Global Tissue Engineered Skin Substitutes Market

Market Size in USD Billion

CAGR :

%

USD

2.50 Billion

USD

7.59 Billion

2025

2033

USD

2.50 Billion

USD

7.59 Billion

2025

2033

| 2026 –2033 | |

| USD 2.50 Billion | |

| USD 7.59 Billion | |

| % | |

|

Tissue Engineered Skin Substitute Market Size

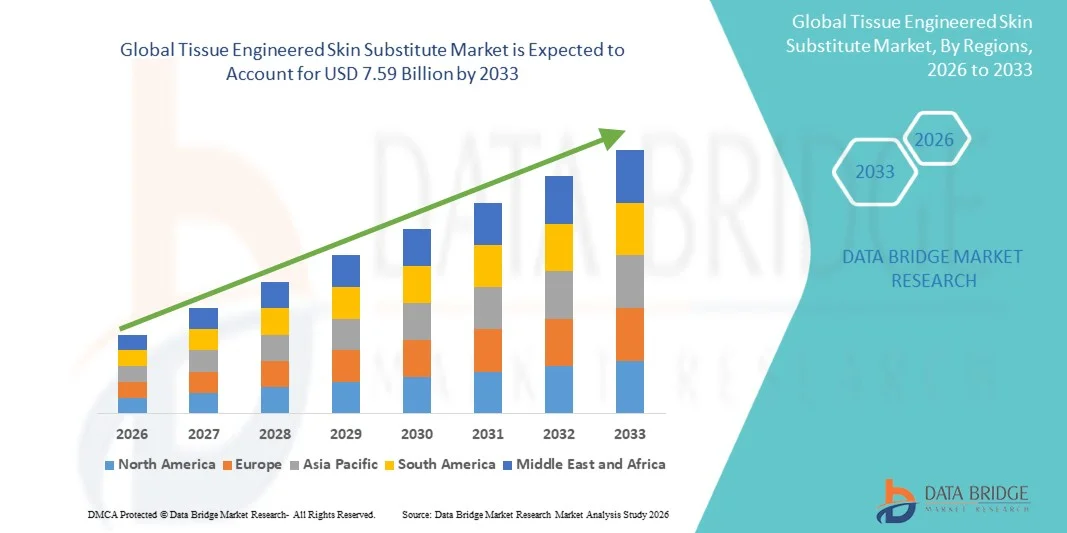

- The global tissue engineered skin substitute market size was valued at USD 2.50 billion in 2025 and is expected to reach USD 7.59 billion by 2033, at a CAGR of 14.90% during the forecast period

- The market growth is largely fueled by rising incidences of chronic wounds, burns, and skin-related disorders, alongside technological advancements in bioengineered and regenerative skin solutions

- Furthermore, increasing demand for faster wound healing, reduced hospitalization time, and improved quality of life is driving adoption in both hospitals and specialized care centers. These converging factors are accelerating the uptake of tissue engineered skin substitutes, thereby significantly boosting the industry's growth

Tissue Engineered Skin Substitute Market Analysis

- Tissue engineered skin substitutes, providing bioengineered or regenerative skin for wound healing and burn management, are increasingly vital in modern healthcare due to their ability to promote faster recovery, reduce infection risks, and improve patient outcomes in both hospital and specialized care settings

- The escalating demand for tissue engineered skin substitutes is primarily fueled by the rising prevalence of chronic wounds, diabetic ulcers, and severe burn injuries, coupled with advancements in biomaterials, stem cell therapies, and scaffold technologies

- North America dominated the tissue engineered skin substitute market with the largest revenue share of 40.9% in 2025, characterized by advanced healthcare infrastructure, high awareness of regenerative medicine, and strong presence of key industry players. The U.S. experienced substantial growth in skin substitute adoption, particularly in burn centers and wound care clinics, driven by innovations from both established biotech firms and emerging regenerative medicine startups

- Asia-Pacific is expected to be the fastest growing region in the tissue engineered skin substitute market during the forecast period due to increasing incidence of chronic wounds, growing healthcare investments, and rising accessibility of advanced wound care solutions

- Allogeneic segment dominated the market with a market share of 42.7% in 2025, driven by their proven clinical efficacy, ready availability, and ability to reduce healing time and complications compared to conventional grafts

Report Scope and Tissue Engineered Skin Substitute Market Segmentation

|

Attributes |

Tissue Engineered Skin Substitute Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Tissue Engineered Skin Substitute Market Trends

“Advancements Through Stem Cell and 3D Bioprinting Integration”

- A significant and accelerating trend in the global tissue engineered skin substitutes market is the increasing integration of stem cell therapies and 3D bioprinting technologies, enhancing graft efficacy, customization, and regenerative outcomes

- For instance, researchers at Organovo have developed bioprinted skin constructs combining patient-derived cells to better mimic native tissue architecture for wound healing and burn care

- Integration of stem cells enables improved tissue regeneration, reduced scarring, and faster wound closure, while bioprinting allows precise control over skin layer composition and structure, optimizing patient outcomes

- The seamless integration of these technologies with advanced biomaterials facilitates the production of skin substitutes tailored to individual patient needs, promoting personalized regenerative medicine approaches

- This trend toward more biologically advanced, customizable, and clinically effective skin substitutes is fundamentally reshaping expectations in wound care and burn management. Consequently, companies such as PolarityTE are developing stem cell-enhanced and bioprinted skin substitutes with improved healing rates and functional recovery

- The demand for tissue engineered skin substitutes that offer enhanced regenerative capability and personalization is growing rapidly across hospitals, burn centers, and chronic wound clinics, as healthcare providers increasingly prioritize superior clinical outcomes and reduced hospitalization times

- Adoption of digital health tools, including wound imaging and telemedicine, is complementing tissue engineered skin substitutes by enabling remote monitoring and improving clinical decision-making for personalized treatments

Tissue Engineered Skin Substitute Market Dynamics

Driver

“Rising Prevalence of Chronic Wounds and Burn Injuries”

- The increasing prevalence of chronic wounds, diabetic ulcers, and severe burn injuries is a significant driver for the heightened demand for tissue engineered skin substitutes

- For instance, in March 2025, Avita Medical reported a surge in usage of its ReCell system for acute burn patients, highlighting rising clinical adoption of skin regeneration therapies

- As patients and healthcare providers seek faster healing, reduced complications, and improved quality of life, tissue engineered skin substitutes provide advanced solutions compared to traditional grafting methods

- Furthermore, increasing awareness of regenerative medicine and improved reimbursement policies in developed regions are supporting broader adoption of skin substitute products

- The convenience of ready-to-use grafts, reduced need for autografting, and compatibility with outpatient and hospital-based wound care settings are key factors propelling market growth in both chronic wound and burn care segments

- Rising geriatric population and increased incidence of lifestyle diseases such as diabetes are expanding the patient pool requiring advanced wound care solutions, driving demand for tissue engineered skin substitutes

- Government initiatives and funding to promote regenerative medicine research and commercialization are accelerating product availability and adoption across key healthcare markets

Restraint/Challenge

“High Cost and Regulatory Approval Complexity”

- The relatively high manufacturing cost of tissue engineered skin substitutes and complex regulatory approval requirements pose significant challenges to market expansion

- For instance, strict FDA and EMA guidelines for tissue-engineered products can delay product launches and limit rapid commercialization in major markets

- Ensuring consistent clinical efficacy, sterility, and safety while meeting regulatory standards increases production complexity and cost, making some products less accessible in price-sensitive regions

- While companies are working on cost optimization and scalable production methods, premium pricing can still hinder adoption, particularly in developing countries or smaller healthcare facilities

- Overcoming these challenges through streamlined regulatory pathways, cost-effective production, and healthcare provider education on clinical and economic benefits will be crucial for sustained market growth

- Limited long-term clinical data and concerns over graft durability or immune response may restrain healthcare providers from fully adopting tissue engineered skin substitutes

- Supply chain constraints for specialized biomaterials and patient-derived cells can create production bottlenecks, slowing market expansion despite rising demand

Tissue Engineered Skin Substitute Market Scope

The market is segmented on the basis of duration, anatomical structure, biomaterial, technology, application, end-users, and type.

- By Duration

On the basis of duration, the market is segmented into permanent and semi-permanent skin substitutes. The permanent segment dominated the market with the largest revenue share in 2025, driven by its long-term efficacy in wound coverage and reduced need for repeated interventions. Permanent substitutes are preferred in burn care and chronic wound management as they provide stable coverage, accelerate healing, and minimize the risk of secondary infections. Hospitals and specialized burn centers often favor permanent grafts for their predictable clinical outcomes and compatibility with standard wound care protocols. Their adoption is also fueled by advancements in bioengineered cellular and acellular scaffolds that enhance graft integration. The segment benefits from strong physician trust and patient acceptance, contributing to sustained market leadership.

The semi-permanent segment is expected to witness the fastest growth rate during 2026–2033, driven by increasing use in temporary wound coverage and skin regeneration therapy. Semi-permanent substitutes are often utilized in early wound stabilization, allowing for interim protection while preparing autologous grafts or advanced regenerative treatments. The flexibility of semi-permanent grafts in different wound types, combined with their cost-effectiveness and ease of storage, supports rising adoption in emerging markets. Growing awareness of staged wound care approaches in chronic and traumatic wounds also contributes to accelerated growth in this segment.

- By Anatomical Structure

On the basis of anatomical structure, the market is segmented into cellular and acellular skin substitutes. The cellular segment dominated the market in 2025 due to its ability to promote faster tissue regeneration, enhanced vascularization, and reduced scarring. Cellular substitutes, containing viable fibroblasts, keratinocytes, or stem cells, are highly effective in burn cases and chronic wound management, providing both structural and functional benefits. Hospitals and specialized wound care centers prefer cellular grafts for their superior clinical outcomes and compatibility with advanced regenerative protocols. The segment also benefits from increasing research in stem cell-based skin regeneration therapies.

The acellular segment is projected to witness the fastest growth during the forecast period, driven by its cost-effectiveness and broad applicability across chronic wounds, diabetic foot ulcers, and traumatic injuries. Acellular grafts act as temporary scaffolds, facilitating host cell migration and tissue remodeling. Their ease of storage, lower regulatory hurdles compared to cellular substitutes, and minimal risk of immune rejection contribute to rapid adoption. Emerging markets are increasingly utilizing acellular options due to affordability and scalability in hospital and outpatient settings.

- By Biomaterial

On the basis of biomaterial, the market is segmented into autologous, allogeneic, xenogeneic, and others. The allogeneic segment dominated the market with a market share of 42.7% in 2025, driven by its ready availability, scalability, and proven clinical efficacy in wound healing and burn care. Allogeneic grafts, sourced from donor tissue, are widely adopted in hospitals and specialized care centers for emergency cases, large-area wounds, and chronic ulcers. The segment benefits from advances in tissue preservation, immunomodulation, and storage techniques that enhance graft survival and clinical outcomes. Hospitals favor allogeneic substitutes for their ability to provide consistent quality and reduce reliance on patient-derived tissue. In addition, strong collaborations between biotech companies and tissue banks have expanded access, further reinforcing market leadership.

The autologous segment is expected to witness the fastest CAGR during 2026–2033, fueled by rising demand for patient-specific regenerative therapies and lower risk of immune rejection. Autologous substitutes, derived from the patient’s own cells, are increasingly preferred in personalized medicine approaches, especially for burns, chronic wounds, and diabetic ulcers. Technological innovations in harvesting, expansion, and delivery methods are enhancing the feasibility and efficiency of autologous grafts. Growing awareness among clinicians and patients about the advantages of personalized skin substitutes is further driving adoption. Emerging markets are witnessing increasing use of autologous products due to improved accessibility, reduced complications, and better overall patient outcomes

- By Technology

On the basis of technology, the market is segmented into laser-assisted bioprinting, 3D bioprinting, robotic technology, and others. The 3D bioprinting segment dominated the market in 2025, driven by precise layering of cells and biomaterials, enabling production of skin substitutes that closely mimic native tissue architecture. 3D bioprinting allows customization for patient-specific wound dimensions and tissue composition, making it highly suitable for burn centers and regenerative medicine applications. Hospitals are increasingly adopting 3D bioprinted grafts due to improved healing rates, reduced scar formation, and enhanced vascularization. The technology also supports research into complex wound models and personalized therapeutics, sustaining market dominance.

The laser-assisted bioprinting segment is expected to witness the fastest growth rate during 2026–2033, fueled by its ability to deposit cells and biomaterials with high precision and minimal cell damage. Laser-assisted methods enable development of complex, multi-layered skin constructs for chronic wounds and diabetic foot ulcers. Its application in research and clinical trials is accelerating adoption, particularly in advanced healthcare facilities. The segment benefits from ongoing innovation in laser-assisted printing and growing interest in tissue engineering startups focusing on precision wound care solutions.

- By Application

On the basis of application, the market is segmented into chronic wounds, burns, traumatic wounds, diabetic foot ulcers, and others. The burns segment dominated the market in 2025 due to high prevalence of burn injuries and urgent need for effective wound coverage. Burn centers and hospitals prioritize tissue engineered skin substitutes for their ability to accelerate healing, reduce infection risk, and improve functional outcomes. Demand is driven by advancements in both autologous and allogeneic grafts that provide durable and biologically active coverage. Clinical success in severe burn cases further reinforces market leadership.

The diabetic foot ulcers segment is expected to witness the fastest growth rate during 2026–2033, fueled by increasing prevalence of diabetes and associated chronic wounds worldwide. Tissue engineered substitutes for diabetic ulcers reduce hospitalization time, promote faster healing, and lower amputation risk. Emerging markets with rising diabetic populations are driving adoption. In addition, reimbursement initiatives and awareness campaigns by healthcare providers further support segment growth.

- By End-Users

On the basis of end-users, the market is segmented into hospitals and other healthcare facilities. The hospitals segment dominated the market in 2025, driven by high adoption of advanced wound care solutions and access to specialized burn and chronic wound care units. Hospitals benefit from established supply chains, trained personnel, and infrastructure to handle tissue engineered skin substitutes. Clinical preference for reliable, high-efficacy grafts reinforces segment dominance. Strong partnerships with biotech companies for product trials and integration of novel therapies further support leadership in the hospital segment.

The other healthcare facilities segment (clinics, outpatient centers, and home care providers) is expected to witness the fastest growth during 2026–2033, fueled by the rising trend of outpatient wound management and home-based care. Portable and ready-to-use skin substitutes make it feasible for smaller healthcare facilities to adopt advanced wound care products. Growth is also supported by telemedicine integration and rising awareness of regenerative therapies. Cost-effectiveness and ease of application further accelerate adoption in this segment.

- By Type

On the basis of type, the market is segmented into synthetic, biosynthetic, biological, allograft, xenograft, acellular, acellular based on amniotic membrane, cellular, cellular based on amniotic membrane, and others. The biological skin substitutes segment dominated the market in 2025, driven by their superior clinical performance, biocompatibility, and ability to promote tissue regeneration. Biological grafts are widely used in burn care, chronic wounds, and traumatic injuries, and are preferred by hospitals due to their predictable outcomes and reduced risk of infection. Advancements in processing and preservation have further enhanced their adoption.

The acellular skin substitutes segment is expected to witness the fastest growth rate during 2026–2033, fueled by lower cost, wide applicability, and minimal immunogenicity. Acellular substitutes are suitable for chronic wounds, diabetic foot ulcers, and temporary wound coverage. Easy storage, longer shelf life, and regulatory simplicity make them increasingly popular across emerging and developed markets. Rising demand for scalable and off-the-shelf wound care products further drives segment expansion.

Tissue Engineered Skin Substitute Market Regional Analysis

- North America dominated the tissue engineered skin substitute market with the largest revenue share of 40.9% in 2025, characterized by advanced healthcare infrastructure, high awareness of regenerative medicine, and strong presence of key industry players

- Healthcare providers in the region highly value the clinical efficacy, faster healing rates, and reduced risk of complications offered by tissue engineered skin substitutes, particularly in hospitals and specialized burn centers

- This widespread adoption is further supported by well-established healthcare infrastructure, high healthcare expenditure, advanced research and development in tissue engineering, and strong presence of key industry players, establishing tissue engineered skin substitutes as a preferred treatment option for both acute and chronic wound management in North America

U.S. Tissue Engineered Skin Substitute Market Insight

The U.S. tissue engineered skin substitutes market captured the largest revenue share of 40% in 2025 within North America, fueled by the rising prevalence of chronic wounds, diabetic ulcers, and burn injuries. Hospitals and specialized burn centers are increasingly adopting advanced skin substitutes to improve healing outcomes and reduce complications. The growing focus on regenerative medicine, coupled with high healthcare expenditure and well-established reimbursement frameworks, further propels market growth. Moreover, innovations in autologous and allogeneic grafts, combined with the integration of 3D bioprinting and stem cell-based therapies, are significantly contributing to the expansion of the U.S. market.

Europe Tissue Engineered Skin Substitutes Market Insight

The Europe tissue engineered skin substitutes market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by increased awareness of regenerative medicine and rising incidences of chronic wounds and burns. Stringent healthcare regulations, supportive reimbursement policies, and strong R&D investments are fostering market adoption. European hospitals and outpatient care facilities are leveraging advanced skin substitutes for both new treatments and post-surgical wound management. The region is witnessing growth across both public and private healthcare systems, with substitutes increasingly incorporated into clinical protocols for burns, traumatic wounds, and diabetic ulcers.

U.K. Tissue Engineered Skin Substitutes Market Insight

The U.K. tissue engineered skin substitutes market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by the rising focus on improving wound care outcomes and reducing hospitalization times. Chronic wounds and burns are significant concerns, encouraging healthcare providers to adopt advanced skin substitutes. In addition, the U.K.’s strong healthcare infrastructure, awareness campaigns for regenerative therapies, and emphasis on clinical efficacy are expected to continue stimulating market growth. Hospitals, specialized wound care centers, and outpatient clinics are all contributing to the increasing adoption of tissue engineered skin substitutes.

Germany Tissue Engineered Skin Substitutes Market Insight

The Germany market is expected to expand at a considerable CAGR during the forecast period, fueled by rising chronic wound prevalence, technological advancements in biomaterials, and growing awareness of regenerative medicine. Hospitals and burn centers in Germany are increasingly integrating skin substitutes with advanced wound care protocols to enhance patient recovery. The country’s strong focus on innovation, research, and high-quality healthcare services promotes adoption of both autologous and allogeneic grafts. In addition, initiatives to improve post-surgical wound management and reduce infection rates are supporting market growth.

Asia-Pacific Tissue Engineered Skin Substitutes Market Insight

The Asia-Pacific market is poised to grow at the fastest CAGR during the forecast period of 2026 to 2033, driven by increasing burn and chronic wound cases, rapid urbanization, and rising healthcare investments in countries such as China, Japan, and India. Expanding awareness of advanced wound care solutions, coupled with improving access to modern hospitals and clinics, is fueling adoption. Moreover, emerging healthcare infrastructure and government support for regenerative medicine initiatives are enabling the availability of tissue engineered skin substitutes across both urban and semi-urban regions.

Japan Tissue Engineered Skin Substitutes Market Insight

The Japan market is gaining momentum due to the country’s advanced healthcare infrastructure, technological expertise, and focus on regenerative medicine. Hospitals and wound care centers prioritize tissue engineered skin substitutes to improve healing outcomes in chronic wounds and burns. The aging population is further driving demand for effective and easy-to-use solutions. Integration with digital health tools, such as remote monitoring and wound assessment systems, is also fueling growth. Japan continues to lead in clinical research and adoption of cutting-edge skin regeneration technologies.

India Tissue Engineered Skin Substitutes Market Insight

The India market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to rising prevalence of chronic wounds, diabetic ulcers, and burn injuries, along with expanding healthcare infrastructure. Hospitals and specialty wound care centers are increasingly adopting tissue engineered skin substitutes due to improved clinical outcomes and reduced healing times. Government initiatives promoting advanced wound care, growing awareness among clinicians, and the presence of domestic manufacturers offering cost-effective solutions are key factors driving market expansion. Rapid urbanization and the rise of private healthcare facilities further accelerate adoption across the country.

Tissue Engineered Skin Substitute Market Share

The Tissue Engineered Skin Substitute industry is primarily led by well-established companies, including:

- Organogenesis Holdings Inc. (U.S.)

- Smith+Nephew (U.K.)

- Integra LifeSciences Corporation (U.S.)

- LifeNet Health Inc. (U.S.)

- AlloSource Inc. (U.S.)

- MiMedx Group Inc (U.S.)

- Mölnlycke Health Care AB (Sweden)

- Aroa Biosurgery Limited (New Zealand)

- Medline Industries Inc. (U.S.)

- Avita Medical (Australia)

- PolarityTE Inc. (U.S.)

- AxoGen Inc. (U.S.)

- Regenicin Inc. (U.S.)

- Tissue Regenix Group plc (U.K.)

- Vericel Corporation (U.S.)

- Avita Medical Ltd (Australia)

- BioTime Inc. (U.S.)

- Cellular Biomedicine Group Inc. (U.S.)

- Sientra Inc. (U.S.)

- Stratatech Corp (U.S.)

What are the Recent Developments in Global Tissue Engineered Skin Substitute Market?

- In December 2025, CUTISS announced the publication of 1‑year follow‑up results from its Phase IIb denovoSkin™ burn trial in eClinicalMedicine (The Lancet Discovery Science), demonstrating higher expansion capacity and improved scar outcomes versus traditional split‑thickness grafts, strengthening clinical validation of personalized skin substitutes

- In September 2025, CUTISS raised CHF 56 million in a Series C funding round and signed a collaboration with a leading European burn center to support Phase 3 trials and scale industrial production of denovoSkin™, enhancing commercialization prospects for engineered skin therapies

- In May 2025, CUTISS completed patient recruitment in its Phase 2 pediatric burns trial evaluating denovoSkin™, advancing clinical evidence for its safety and efficacy in children with severe burns, supporting continued development toward broader wound care applications

- In April 2025, the U.S. Food and Drug Administration (FDA) approved Zevaskyn (prademagene zamikeracel), the first and only autologous cell‑based gene therapy for wounds in adults and pediatric patients with rare Recessive Dystrophic Epidermolysis Bullosa (RDEB), marking a significant milestone in gene‑modified skin wound healing and reducing chronic wound burden

- In February 2025, CUTISS AG reported positive long‑term efficacy and safety results from Phase 2 clinical trials of denovoSkin™, an autologous bio‑engineered dermo‑epidermal skin graft, showing reduced need for donor‑site harvesting and improved scar quality in both reconstructive surgery and burns compared to standard treatments

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.