Global Taxane Market

Market Size in USD Billion

CAGR :

%

USD

5.50 Billion

USD

8.31 Billion

2025

2033

USD

5.50 Billion

USD

8.31 Billion

2025

2033

| 2026 - 2033 | |

| USD 5.50 Billion | |

| USD 8.31 Billion | |

| % | |

|

Taxane Market Overview

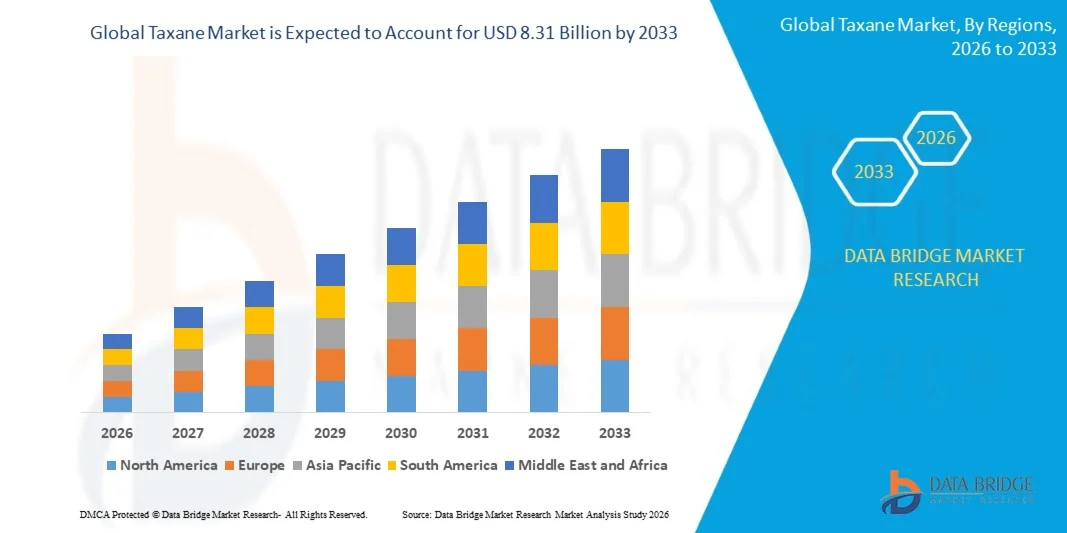

The Taxane Market was valued at USD 5.50 billion in 2025 and is projected to reach USD 8.31 billion by 2033, growing at a CAGR of 5.30% from 2026 to 2033. The Taxane Market is experiencing steady growth driven by the rising incidence of cancer worldwide and the increasing adoption of chemotherapy-based treatment regimens across both developed and emerging healthcare systems. Taxanes, including paclitaxel, docetaxel, and cabazitaxel, are widely used in the treatment of breast cancer, lung cancer, ovarian cancer, prostate cancer, and other solid tumors due to their effectiveness in inhibiting cancer cell division. The growing global cancer burden, particularly among aging populations, is significantly contributing to higher demand for taxane-based therapies.

In addition, advancements in oncology drug development, including nanoparticle albumin-bound formulations (such as nab-paclitaxel), are improving drug efficacy and reducing side effects, further supporting market adoption. Increasing investment in cancer research, expansion of healthcare infrastructure, and improved access to oncology treatments in emerging economies are also accelerating market growth. However, the market continues to face challenges such as high treatment costs, side effects associated with chemotherapy (including neuropathy and myelosuppression), and the development of drug resistance in certain patients. Despite these challenges, ongoing clinical trials, combination therapies, and the introduction of generic versions of taxanes are expected to expand treatment accessibility and support sustained market growth globally.

Key Market Trends & Insights

- North America dominated the Taxane Market with the largest revenue share of 38.62% in 2025, supported by high cancer prevalence, strong presence of advanced oncology treatment centers, extensive adoption of chemotherapy regimens, and well-established healthcare reimbursement systems. The region also benefits from robust clinical research activities, early adoption of novel drug formulations such as nanoparticle and liposomal taxanes, and strong presence of key pharmaceutical companies driving innovation in oncology therapeutics.

- The Paclitaxel segment led the market with a 44.37% share in 2025, driven by its widespread use as a first-line chemotherapy agent for breast cancer, ovarian cancer, and non-small cell lung cancer. Its proven clinical efficacy, broad indication profile, and availability in both branded and generic formulations continue to support strong demand across global healthcare systems.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 8.4% from 2026 to 2033, fueled by rising cancer burden, expanding access to oncology treatments, improving healthcare infrastructure, and increasing government investments in cancer care programs across China, India, and Japan. Growing availability of generic taxanes and expanding hospital networks are further accelerating regional market growth.

- The Docetaxel segment is expected to witness the fastest growth at a CAGR of 7.9%, driven by increasing adoption in prostate cancer and lung cancer treatment protocols, rising use in combination therapies, and growing availability of cost-effective generic formulations in emerging markets.

- The Branded drug segment accounts for a significant share of 56.21% in 2025, supported by strong physician preference for original formulations, higher clinical trust, and continued use of patented and premium oncology drugs in developed markets, despite growing penetration of generics.

- The Nanoparticle formulation segment is expected to register the fastest CAGR of 8.1%, driven by increasing adoption of nab-paclitaxel and other nano-based delivery systems that improve drug solubility, reduce toxicity, and enhance targeted drug delivery in cancer treatment.

- The Breast Cancer application segment dominated the market with a 39.56% revenue share in 2025, due to high global incidence rates and strong reliance on taxane-based chemotherapy as a standard treatment option in both early-stage and metastatic breast cancer cases.

- The Prostate Cancer segment is expected to witness the fastest CAGR of 7.6%, supported by increasing global incidence, expanding use of docetaxel-based therapies in metastatic cases, and growing adoption of combination treatment approaches in advanced oncology care.

- Hospitals dominated the end-user segment with a 61.18% share in 2025, driven by high patient inflow, availability of advanced oncology departments, and centralized chemotherapy administration facilities.

- Ambulatory Surgical Centers are expected to witness the fastest CAGR of 7.3%, supported by rising shift toward outpatient chemotherapy administration, cost-efficiency benefits, and increasing adoption of decentralized cancer care models.

- Direct Tender distribution channel dominated the market with a 66.42% share in 2025, due to bulk procurement by government hospitals, oncology centers, and large healthcare networks ensuring cost efficiency and steady drug supply.

- Retail sales channel is expected to grow steadily at a CAGR of 7.1%, driven by increasing availability of oncology drugs through specialty pharmacies and expanding access in emerging healthcare markets.

- The Generics segment dominated the market with a 61.38% share in 2025 due to its affordability, widespread availability, and strong penetration across global healthcare systems

Market Size & Forecast

- Global Market Value (2025): USD 5.50 Billion

- Expected Market Value (2033): USD 8.31 Billion

- Forecast CAGR (2026–2033): 5.30%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Taxane Market Segmentation

|

Attributes |

Taxane Key Market Insights |

|

Segments Covered |

· By Type: Paclitaxel, Docetaxel, and Cabazitaxel · By Drug Type: Generics and Branded · By Formulation: Liposomes, Nanoparticles, Polymeric Micelles, and Others · By Age Group: Adults and Geriatric · By Application: Breast Cancer, Non-Small Cell Lung Cancer, Pancreatic Cancer, Ovarian Cancer, Prostate Cancer, and Others · By End User: Hospitals, Ambulatory Surgical Centers, Specialty Clinics, and Others · By Distribution Channel: Retail Sales and Direct Tender |

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

• Pfizer Inc. (U.S.) |

|

Market Opportunities |

· Expansion of nanoparticle and advanced drug delivery formulations · Rising demand for generics in emerging healthcare markets · Growing adoption of combination therapies and personalized oncology treatment |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Taxane Market Trends

Trend: Expansion of Taxane-Based Combination Therapy and Advanced Oncology Treatment Regimens

The Taxane Market is witnessing a strong trend toward the increasing use of taxane-based combination therapies with immunotherapy, targeted therapy, and hormonal therapy to improve overall cancer treatment outcomes. Taxanes such as paclitaxel and docetaxel are being widely integrated into multi-drug regimens for breast cancer, non-small cell lung cancer, ovarian cancer, and prostate cancer. Clinical studies published across major oncology journals have shown that combining paclitaxel with immune checkpoint inhibitors (such as pembrolizumab) improves progression-free survival in certain solid tumors. Pharmaceutical companies are also investing in next-generation formulations like nanoparticle albumin-bound paclitaxel (nab-paclitaxel) to enhance tumor penetration and reduce systemic toxicity. The increasing shift toward personalized oncology treatment and biomarker-driven therapy selection is further strengthening this trend globally.

Taxane Market Dynamics

Key Market Driver: Rising Global Cancer Burden and Expanding Chemotherapy Adoption

The rapid rise in global cancer incidence is one of the strongest drivers of the Taxane market. According to the World Health Organization (WHO), cancer cases are projected to exceed 29 million annually by 2040, with breast, lung, and colorectal cancers being the most prevalent. Taxanes remain a cornerstone of chemotherapy protocols due to their proven efficacy in inhibiting cancer cell mitosis by stabilizing microtubules.

Paclitaxel and docetaxel are widely used as first-line or second-line treatments in multiple oncology indications, particularly in breast cancer where taxane-based regimens are included in over 70% of standard chemotherapy protocols in many developed healthcare systems. Increasing investments in oncology infrastructure, expansion of cancer treatment centers in emerging economies such as India and China, and improved access to affordable generic chemotherapy drugs are further accelerating market demand. In addition, rising adoption of biosimilar and generic taxane formulations is expanding treatment accessibility in cost-sensitive regions.

Key Restraint/Challenge: Severe Side Effects, Drug Resistance, and High Treatment Costs

A major challenge in the Taxane Market is the occurrence of significant chemotherapy-associated side effects, including peripheral neuropathy, myelosuppression, alopecia, and gastrointestinal toxicity, which can limit long-term patient compliance. In addition, tumor resistance to taxane-based therapies is increasingly being observed in advanced and metastatic cancer cases, reducing treatment effectiveness over time.

Another key limitation is the high cost of branded oncology drugs and advanced formulations such as nanoparticle and liposomal taxanes, which restricts accessibility in low- and middle-income countries. Even though generics have improved affordability, the overall cost burden of chemotherapy—including hospital administration, supportive care, and long treatment cycles—remains substantial. For example, taxane-based chemotherapy regimens can cost several thousand USD per treatment cycle in developed markets, placing financial strain on patients without adequate insurance coverage.

Key Market Opportunity: Advancements in Targeted Drug Delivery and Next-Generation Oncology Innovations

The integration of advanced drug delivery technologies and precision oncology approaches presents a significant opportunity in the Taxane market. Innovations such as nanoparticle albumin-bound formulations (nab-paclitaxel), liposomal encapsulation, and polymeric micelle systems are improving drug bioavailability, reducing toxicity, and enhancing tumor-specific targeting.

In addition, ongoing clinical trials exploring taxanes in combination with immunotherapy agents and PARP inhibitors are expanding their therapeutic applications across multiple cancer types. Pharmaceutical companies are increasingly investing in R&D pipelines focused on reducing chemotherapy resistance and improving patient outcomes. The global shift toward personalized medicine—supported by genomic profiling and biomarker-based treatment selection—is further enabling more effective use of taxanes in targeted patient populations. Expanding healthcare infrastructure in Asia-Pacific and Latin America, along with increasing oncology drug approvals by regulatory agencies such as the FDA and EMA, is expected to create substantial growth opportunities for both branded and generic taxane manufacturers over the forecast period.

Taxane Market Scope

The Taxane market is segmented on the basis of type, drug type, formulation, age group, application, end user, and distribution channel.

- By Type

On the basis of type, the Taxane Market is segmented into Paclitaxel, Docetaxel, and Cabazitaxel. The Paclitaxel segment dominated the market with a 46.21% share in 2025, owing to its extensive use as a first-line chemotherapy drug across multiple cancer indications including breast, ovarian, and non-small cell lung cancer. Its strong clinical acceptance and inclusion in global treatment guidelines significantly enhance its adoption across hospitals and oncology centers. The drug’s wide availability in both branded and generic forms further strengthens its market penetration. Established manufacturing capabilities and global supply chains ensure consistent availability. High patient volume and repeated usage in combination therapies support sustained demand. Its cost-effectiveness compared to newer oncology drugs reinforces preference among healthcare providers. Strong reimbursement support in developed and emerging economies drives adoption. Continuous clinical validation across multiple cancer types further strengthens its dominance. Hospitals and cancer treatment centers rely heavily on Paclitaxel-based regimens. Its versatility across oncology applications ensures long-term market stability.

The Cabazitaxel segment is expected to witness the fastest growth at a CAGR of 7.4% from 2026 to 2033, driven by increasing adoption in treatment-resistant metastatic prostate cancer cases. Its ability to overcome resistance to earlier-generation Taxanes enhances its clinical importance. Rising prevalence of advanced-stage prostate cancer globally is a major growth driver. Expanding use in second-line and third-line therapy settings is further accelerating demand. Ongoing clinical trials exploring additional oncology indications are supporting future expansion. Improved survival outcomes compared to older chemotherapy options increase physician preference. Growing adoption in developed healthcare systems strengthens market penetration. Increasing focus on precision oncology and personalized treatment supports usage. Pharmaceutical companies are investing in advanced formulations to improve efficacy. Strong pipeline development activity is expected to further boost adoption. Overall, Cabazitaxel is emerging as a high-value oncology therapeutic segment.

- By Drug Type

On the basis of drug type, the market is segmented into Generics and Branded drugs. The Generics segment dominated the market with a 61.38% share in 2025 due to its affordability, widespread availability, and strong penetration across global healthcare systems. Patent expirations of major Taxane drugs have enabled large-scale generic production, significantly reducing treatment costs. Hospitals and government healthcare programs strongly prefer generics to manage oncology treatment budgets efficiently. High accessibility in developing regions further supports dominance. Large manufacturing capacity and competitive pricing increase market reach. Generics are widely used in public healthcare systems and cancer treatment centers. Clinical equivalence to branded drugs ensures physician confidence in treatment outcomes. Strong distribution networks enhance availability across pharmacies and hospitals. Increasing cancer burden globally supports sustained demand for generics. Overall, cost-effectiveness remains the key factor driving dominance.

The Branded segment is expected to witness the fastest growth at a CAGR of 6.9% from 2026 to 2033, driven by rising demand for advanced drug formulations and improved delivery systems. Branded Taxanes often incorporate innovations such as nanoparticle-based and liposomal delivery technologies. These advancements enhance drug efficacy and reduce toxicity. Increasing investment in oncology research and development is accelerating product innovation. Physicians prefer branded drugs for complex and resistant cancer cases. Strong clinical validation and regulatory approvals further support adoption. Premium pricing contributes to higher revenue growth. Expanding availability of next-generation formulations strengthens market presence. Growing focus on precision oncology is boosting demand. Pharmaceutical companies are actively developing differentiated oncology products. Overall, branded drugs are emerging as a key innovation-driven segment.

- By Formulation

On the basis of formulation, the market is segmented into Liposomes, Nanoparticles, Polymeric Micelles, and Others. The Nanoparticles segment dominated the market with a 39.84% share in 2025 due to its superior drug delivery efficiency and enhanced tumor targeting capability. Nanoparticle-based Taxanes improve solubility and bioavailability, increasing therapeutic effectiveness. Reduced systemic toxicity compared to conventional formulations further strengthens adoption. Strong use in advanced oncology treatments supports segment leadership. Pharmaceutical companies are heavily investing in nanotechnology-based drug delivery systems. Hospitals prefer nanoparticle formulations for better patient outcomes. Controlled release mechanisms enhance treatment precision. Increasing regulatory approvals support commercialization. Strong research pipeline activity in nanomedicine reinforces dominance. Growing demand for targeted cancer therapies further boosts usage.

The Polymeric Micelles segment is expected to witness the fastest growth at a CAGR of 7.1% from 2026 to 2033, driven by its ability to improve solubility of hydrophobic Taxane drugs. These systems provide enhanced stability and controlled drug release. Targeted delivery improves treatment efficiency and reduces side effects. Rising research in smart drug delivery systems is accelerating adoption. Increasing clinical trials in oncology are supporting expansion. Pharmaceutical companies are investing in polymer-based nanocarriers. Growing focus on precision medicine enhances demand. Improved therapeutic outcomes drive physician preference. Expanding use in advanced cancer therapies supports growth. Technological advancements in formulation science are boosting innovation. Overall, polymeric micelles represent a high-growth formulation segment.

- By Age Group

On the basis of age group, the market is segmented into Adults and Geriatric populations. The Geriatric segment dominated the market with a 58.47% share in 2025 due to the higher incidence of cancer among elderly populations. Aging is a major risk factor for multiple cancers treated using Taxane-based chemotherapy. Increasing life expectancy globally contributes to a growing elderly patient base. Hospitals frequently report higher chemotherapy usage among geriatric patients. Strong healthcare infrastructure supports elderly cancer care. Early diagnosis programs in older populations further enhance treatment demand. High hospitalization rates among elderly patients reinforce dominance. Government healthcare systems prioritize geriatric oncology care. Specialized oncology treatments for elderly patients support sustained usage. Overall, geriatric population remains the primary consumer base.

The Adult segment is expected to witness the fastest growth at a CAGR of 6.8% from 2026 to 2033, driven by rising cancer incidence among middle-aged populations. Lifestyle changes, environmental exposure, and genetic factors are increasing cancer risk. Early screening and diagnosis programs are improving detection rates. Expanding access to oncology care is boosting treatment adoption. Improved healthcare awareness supports early intervention. Increasing insurance coverage enhances affordability of treatment. Rising incidence of breast, lung, and ovarian cancers among adults supports growth. Advancements in targeted therapies improve survival outcomes. Expanding clinical trials involving adult populations strengthen adoption. Corporate healthcare initiatives further support treatment access. Overall, the adult segment shows strong future growth potential.

- By Application

On the basis of application, the market is segmented into Breast Cancer, Non-Small Cell Lung Cancer, Pancreatic Cancer, Ovarian Cancer, Prostate Cancer, and Others. The Breast Cancer segment dominated the market with a 42.73% share in 2025 due to its high global incidence and strong reliance on Taxane-based chemotherapy. Taxanes are widely used in both early-stage and metastatic breast cancer treatment protocols. Established clinical guidelines support their use in combination therapies. High awareness and screening programs contribute to early diagnosis and treatment. Strong hospital adoption ensures consistent demand. Large patient volume across global healthcare systems reinforces dominance. Continuous clinical validation strengthens therapeutic trust. Government cancer control programs support treatment accessibility. Increasing use in combination regimens enhances effectiveness. Overall, breast cancer remains the leading application segment.

The Pancreatic Cancer segment is expected to witness the fastest growth at a CAGR of 7.6% from 2026 to 2033, driven by rising incidence and limited treatment options. Taxanes are increasingly used in combination chemotherapy regimens to improve survival outcomes. Poor prognosis of pancreatic cancer creates high unmet medical need. Advancements in diagnostic technologies are improving early detection. Rising research funding is supporting drug development. Clinical trials are expanding use of Taxane-based therapies. Increasing healthcare investment in oncology supports growth. Combination therapies are improving patient outcomes. Pharmaceutical innovation is accelerating treatment adoption. Growing awareness among clinicians supports usage expansion. Overall, pancreatic cancer represents a high-growth opportunity segment.

- By End User

On the basis of end user, the market is segmented into Hospitals, Ambulatory Surgical Centers, Specialty Clinics, and Others. The Hospitals segment dominated the market with a 64.12% share in 2025 due to high patient inflow and advanced oncology infrastructure. Hospitals are primary centers for chemotherapy administration. Availability of specialized oncology departments supports strong adoption. Large-scale procurement of Taxane drugs strengthens dominance. Government healthcare funding supports hospital-based treatment. Presence of skilled oncologists enhances treatment delivery. Strong reimbursement systems increase accessibility. Hospitals handle complex and late-stage cancer cases. Established supply chains ensure drug availability. Overall, hospitals remain the central treatment hub.

The Specialty Clinics segment is expected to witness the fastest growth at a CAGR of 6.5% from 2026 to 2033, driven by increasing demand for outpatient and personalized cancer care. Specialty clinics offer cost-effective treatment compared to hospitals. Rising preference for shorter hospital stays supports adoption. Expanding oncology-focused clinics enhance accessibility. Improved drug administration technologies boost efficiency. Urban healthcare expansion supports clinic growth. Better patient monitoring systems improve outcomes. Increasing private healthcare investment accelerates expansion. Growing awareness of early treatment supports usage. Enhanced convenience drives patient preference. Overall, specialty clinics are emerging as a fast-growing segment.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into Retail Sales and Direct Tender. The Direct Tender segment dominated the market with a 67.89% share in 2025 due to bulk procurement by hospitals and government healthcare systems. This channel ensures cost efficiency and consistent drug supply. Large-scale institutional purchasing strengthens dominance. Government oncology programs heavily rely on direct procurement. Centralized purchasing systems improve supply chain efficiency. Pharmaceutical companies prefer long-term institutional contracts. Strong regulatory frameworks support tender-based systems. High oncology patient volume drives bulk demand. Reliable distribution networks enhance accessibility. Overall, direct tender remains the leading distribution channel.

The Retail Sales segment is expected to witness the fastest growth at a CAGR of 6.7% from 2026 to 2033, driven by increasing outpatient treatments and expanding pharmacy networks. Rising availability of oncology drugs in retail pharmacies supports adoption. Digital pharmacy platforms are improving accessibility. Growing patient preference for convenience enhances demand. Expanding healthcare infrastructure supports distribution growth. Improved insurance coverage increases affordability. E-commerce penetration is supporting drug availability. Urbanization is strengthening pharmacy networks. Rising awareness of cancer treatment options boosts usage. Overall, retail sales are emerging as a fast-growing channel.

Taxane Market Regional Analysis

North America dominated the Taxane Market and accounted for the largest revenue share of 38.62% in 2025, supported by high cancer prevalence, strong presence of advanced oncology treatment centers, extensive adoption of chemotherapy regimens, and well-established healthcare reimbursement systems. The region also benefits from robust clinical research activities, early adoption of novel drug formulations such as nanoparticle and liposomal taxanes, and strong presence of key pharmaceutical companies driving innovation in oncology therapeutics. Increasing utilization of taxane-based chemotherapy in breast cancer, lung cancer, and prostate cancer treatment continues to strengthen regional demand.

U.S. Taxane Market Insight

The U.S. Taxane market is witnessing strong growth due to rising cancer incidence, particularly breast, lung, and prostate cancers, along with increasing adoption of advanced chemotherapy protocols in hospitals and specialty oncology centers. Strong presence of leading pharmaceutical companies and research institutes is accelerating drug innovation and clinical trials. In addition, favorable reimbursement policies and widespread access to oncology care are supporting treatment adoption across both public and private healthcare systems. Growing investment in precision oncology and combination therapies is further enhancing market expansion in the country.

Europe Taxane Market Insight

The Europe Taxane market remains a major contributor to global revenue, driven by strong healthcare infrastructure, increasing cancer burden, and high adoption of standardized chemotherapy treatment protocols. The region benefits from well-established oncology care systems, strong regulatory frameworks, and increasing use of taxane-based drugs in breast cancer and non-small cell lung cancer treatment. Rising geriatric population and expanding cancer screening programs are further supporting market growth across European countries.

U.K. Taxane Market Insight

The U.K. Taxane market is experiencing steady growth due to rising cancer diagnosis rates and strong reliance on taxane-based chemotherapy in hospital treatment protocols. Increasing investment in oncology research, clinical trials, and precision medicine is strengthening treatment outcomes. In addition, strong NHS-driven cancer care programs and expanding access to innovative oncology drugs are supporting market demand. Growing focus on early cancer detection and personalized treatment approaches is further driving adoption.

Germany Taxane Market Insight

The Germany Taxane market is expanding steadily due to its strong pharmaceutical manufacturing base, advanced oncology infrastructure, and high adoption of innovative cancer therapies. Hospitals and specialized cancer centers are increasingly using taxane-based regimens for breast, lung, and prostate cancers. In addition, strong clinical research activity and government support for oncology innovation are supporting drug development and adoption. Rising demand for biologics and combination therapies is further strengthening market growth in Germany.

Asia-Pacific Taxane Market Insight

The Asia-Pacific Taxane market is expected to witness rapid growth, driven by increasing cancer burden, expanding healthcare infrastructure, and rising government investments in oncology care programs across countries such as China, India, and Japan. Growing awareness regarding early cancer diagnosis, improving access to chemotherapy, and rising adoption of affordable generic taxanes are supporting regional market expansion. In addition, increasing hospital infrastructure and oncology treatment capacity are accelerating demand across the region.

Japan Taxane Market Insight

The Japan Taxane market is witnessing consistent growth due to its aging population, high cancer prevalence, and strong healthcare system focused on advanced oncology treatments. Japanese hospitals are widely adopting taxane-based chemotherapy for breast, lung, and gastric cancers. In addition, strong pharmaceutical innovation, clinical research activity, and early adoption of novel drug formulations such as nanoparticle-based taxanes are supporting market growth. Government focus on cancer prevention and precision medicine is further strengthening demand.

China Taxane Market Insight

The China Taxane market is growing rapidly, driven by rising cancer incidence, expanding healthcare infrastructure, and increasing government investments in oncology treatment programs. The country is witnessing strong adoption of both branded and generic taxane drugs across hospitals and cancer treatment centers. In addition, rapid expansion of pharmaceutical manufacturing, improving reimbursement coverage, and growing clinical research activities are boosting market development. Increasing awareness of early cancer diagnosis and treatment accessibility is positioning China as one of the fastest-growing markets globally.

Taxane Market Share

The Taxane industry is primarily led by well-established companies, including:

- Pfizer Inc. (U.S.)

- Bristol Myers Squibb Company (U.S.)

- Novartis AG (Switzerland)

- Sanofi S.A. (France)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Cipla Ltd. (India)

- Sun Pharmaceutical Industries Ltd. (India)

- Dr. Reddy’s Laboratories Ltd. (India)

- Fresenius Kabi AG (Germany)

- Hetero Drugs Ltd. (India)

- Lupin Limited (India)

- Viatris Inc. (U.S.)

- Hikma Pharmaceuticals PLC (U.K.)

- Johnson & Johnson (U.S.)

- Celgene Corporation (now part of Bristol Myers Squibb, U.S.)

- Baxter International Inc. (U.S.)

- Accord Healthcare (U.K.)

- Aurobindo Pharma Ltd. (India)

- Zydus Lifesciences Ltd. (India)

- Mylan N.V. (now Viatris, U.S.)

- Eli Lilly and Company (U.S.)

- Amgen Inc. (U.S.)

- Takeda Pharmaceutical Company Limited (Japan)

- Sandoz Group AG (Switzerland)

- Intas Pharmaceuticals Ltd. (India)

Latest Developments in Taxane Market

- In October 2021, the U.S. Food and Drug Administration (FDA) granted accelerated approval to tisotumab vedotin (Tivdak) for the treatment of recurrent or metastatic cervical cancer in patients whose disease progressed during or after chemotherapy. This approval expanded the broader taxane-based oncology ecosystem by strengthening interest in next-generation microtubule-targeting antibody-drug conjugates, reinforcing innovation beyond traditional taxanes such as paclitaxel and docetaxel

- In September 2023, regulatory and clinical adoption of albumin-bound paclitaxel (nab-paclitaxel; Abraxane) continued to expand globally, supported by increasing use in pancreatic cancer, non-small cell lung cancer, and metastatic breast cancer treatment protocols. The formulation’s solvent-free nanoparticle design enabled higher drug delivery efficiency and reduced hypersensitivity reactions compared to conventional paclitaxel, strengthening its position in chemotherapy regimens across major oncology centers worldwide

- In November 2023, the European Medicines Agency (EMA) Committee for Medicinal Products for Human Use (CHMP) issued a positive opinion for new paclitaxel-based formulations, including expanded indications for metastatic breast cancer, pancreatic adenocarcinoma, and non-small cell lung cancer. This development highlighted continued innovation in taxane reformulations aimed at improving efficacy, solubility, and patient tolerability, particularly in combination chemotherapy settings

- In April 2024, the FDA granted traditional approval to tisotumab vedotin (Tivdak) for recurrent or metastatic cervical cancer, transitioning it from accelerated approval status. This milestone demonstrated increasing regulatory confidence in antibody–drug conjugate therapies linked to microtubule-disrupting mechanisms, reinforcing the evolution of taxane-class therapeutic strategies in oncology

- In May 2024, the EMA CHMP adopted a positive opinion for Apexelsin, a paclitaxel-based therapy intended for metastatic breast cancer, pancreatic adenocarcinoma, and non-small cell lung cancer. This approval reflected growing demand for improved taxane formulations in Europe, particularly in cancers with high global incidence and rising chemotherapy dependency

- In January 2025, the EMA issued a positive opinion for Tivdak (tisotumab vedotin) for recurrent or metastatic cervical cancer, supporting its authorization across European markets. This development further expanded access to advanced taxane-related therapeutic mechanisms in oncology, particularly in regions with rising cervical cancer burden and increasing adoption of targeted chemotherapy approaches

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.