Global Surgical Meshes Market

Market Size in USD Billion

CAGR :

%

USD

2.67 Billion

USD

4.76 Billion

2025

2033

USD

2.67 Billion

USD

4.76 Billion

2025

2033

| 2026 - 2033 | |

| USD 2.67 Billion | |

| USD 4.76 Billion | |

| % | |

|

Surgical Meshes Market Overview

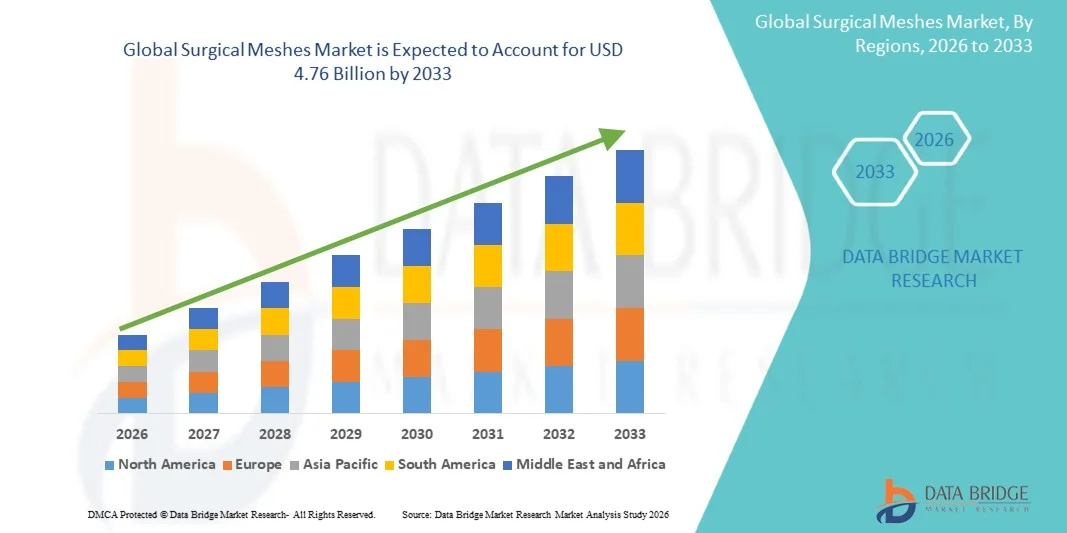

The Surgical Meshes Market was valued at USD 2.67 billion in 2025 and is projected to reach USD 4.76 billion by 2033, growing at a CAGR of 7.50% from 2026 to 2033. The market is experiencing steady growth driven by the rising prevalence of hernias and chronic wounds, increasing volume of surgical procedures, and continuous advancements in biomaterial technologies and minimally invasive surgical techniques.

The growing burden of obesity, aging populations, and lifestyle-related disorders has led to a higher incidence of hernia repairs and soft tissue reconstruction procedures worldwide, driving demand for surgical meshes. In addition, the increasing preference for laparoscopic and robotic-assisted surgeries is accelerating the adoption of lightweight, composite, and biologic mesh products that offer improved biocompatibility, reduced postoperative complications, and faster recovery times. Technological innovations in absorbable and antimicrobial meshes, coupled with expanding healthcare infrastructure and greater access to surgical care in emerging economies, are further supporting market growth. Rising awareness among healthcare providers regarding effective tissue reinforcement and favorable reimbursement policies in developed markets continue to strengthen the adoption of surgical mesh products across a wide range of surgical applications.

Key Market Trends & Insights

- North America dominated the Surgical Meshes Market with the largest revenue share of 38.46% in 2025, supported by a high volume of hernia repair procedures, advanced healthcare infrastructure, favorable reimbursement policies, and strong adoption of innovative mesh technologies.

- The Non-Absorbable Surgical Mesh segment led the market with a 57.82% share in 2025, driven by its proven long-term durability, widespread use in hernia repair surgeries, and strong clinical acceptance among surgeons.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 8.1% from 2026 to 2033, fueled by expanding healthcare infrastructure, increasing surgical procedure volumes, growing medical tourism, and rising healthcare expenditure across China, India, and Southeast Asian countries.

- The Absorbable Surgical Mesh segment is the fastest-growing type category, projected to register a CAGR of 8.7%, reflecting increasing demand for advanced biomaterials that reduce long-term complications and improve patient outcomes.

- The Hernia Repair segment dominates the application category with a 63.24% revenue share in 2025, led by the growing prevalence of inguinal, ventral, and incisional hernias worldwide and the increasing adoption of mesh-based repair procedures.

- Hospitals account for 61.38% of the market, preferred due to their advanced surgical capabilities, availability of specialized surgeons, and high volume of complex abdominal and reconstructive procedures.

- The Distribution Channel segment held a 54.67% market share in 2025, driven by the extensive networks of medical device distributors that enable broad product availability across hospitals, ambulatory surgical centers, and clinics.

- The Abdominal Wall Reconstruction segment is the fastest-growing application category, with a CAGR of 8.4%, supported by increasing cases of complex abdominal defects, rising obesity rates, and growing adoption of biologic and composite mesh products in reconstructive surgeries.

- The Hernia Repair segment dominated the market with a 24% share in 2025 owing to the increasing prevalence of inguinal, femoral, umbilical, and ventral hernias worldwide

Market Size & Forecast

- Global Market Value (2025): USD 2.67 Billion

- Expected Market Value (2033): USD 4.76 Billion

- Forecast CAGR (2026–2033): 7.50%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Surgical Meshes Market Segmentation

|

Attributes |

Surgical Meshes Key Market Insights |

|

Segments Covered |

· By Type: Non-Absorbable Surgical Mesh, Absorbable Surgical Mesh, and Others · By Application: Hernia Repair, Traumatic or Surgical Wounds, Abdominal Wall Reconstruction, and Other Facial Surgery · By End User: Hospitals, Ambulatory Surgical Centers, Clinics, and Others · By Sales Channel: Direct Channel and Distribution Channel |

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Becton, Dickinson and Company (BD) (U.S.) · Johnson & Johnson (Ethicon) (U.S.) · Medtronic plc (Ireland) · B. Braun SE (Germany) · W. L. Gore & Associates, Inc. (U.S.) · Getinge AB (Sweden) · Baxter International Inc. (U.S.) · Cook Medical LLC (U.S.) · Integra LifeSciences Holdings Corporation (U.S.) · TELA Bio, Inc. (U.S.) · Atrium Medical Corporation (U.S.) · LifeCell Corporation (an AbbVie company) (U.S.) · RTI Surgical Holdings, Inc. (U.S.) · Groupe Cousin Biotech (France) · FEG Textiltechnik mbH (Germany) · Proxy Biomedical Ltd. (Ireland) · THT Bio-Science Group (Netherlands) · Meril Life Sciences Pvt. Ltd. (India) · Healthium Medtech Limited (India) · Lotus Surgicals Pvt. Ltd. (India) · Sutures India Pvt. Ltd. (India) · Futura Surgicare Pvt. Ltd. (India) · Mesh Suture Inc. (U.S.) · BioCer Entwicklungs-GmbH (Germany) · Dipromed S.r.l. (Italy) · Assut Europe S.p.A. (Italy) · PFM Medical AG (Germany) · Aroa Biosurgery Limited (New Zealand) · Gunze Limited (Japan) · Samyang Biopharmaceuticals Corporation (South Korea) · Riverpoint Medical LLC (U.S.) · Deep Blue Medical Advances, Inc. (U.S.) · Tissium SA (France) · Poly-Med, Inc. (U.S.) |

|

Market Opportunities |

· Growing Adoption of Biologic and Absorbable Surgical Meshes · Rising Demand in Emerging Healthcare Markets · Increasing Volume of Minimally Invasive and Robotic Surgeries |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Surgical Meshes Market Trends

Trend: Rising Adoption of Biologic and Absorbable Surgical Meshes

The surgical meshes market is witnessing a strong shift toward biologic and absorbable mesh products as healthcare providers seek solutions that reduce long-term complications, chronic pain, infection risks, and foreign-body reactions. Advanced biomaterial technologies are enabling the development of meshes that provide temporary support while promoting natural tissue regeneration. These products are increasingly being utilized in complex hernia repairs, abdominal wall reconstruction procedures, and contaminated surgical fields where permanent synthetic meshes may be less suitable. Growing clinical evidence supporting improved patient outcomes, coupled with increasing surgeon preference for personalized treatment approaches, is accelerating adoption across developed healthcare markets.

Surgical Meshes Market Dynamics

Key Market Driver: Increasing Incidence of Hernia and Abdominal Wall Reconstruction Procedures

The rising prevalence of hernias worldwide is a major factor driving demand for surgical meshes. According to the healthcare literature, millions of hernia repair procedures are performed globally each year, making hernia repair one of the most common general surgical procedures. Factors such as aging populations, obesity, heavy physical labor, and previous abdominal surgeries are contributing to increased hernia incidence. Surgical meshes have become the standard of care in most hernia repair procedures due to their ability to reduce recurrence rates and improve long-term outcomes. Furthermore, growing adoption of minimally invasive laparoscopic and robotic-assisted surgical techniques is supporting demand for lightweight and advanced mesh products designed for enhanced surgical performance and faster patient recovery.

Key Restraint/Challenge: Product Recall Risks and Postoperative Complications

Despite technological advancements, concerns regarding mesh-related complications remain a significant challenge for market growth. Issues such as infection, adhesion formation, mesh migration, chronic pain, and recurrence continue to attract regulatory scrutiny and litigation in several countries. Product recalls and safety concerns can negatively impact physician confidence and patient acceptance. In addition, stringent regulatory approval requirements for novel biomaterials increase product development timelines and compliance costs. Manufacturers must continuously invest in clinical studies, post-market surveillance, and quality assurance programs to demonstrate long-term safety and effectiveness.

For instance, several mesh manufacturers have faced product safety reviews and litigation over the past decade, prompting healthcare providers to carefully evaluate product selection and encouraging regulators to impose stricter clinical evidence requirements before commercialization.

Key Market Opportunity: Expansion of Advanced Biomaterials and Regenerative Medicine Applications

The integration of regenerative medicine and next-generation biomaterials presents a significant opportunity for the surgical meshes market. Companies are increasingly developing biologic, hybrid, and bioresorbable meshes designed to enhance tissue healing while minimizing foreign-body response. These innovations are particularly valuable in complex abdominal wall reconstruction, trauma surgery, and high-risk patient populations.

A notable example is the continued expansion of reinforced tissue matrices and extracellular matrix-based mesh products that support tissue regeneration while providing mechanical strength. Furthermore, increasing investments in healthcare infrastructure across Asia-Pacific, Latin America, and the Middle East are expanding access to advanced surgical procedures, creating new growth opportunities for premium mesh technologies. The growing adoption of robotic surgery platforms is also expected to drive demand for specialized mesh products optimized for minimally invasive surgical applications, supporting long-term market expansion.

Surgical Meshes Market Scope

The Surgical Meshes market is segmented on the basis of type, application, end user, and sales channel.

- By Type

On the basis of type, the Surgical Meshes Market is segmented into Non-Absorbable Surgical Mesh, Absorbable Surgical Mesh, and Others. The Non-Absorbable Surgical Mesh segment dominated the market with a 57.82% share in 2025 due to its superior tensile strength, long-term durability, and widespread use in hernia repair and abdominal wall reinforcement procedures. These meshes provide permanent structural support to weakened tissues, significantly reducing the risk of hernia recurrence. The segment's dominance is further supported by extensive clinical evidence demonstrating favorable long-term outcomes and surgeon familiarity with polypropylene and polyester-based mesh products. Growing numbers of inguinal, ventral, and incisional hernia surgeries worldwide continue to drive demand. In addition, healthcare providers often prefer non-absorbable meshes for patients requiring durable tissue reinforcement. Strong product availability, established reimbursement pathways, and continuous improvements in lightweight and composite mesh designs further reinforce the segment's leading position. The increasing adoption of minimally invasive hernia repair techniques has also contributed to sustained utilization of non-absorbable meshes across hospitals and surgical centers globally.

The Absorbable Surgical Mesh segment is expected to witness the fastest CAGR of 8.7% from 2026 to 2033, driven by growing demand for advanced biomaterials that minimize long-term foreign-body reactions and postoperative complications. These meshes gradually degrade after providing temporary support, promoting natural tissue regeneration and healing. Increasing surgeon preference for absorbable products in contaminated surgical fields and complex reconstruction procedures is accelerating adoption. Technological advancements in bioresorbable polymers and regenerative medicine are further enhancing product effectiveness. Rising awareness regarding chronic pain and mesh-related complications associated with permanent implants is encouraging healthcare providers to consider absorbable alternatives. Growing investments in biomaterial research, coupled with expanding clinical evidence supporting favorable patient outcomes, are expected to drive substantial market growth throughout the forecast period.

- By Application

On the basis of application, the Surgical Meshes Market is segmented into Hernia Repair, Traumatic or Surgical Wounds, Abdominal Wall Reconstruction, and Other Facial Surgery. The Hernia Repair segment dominated the market with a 63.24% share in 2025 owing to the increasing prevalence of inguinal, femoral, umbilical, and ventral hernias worldwide. Surgical meshes have become the standard of care for most hernia repair procedures due to their ability to reduce recurrence rates and improve long-term surgical outcomes. Growing obesity rates, aging populations, and increasing abdominal surgeries are contributing to a higher incidence of hernias globally. The widespread adoption of laparoscopic and robotic-assisted hernia repair procedures has further accelerated mesh utilization. Strong clinical guidelines recommending mesh-based repairs and increasing patient awareness regarding advanced treatment options continue to support segment growth. Moreover, continuous innovation in lightweight, composite, and biologic meshes is enhancing procedural success rates and postoperative recovery.

The Abdominal Wall Reconstruction segment is anticipated to witness the fastest CAGR of 8.4% from 2026 to 2033, driven by rising cases of complex abdominal defects, trauma injuries, tumor resections, and recurrent hernias. Increasing demand for advanced reconstructive procedures requiring durable tissue reinforcement is fueling mesh adoption. Surgeons are increasingly utilizing biologic and hybrid meshes in complex reconstruction cases to improve healing outcomes and reduce complications. Growing healthcare expenditure, improved surgical capabilities, and expanding access to specialized reconstructive procedures are supporting market expansion. Furthermore, advancements in regenerative medicine and next-generation biomaterials are creating significant opportunities for innovative mesh products designed specifically for abdominal wall reconstruction applications.

- By End User

On the basis of end user, the Surgical Meshes Market is segmented into Hospitals, Ambulatory Surgical Centers, Clinics, and Others. The Hospitals segment dominated the market with a 61.38% share in 2025 due to the high volume of hernia repair, abdominal wall reconstruction, and trauma surgeries performed in hospital settings. Hospitals possess advanced surgical infrastructure, specialized surgical teams, and access to a wide range of mesh products required for complex procedures. The increasing adoption of minimally invasive and robotic-assisted surgeries is further supporting mesh utilization in hospitals. Favorable reimbursement policies, comprehensive postoperative care capabilities, and growing patient preference for hospital-based surgical treatment contribute to the segment's dominance. In addition, hospitals serve as primary centers for emergency and high-risk surgeries that often require advanced mesh implantation procedures. Rising healthcare investments and expansion of tertiary care facilities worldwide continue to strengthen the market position of this segment.

The Ambulatory Surgical Centers (ASCs) segment is expected to witness the fastest CAGR of 8.1% from 2026 to 2033, driven by increasing demand for cost-effective outpatient surgical procedures. Advances in minimally invasive surgery have enabled many hernia repair procedures to be safely performed in ambulatory settings. Shorter patient recovery times, reduced healthcare costs, and improved procedural efficiency are encouraging greater utilization of ASCs. Growing healthcare system focus on reducing hospital burden and improving operational efficiency is further accelerating adoption. In addition, favorable reimbursement trends and increasing investments in outpatient surgical infrastructure are expected to support significant growth during the forecast period.

- By Sales Channel

On the basis of sales channel, the Surgical Meshes Market is segmented into Direct Channel and Distribution Channel. The Distribution Channel segment dominated the market with a 54.67% share in 2025 owing to the extensive networks established by medical device distributors across developed and emerging markets. Distribution partners enable manufacturers to efficiently reach hospitals, ambulatory surgical centers, clinics, and healthcare providers across diverse geographic regions. Their ability to provide inventory management, logistics support, regulatory compliance assistance, and localized customer service enhances product accessibility. The growing number of surgical procedures worldwide has increased demand for efficient product distribution systems. In addition, distributor relationships with healthcare institutions help accelerate product adoption and improve market penetration. Manufacturers continue to leverage distributor expertise to expand into emerging markets while minimizing operational costs and infrastructure investments.

The Direct Channel segment is projected to register the fastest CAGR of 7.9% from 2026 to 2033, driven by increasing efforts from leading manufacturers to strengthen direct relationships with healthcare providers and large hospital networks. Direct sales models offer improved pricing control, stronger customer engagement, and enhanced technical support capabilities. Growing adoption of digital procurement platforms and strategic purchasing agreements is further facilitating direct sales expansion. In addition, direct channels enable manufacturers to better showcase innovative mesh technologies, provide specialized clinical training, and gather real-time customer feedback, supporting long-term market growth.

Surgical Meshes Market Regional Analysis

North America dominated the Surgical Meshes market and accounted for the largest revenue share of 38.46% in 2025, supported by a high volume of hernia repair procedures, advanced healthcare infrastructure, favorable reimbursement policies, and strong adoption of innovative mesh technologies. The region benefits from the presence of leading medical device manufacturers, extensive surgeon expertise, and widespread utilization of minimally invasive and robotic-assisted surgical procedures. Growing prevalence of obesity, hernias, and chronic wounds continues to drive procedural volumes across hospitals and ambulatory surgical centers. In addition, increasing adoption of biologic, composite, and absorbable mesh products, coupled with ongoing investments in healthcare innovation and surgical research, further strengthens North America's leadership position in the global market.

U.S. Surgical Meshes Market Insight

The U.S. Surgical Meshes market is witnessing strong growth due to the increasing incidence of hernias, rising obesity rates, and growing demand for advanced surgical treatment options. The country's well-established healthcare system, high surgical procedure volumes, and strong reimbursement framework support widespread adoption of premium mesh products. In addition, increasing utilization of robotic-assisted and laparoscopic hernia repair procedures is driving demand for lightweight and advanced mesh technologies. Continuous product innovation and strong clinical research activity further contribute to market expansion across the country.

Europe Surgical Meshes Market Insight

The Europe Surgical Meshes market remains a major contributor to global revenue, driven by advanced healthcare systems, increasing adoption of minimally invasive surgeries, and strong regulatory standards supporting patient safety. Growing elderly populations and rising prevalence of abdominal disorders requiring surgical intervention are contributing to market growth. Furthermore, increasing surgeon preference for biologic and absorbable mesh products, coupled with continuous advancements in biomaterials and surgical techniques, is supporting widespread adoption throughout the region.

U.K. Surgical Meshes Market Insight

The U.K. Surgical Meshes market is experiencing steady growth, supported by rising adoption of simulation technologies in professional driver training, automotive testing, and motorsport applications. Increasing investments in advanced simulator infrastructure and growing demand for cost-effective, risk-free training solutions are contributing to market growth. Furthermore, integration of AI, VR, and data analytics technologies is improving simulator performance and training efficiency, positioning the U.K. as a key innovation hub in the Surgical Meshes industry.

Germany Surgical Meshes Market Insight

The Germany Surgical Meshes market is expanding steadily due to the country's advanced healthcare infrastructure, high surgical volumes, and strong focus on medical innovation. Hospitals and specialized surgical centers are increasingly adopting next-generation mesh products to improve patient outcomes and reduce recurrence rates. Growing demand for laparoscopic and robotic-assisted surgeries, along with rising investments in healthcare technology and clinical research, continues to drive market growth in Germany.

Asia-Pacific Surgical Meshes Market Insight

The Asia-Pacific Surgical Meshes market is expected to witness the fastest growth at a CAGR of 8.1% from 2026 to 2033, driven by expanding healthcare infrastructure, increasing surgical procedure volumes, growing medical tourism, and rising healthcare expenditure across China, India, and Southeast Asian countries. Rising awareness regarding advanced surgical treatment options and improving access to healthcare services are accelerating market adoption. Furthermore, increasing investments in hospital infrastructure, growing availability of skilled surgeons, and expanding healthcare insurance coverage are supporting regional market expansion.

Japan Surgical Meshes Market Insight

The Japan Surgical Meshes market is witnessing consistent growth due to the country's aging population, increasing prevalence of hernias, and strong adoption of advanced surgical technologies. Hospitals are increasingly utilizing minimally invasive and robotic-assisted procedures, which is driving demand for high-performance surgical meshes. In addition, ongoing research in biomaterials and regenerative medicine is supporting the development and adoption of innovative mesh products throughout the country.

China Surgical Meshes Market Insight

The China Surgical Meshes market is growing rapidly, driven by expanding healthcare infrastructure, rising healthcare spending, and increasing numbers of surgical procedures performed annually. Growing awareness regarding modern hernia repair techniques and increasing adoption of advanced mesh technologies are significantly boosting market demand. In addition, government initiatives aimed at improving healthcare accessibility, combined with rising investments in medical device manufacturing and hospital modernization, are positioning China as one of the fastest-growing markets for surgical meshes globally.

Surgical Meshes Market Share

The Surgical Meshes industry is primarily led by well-established companies, including:

- • Becton, Dickinson and Company (BD) (U.S.)

- Johnson & Johnson (Ethicon) (U.S.)

- Medtronic plc (Ireland)

- B. Braun SE (Germany)

- W. L. Gore & Associates, Inc. (U.S.)

- Getinge AB (Sweden)

- Baxter International Inc. (U.S.)

- Cook Medical LLC (U.S.)

- Integra LifeSciences Holdings Corporation (U.S.)

- TELA Bio, Inc. (U.S.)

- Atrium Medical Corporation (U.S.)

- LifeCell Corporation (an AbbVie company) (U.S.)

- RTI Surgical Holdings, Inc. (U.S.)

- Groupe Cousin Biotech (France)

- FEG Textiltechnik mbH (Germany)

- Proxy Biomedical Ltd. (Ireland)

- THT Bio-Science Group (Netherlands)

- Meril Life Sciences Pvt. Ltd. (India)

- Healthium Medtech Limited (India)

- Lotus Surgicals Pvt. Ltd. (India)

- Sutures India Pvt. Ltd. (India)

- Futura Surgicare Pvt. Ltd. (India)

- Mesh Suture Inc. (U.S.)

- BioCer Entwicklungs-GmbH (Germany)

- Dipromed S.r.l. (Italy)

- Assut Europe S.p.A. (Italy)

- PFM Medical AG (Germany)

- Aroa Biosurgery Limited (New Zealand)

- Gunze Limited (Japan)

- Samyang Biopharmaceuticals Corporation (South Korea)

- Riverpoint Medical LLC (U.S.)

- Deep Blue Medical Advances, Inc. (U.S.)

- Tissium SA (France)

- Poly-Med, Inc. (U.S.)

Latest Developments in Surgical Meshes Market

- In April 2025, Becton, Dickinson and Company (BD) announced the commercial launch of the Phasix ST Umbilical Hernia Patch following U.S. FDA 510(k) clearance. The product is the first fully absorbable hernia patch specifically designed for umbilical hernia repair and utilizes BD's bioresorbable P4HB (Poly-4-hydroxybutyrate) technology. The launch expands the company's hernia repair portfolio and addresses growing demand for absorbable mesh solutions that support tissue remodeling while reducing the long-term presence of synthetic implants

- In March 2025, TELA Bio announced the U.S. commercial launch of larger-size OviTex® PRS Reinforced Tissue Matrix products for plastic and reconstructive surgery applications. The expanded portfolio includes new 25 x 30 cm oval and 25 cm circular configurations, providing surgeons with larger coverage options for complex soft-tissue reconstruction procedures. The development strengthens TELA Bio's position in the growing biologic and reinforced tissue matrix segment of the surgical meshes market

- In June 2025, TELA Bio announced the European commercial launch of OviTex Inguinal Reinforced Tissue Matrix for robotic and laparoscopic inguinal hernia repair. The product is specifically engineered for minimally invasive inguinal hernia procedures and follows its successful U.S. launch in 2024. The expansion reflects increasing demand for advanced tissue-based alternatives to traditional synthetic meshes in hernia repair surgery

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.