Global Stapling And Closure Market

Market Size in USD Billion

CAGR :

%

USD

4.82 Billion

USD

8.92 Billion

2025

2033

USD

4.82 Billion

USD

8.92 Billion

2025

2033

| 2026 - 2033 | |

| USD 4.82 Billion | |

| USD 8.92 Billion | |

| % | |

|

Stapling & Closure Market Overview

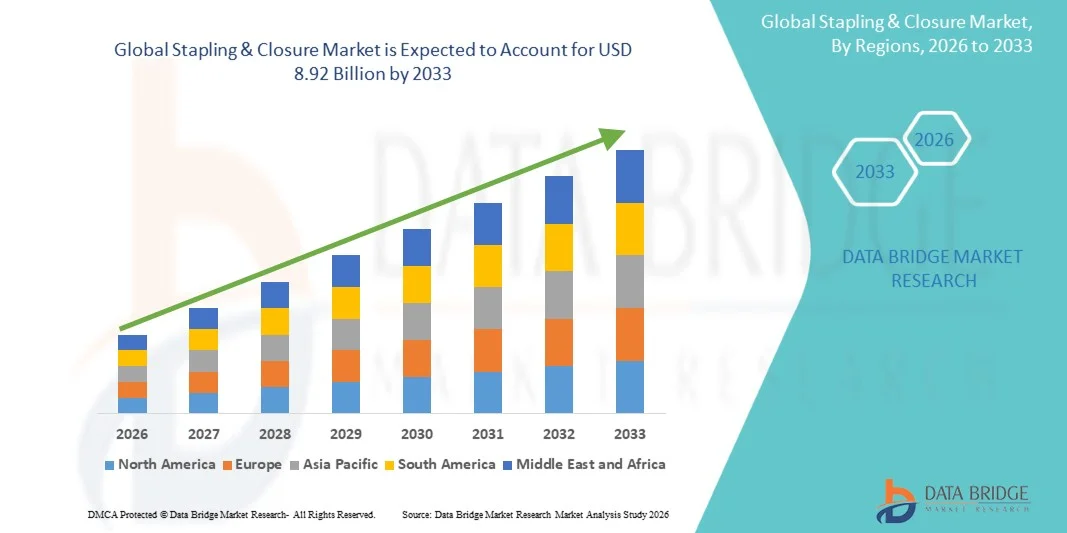

The Stapling & Closure Market was valued at USD 4.82 billion in 2025 and is projected to reach USD 8.92 billion by 2033, growing at a CAGR of 8.00% from 2026 to 2033. The market is experiencing steady growth driven by the increasing volume of surgical procedures worldwide, rising adoption of minimally invasive surgeries, and continuous advancements in wound closure technologies and surgical stapling devices.

The growing prevalence of chronic diseases, trauma injuries, and age-related conditions requiring surgical intervention, combined with the need for faster wound healing and reduced operating times, is encouraging hospitals and surgical centers to adopt advanced stapling and closure solutions. Powered staplers, absorbable sutures, tissue sealants, and surgical adhesives are increasingly replacing conventional wound closure methods in many clinical settings, offering improved precision, reduced complications, and enhanced patient outcomes across general surgery, cardiovascular surgery, orthopedic procedures, and other specialty applications.

Key Market Trends & Insights

- North America dominated the Stapling & Closure Market with the largest revenue share of 38.42% in 2025, supported by high surgical procedure volumes, advanced healthcare infrastructure, and strong adoption of minimally invasive surgical technologies.

- The Surgical Staplers segment led the market with a 44.87% share in 2025, driven by their widespread use across general, gastrointestinal, cardiovascular, and thoracic surgeries.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 7.4% from 2026 to 2033, fueled by expanding healthcare infrastructure, rising healthcare expenditure, and growing access to advanced surgical care in China, India, and Southeast Asia.

- Tissue Sealants & Adhesives are the fastest-growing product type, projected to register a CAGR of 6.9%, reflecting the surge in demand for minimally invasive procedures and advanced wound management solutions.

- The Manual Stapling Systems segment dominated the technology category with a 57.42% revenue share in 2025, led by their extensive utilization across hospitals and surgical centers worldwide.

- General Surgery accounted for 36.18% of the market, preferred by the high volume of abdominal, colorectal, bariatric, and hernia repair procedures performed globally.

- The Cardiovascular Surgery segment is the fastest-growing application category, with a CAGR of 7.3%, driven by the rising prevalence of cardiovascular diseases and increasing surgical treatment rates.

Market Size & Forecast

- Global Market Value (2025): USD 4.82 Billion

- Expected Market Value (2033): USD 8.92 Billion

- Forecast CAGR (2026–2033): 8.00%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia Pacific

Report Scope and Stapling & Closure Market Segmentation

|

Attributes |

Stapling & Closure Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Ethicon, Inc. (U.S.) · Medtronic (Ireland) · Baxter (U.S.) · B. Braun SE (Germany) · Smith+Nephew plc (U.K.) · CONMED Corporation (U.S.) · Stryker (U.S.) · Zimmer Biomet (U.S.) · Intuitive Surgical, Inc. (U.S.) · Olympus Corporation (Japan) · Boston Scientific Corporation (U.S.) · Karl Storz SE & Co. KG (Germany) · Advanced Medical Solutions Group plc (U.K.) · Teleflex Incorporated (U.S.) · Frankenman International Ltd. (China) · Stapleline Medizintechnik GmbH (Germany) · Purple Surgical International Limited (U.K.) · Meril Life Sciences Pvt. Ltd. (India) · Futura Surgicare Pvt. Ltd. (India) · Grena Ltd. (U.K.) |

|

Market Opportunities |

· Expansion of robotic-assisted and minimally invasive surgeries · Growing healthcare infrastructure investments in emerging economies · Rising development of bioabsorbable and antimicrobial closure materials |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Stapling & Closure Market Trends

Trend: Rising Adoption of Powered and Minimally Invasive Surgical Closure Technologies

Healthcare providers are increasingly adopting powered surgical staplers and advanced wound closure products to improve procedural efficiency, reduce operating time, and enhance clinical outcomes without the limitations associated with conventional manual closure methods. The integration of ergonomic designs and intelligent stapling mechanisms enables greater precision during complex procedures and minimizes tissue trauma. Hospitals and ambulatory surgical centers are similarly utilizing advanced closure technologies to support minimally invasive surgeries through standardized, outcome-focused approaches, while bioabsorbable materials and tissue adhesives create effective solutions that closely support natural healing processes. For instance, in March 2024, Johnson & Johnson MedTech expanded its advanced stapling portfolio to support minimally invasive and robotic-assisted surgical procedures, reflecting the growing industry focus on precision closure technologies

Stapling & Closure Market Dynamics

Key Market Driver: Growing Volume of Surgical Procedures and Minimally Invasive Interventions

The increasing number of surgical procedures and the expanding adoption of minimally invasive techniques have created substantial demand for advanced stapling and closure products that can improve procedural consistency, reduce complications, and support faster patient recovery across diverse clinical applications. Hospitals, surgical centers, and specialty care providers are deploying these solutions as a core component of modern surgical workflows, reducing procedure times, enhancing operational efficiency, and improving patient outcomes. The growing burden of chronic diseases and age-related conditions continues to strengthen demand for reliable and technologically advanced wound closure systems. For instance, in 2024, Medtronic continued expanding its surgical stapling technologies designed to improve efficiency and consistency across minimally invasive and open surgical procedures.

Key Restraint/Challenge: High Cost of Advanced Stapling Devices and Closure Solutions

A significant restraint in the global stapling and closure market is the high acquisition cost associated with advanced powered staplers and premium wound closure technologies. Modern systems incorporate sophisticated firing mechanisms, enhanced tissue management capabilities, and specialized materials, requiring substantial investment in procurement, training, and ongoing product utilization. The overall expenditure extends to disposable reloads, maintenance requirements, and inventory management, making adoption challenging for smaller healthcare facilities, cost-sensitive providers, and institutions operating under constrained healthcare budgets. These economic considerations can limit penetration despite the demonstrated clinical benefits of advanced closure technologies.

For instance, in 2024, several hospitals across emerging healthcare markets continued favoring conventional sutures over premium powered stapling systems due to budget constraints and reimbursement limitations, highlighting ongoing adoption challenges.

Key Market Opportunity: Development of Bioabsorbable and Next-Generation Tissue Closure Technologies

The development of bioabsorbable closure materials and advanced tissue sealing technologies presents a significant market opportunity. Next-generation solutions can reduce foreign-body presence, support improved healing outcomes, and minimize post-operative complications while enhancing patient comfort and recovery experiences. The advancement of antimicrobial coatings, regenerative biomaterials, and smart closure systems is further expanding clinical applications, opening growth opportunities across general surgery, cardiovascular procedures, orthopedics, and other specialized surgical fields. These innovations are expected to drive differentiation and long-term market expansion globally. For instance, in 2024, Baxter International continued advancing tissue sealant and hemostatic product development initiatives aimed at improving surgical closure effectiveness and post-operative recovery outcomes.

Stapling & Closure Market Scope

The stapling & closure market is segmented on the basis of product type, technology, application, and end user.

- By Product Type

On the basis of product type, the Stapling & Closure Market is segmented into surgical staplers, sutures, hemostatic agents, tissue sealants & adhesives, and staple line reinforcement materials. The Surgical Staplers segment dominated the market with a 44.87% share in 2025, owing to their widespread use across general, gastrointestinal, cardiovascular, and thoracic surgeries. Surgical staplers help reduce procedure time while providing consistent wound closure and minimizing tissue trauma. Their growing adoption in minimally invasive and laparoscopic procedures has further strengthened market demand. Hospitals increasingly prefer stapling devices due to their ability to improve surgical efficiency and reduce post-operative complications. Continuous technological advancements, including powered staplers and enhanced tissue management systems, are improving clinical outcomes. The increasing global volume of surgical procedures continues to support the segment’s dominant position in the market.

The Tissue Sealants & Adhesives segment is projected to register the fastest growth at a CAGR of 6.9% from 2026 to 2033, driven by increasing demand for minimally invasive procedures and advanced wound management solutions. These products provide effective tissue bonding while reducing the need for traditional sutures and staples in selected procedures. Growing emphasis on faster healing, reduced scarring, and lower infection risks is accelerating adoption across multiple surgical specialties. Advancements in synthetic and biologically derived sealants are expanding their clinical applications. Healthcare providers are increasingly utilizing these products to enhance patient recovery and improve procedural efficiency. Rising investments in innovative biomaterials and regenerative medicine technologies are expected to further support segment growth.

- By Technology

On the basis of technology, the Stapling & Closure Market is segmented into manual stapling systems, powered stapling systems, and robotic-assisted stapling systems. The Manual Stapling Systems segment dominated the market with an estimated 57.42% share in 2025 due to their extensive utilization across hospitals and surgical centers worldwide. These systems are cost-effective, reliable, and widely accepted across a broad range of surgical procedures. Their ease of use and availability make them particularly attractive in developing healthcare markets and budget-sensitive institutions. Manual staplers continue to be preferred for routine surgeries where advanced automation may not be required. Strong physician familiarity and established clinical performance further contribute to sustained demand. The segment benefits from its broad accessibility and lower acquisition costs compared to advanced alternatives.

The Robotic-Assisted Stapling Systems segment is expected to witness the fastest growth at a CAGR of 8.1% from 2026 to 2033, driven by the increasing adoption of robotic surgery platforms globally. These systems offer enhanced precision, improved articulation, and greater control during complex surgical procedures. Growing demand for minimally invasive interventions is encouraging healthcare providers to integrate robotic-assisted technologies into surgical workflows. Advancements in surgical robotics and digital visualization are improving procedural accuracy and patient outcomes. Leading healthcare institutions are investing heavily in robotic operating environments to enhance efficiency and competitiveness. The expanding use of robotic surgery across general, urological, gynecological, and colorectal procedures is expected to accelerate segment growth.

- By Application

On the basis of application, the Stapling & Closure Market is segmented into general surgery, gastrointestinal surgery, cardiovascular surgery, orthopedic surgery, gynecological surgery, thoracic surgery, urology surgery, neurosurgery, and plastic & reconstructive surgery. The General Surgery segment accounted for the largest market share of 36.18% in 2025, supported by the high volume of abdominal, colorectal, bariatric, and hernia repair procedures performed globally. Stapling and closure products are extensively used in these procedures to improve efficiency and ensure reliable tissue approximation. The increasing prevalence of chronic diseases requiring surgical intervention continues to support procedure growth. Healthcare providers favor advanced closure solutions to reduce operating time and enhance patient outcomes. Continuous innovation in surgical devices is improving procedural safety and effectiveness. The broad procedural scope of general surgery remains a key factor supporting segment dominance.

The Cardiovascular Surgery segment is anticipated to register the fastest growth at a CAGR of 7.3% from 2026 to 2033, driven by the rising prevalence of cardiovascular diseases and increasing surgical treatment rates. Advanced stapling and closure technologies are being adopted to improve procedural precision and reduce complications in complex cardiac interventions. Growing aging populations and lifestyle-related risk factors are contributing to higher demand for cardiovascular procedures globally. Technological advancements in tissue sealing and vascular closure systems are expanding treatment capabilities. Healthcare systems are increasingly investing in specialized cardiovascular care infrastructure. The need for improved surgical outcomes and reduced recovery times is expected to further support segment expansion.

- By End User

On the basis of end user, the Stapling & Closure Market is segmented into hospitals, ambulatory surgical centers, specialty clinics, and academic & research institutes. The Hospitals segment dominated the market with a 61.34% share in 2025, owing to the large volume of surgical procedures conducted within hospital settings. Hospitals possess advanced surgical infrastructure, highly skilled healthcare professionals, and access to a broad range of stapling and closure technologies. The increasing number of inpatient and outpatient surgeries continues to drive product utilization. Large healthcare institutions are also early adopters of innovative wound closure solutions and powered surgical devices. Growing investments in surgical modernization programs further support demand. The concentration of complex and high-risk procedures within hospitals strengthens their leading market position.

The Ambulatory Surgical Centers (ASCs) segment is projected to experience the fastest growth at a CAGR of 7.0% from 2026 to 2033, driven by the shift toward outpatient and same-day surgical procedures. ASCs offer cost-effective treatment options, shorter patient stays, and efficient surgical workflows compared to traditional hospital settings. Increasing advancements in minimally invasive surgery are enabling a greater number of procedures to be performed in outpatient environments. Healthcare payers and providers are increasingly supporting ASC utilization to reduce overall healthcare expenditures. The growing preference for convenient and faster treatment experiences is further encouraging patient adoption. Continued expansion of ASC networks worldwide is expected to significantly contribute to segment growth.

Stapling & Closure Market Regional Analysis

North America dominated the Stapling & Closure Market with the largest revenue share of 38.42% in 2025, supported by high surgical procedure volumes, advanced healthcare infrastructure, and strong adoption of minimally invasive surgical technologies. The region also benefits from strong adoption of minimally invasive surgical techniques, increasing utilization of powered stapling technologies, and growing demand for advanced wound closure solutions across hospitals and ambulatory surgical centers. Rising healthcare expenditures, favorable reimbursement frameworks, and continuous technological innovations in surgical devices continue to support market expansion. Increasing focus on improving surgical outcomes and reducing post-operative complications further strengthens North America’s leadership position in the global market.

U.S. Stapling & Closure Market Insight

The U.S. stapling & closure market is witnessing strong growth due to rising surgical procedure volumes, increasing adoption of minimally invasive surgeries, and continuous advancements in wound closure technologies. The country’s mature healthcare infrastructure, along with growing utilization of powered staplers, tissue sealants, and advanced surgical closure systems, is driving demand across hospitals, ambulatory surgical centers, and specialty clinics. In addition, growing emphasis on improving surgical outcomes and reducing post-operative complications is accelerating the adoption of innovative stapling and closure products across healthcare facilities.

Europe Stapling & Closure Market Insight

The Europe stapling & closure market remains a major contributor to global revenue, driven by strong healthcare systems, technological innovation, and high demand for advanced surgical solutions. The widespread use of surgical staplers, tissue adhesives, and hemostatic agents in general, cardiovascular, and gastrointestinal procedures is supporting market expansion across the region. Increasing investments in minimally invasive surgery technologies, coupled with favorable healthcare policies and a highly skilled medical workforce, continue to enhance the adoption of stapling and closure products throughout Europe.

U.K. Stapling & Closure Market Insight

The U.K. stapling & closure market is experiencing steady growth, supported by rising adoption of advanced surgical technologies, increasing procedure volumes, and growing demand for efficient wound management solutions. Increasing investments in modern healthcare infrastructure and growing preference for minimally invasive surgical techniques are contributing to market growth. Furthermore, integration of powered stapling systems and advanced tissue closure products is improving procedural efficiency and patient outcomes, positioning the U.K. as a key innovation hub in the stapling and closure industry.

Germany Stapling & Closure Market Insight

The Germany stapling & closure market is expanding steadily due to the country’s advanced healthcare infrastructure, strong medical device industry, and increasing adoption of next-generation surgical technologies. Hospitals, specialty clinics, and surgical centers are increasingly utilizing stapling and closure products for procedure optimization, wound management, and improved clinical outcomes. Continuous advancements in powered stapling devices, tissue sealants, and minimally invasive surgical techniques, along with strong government support for healthcare innovation, are further driving market growth in Germany.

Asia-Pacific Stapling & Closure Market Insight

The Asia-Pacific stapling & closure market is expected to witness rapid growth, driven by increasing healthcare expenditure, expanding hospital infrastructure, and rising surgical procedure volumes across countries such as China, India, and Japan. Growing awareness regarding advanced wound closure techniques, rising adoption of minimally invasive surgeries, and increasing demand for cost-effective surgical solutions are supporting regional market expansion. Additionally, the growing presence of healthcare modernization initiatives and improving access to advanced medical technologies is accelerating adoption across public and private healthcare sectors.

Japan Stapling & Closure Market Insight

The Japan stapling & closure market is witnessing consistent growth due to rising investments in advanced surgical technologies, healthcare modernization, and patient safety initiatives. Healthcare providers, specialty hospitals, and surgical centers are increasingly adopting innovative stapling and closure solutions for enhanced procedural efficiency and clinical outcomes. Moreover, increasing integration of minimally invasive surgical techniques and the country’s focus on high-quality healthcare delivery are further contributing to market growth.

China Stapling & Closure Market Insight

The China stapling & closure market is growing rapidly, driven by increasing healthcare infrastructure development, expanding surgical volumes, and rising government focus on improving healthcare services. Growing adoption of advanced stapling devices, tissue adhesives, and wound closure technologies across hospitals and specialty clinics is significantly boosting market demand. In addition, rising investments in healthcare modernization, increasing awareness regarding surgical safety, and rapid technological advancements are positioning China as one of the fastest-growing markets for stapling and closure products globally.

Stapling & Closure Market Share

The stapling & closure industry is primarily led by well-established companies, including:

- Ethicon, Inc. (U.S.)

- Medtronic (Ireland)

- Baxter (U.S.)

- Braun SE (Germany)

- Smith+Nephew plc (U.K.)

- CONMED Corporation (U.S.)

- Stryker (U.S.)

- Zimmer Biomet (U.S.)

- Intuitive Surgical, Inc. (U.S.)

- Olympus Corporation (Japan)

- Boston Scientific Corporation (U.S.)

- Karl Storz SE & Co. KG (Germany)

- Advanced Medical Solutions Group plc (U.K.)

- Teleflex Incorporated (U.S.)

- Frankenman International Ltd. (China)

- Stapleline Medizintechnik GmbH (Germany)

- Purple Surgical International Limited (U.K.)

- Meril Life Sciences Pvt. Ltd. (India)

- Futura Surgicare Pvt. Ltd. (India)

- Grena Ltd. (U.K.)

Latest Developments in Stapling & Closure Market

- In June 2025, Johnson & Johnson announced the U.S. launch of the ETHICON™ 4000 Stapler, an advanced surgical stapler designed to improve staple-line integrity and reduce the risk of leaks and bleeding complications. The system incorporates ETHICON™ 3D Reloads with proprietary 3D Stapling Technology and enhanced Gripping Surface Technology to address tissue complexities across multiple surgical specialties. This launch highlights the industry's focus on next-generation powered stapling platforms and robotic surgery integration

- In May 2024, Johnson & Johnson launched the ECHELON LINEAR™ Cutter, the first linear surgical stapler combining 3D-Stapling Technology and Gripping Surface Technology. The device demonstrated 47% fewer leaks at the staple line and was developed to enhance staple-line security and reduce surgical risks during colorectal and other procedures. The launch strengthened Ethicon’s advanced stapling portfolio within the global wound closure market

- In October 2023, Advanced Medical Solutions Group plc announced that all U.S. hospital distribution agreements for its LiquiBand® tissue adhesive portfolio had become operational. The expanded distribution strategy was designed to accelerate market penetration of advanced wound closure products and strengthen the company’s position in the growing tissue adhesive segment. The development reflects increasing adoption of adhesive-based closure technologies as alternatives to traditional sutures and staples

- In June 2023, Advanced Medical Solutions Group plc received U.S. FDA approval for LiquiBandFix8®, an internal surgical adhesive used for hernia mesh fixation. The product utilizes cyanoacrylate adhesive technology instead of traditional fixation tacks, helping reduce tissue trauma and supporting improved patient outcomes. The approval marked a significant advancement in adhesive-based surgical closure technologies and expanded the company’s presence in the surgical fixation market

- In June 2022, Ethicon announced the U.S. launch of the ECHELON™ 3000 Stapler, a digitally enabled powered stapler featuring enhanced articulation, greater jaw aperture, and real-time feedback capabilities. The device was designed to provide surgeons with improved access and control during minimally invasive procedures, supporting the growing trend toward intelligent surgical stapling technologies

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.