Global Surgical Pliers Market

Market Size in USD Million

CAGR :

%

USD

759.58 Million

USD

1,064.58 Million

2025

2033

USD

759.58 Million

USD

1,064.58 Million

2025

2033

| 2026 –2033 | |

| USD 759.58 Million | |

| USD 1,064.58 Million | |

| % | |

|

Surgical Pliers Market Size

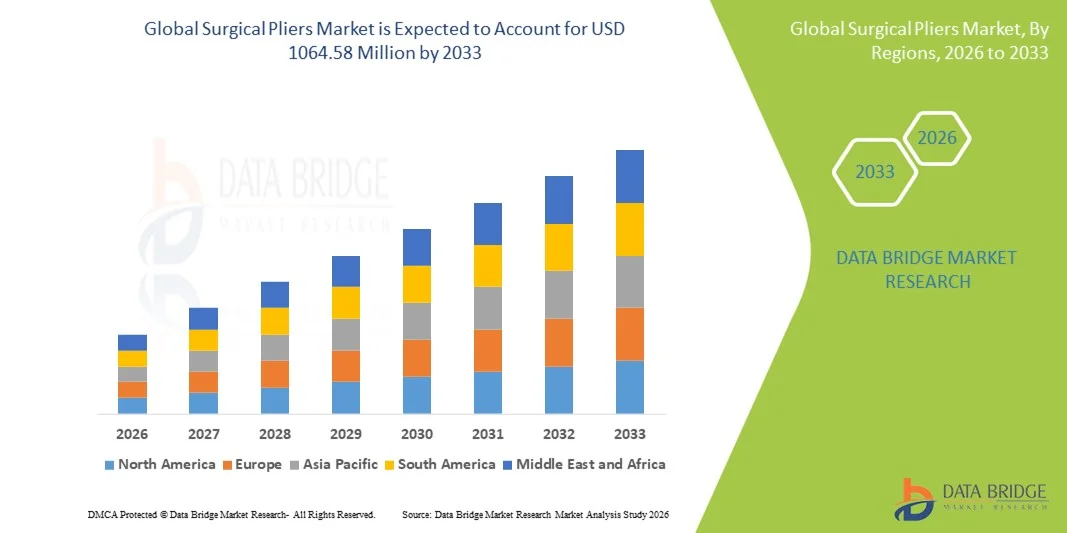

- The global surgical pliers market size was valued at USD 759.58 Million in 2025 and is expected to reach USD 1064.58 Million by 2033, at a CAGR of 4.31% during the forecast period

- The market growth is largely fueled by the increasing number of surgical procedures globally, along with the rising demand for advanced surgical instruments that provide precision and safety during operations

- Furthermore, growing healthcare infrastructure development and rising healthcare spending in emerging economies are driving the adoption of surgical pliers across hospitals and ambulatory surgical centers. These factors are accelerating the uptake of Surgical Pliers, thereby significantly boosting the industry's growth

Surgical Pliers Market Analysis

- Surgical pliers are precision instruments used across various surgical procedures for gripping, bending, cutting, and manipulating tissues or materials such as wires, sutures, and implants

- The demand for surgical pliers is rising due to increasing surgical procedures globally, especially in orthopedics, cardiovascular, and general surgery, where reliable and durable instruments are essential for better clinical outcomes

- The growing adoption of minimally invasive surgeries and advancements in surgical techniques are further driving the need for high-quality, ergonomically designed pliers that offer precision and control

- North America dominated the surgical pliers market with the largest revenue share of 39.8% in 2025, supported by advanced healthcare infrastructure, high surgical volumes, and strong presence of leading medical device manufacturers

- Asia Pacifica is expected to be the fastest-growing region in the surgical pliers market during the forecast period, registering a CAGR of 18.6%, driven by rising healthcare expenditure, increasing surgical procedures, expanding hospital infrastructure, and growing medical tourism across countries such as China, India, Japan, and South Korea

- The metal segment dominated the market with a revenue share of 78.6% in 2025, due to its high strength, durability, and repeated sterilization capability

Report Scope and Surgical Pliers Market Segmentation

|

Attributes |

Surgical Pliers Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Surgical Pliers Market Trends

Enhanced Convenience Through Automation & Digital Workflow Integration

- A major and growing trend in the global surgical pliers market is the shift toward automated surgical workflows and digital integration within operating rooms. This includes increased adoption of digitally-enabled surgical instrument management systems, which streamline inventory tracking, sterilization cycles, and procedural usage

- For instance, major hospitals and surgical centers are increasingly implementing RFID-based instrument tracking systems and digital sterilization monitoring, allowing surgical teams to reduce instrument loss, improve inventory control, and ensure sterilization compliance

- The growing focus on minimally invasive and precision surgeries is pushing manufacturers to develop surgical pliers that are compatible with robot-assisted surgery, laparoscopic procedures, and advanced endoscopic operations. These instruments are being designed for enhanced ergonomics, higher precision, and reduced fatigue for surgeons during long procedures

- In addition, there is an increasing trend toward specialized surgical pliers designed for specific surgical disciplines such as orthopedics, cardiovascular, neurosurgery, and dental surgery, which is driven by rising demand for procedure-specific tools that provide better handling and improved outcomes

- This trend is further supported by the healthcare industry’s increasing investment in smart operating rooms and digital surgery platforms, which require surgical tools to be more adaptable, standardized, and integrated into modern surgical workflows

- Overall, the trend toward digital and automated surgical workflows is redefining expectations for surgical instruments, driving companies to innovate faster in terms of instrument design, material quality, and procedure-specific functionality

Surgical Pliers Market Dynamics

Driver

Rising Surgical Procedures and Demand for Precision Tools

- The growing global demand for surgical procedures, particularly in orthopedics, cardiovascular surgery, and minimally invasive procedures, is driving the need for high-quality surgical pliers

- For instance, increasing rates of chronic diseases and trauma cases worldwide are boosting surgical interventions, thereby increasing the need for advanced surgical tools such as precision pliers

- The expanding number of hospital beds and surgical centers in developing countries is also fueling demand, as healthcare infrastructure grows and access to surgical care improves

- Moreover, the adoption of minimally invasive surgery (MIS) is accelerating globally, increasing the demand for specialized pliers designed for laparoscopic and endoscopic applications

- As hospitals and clinics aim to improve surgical efficiency and reduce procedure time, surgical pliers that offer better grip, durability, and control are becoming increasingly preferred

- The growing focus on patient safety and surgical outcomes is prompting hospitals to invest in high-quality surgical instruments, thereby supporting market growth

Restraint/Challenge

High Cost of Advanced Instruments and Stringent Regulatory Compliance

- The high cost of advanced surgical pliers, especially those made from premium materials like titanium or specialized alloys, can be a major restraint for adoption in price-sensitive markets

- For instance, advanced pliers designed for minimally invasive or robotic-assisted surgeries are often priced significantly higher than standard surgical instruments, limiting their adoption in smaller clinics and developing regions

- Another key challenge is the stringent regulatory requirements for surgical instruments across regions such as the US FDA, EU MDR, and other regulatory bodies, which can delay product approvals and increase development costs

- In addition, surgical pliers require strict sterilization and infection control protocols, which increase operational costs and limit usage in low-resource settings

- The need for continuous instrument maintenance and replacement also adds to the overall cost of ownership, making hospitals cautious about large-scale adoption

- Addressing these challenges through cost-effective manufacturing, improved material innovation, and simplified compliance pathways will be essential for sustained market growth

Surgical Pliers Market Scope

The market is segmented on the basis of application, material, modality, design, utility, and end use.

- By Application

On the basis of application, the Surgical Pliers market is segmented into clamping and occluding, dissecting, retracting, and holding. The clamping and occluding segment dominated the market with the largest revenue share of 42.5% in 2025, due to its critical role in controlling bleeding and securing tissues during surgery. These pliers are essential in general surgery, cardiovascular procedures, and trauma care, driving high demand. Hospitals prefer clamping pliers because they provide precise control and are compatible with sterilization processes. The segment’s dominance is further strengthened by rising surgical volumes worldwide. Increasing focus on patient safety and reduced surgical complications also supports market leadership. The availability of advanced designs such as locking and ratchet clamping pliers boosts adoption. Growing healthcare infrastructure in emerging markets further contributes to the segment’s growth. Overall, clamping and occluding instruments remain indispensable in most surgical procedures, ensuring steady demand and high revenue share.

The retracting segment is expected to witness the fastest CAGR of 22.4% from 2026 to 2033, driven by increasing complex surgical procedures and the need for better visibility during operations. Retracting pliers are used extensively in orthopaedic, neurosurgical, and ENT procedures where deep tissue access is required. Rising adoption of minimally invasive surgeries increases the need for specialized retractors. Technological improvements like ergonomic handles and lightweight materials make retracting instruments more efficient and preferred. Growing demand from hospitals and ambulatory surgical centers also boosts the segment. As surgical procedures become more complex, the need for reliable retraction tools grows, fueling rapid CAGR. Emerging economies are investing heavily in modern operating theatres, further supporting demand. Overall, retracting pliers are expected to expand rapidly due to clinical necessity and innovation.

- By Material

On the basis of material, the Surgical Pliers market is segmented into metal and plastic. The metal segment dominated the market with a revenue share of 78.6% in 2025, due to its high strength, durability, and repeated sterilization capability. Stainless steel is the preferred material because it resists corrosion and meets medical safety standards. Metal pliers are widely used in hospitals due to their long life span and high precision in critical procedures. Hospitals and surgical centers favor metal pliers for their ability to withstand repeated autoclaving and harsh sterilization. The segment benefits from strong demand in developed regions with high surgical volumes. Continuous innovation in metal alloys and coatings also supports market dominance. Metal pliers remain essential in most surgeries, ensuring steady demand and high market share.

The plastic segment is expected to register the fastest CAGR of 19.3% from 2026 to 2033, driven by rising demand for disposable instruments to prevent infection and reduce sterilization costs. Plastic pliers are increasingly used in outpatient centers and minor surgical procedures. These instruments are cost-effective and suitable for single-use, reducing contamination risks. Rising awareness of infection control and stringent hygiene norms support growth. The segment benefits from increasing demand in emerging markets with limited sterilization facilities. As healthcare providers focus on patient safety, disposable plastic pliers become more popular. The segment is also supported by growing use in dental and minor surgeries. Overall, plastic pliers are expected to grow rapidly due to convenience and safety.

- By Modality

On the basis of modality, the Surgical Pliers market is segmented into general, dental, ENT, obstetrics & gynaecology, neurosurgical, and orthopaedic. The general surgery segment dominated with 33.8% market share in 2025, due to the high number of general surgical procedures performed globally. General surgery requires a wide variety of pliers for tissue handling, clamping, and dissection, driving strong demand. Hospitals and surgical centers maintain large inventories of general surgical pliers. Increasing healthcare expenditure and rising surgical volumes in emerging economies further strengthen the segment. General surgery remains the largest user of surgical instruments due to the wide range of procedures. Continuous advancements in surgical techniques also contribute to high adoption. Overall, general surgery remains the dominant modality segment due to consistent clinical demand.

The orthopaedic segment is expected to witness the fastest CAGR of 20.1% from 2026 to 2033, driven by rising orthopaedic surgeries, ageing population, and increasing trauma cases worldwide. Orthopaedic procedures require specialized pliers for bone fixation, soft tissue handling, and implant placement. Increasing incidence of fractures and joint disorders fuels demand. Growing medical tourism for orthopaedic care also supports the segment. New product innovations and improved surgical techniques further accelerate growth. As the global population ages, orthopaedic surgeries are expected to rise, increasing demand for specialised pliers. Overall, orthopaedic is the fastest-growing modality due to rising clinical needs and technological advancements.

- By Design

On the basis of design, the Surgical Pliers market is segmented into straight, curved, and angled. The straight design segment dominated with 46.2% market share in 2025, as straight pliers are widely used for general surgical tasks and offer easier handling. Straight pliers are preferred for their versatility and strong performance in basic surgical procedures. Hospitals and surgical centers rely on straight instruments for routine operations. The design is suitable for clamping, gripping, and cutting, making it highly practical. Straight pliers are also cost-effective and available in multiple sizes, supporting high adoption. The segment benefits from strong demand across general surgery, dental, and ENT. Overall, straight design remains dominant due to its versatility and widespread clinical use.

The angled design segment is expected to register the fastest CAGR of 18.7% from 2026 to 2033, driven by increasing complex surgeries requiring precise access in deep anatomical areas. Angled pliers provide better visibility and access in confined spaces, especially in neurosurgery and orthopaedic procedures. Surgeons prefer angled instruments for improved precision and reduced tissue damage. Innovation in ergonomic designs also supports growth. As surgical techniques become more advanced, angled pliers become essential for complex operations. The segment is expected to grow rapidly due to increasing demand for precision instruments.

- By Utility

On the basis of utility, the Surgical Pliers market is segmented into disposable and reusable. The reusable segment dominated with 61.4% market share in 2025, driven by cost efficiency and long-term use in hospitals. Reusable pliers are preferred for high-value surgical procedures due to durability and long-term savings. Hospitals invest in reusable instruments to reduce overall costs and maintain a consistent supply for routine surgeries. These instruments can withstand repeated sterilization cycles, maintaining performance and reliability. The segment benefits from strong demand in developed countries with established sterilization infrastructure. Advanced material coatings and corrosion-resistant stainless steel enhance longevity. Reusable pliers are also preferred for complex surgeries requiring high precision. Long-term procurement contracts by hospitals further support this dominance. The market leadership is reinforced by high surgical volumes in hospitals worldwide.

The disposable segment is expected to witness the fastest CAGR of 23.0% from 2026 to 2033, driven by infection control and rising demand in ambulatory surgical centers. Disposable pliers reduce cross-contamination risk and eliminate sterilization costs, making them ideal for outpatient procedures. Rising outpatient surgeries and minor procedures increase demand. The segment is growing rapidly in emerging markets where sterilization facilities are limited. Manufacturers are introducing cost-effective disposable models with improved grip and performance. Increasing awareness about hospital-acquired infections boosts adoption. Disposable pliers are also preferred in emergency surgeries for quick availability. The growing trend of single-use medical devices supports rapid CAGR.

- By End Use

On the basis of end use, the Surgical Pliers market is segmented into hospitals and ambulatory surgical centres. The hospital segment dominated with 82.5% market share in 2025, owing to the high number of surgical procedures and established healthcare infrastructure. Hospitals are the largest consumers due to their large surgical volumes and advanced operating rooms. They require a wide range of pliers for general and specialized surgeries, driving consistent demand. Hospitals also maintain large inventories and long-term contracts with instrument suppliers. Rising healthcare expenditure and expansion of hospital facilities further support dominance. Advanced surgical procedures and high patient footfall in hospitals ensure continuous demand. Hospitals prefer reusable instruments due to cost efficiency.

The ambulatory surgical centres segment is expected to witness the fastest CAGR of 17.8% from 2026 to 2033, driven by increasing outpatient surgeries and cost-effective healthcare delivery. ASCs are expanding due to patient preference for shorter hospital stays and lower costs. ASCs often prefer disposable pliers for infection control and convenience. The growing trend of minimally invasive procedures supports this segment. Rising medical tourism and outpatient diagnostic services also increase demand. ASCs in emerging economies are investing in modern surgical equipment. The segment’s rapid growth is driven by increasing healthcare accessibility and efficiency.

Surgical Pliers Market Regional Analysis

- North America dominated the surgical pliers market with the largest revenue share of 39.8% in 2025. This dominance is supported by advanced healthcare infrastructure, high surgical volumes, and the strong presence of leading medical device manufacturers

- The region has a well-established healthcare system that consistently invests in modern surgical equipment, increasing the demand for precision surgical instruments such as surgical pliers. Continuous innovation and frequent upgrades in surgical tools, driven by high research and development activity, further strengthen North America’s market leadership

- In addition, the growing preference for minimally invasive surgeries and specialized procedures is driving increased usage of advanced surgical pliers. The high adoption rate of premium quality instruments among hospitals and surgical centers ensures steady market growth in the region

U.S. Surgical Pliers Market Insight

The U.S. surgical pliers market captured the largest revenue share within North America, due to high surgical procedure volumes and continuous hospital modernization. The country’s healthcare sector is highly advanced, with a strong focus on adopting innovative surgical tools and technology. Hospitals and ambulatory surgical centers invest heavily in high-quality instruments to support various specialties including orthopedic, neurosurgery, and cardiovascular surgeries. The growing demand for minimally invasive procedures, combined with rising healthcare spending, further supports market expansion. The presence of major medical device manufacturers and strong regulatory support for advanced surgical equipment also contributes to the U.S. market dominance.

Europe Surgical Pliers Market Insight

The Europe surgical pliers market is projected to expand at a substantial CAGR during the forecast period, driven by increasing surgical procedures, rising healthcare expenditure, and technological advancements. European countries are investing heavily in modernizing healthcare infrastructure and upgrading operating rooms with advanced surgical tools. Increasing prevalence of chronic diseases and aging population further supports growth in surgical interventions, boosting demand for surgical pliers. The region also emphasizes product quality, sterilization standards, and safety, leading hospitals to prefer high-quality surgical instruments. Continued focus on healthcare innovation and adoption of advanced surgical techniques will sustain market growth across Europe.

U.K. Surgical Pliers Market Insight

The U.K. surgical pliers market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by increasing surgical procedures, rising healthcare investments, and strong adoption of advanced surgical equipment. The National Health Service (NHS) continues to upgrade surgical infrastructure and improve operational efficiency, increasing demand for reliable surgical instruments. In addition, the growing number of outpatient and ambulatory surgeries supports adoption of both reusable and disposable surgical pliers. The U.K. also benefits from strong medical research and development, supporting new product launches and innovation in surgical tools.

Germany Surgical Pliers Market Insight

The Germany surgical pliers market is expected to expand at a considerable CAGR during the forecast period, fueled by increasing healthcare expenditure, advanced medical infrastructure, and strong emphasis on medical technology innovation. Germany is known for its high standards in medical device manufacturing and stringent quality regulations, encouraging hospitals to adopt premium surgical instruments. The rising number of surgeries and expansion of hospital capacity further supports demand. Moreover, Germany’s focus on sustainability and long-term cost efficiency encourages the adoption of reusable surgical pliers, which are widely preferred in established healthcare settings.

Asia-Pacific Surgical Pliers Market Insight

The Asia-Pacific surgical pliers market is expected to grow at the fastest CAGR of 18.6% during the forecast period, driven by rising healthcare expenditure, increasing surgical procedures, expanding hospital infrastructure, and growing medical tourism. Countries such as China, India, Japan, and South Korea are investing heavily in healthcare modernization and adopting advanced surgical equipment. Rapid urbanization and increasing access to quality healthcare also boost demand for surgical instruments. The growing number of hospitals and ambulatory surgical centers, along with rising awareness about advanced surgical treatments, supports strong market growth in the region.

Japan Surgical Pliers Market Insight

The Japan surgical pliers market is gaining momentum due to rising healthcare spending, advanced medical infrastructure, and high demand for precision surgical instruments. Japan’s aging population and increasing number of surgeries contribute to growing demand for surgical pliers across multiple specialties. The country’s strong emphasis on medical technology innovation and high standards for quality and safety further supports market growth. In addition, Japan’s strong presence of medical device manufacturers and continuous product development encourage adoption of advanced surgical tools in hospitals and surgical centers.

China Surgical Pliers Market Insight

The China surgical pliers market is expanding rapidly due to rising healthcare expenditure, increasing number of surgeries, and growing hospital infrastructure. China is witnessing strong growth in medical tourism and adoption of advanced surgical technologies, which is driving demand for high-quality surgical instruments. Increasing investment in healthcare modernization and rising access to advanced surgical procedures across urban and semi-urban areas further supports the market. Domestic manufacturing capabilities and cost-effective product availability also contribute to growth, making China a major market within the Asia-Pacific region.

Surgical Pliers Market Share

The Surgical Pliers industry is primarily led by well-established companies, including:

• B. Braun S.E. (Germany)

• Medtronic (Ireland)

• Stryker (U.S.)

• Johnson & Johnson (U.S.)

• Smith & Nephew (U.K.)

• Becton, Dickinson and Company (U.S.)

• KARL STORZ (Germany)

• Zimmer Biomet Holdings, Inc. (U.S.)

• Integra LifeSciences (U.S.)

• ConMed Corporation (U.S.)

• Rheinmetall (Germany)

• Aesculap (Germany)

• Surgical Holdings Ltd. (U.K.)

• Teleflex Incorporated (U.S.)

• LivaNova PLC (U.K.)

• Aesculap AG (Germany)

• Lohmann & Rauscher (Germany)

• Medline Industries (U.S.)

Latest Developments in Global Surgical Pliers Market

- In June 2023, SURE Retractors Inc. introduced a new line of single-use sterile retractors and associated surgical tools designed for trauma, orthopedic, and spinal surgeries, improving procedural efficiency and reducing infection risk—reflecting broader instrument innovation trends that also benefit surgical pliers design and adoption in operating rooms worldwide

- In October 2023, Channellock, Inc. launched its SpeedGrip V-Jaw Tongue & Groove Pliers, engineered for enhanced grip strength and ergonomic control, signaling ongoing advances in surgical instrument design focused on precision and operator comfort

- In February 2025, industry reports highlighted rising incorporation of sensor-embedded surgical instruments—including pliers with advanced tip stabilization and ergonomic enhancements—driven by increased demand for precision instruments in robotic and minimally invasive surgeries

- In March 2025, surgical instrument market analysts noted a sharp increase in patent filings for next-generation minimally invasive surgical tools, including pliers with improved curved tips and locking mechanisms, reflecting manufacturers’ focus on innovation for improved surgical outcomes and workflow efficiency

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.