as the fastest-growing end-user segment.

• By Distribution Channel

On the basis of distribution channel, the market is segmented into Hospital Pharmacy, Online Pharmacy, and Retail Pharmacy. The Hospital Pharmacy segment held the largest market revenue share of 52.1% in 2025, driven by integrated treatment services within hospital facilities. Patients receive medications directly after consultations with oncologists, ensuring proper handling and dosing. Cold-chain maintenance supports drug stability. Insurance coverage and government programs often route medications through hospital pharmacies. Skilled pharmacists provide patient education and adherence monitoring. Established hospital pharmacy networks ensure consistent supply. High reliability and regulatory compliance support adoption. Integration with electronic health records improves tracking. Hospitals coordinate immunotherapy, targeted therapy, and oral therapy distribution efficiently. Geographic expansion of hospital pharmacies increases patient reach. Partnerships with pharmaceutical manufacturers strengthen supply. Overall, hospital pharmacies dominate distribution due to reliability and integration.

The Online Pharmacy segment is expected to witness the fastest CAGR of 18.1% from 2026 to 2033, fueled by rising digital adoption and patient preference for home delivery. Online pharmacies enable convenient access to oral medications and supportive therapies. Telehealth integration supports prescription verification and patient counseling. Competitive pricing and subscription models attract consumers. Improved logistics and cold-chain solutions ensure safe delivery. Regulatory support for e-pharmacies expands market reach. Partnerships with manufacturers and specialty centers increase availability. Busy lifestyles and pandemic-driven trends favor digital ordering. Awareness campaigns highlight safety and convenience. Urban and semi-urban populations drive growth. Population expansion and higher incidence of skin cancer sustain demand. Overall, online pharmacy emerges as the fastest-growing distribution channel.

Squamous Cell Carcinoma Treatment Market Regional Analysis

- North America dominated the squamous cell carcinoma treatment market with the largest revenue share of 37.8% in 2025, supported by advanced healthcare facilities, strong research and development activity, high adoption of targeted therapies, and well-established patient access to oncology care

- The region benefits from a highly skilled oncology workforce, widespread availability of early detection programs, and high public awareness of cancer screening, enabling timely treatment initiation and better patient outcomes

- Widespread government support, private insurance coverage, and reimbursement policies further contribute to accessibility of advanced treatment options across both urban and semi-urban regions

U.S. Squamous Cell Carcinoma Treatment Market Insight

The U.S. squamous cell carcinoma treatment market captured the largest revenue share within North America in 2025, driven by rapid adoption of targeted therapies, immunotherapies, and combination treatment protocols. Clinicians are increasingly using precision medicine approaches to tailor therapy to individual patient tumor profiles. Additionally, well-established clinical trial networks and strong pharmaceutical R&D investment are fueling pipeline innovation and expanding treatment options. Rising patient awareness about early screening and treatment efficacy further propels market growth.

Europe Squamous Cell Carcinoma Treatment Market Insight

The Europe squamous cell carcinoma treatment market is projected to expand at a substantial CAGR throughout the forecast period, driven by stringent healthcare regulations, early cancer detection programs, and high adoption of advanced oncology treatments. Increasing urbanization, growing healthcare expenditure, and rising prevalence of skin cancers are fostering adoption of innovative treatment approaches. Key countries such as France, Germany, and Italy are experiencing growth in both hospital-based and outpatient oncology treatment facilities.

U.K. Squamous Cell Carcinoma Treatment Market Insight

The U.K. squamous cell carcinoma treatment market is expected to grow at a notable CAGR during the forecast period, fueled by increased public awareness about skin cancers, government-led screening programs, and improved access to advanced therapies. The expansion of oncology centers and research institutions, combined with growing insurance coverage for innovative treatments, continues to stimulate market growth.

Germany Squamous Cell Carcinoma Treatment Market Insight

The Germany squamous cell carcinoma treatment market is anticipated to expand significantly, driven by well-developed healthcare infrastructure, early diagnosis initiatives, and emphasis on personalized treatment protocols. Rising investment in oncology research and the adoption of innovative therapies, including targeted and combination regimens, are key factors supporting market growth in both hospitals and specialized cancer centers.

Asia-Pacific Squamous Cell Carcinoma Treatment Market Insight

The Asia-Pacific squamous cell carcinoma treatment market is poised to grow at the fastest CAGR during the forecast period, fueled by increasing healthcare spending, rising cancer awareness programs, and expansion of advanced treatment centers in countries such as China, Japan, and India. The region’s growing middle-class population, improving access to oncology care, and government initiatives promoting early detection and treatment adoption are driving market expansion.

Japan Squamous Cell Carcinoma Treatment Market Insight

The Japan squamous cell carcinoma treatment market is witnessing significant growth due to a high prevalence of skin cancers, rapid adoption of targeted therapies, and advanced hospital infrastructure. Increasing emphasis on early detection programs and integration of multidisciplinary oncology treatment approaches are fueling demand for innovative therapies. An aging population further drives the need for accessible, effective treatment solutions.

China Squamous Cell Carcinoma Treatment Market Insight

The China squamous cell carcinoma treatment market accounted for the largest revenue share in Asia-Pacific in 2025, attributed to the country’s expanding middle class, rapid urbanization, and rising cancer incidence. Expansion of specialized oncology centers, government-led cancer awareness initiatives, and increasing adoption of modern treatment regimens such as immunotherapy and combination therapies are key factors propelling market growth.

Squamous Cell Carcinoma Treatment Market Share

The Squamous Cell Carcinoma Treatment industry is primarily led by well-established companies, including:

- Merck & Co. (U.S.)

- Bristol-Myers Squibb (U.S.)

- Roche (Switzerland)

- Novartis (Switzerland)

- Sanofi (France)

- Pfizer (U.S.)

- Amgen (U.S.)

- Astellas Pharma (Japan)

- Sun Pharmaceutical (India)

- Bayer (Germany)

- Takeda Pharmaceutical Company (Japan)

- Eisai Co., Ltd. (Japan)

- F. Hoffmann-La Roche Ltd. (Switzerland)

- Ipsen (France)

- AstraZeneca (Sweden)

- Celgene Corporation (U.S)

- Regeneron Pharmaceuticals (U.S.)

- BeiGene (China)

- Hutchmed (China)

- Incyte Corporation (U.S.)

Latest Developments in Global Squamous Cell Carcinoma Treatment Market

- In December 2024, the U.S. Food and Drug Administration approved UNLOXCYT (cosibelimab‑ipdl) for the treatment of adults with advanced cutaneous squamous cell carcinoma (cSCC) who are not candidates for curative surgery or radiation, marking the first anti‑PD‑L1 therapy approved specifically for this indication and expanding immunotherapy options for advanced skin cancer patients

- In January 2025, Regeneron Pharmaceuticals announced positive results from the Phase 3 C‑POST trial showing that adjuvant treatment with the PD‑1 inhibitor Libtayo (cemiplimab) significantly improved disease‑free survival after surgery in individuals with high‑risk cutaneous squamous cell carcinoma, reinforcing the shift toward immunotherapy in earlier treatment settings

- In May 2025, the U.S. FDA approved retifanlimab‑dlwr (Zynyz) with carboplatin and paclitaxel and as a single agent for the first‑line treatment of adults with inoperable locally recurrent or metastatic squamous cell carcinoma of the anal canal (SCAC), providing a new immunotherapy‑based treatment option beyond skin cancers and showing expansion of PD‑1 inhibitors across squamous carcinoma subtypes

- In October 2025, the U.S. Food and Drug Administration approved cemiplimab‑rwlc (Libtayo) as an adjuvant treatment for adults with cutaneous squamous cell carcinoma at high risk of recurrence following surgery and radiation, representing the first FDA‑approved adjuvant immunotherapy for high‑risk CSCC and reflecting an important milestone in treatment paradigms

- In September 2025, global market reports projected robust growth in the cutaneous squamous cell carcinoma treatment market driven by rising skin cancer incidence, expanded adoption of immunotherapies and targeted therapies such as checkpoint inhibitors, and increasing public awareness and early detection efforts, reinforcing the accelerating evolution of the market landscape

- In November 2025, industry analyses highlighted ongoing innovations including immunotherapies, targeted drugs, and combination treatment strategies being developed by major players like Sanofi, Sun Pharma, and Eli Lilly, underscoring continued advancement and competitive dynamics in the broader squamous cell carcinoma market

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.