Global Thermoelectric Modules Market

Market Size in USD Million

CAGR :

%

USD

950.13 Million

USD

1,933.87 Million

2025

2033

USD

950.13 Million

USD

1,933.87 Million

2025

2033

| 2026 –2033 | |

| USD 950.13 Million | |

| USD 1,933.87 Million | |

| % | |

|

Global Thermoelectric Modules Market Overview

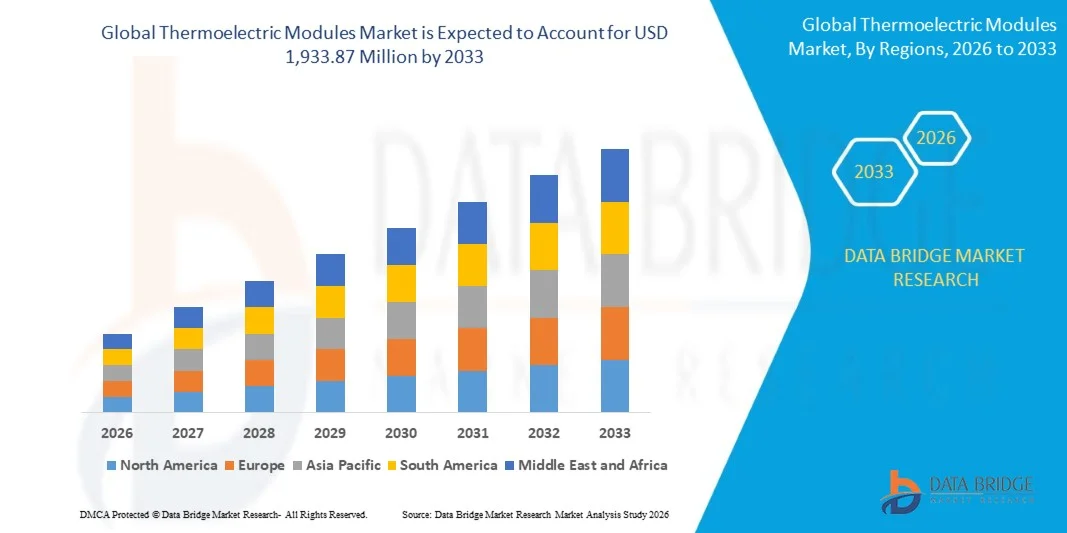

The global thermoelectric modules market was valued at USD 950.13 million in 2025 and is projected to reach USD 1,933.87 million by 2033, growing at a CAGR of 9.29% from 2026 to 2033. The market is witnessing steady growth driven by increasing demand for compact solid-state cooling and power generation solutions across electronics, automotive, aerospace, and healthcare applications. Growing emphasis on energy efficiency and waste heat recovery is further accelerating the adoption of thermoelectric modules as a sustainable alternative to conventional cooling systems.

The rising miniaturization of electronic devices, coupled with the need for precise temperature control in sensitive components, is significantly boosting the deployment of thermoelectric modules in consumer electronics and semiconductor applications. In addition, expanding use in automotive seat cooling, battery thermal management in electric vehicles, and medical devices such as portable refrigerators and diagnostic equipment is strengthening market growth. Continuous advancements in thermoelectric materials and improvements in conversion efficiency are further enhancing product performance and widening commercial adoption.

Key Market Trends & Insights

- North America dominated the global thermoelectric modules market with the largest revenue share of 36.8% in 2025, supported by strong adoption of advanced thermal management technologies across automotive, aerospace, defense, and semiconductor industries.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR from 2026 to 2033, fueled by rapid industrialization, expanding consumer electronics manufacturing, and increasing electric vehicle production across countries such as China, Japan, South Korea, and India.

- The Single-Stage segment held the largest market revenue share of approximately 64.8% in 2025 driven by its widespread use in consumer electronics, automotive cooling systems, and industrial temperature stabilization applications.

- The Multi-Stage segment is projected to register the fastest growth at a CAGR of 10.8% from 2026 to 2033, driven by increasing demand for ultra-low temperature cooling in medical devices, aerospace systems, and laboratory instrumentation.

- The Bulk Thermoelectric Modules segment accounted for the largest market share of nearly 58.3% in 2025 driven by its extensive adoption across automotive, industrial waste heat recovery, and consumer cooling applications.

- The Thin-Film Thermoelectric Modules segment is projected to register the fastest growth at a CAGR of 11.6% from 2026 to 2033, driven by increasing integration in wearable electronics, compact medical sensors, and semiconductor devices.

- The General-purpose Modules segment dominated the market with a revenue share of approximately 69.1% in 2025 driven by broad deployment across refrigeration systems, portable cooling devices, telecommunications equipment, and automotive applications.

- The Deep Cooling Modules segment is projected to register the fastest growth at a CAGR of 10.3% from 2026 to 2033, driven by rising demand for ultra-low temperature environments in medical laboratories, aerospace electronics, and defense-grade thermal imaging equipment.

- The Hardware segment held the largest market share of around 76.4% in 2025 driven by high demand for thermoelectric chips, cooling assemblies, controllers, and integrated thermal systems across industrial and automotive sectors.

- The Services segment is projected to register the fastest growth at a CAGR of 11.1% from 2026 to 2033, driven by increasing demand for thermal system optimization, maintenance support, and customized module integration services. Growing adoption of advanced thermal management technologies across industrial facilities and data centers is accelerating segment expansion.

Market Size & Forecast

- Global Market Value (2025): USD 950.13 Million

- Expected Market Value (2033): USD 1,933.87 Million

- Forecast CAGR (2026–2033): 9.29%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Thermoelectric Modules Market Segmentation

|

Attributes |

Thermoelectric Modules Key Market Insights |

|

Segments Covered |

· By Model: Single-Stage and Multi-Stage · By Type: Bulk Thermoelectric Modules, Micro Thermoelectric Modules, and Thin-Film Thermoelectric Modules · By Functionality: Deep Cooling Modules and General-purpose Modules · By Offering: Hardware, Software and Services · By End- Use Application: Consumer Electronics, Telecommunications, Automotive, Industrial, Medical and Laboratories, Aerospace and Defense, and Oil, Gas and Mining |

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

• Custom Thermoelectric, LLC (U.S.) |

|

Market Opportunities |

• Expansion In Electric Vehicle Thermal Management Systems |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Global Thermoelectric Modules Market Trends

Trend: Growth In Waste Heat Recovery And Advanced Solid-State Cooling Applications

Increasing demand for energy-efficient, compact, and environmentally sustainable thermal management technologies across automotive, industrial, and electronics sectors. Conventional compressor-based cooling systems consume higher energy, require continuous maintenance, and use refrigerants associated with environmental concerns, encouraging industries to adopt solid-state alternatives with lower operational complexity.

In modern electric vehicles, manufacturers are integrating thermoelectric systems, for instance for battery thermal management and cabin temperature control, to improve efficiency and extend battery life while reducing noise and vibration. In industrial systems, these modules are being used to convert low-grade waste heat from manufacturing processes into usable electrical energy, improving overall energy utilization and reducing thermal losses.

The rapid expansion of compact consumer electronics and high-performance computing infrastructure is also increasing demand for silent and highly precise cooling systems capable of operating in limited spaces. In addition, space and defense sectors continue to rely on thermoelectric technology, such as NASA’s radioisotope thermoelectric generators used in Voyager and Mars rover missions, because of their reliability in extreme operating environments. Growing industry validation through pilot automotive trials in 2025 integrating thermoelectric modules directly into EV battery packs is showing efficiency improvements of nearly 8–12% in localized thermal regulation under high-load operating conditions

Global Thermoelectric Modules Market Dynamics

Key Market Driver: Rising Adoption Of Energy Efficient Waste Heat Recovery Systems

Industries worldwide are facing increasing regulatory and economic pressure to reduce energy wastage, lower carbon emissions, and improve operational efficiency. Large quantities of heat generated from industrial machinery, automotive engines, and manufacturing processes are typically dissipated into the environment without utilization, creating strong demand for technologies capable of converting excess thermal energy into usable electricity.

Industries such as automotive, oil and gas, and manufacturing are increasingly deploying thermoelectric generators to capture and reuse waste heat from engines, exhaust systems, and industrial equipment to reduce fuel consumption and improve energy efficiency. Automotive OEMs are actively testing thermoelectric systems, for instance in electric and hybrid vehicles for enhanced energy recovery, to support stricter fuel efficiency and emission reduction targets.

Similarly, data centers and semiconductor facilities are exploring thermoelectric cooling to manage rising heat loads generated by AI-driven computing infrastructure while reducing dependence on energy-intensive cooling technologies. Real-world industrial deployments in Japan and Germany during 2024 integrating thermoelectric waste heat recovery units into furnace exhaust systems demonstrated recovery of around 3–5% of dissipated thermal energy in continuous manufacturing operations

Key Restraint/Challenge: Low Conversion Efficiency And High Material Costs

Currently available thermoelectric materials are unable to deliver energy conversion efficiencies comparable to conventional cooling and power generation technologies in large-scale applications. The performance limitations of materials such as bismuth telluride reduce the ability of thermoelectric modules to generate high electrical output from low-temperature heat sources, limiting their suitability for high-power industrial deployment.

In addition, expensive raw materials, specialized semiconductor fabrication processes, and complex module assembly increase overall system costs, creating affordability concerns for small-scale industries and cost-sensitive markets. Limited scalability for high-energy output applications further restricts commercialization in emerging economies where return on investment remains a key purchasing consideration.

Commercial benchmarking studies indicate that thermoelectric modules, for instance standard bismuth telluride-based systems, typically operate at efficiencies of around 5–8%, significantly lower than vapor compression systems exceeding 25–30% efficiency in large-scale cooling applications

Key Market Opportunity: Integration In Electric Vehicles And Next-Generation Electronics

Modern electric vehicles, wearable devices, AI processors, and compact electronic systems increasingly require lightweight, compact, and highly precise thermal management technologies. Conventional cooling systems are often bulky, noisy, and difficult to integrate into miniaturized electronic architectures, creating demand for compact solid-state cooling solutions with low maintenance requirements.

Automotive companies are increasingly exploring thermoelectric systems, for instance for seat cooling, battery thermal regulation, and exhaust energy recovery, to improve EV performance, passenger comfort, and battery efficiency without increasing mechanical complexity. In consumer electronics, rising device miniaturization and increasing thermal density are accelerating demand for silent and highly efficient cooling systems for smartphones, sensors, and IoT devices.

In addition, advancements in nanostructured thermoelectric materials and hybrid system designs are improving module performance, opening opportunities across aerospace, defense, and AI-powered computing infrastructure markets in Asia-Pacific and North America. EV testing programs conducted in 2025 across China and South Korea reported temperature stabilization improvements of around 10–15°C under peak load conditions after integrating thermoelectric-based battery thermal management systems

Global Thermoelectric Modules Market Scope

The market is segmented on the basis of model, type, functionality, offering, and end-use application.

- By Model

On the basis of model, the thermoelectric modules market is segmented into Single-Stage and Multi-Stage. The Single-Stage segment held the largest market revenue share of approximately 64.8% in 2025 driven by its widespread use in consumer electronics, automotive cooling systems, and industrial temperature stabilization applications. Single-stage modules are preferred due to their compact structure, lower power consumption, and cost-effectiveness for standard cooling requirements across electronic devices and battery management systems.

The Multi-Stage segment is projected to register the fastest growth at a CAGR of 10.8% from 2026 to 2033, driven by increasing demand for ultra-low temperature cooling in medical devices, aerospace systems, and laboratory instrumentation. Rising adoption in scientific research applications and defense-grade thermal management systems is accelerating segment expansion.

- By Type

On the basis of type, the thermoelectric modules market is segmented into Bulk Thermoelectric Modules, Micro Thermoelectric Modules, and Thin-Film Thermoelectric Modules. The Bulk Thermoelectric Modules segment accounted for the largest market share of nearly 58.3% in 2025 driven by its extensive adoption across automotive, industrial waste heat recovery, and consumer cooling applications. These modules offer higher durability, established manufacturing processes, and reliable performance in medium- and high-power thermal management systems.

The Thin-Film Thermoelectric Modules segment is projected to register the fastest growth at a CAGR of 11.6% from 2026 to 2033, driven by increasing integration in wearable electronics, compact medical sensors, and semiconductor devices. Advancements in miniaturization technologies and growing demand for localized thermal control in next-generation electronic systems are accelerating segment expansion.

- By Functionality

On the basis of functionality, the thermoelectric modules market is segmented into Deep Cooling Modules and General-purpose Modules. The General-purpose Modules segment dominated the market with a revenue share of approximately 69.1% in 2025 driven by broad deployment across refrigeration systems, portable cooling devices, telecommunications equipment, and automotive applications. These modules are widely preferred for standard heating and cooling operations due to their affordability, versatility, and ease of integration into commercial electronic systems.

The Deep Cooling Modules segment is projected to register the fastest growth at a CAGR of 10.3% from 2026 to 2033, driven by rising demand for ultra-low temperature environments in medical laboratories, aerospace electronics, and defense-grade thermal imaging equipment. Increasing investments in advanced diagnostic technologies and scientific instrumentation are accelerating segment expansion.

- By Offering

On the basis of offering, the thermoelectric modules market is segmented into Hardware, Software, and Services. The Hardware segment held the largest market share of around 76.4% in 2025 driven by high demand for thermoelectric chips, cooling assemblies, controllers, and integrated thermal systems across industrial and automotive sectors. Continuous deployment of physical cooling infrastructure in EVs, consumer electronics, and industrial machinery is significantly contributing to segment dominance.

The Services segment is projected to register the fastest growth at a CAGR of 11.1% from 2026 to 2033, driven by increasing demand for thermal system optimization, maintenance support, and customized module integration services. Growing adoption of advanced thermal management technologies across industrial facilities and data centers is accelerating segment expansion.

- By End-Use Application

On the basis of end-use application, the thermoelectric modules market is segmented into Consumer Electronics, Telecommunications, Automotive, Industrial, Medical and Laboratories, Aerospace and Defense, and Oil, Gas and Mining. The Consumer Electronics segment accounted for the largest market revenue share of nearly 31.7% in 2025 driven by increasing integration of thermoelectric cooling systems in smartphones, portable refrigerators, gaming systems, and wearable electronic devices. Rising demand for compact, silent, and energy-efficient cooling technologies in miniaturized electronic products is further supporting segment expansion.

The Automotive segment is projected to register the fastest growth at a CAGR of 12.4% from 2026 to 2033, driven by increasing integration of thermoelectric systems in electric vehicles for battery thermal management, seat cooling, and waste heat recovery applications. Expanding EV production globally and growing focus on vehicle energy efficiency and passenger comfort are accelerating segment expansion.

Global Thermoelectric Modules Market Regional Analysis

- North America dominated the thermoelectric modules market with the largest revenue share of 36.8% in 2025, driven by strong adoption of advanced thermal management technologies across automotive, aerospace, defense, and semiconductor industries

- The region benefits from high investments in energy-efficient technologies, increasing deployment of electric vehicles, and growing focus on waste heat recovery systems across industrial manufacturing operations

- Rising demand for compact cooling systems in data centers, medical devices, and consumer electronics, alongside strong R&D capabilities and the presence of leading thermoelectric technology providers, is further supporting market expansion across residential, commercial, and industrial sectors

U.S. Thermoelectric Modules Market Insight

The U.S. thermoelectric modules market captured the largest revenue share in 2025 within North America, fueled by increasing demand for energy-efficient cooling technologies and expanding adoption of electric vehicles and advanced semiconductor systems. Industries are increasingly deploying thermoelectric modules for battery thermal management, industrial waste heat recovery, and aerospace applications. The country’s strong focus on AI-driven data centers and high-performance computing infrastructure is also accelerating demand for compact and precise cooling technologies. Moreover, increasing government support for energy efficiency and carbon reduction initiatives is significantly contributing to market growth.

Europe Thermoelectric Modules Market Insight

The Europe thermoelectric modules market is expected to witness the fastest growth rate from 2026 to 2033, primarily driven by stringent environmental regulations and increasing investments in sustainable energy technologies. The region is witnessing rising adoption of thermoelectric systems in electric vehicles, industrial waste heat recovery, and renewable energy applications. Growing demand for low-emission thermal management technologies across automotive and manufacturing sectors is further accelerating market expansion. In addition, increasing integration of thermoelectric cooling systems into medical devices and smart industrial equipment is supporting regional growth.

U.K. Thermoelectric Modules Market Insight

The U.K. thermoelectric modules market is expected to witness the fastest growth rate from 2026 to 2033, driven by rising investments in electric mobility, advanced electronics manufacturing, and energy-efficient industrial systems. The country is increasingly adopting thermoelectric technologies for battery cooling, portable refrigeration, and precision medical equipment applications. Growing emphasis on carbon neutrality targets and industrial energy optimization is further encouraging deployment of waste heat recovery technologies across manufacturing facilities and commercial infrastructure.

Germany Thermoelectric Modules Market Insight

The Germany thermoelectric modules market is expected to witness the fastest growth rate from 2026 to 2033, fueled by strong automotive manufacturing capabilities and increasing adoption of advanced thermal management technologies in electric vehicles and industrial automation systems. Germany’s focus on energy efficiency and industrial sustainability is promoting integration of thermoelectric systems into waste heat recovery infrastructure and high-performance electronics. The presence of advanced semiconductor and automotive industries, combined with increasing investments in Industry 4.0 technologies, is further strengthening market growth.

Asia-Pacific Thermoelectric Modules Market Insight

The Asia-Pacific thermoelectric modules market is expected to witness the fastest growth rate from 2026 to 2033, driven by rapid industrialization, expanding consumer electronics manufacturing, and increasing electric vehicle production across countries such as China, Japan, South Korea, and India. Growing urbanization and rising demand for energy-efficient cooling technologies are accelerating deployment across automotive, telecommunications, and industrial applications. Furthermore, the region’s strong semiconductor manufacturing ecosystem and expanding investments in smart electronics and renewable energy systems are contributing significantly to market expansion.

Japan Thermoelectric Modules Market Insight

The Japan thermoelectric modules market is expected to witness the fastest growth rate from 2026 to 2033 due to the country’s advanced electronics industry, high adoption of precision cooling technologies, and growing focus on energy-efficient industrial systems. Japanese manufacturers are increasingly integrating thermoelectric modules into automotive electronics, medical equipment, and semiconductor cooling applications. The country’s emphasis on technological innovation and miniaturized electronic devices is further supporting adoption of compact solid-state thermal management systems across industrial and consumer applications.

China Thermoelectric Modules Market Insight

The China thermoelectric modules market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to the country’s large-scale electronics manufacturing sector, rapid EV production growth, and expanding industrial automation infrastructure. China is one of the largest producers and consumers of thermoelectric cooling technologies, with increasing adoption across consumer electronics, automotive battery systems, telecommunications, and industrial equipment. Government initiatives supporting electric vehicles, renewable energy technologies, and semiconductor manufacturing, alongside the presence of cost-competitive domestic manufacturers, are major factors driving market growth in China.

Global Thermoelectric Modules Market Share

The Thermoelectric Modules industry is primarily led by well-established companies, including:

Custom Thermoelectric, LLC (U.S.)

• WATRONIX, Inc. (U.S.)

• Alutron Modules Inc (U.S.)

• Bourns, Inc. (U.S.)

• Crystal Ltd. (Russia)

• Ferrotec (USA) Corporation. (U.S.)

• Laird Thermal Systems (U.S.)

• II-VI Incorporated (U.S.)

• TE Technology, Inc. (U.S.)

• TEC Microsystems GmbH (Germany)

• kreazone.ru (Russia)

• RMT Ltd. (Russia)

• Thermonamic Electronics (Jiangxi) Corp., Ltd. (China)

• KELK Ltd. (Japan)

• Guangdong Fuxin Electronic Technology Co., Ltd. (China)

• EVERREDtronics Ltd. (China)

• Xiamen Hicool Electronics Co., Ltd. (China)

• Hui Mao (China)

• EH4 GmbH (Germany)

• Quick-OHM Küpper & Co. GmbH (Germany)

Latest Developments in Global Thermoelectric Modules Market

- In November 2025, Laird Thermal Systems (U.S.) entered into a strategic collaboration with a renewable energy company to develop thermoelectric modules specifically designed for solar energy applications. The partnership focuses on improving thermal-to-electric energy conversion efficiency in solar infrastructure and supporting next-generation sustainable energy systems. The development is expected to strengthen Laird Thermal Systems’ position in the renewable energy thermal management sector while expanding its product portfolio for industrial and utility-scale applications. The collaboration also reflects growing industry interest in integrating thermoelectric technologies into renewable power generation systems to improve overall energy utilization and reduce operational losses. Increasing investments in clean energy infrastructure globally are expected to further support commercial adoption of such advanced thermoelectric solutions

- In October 2025, RMT Ltd. (U.K.) launched a new range of thermoelectric generators targeted toward industrial energy recovery applications. The newly introduced product line is designed to improve waste heat conversion efficiency across manufacturing plants, industrial processing facilities, and heavy machinery operations. The launch strengthens the company’s position in industrial thermoelectric technology while addressing increasing global demand for energy-efficient and low-emission industrial systems. The new generators are expected to support industrial operators in reducing energy wastage and improving operational sustainability through advanced thermal energy recovery capabilities. The development also reflects increasing adoption of thermoelectric systems in industrial decarbonization strategies and energy optimization initiatives

- In September 2025, Micropelt (Germany) secured a major supply contract with a European automotive manufacturer for thermoelectric modules used in electric vehicle applications. The agreement focuses on integrating thermoelectric technology into EV battery thermal management and automotive electronic cooling systems to improve energy efficiency and temperature stability. The contract strengthens Micropelt’s presence in the rapidly expanding electric mobility market and highlights growing automotive demand for compact solid-state cooling technologies. The partnership is also expected to accelerate commercialization of thermoelectric solutions within next-generation electric vehicles and connected automotive systems. Rising EV production across Europe and increasing focus on battery performance optimization are further supporting adoption of advanced thermoelectric technologies in the automotive sector

- In June 2024, Ferrotec Corporation (Japan) announced the relocation of its U.S. subsidiary operations from Santa Clara to Livermore, California to strengthen its semiconductor and precision thermal component manufacturing capabilities. The expansion is intended to improve operational efficiency, enhance supply chain capabilities, and support increasing customer demand from semiconductor and electronics industries across North America. The relocation further reinforces the company’s strategic presence within the U.S. technology and semiconductor ecosystem, particularly in high-growth AI and advanced computing markets. The development is expected to improve Ferrotec’s production scalability and strengthen long-term customer partnerships within the semiconductor thermal management sector. Growing investments in AI infrastructure and semiconductor manufacturing are likely to further support market demand for precision thermoelectric solutions

- In April 2023, Laird Thermal Systems (U.S.) launched the OptoTEC MBX Series micro thermoelectric cooler designed for high-temperature operating environments and compact-space applications. The product introduction aims to improve cooling efficiency and thermal precision for optoelectronics, medical devices, semiconductor systems, and industrial laser applications. The new series offers enhanced thermal cycling performance and miniaturized architecture, supporting growing demand for compact and highly reliable cooling technologies in advanced electronics. The launch strengthens the company’s product portfolio in micro-scale thermal management solutions and expands its capabilities in high-performance cooling applications. Increasing demand for compact semiconductor devices and high-density electronics is expected to further accelerate adoption of advanced micro thermoelectric cooling systems

- In October 2022, RMT Ltd. (U.K.) introduced a new multi-purpose thermoelectric module product line developed for high heat absorption applications, including infrared sensors, deep-cooled CMOS systems, and scientific instrumentation. The new modules are designed to provide improved cooling stability, enhanced thermal control, and higher reliability in precision electronic and imaging systems. The launch strengthens the company’s position in industrial and laboratory thermal management applications while expanding its product offerings for specialized cooling environments. The development also reflects increasing demand for advanced thermoelectric cooling technologies across aerospace, defense, medical imaging, and scientific research sectors. Rising adoption of high-performance infrared sensing and imaging technologies is expected to further support demand for deep-cooling thermoelectric modules

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Thermoelectric Modules Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Thermoelectric Modules Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Thermoelectric Modules Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.