Global Surge Protection Devices Market

Market Size in USD Billion

CAGR :

%

USD

3.99 Billion

USD

6.12 Billion

2025

2033

USD

3.99 Billion

USD

6.12 Billion

2025

2033

| 2026 –2033 | |

| USD 3.99 Billion | |

| USD 6.12 Billion | |

| % | |

|

Global Surge Protection Devices Market Overview

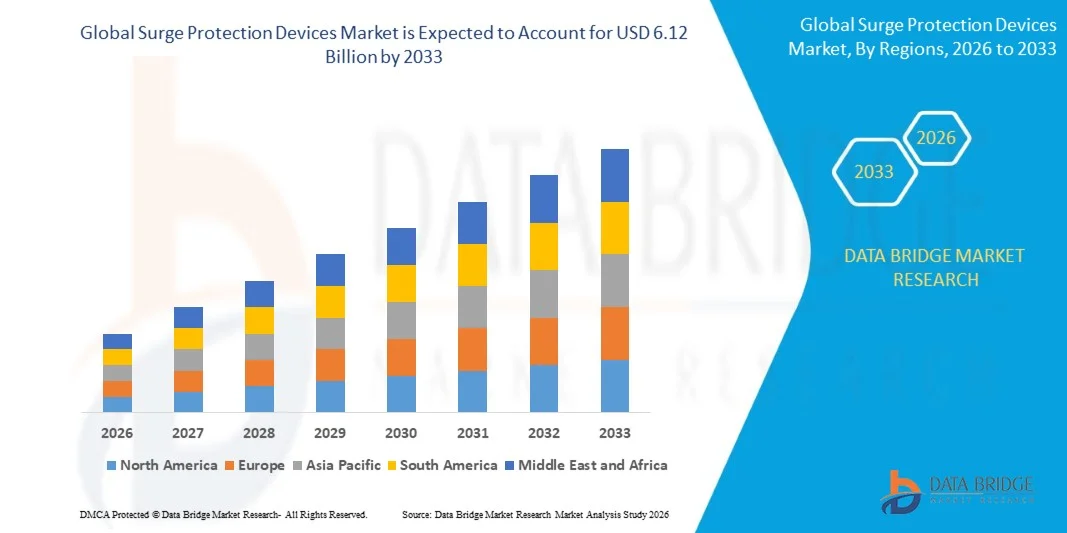

The global surge protection devices market was valued at USD 3.99 billion in 2025 and is projected to reach USD 6.12 billion by 2033, growing at a CAGR of 5.50% from 2026 to 2033. The market is experiencing steady growth driven by rising demand for reliable power protection systems, increasing deployment of sensitive electronic equipment, and rapid expansion of smart grid and industrial automation infrastructure across residential, commercial, and industrial sectors.

The increasing frequency of power fluctuations, lightning-induced surges, and grid instability globally, combined with growing dependence on connected electronic systems and critical digital infrastructure, is compelling industries and consumers to adopt advanced surge protection solutions. Type 1, Type 2, and smart surge protection devices are increasingly being integrated into data centers, telecommunications infrastructure, manufacturing facilities, renewable energy systems, and smart buildings to prevent equipment damage, minimize downtime, and improve operational reliability across modern electrical networks

Key Market Trends & Insights

- North America dominated the global driving simulators market with the largest revenue share of 39.6% in 2025, supported by extensive deployment of advanced electrical infrastructure, strong adoption of industrial automation, and high penetration of data centers and renewable energy installations.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR from 2026 to 2033, fueled by rapid urbanization, large-scale infrastructure development, and increasing adoption of smart grid and renewable energy systems.

- The Hard-Wired Surge Protection Devices segment held the largest market revenue share of approximately 52.6% in 2025 driven by its extensive deployment in industrial facilities, commercial buildings, and utility-scale power systems where permanent, high-capacity protection is required against lightning-induced and switching surges.

- The Plug in Surge Protection Devices segment is projected to register the fastest growth at a CAGR of 9.4% from 2026 to 2033, driven by increasing adoption in residential electronics, small offices, and consumer-level protection needs for computers, smart home systems, and entertainment devices.

- The Industrial segment held the largest market revenue share of approximately 45.3% in 2025 driven by high dependency on automated machinery, power distribution systems, and sensitive control equipment across manufacturing plants, oil and gas facilities, and utilities.

- The Residential segment is projected to register the fastest growth at a CAGR of 8.7% from 2026 to 2033, driven by increasing adoption of home automation systems, smart appliances, and rising incidents of lightning-related electrical damage in urban and semi-urban regions.

- The 10 kA–25 kA segment held the largest market revenue share of approximately 48.1% in 2025 driven by its balanced performance suitability for commercial buildings, telecom infrastructure, and industrial control systems where moderate-to-high surge protection is required without excessive system cost or complexity.

- The Above 25 kA segment is projected to register the fastest growth at a CAGR of 10.2% from 2026 to 2033, driven by increasing deployment in heavy industrial applications, renewable energy installations, and utility-scale power networks exposed to frequent lightning strikes and high-energy surge events.

- The Metal Oxide Varistor segment held the largest market revenue share of approximately 57.9% in 2025 driven by its widespread use as the primary surge suppression component due to its fast response time, cost-effectiveness, and ability to absorb high transient energy levels in both low-voltage and medium-voltage applications.

- The Silicon Avalanche Diode segment is projected to register the fastest growth at a CAGR of 11.1% from 2026 to 2033, driven by increasing demand for highly precise voltage clamping in sensitive electronics such as data center equipment, telecommunications systems, and semiconductor manufacturing tools.

Market Size & Forecast

- Global Market Value (2025): USD 3.99 Billion

- Expected Market Value (2033): USD 6.12 Billion

- Forecast CAGR (2026–2033): 5.50%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Surge Protection Devices Market Segmentation

|

Attributes |

Surge Protection Devices Key Market Insights |

|

Segments Covered |

· By Type: Hard Wired Surge Protection Devices, Plug in Surge Protection Devices, Line Cord Surge Protectors, and Power Control Devices Surge Protection Devices · By End- User: Industrial, Commercial, and Residential · By Discharge Current: Below 10 kA, 10 kA–25 kA, and Above 25 kA · By Component: Metal Oxide Varisto, Gas Discharge Tube, Silicon Avalanche Diode, and Others |

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

• ABB (Switzerland) |

|

Market Opportunities |

• Expansion Of Smart Grid And Renewable Energy Infrastructure • Rising Adoption Of IoT-Enabled Surge Protection Systems |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Global Surge Protection Devices Market Trends

Trend: Growth In Renewable Energy Integration, Smart Grid Expansion, And Advanced Electrical Safety Systems

The global surge protection devices (SPDs) market is witnessing strong growth due to increasing electrification across residential, commercial, and industrial infrastructure, along with rising vulnerability of modern electronic systems to voltage spikes and transient surges. Rapid expansion of renewable energy installations, such as solar PV and wind farms, is increasing exposure to lightning-induced surges and grid instability, driving demand for advanced protection systems. Conventional electrical networks are becoming more sensitive due to widespread adoption of semiconductor-based devices, which require highly stable voltage conditions and precise protection against transient disturbances.

In modern data centers, surge protection devices are being widely deployed to safeguard mission-critical servers and cloud infrastructure from lightning strikes and switching surges, particularly in hyperscale facilities across the U.S., Europe, and Asia-Pacific. For instance, large-scale data center operators are integrating Type 1 and Type 2 SPDs compliant with IEC 61643 standards to reduce downtime risks caused by power anomalies. In renewable installations, solar inverters and wind turbine control systems are increasingly equipped with multi-stage surge protection architectures to prevent damage from grid fluctuations and atmospheric lightning events. Additionally, transportation infrastructure such as electric vehicle charging stations and metro rail systems are adopting SPDs to ensure operational stability under high-load switching conditions. Global lightning activity, estimated at nearly 100 lightning flashes per second worldwide, continues to reinforce the need for robust surge mitigation solutions across exposed infrastructure networks.

Global Surge Protection Devices Market Dynamics

Key Market Driver: Rising Electrification And Expansion Of Critical Digital Infrastructure

The increasing dependence on digital infrastructure, electrified transport systems, and automated industrial operations is significantly driving demand for surge protection devices. Industries such as telecommunications, oil and gas, manufacturing, and utilities are deploying sensitive electronic control systems that are highly vulnerable to transient overvoltage conditions caused by switching operations, lightning strikes, and grid disturbances.

Data center expansion, particularly driven by AI workloads and cloud computing demand, is accelerating SPD adoption to ensure uninterrupted uptime and prevent costly equipment failures. For instance, hyperscale facilities operated by major cloud providers are implementing layered surge protection systems at service entrances, distribution panels, and equipment racks to maintain continuity of operations. Similarly, renewable energy expansion across India, China, and Europe is increasing installation of SPDs in solar combiner boxes and wind turbine nacelles to protect power electronics from high-frequency voltage spikes. Industrial automation systems and smart factories are also integrating advanced surge protection to safeguard PLCs, robotics, and control systems from electrical transients, thereby improving operational reliability and reducing maintenance costs.

Key Restraint/Challenge: High Installation Complexity And Limited Awareness In Emerging Markets

Despite strong demand growth, the surge protection devices market faces challenges related to inconsistent installation practices, lack of technical awareness, and improper system coordination in low and mid-voltage applications. Many end users underestimate the importance of multi-layer surge protection design, leading to insufficient protection against indirect lightning strikes and internal switching surges.

In addition, integration complexity with legacy electrical infrastructure increases deployment challenges, particularly in older industrial facilities and residential buildings where electrical grounding systems may not meet modern safety standards. Cost sensitivity in emerging economies further limits widespread adoption of high-performance SPD systems, especially in small commercial and residential segments. Field studies in industrial regions of Southeast Asia and South America have shown that a significant portion of electrical equipment failures linked to transient overvoltage events occur due to absence or improper sizing of surge protection devices, highlighting the gap between awareness and implementation.

Key Market Opportunity: Expansion In Smart Grids, EV Infrastructure, And Renewable Energy Systems

The rapid development of smart grids, electric mobility infrastructure, and distributed renewable energy systems is creating significant opportunities for surge protection device manufacturers. Modern power systems are becoming increasingly decentralized, with bidirectional energy flow and higher exposure to switching transients, making advanced surge protection essential for system stability.

Electric vehicle charging networks, including fast-charging and ultra-fast charging stations, are increasingly deploying SPDs to protect power conversion modules and charging electronics from voltage spikes during high-load switching events. For instance, public EV charging infrastructure expansion across Europe and China is integrating coordinated surge protection across AC and DC charging circuits to ensure equipment longevity and user safety. In renewable energy systems, floating solar farms and offshore wind installations are adopting ruggedized SPD solutions designed to withstand harsh environmental conditions and frequent lightning exposure. Additionally, advancements in modular and smart surge protection technologies with remote monitoring capabilities are opening new opportunities in industrial IoT and predictive maintenance applications across North America and Asia-Pacific markets.

Global Surge Protection Devices Market Scope

The market is segmented on the basis of type, end-user, discharge current, and component.

- By Type

On the basis of type, the surge protection devices market is segmented into Hard Wired Surge Protection Devices, Plug in Surge Protection Devices, Line Cord Surge Protectors, and Power Control Devices Surge Protection Devices. The Hard Wired Surge Protection Devices segment held the largest market revenue share of approximately 52.6% in 2025 driven by its extensive deployment in industrial facilities, commercial buildings, and utility-scale power systems where permanent, high-capacity protection is required against lightning-induced and switching surges. These devices are widely integrated into main distribution panels and substations due to their higher durability, compliance with IEC 61643 standards, and ability to handle high surge currents in mission-critical infrastructure.

The Plug in Surge Protection Devices segment is projected to register the fastest growth at a CAGR of 9.4% from 2026 to 2033, driven by increasing adoption in residential electronics, small offices, and consumer-level protection needs for computers, smart home systems, and entertainment devices. Rising awareness of electronic device protection and growing penetration of IoT-enabled appliances are accelerating demand for compact and user-friendly surge protection solutions across urban households.

- By End-User

On the basis of end-user, the surge protection devices market is segmented into Industrial, Commercial, and Residential. The Industrial segment held the largest market revenue share of approximately 45.3% in 2025 driven by high dependency on automated machinery, power distribution systems, and sensitive control equipment across manufacturing plants, oil and gas facilities, and utilities. Industries increasingly deploy multi-stage surge protection architectures to safeguard PLCs, motors, and SCADA systems from transient voltage disruptions caused by grid instability and heavy electrical switching operations.

The Residential segment is projected to register the fastest growth at a CAGR of 8.7% from 2026 to 2033, driven by increasing adoption of home automation systems, smart appliances, and rising incidents of lightning-related electrical damage in urban and semi-urban regions. Growing penetration of high-value consumer electronics such as smart TVs, routers, and home security systems is further accelerating the need for affordable and easy-to-install surge protection solutions.

- By Discharge Current

On the basis of discharge current, the surge protection devices market is segmented into Below 10 kA, 10 kA–25 kA, and Above 25 kA. The 10 kA–25 kA segment held the largest market revenue share of approximately 48.1% in 2025 driven by its balanced performance suitability for commercial buildings, telecom infrastructure, and industrial control systems where moderate-to-high surge protection is required without excessive system cost or complexity. These devices are widely used as secondary protection layers in coordinated surge protection systems.

The Above 25 kA segment is projected to register the fastest growth at a CAGR of 10.2% from 2026 to 2033, driven by increasing deployment in heavy industrial applications, renewable energy installations, and utility-scale power networks exposed to frequent lightning strikes and high-energy surge events. Expansion of solar farms and wind energy projects in Asia-Pacific and Europe is significantly contributing to demand for high-capacity surge protection systems.

- By Component

On the basis of component, the surge protection devices market is segmented into Metal Oxide Varistor, Gas Discharge Tube, Silicon Avalanche Diode, and Others. The Metal Oxide Varistor segment held the largest market revenue share of approximately 57.9% in 2025 driven by its widespread use as the primary surge suppression component due to its fast response time, cost-effectiveness, and ability to absorb high transient energy levels in both low-voltage and medium-voltage applications. MOVs are extensively used in power strips, industrial SPDs, and building protection systems.

The Silicon Avalanche Diode segment is projected to register the fastest growth at a CAGR of 11.1% from 2026 to 2033, driven by increasing demand for highly precise voltage clamping in sensitive electronics such as data center equipment, telecommunications systems, and semiconductor manufacturing tools. Rising miniaturization of electronic devices and increasing reliance on high-speed digital circuits are accelerating adoption of advanced semiconductor-based surge protection technologies.

Global Surge Protection Devices Market Regional Analysis

- North America dominated the surge protection devices market with the largest revenue share of 39.6% in 2025, driven by extensive deployment of advanced electrical infrastructure, strong adoption of industrial automation, and high penetration of data centers and renewable energy installations

- End users in the region highly prioritize electrical safety, equipment reliability, and compliance with stringent standards such as UL 1449 and IEEE surge protection guidelines, accelerating adoption across residential, commercial, and industrial applications

- This widespread adoption is further supported by rapid expansion of hyperscale cloud facilities, increasing electrification of transportation systems, and high investment in grid modernization projects, establishing surge protection devices as a critical component of modern power distribution networks

U.S. Surge Protection Devices Market Insight

The U.S. surge protection devices market captured the largest revenue share in 2025 within North America, driven by rapid expansion of hyperscale data centers, industrial automation systems, and renewable energy installations. Increasing reliance on sensitive electronic infrastructure across IT, telecom, and manufacturing sectors is significantly boosting demand for multi-layer surge protection architectures. For instance, large-scale cloud service providers in the U.S. are widely deploying coordinated SPD systems across power distribution units and server racks to minimize downtime risks. Additionally, growing adoption of solar and wind energy projects, combined with increasing EV charging infrastructure deployment, is further strengthening market expansion. Rising incidents of lightning-induced electrical failures in high-density industrial zones are also reinforcing the need for advanced surge protection solutions.

Europe Surge Protection Devices Market Insight

The Europe surge protection devices market is expected to witness the fastest growth rate from 2026 to 2033, primarily driven by stringent electrical safety regulations, rapid expansion of renewable energy capacity, and increasing electrification of transportation systems. The region’s strong focus on grid stability and energy efficiency is accelerating adoption of SPDs in industrial automation, commercial buildings, and utility-scale renewable projects. For instance, solar PV installations across Germany, Spain, and Italy are increasingly integrating Type 1 and Type 2 surge protection systems to safeguard inverters and power electronics from lightning-induced surges. Additionally, rising deployment of smart factories under Industry 4.0 initiatives is further contributing to steady market growth across the region.

U.K. Surge Protection Devices Market Insight

The U.K. surge protection devices market is expected to witness strong growth from 2026 to 2033, driven by increasing investment in smart infrastructure, data center expansion, and growing awareness of electrical safety in residential and commercial sectors. Rising frequency of extreme weather events, including lightning storms, is encouraging wider adoption of surge protection solutions in building electrical systems. Additionally, the rapid growth of fintech, cloud computing, and telecom infrastructure in cities such as London is significantly increasing demand for uninterrupted power protection systems. Expansion of EV charging networks across urban and highway corridors is further supporting market adoption.

Germany Surge Protection Devices Market Insight

The Germany surge protection devices market is expected to witness steady growth from 2026 to 2033, fueled by strong industrial automation, high penetration of renewable energy systems, and strict adherence to DIN and IEC electrical safety standards. Germany’s manufacturing sector, particularly automotive and machinery production, is increasingly deploying advanced surge protection systems to safeguard sensitive control equipment and robotics infrastructure. For instance, industrial facilities are integrating coordinated SPD systems within smart factory setups to prevent downtime caused by voltage transients. Additionally, the country’s rapid expansion of wind energy installations is further boosting demand for high-capacity surge protection solutions.

Asia-Pacific Surge Protection Devices Market Insight

The Asia-Pacific surge protection devices market is expected to witness the fastest growth rate from 2026 to 2033, driven by rapid urbanization, large-scale infrastructure development, and increasing adoption of smart grid and renewable energy systems. Countries such as China, India, and South Korea are witnessing significant expansion in industrial automation, data centers, and EV charging infrastructure, all of which require advanced surge protection solutions. Government initiatives promoting electrification and smart city development are further accelerating adoption. For instance, large solar parks and wind farms across India and China are increasingly deploying SPDs to protect critical power electronics from frequent lightning and grid fluctuations.

Japan Surge Protection Devices Market Insight

The Japan surge protection devices market is expected to witness strong growth from 2026 to 2033 due to the country’s highly advanced electrical infrastructure, increasing adoption of smart homes, and strong focus on disaster-resilient systems. Japan’s frequent exposure to typhoons and lightning events is driving widespread deployment of surge protection systems in residential, commercial, and industrial applications. Additionally, increasing integration of robotics, IoT systems, and semiconductor manufacturing equipment is boosting demand for highly precise voltage protection solutions. Expansion of EV infrastructure and smart city projects is further supporting market growth across urban regions.

China Surge Protection Devices Market Insight

The China surge protection devices market accounted for the largest market revenue share in Asia Pacific in 2025, attributed to rapid industrialization, large-scale infrastructure development, and strong expansion of renewable energy capacity. China is one of the largest producers and consumers of electrical equipment, with widespread adoption of surge protection systems across manufacturing plants, data centers, and commercial buildings. For instance, massive deployment of solar PV farms in western China and offshore wind projects is significantly increasing demand for high-capacity SPDs. Additionally, rapid growth of EV charging networks and smart city initiatives is further strengthening market penetration across urban and industrial regions.

Global Surge Protection Devices Market Share

The Surge Protection Devices industry is primarily led by well-established companies, including:

• Zhejiang Yuelong Electric Co., Ltd (China)

• True Power Earthings Private Limited (India)

• Havells India Ltd. (India)

• ABB (Switzerland)

• Schneider Electric (France)

• Cirprotec, S.L. (Spain)

• Eaton (Ireland)

• Littelfuse, Inc. (U.S.)

• MERSEN (France)

• Bourns, Inc. (U.S.)

• Infineon Technologies AG (Germany)

• JEF Techno (Japan)

• City of PHOENIX (U.S.)

• Emerson Electric Co. (U.S.)

• Siemens (Germany)

• Belkin International, Inc. (U.S.)

• Leviton Manufacturing Co., Inc. (U.S.)

• Nortek Control (U.S.)

• Raycap (U.S.)

• Hubbell (U.S.)

• Legrand Group (France)

• Koninklijke Philips N.V. (Netherlands)

• JMV LPS Limited (India)

• ISG Global (U.S.)

Latest Developments in Global Surge Protection Devices Market

- In October 2025, Schneider Electric introduced a plug-and-play surge protection device (SPD) in the U.K., designed for direct integration with Acti9 and KQ Loadcentre distribution boards. The development features an all-in-one design with an embedded backup fuse, eliminating the need for external disconnectors or additional components. It enables faster plug-in installation, reduces labor time, and lowers overall system costs for contractors. The solution is aligned with BS 7671:2018 regulatory requirements, strengthening compliance in commercial and industrial electrical systems. This innovation enhances transient overvoltage protection efficiency and is expected to accelerate adoption of advanced SPDs across modern electrical infrastructure markets.

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Surge Protection Devices Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Surge Protection Devices Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Surge Protection Devices Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.