Global Transcatheter Mitral Valve Repair Devices Market

Market Size in USD Billion

CAGR :

%

USD

1.20 Billion

USD

2.30 Billion

2025

2033

USD

1.20 Billion

USD

2.30 Billion

2025

2033

| 2026 –2033 | |

| USD 1.20 Billion | |

| USD 2.30 Billion | |

| % | |

|

Transcatheter Mitral Valve Repair Devices Market Size

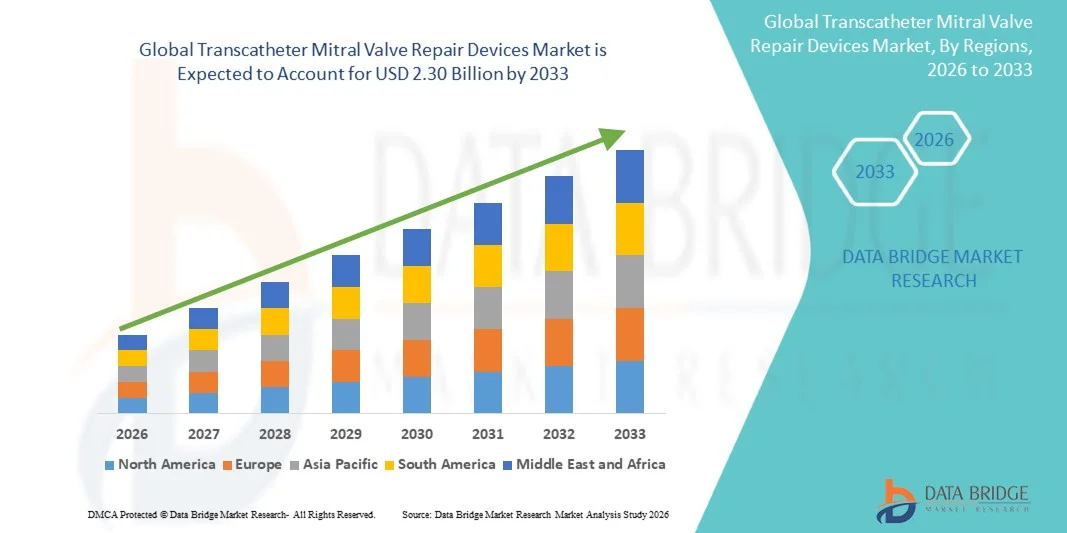

- The global transcatheter mitral valve repair devices market size was valued at USD 1.20 billion in 2025and is expected to reach USD 2.30 billion by 2033, at a CAGR of 8.50% during the forecast period

- The market growth is largely fueled by the rising prevalence of mitral valve regurgitation, increasing geriatric population, and continuous advancements in minimally invasive cardiac procedures, leading to greater adoption of catheter-based structural heart treatment solutions across healthcare settings

- Furthermore, growing demand for safer alternatives to open-heart surgery, increasing awareness regarding early treatment of valvular heart diseases, and expanding availability of advanced transcatheter repair technologies are establishing Transcatheter Mitral Valve Repair Devices solutions as an essential component of modern cardiovascular care. These converging factors are accelerating the uptake of Transcatheter Mitral Valve Repair Devices solutions, thereby significantly boosting the industry's growth

Transcatheter Mitral Valve Repair Devices Market Analysis

- Transcatheter mitral valve repair devices, including edge-to-edge repair systems, annuloplasty devices, and chordal repair technologies, are increasingly vital components of modern structural heart care due to their minimally invasive approach, reduced surgical risk, and improved outcomes for patients with mitral regurgitation

- The escalating demand for transcatheter mitral valve repair devices is primarily fueled by the rising prevalence of valvular heart diseases, growing geriatric population, increasing preference for catheter-based interventions, and continuous technological advancements in image-guided cardiovascular procedures

- North America dominated the Transcatheter Mitral Valve Repair Devices market with the largest revenue share of approximately 46.1% in 2025, characterized by advanced cardiac care infrastructure, strong adoption of minimally invasive heart procedures, favorable reimbursement systems, and presence of leading medical device manufacturers, particularly in the U.S.

- Asia-Pacific is expected to be the fastest growing region in the Transcatheter Mitral Valve Repair Devices market during the forecast period due to rising cardiovascular disease burden, improving hospital infrastructure, increasing healthcare expenditure, growing awareness of structural heart interventions, and expanding access to advanced cardiac technologies across China, Japan, India, and Southeast Asia

- The Dietary Therapy segment accounted for the largest market revenue share of 69.4% in 2025, driven by its role as the lifelong standard of care for most PKU patients

Report Scope and Transcatheter Mitral Valve Repair Devices Market Segmentation

|

Attributes |

Transcatheter Mitral Valve Repair Devices Key Market Insights |

|

Segments Covered |

· By Type: Hyperphenylalaninemia, Mild PKU, Moderate or Variant PKU, and Classic PKU · By Drug Type: Kuvan, Sapropterin, Palynziq, Pagvaliase, Biopten, and Others · By Therapy Type: Gene Therapy and Dietary Therapy · By Route of Administration: Oral, Intravenous, Subcutaneous, and Others · By End User: Hospitals, Homecare, Specialty Clinics, and Others |

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Abbott (U.S.) · Edwards Lifesciences Corporation (U.S.) · Medtronic plc (Ireland) · Boston Scientific Corporation (U.S.) · Johnson & Johnson (U.S.) · Cardioband (Germany) · NeoChord, Inc. (U.S.) · HighLife SAS (France) · Micro Interventional Devices, Inc. (U.S.) · Ancora Heart, Inc. (U.S.) · Venus Medtech (China) · JenaValve Technology, Inc. (Germany) · Colibri Heart Valve LLC (U.S.) · Peijia Medical Limited (China) · Meril Life Sciences Pvt. Ltd. (India) · Lepu Medical Technology Co., Ltd. (China) · Artivion, Inc. (U.S.) · LivaNova PLC (U.K.) · W. L. Gore & Associates, Inc. (U.S.) · Biotronik SE & Co. KG (Germany) |

|

Market Opportunities |

· Rising Adoption of Minimally Invasive Structural Heart Procedures · Technological Advancements and Untapped Emerging Markets |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Transcatheter Mitral Valve Repair Devices Market Trends

“Rising Adoption of Minimally Invasive Structural Heart Procedures and Advanced Repair Technologies”

- A significant and accelerating trend in the global Transcatheter Mitral Valve Repair Devices market is the increasing adoption of minimally invasive cardiac procedures for the treatment of mitral regurgitation, particularly among elderly and high-surgical-risk patients. These technologies are transforming treatment pathways by offering safer alternatives to open-heart surgery

- For instance, Abbott Laboratories has expanded the global use of its MitraClip system, while Edwards Lifesciences continues advancing transcatheter mitral repair and replacement platforms for complex structural heart disease patients

- Improvements in catheter design, real-time imaging guidance, steerability, and device durability are enhancing procedural precision and expanding the pool of eligible patients worldwide

- Growing preference for shorter hospital stays, faster recovery times, and lower perioperative complications is increasing demand for transcatheter solutions across major healthcare markets

- Hospitals are increasingly establishing dedicated structural heart programs that combine cardiologists, cardiac surgeons, and imaging specialists to optimize patient outcomes and streamline treatment selection

- The trend toward less invasive cardiovascular care, supported by clinical evidence and technological innovation, is reshaping the Transcatheter Mitral Valve Repair Devices market globally

Transcatheter Mitral Valve Repair Devices Market Dynamics

Driver

“Increasing Prevalence of Mitral Valve Disease and Expanding High-Risk Patient Population”

- The growing global prevalence of mitral regurgitation, heart failure, degenerative valve disease, and age-related cardiac disorders is a major driver for the Transcatheter Mitral Valve Repair Devices market. Rising life expectancy is increasing the number of patients requiring valve intervention

- For instance, American College of Cardiology and European Society of Cardiology have supported guideline-based use of transcatheter mitral repair in selected symptomatic patients who are unsuitable for conventional surgery

- Many elderly patients or those with multiple comorbidities are considered poor candidates for open surgery, making catheter-based repair a preferred therapeutic option

- Increasing diagnosis rates through echocardiography, cardiac imaging, and routine cardiovascular screening are enabling earlier identification of treatable valve disorders

- Expanding healthcare infrastructure and growing availability of specialized cardiac centers in Asia-Pacific, Latin America, and the Middle East are further supporting market growth

- In addition, favorable clinical outcomes such as symptom relief, improved quality of life, and reduced heart failure hospitalizations are encouraging wider physician adoption

Restraint/Challenge

“High Procedure Costs, Limited Specialist Availability, and Complex Patient Selection”

- High procedural costs associated with transcatheter mitral valve repair devices, imaging systems, hybrid operating rooms, and specialist teams remain a significant barrier to broader adoption, particularly in cost-sensitive healthcare markets

- For instance, several hospitals in developing economies face budget constraints that limit access to premium structural heart devices such as MitraClip and other next-generation repair systems

- The procedure requires highly trained interventional cardiologists, imaging experts, and multidisciplinary heart teams, which are not uniformly available across all regions

- Complex anatomical variations in mitral valve disease can make some patients unsuitable for currently available repair technologies, restricting total addressable demand

- Reimbursement limitations and lengthy regulatory approval timelines in certain countries may delay commercial expansion and hospital purchasing decisions

- Overcoming these challenges through cost optimization, physician training programs, broader reimbursement support, and continued device innovation will be essential for sustained market growth

Transcatheter Mitral Valve Repair Devices Market Scope

The market is segmented on the basis of type, drugs type, therapy type, route of administration, and end-user.

- By Type

On the basis of type, the Phenylketonuria (PKU) Treatment market is segmented into Hyperphenylalaninemia, Mild PKU, Moderate or Variant, and Classic PKU. The Classic PKU segment dominated the largest market revenue share of 44.8% in 2025, driven by severe phenylalanine hydroxylase deficiency requiring lifelong treatment and strict dietary management. Patients diagnosed with classic PKU need continuous monitoring, specialized low-protein nutrition, and adjunct drug therapy. Universal newborn screening programs are increasing early diagnosis rates globally. Strong demand for medical foods and metabolic supplements reinforces segment leadership. Rising healthcare awareness regarding inherited metabolic disorders supports treatment adoption. Expanding reimbursement policies in developed economies further strengthen market growth. Long-term disease burden contributes to sustained revenue generation.

The Moderate or Variant PKU segment is expected to witness the fastest growth rate of 23.2% from 2026 to 2033, driven by improved disease stratification and rising use of personalized treatment approaches. Many patients in this segment respond favorably to cofactor-based therapies such as sapropterin. Increasing physician awareness of genotype-guided treatment supports growth. Expanding access to advanced diagnostic tools is accelerating detection rates. Rising demand for flexible dietary and pharmacological solutions further boosts adoption. Greater focus on quality-of-life improvements enhances segment momentum. Ongoing innovation in metabolic disorder management continues to support expansion.

- By Drugs Type

On the basis of drugs type, the Phenylketonuria (PKU) Treatment market is segmented into Kuvan, Sapropterin, Palynziq, Pagvaliase, and Biopten. The Kuvan segment held the largest market revenue share of 37.1% in 2025, driven by its strong clinical adoption for BH4-responsive PKU patients. It helps lower blood phenylalanine levels and reduces dependence on strict dietary restrictions in eligible patients. Oral administration convenience and proven safety profile support widespread use. Strong brand recognition among metabolic specialists reinforces demand. Regulatory approvals across major markets further strengthen segment dominance. Growing patient adherence due to ease of dosing supports continued revenue growth.

The Palynziq segment is expected to witness the fastest CAGR of 25.6% from 2026 to 2033, driven by increasing use in adult PKU patients with uncontrolled phenylalanine despite conventional treatment. It provides an enzyme substitution approach for difficult-to-manage cases. Rising demand for effective long-term biochemical control is accelerating uptake. Expanding specialist metabolic centers are improving patient access. Improved outcomes with reduced dietary burden support adoption. Increasing awareness of advanced biologic therapies strengthens growth. Continued expansion into new markets further drives segment momentum.

- By Therapy Type

On the basis of therapy type, the Phenylketonuria (PKU) Treatment market is segmented into Gene Therapy and Dietary Therapy. The Dietary Therapy segment accounted for the largest market revenue share of 69.4% in 2025, driven by its role as the lifelong standard of care for most PKU patients. Low-phenylalanine diets, amino acid supplements, and specialized medical foods remain essential from infancy through adulthood. Early nutritional intervention prevents neurological complications and cognitive impairment. Strong physician recommendation supports continued reliance on this therapy. Broad availability of therapeutic nutritional products reinforces leadership. Growing newborn screening programs continue to expand the treated population base.

The Gene Therapy segment is expected to witness the fastest growth rate of 27.8% from 2026 to 2033, driven by rising investment in potentially curative treatments targeting the root cause of PKU. Biotechnology companies are advancing viral vector and gene-editing platforms for durable correction. Increasing clinical trial progress is boosting market confidence. Demand for one-time treatment alternatives to lifelong diet management supports growth. Rare disease funding initiatives further accelerate research activities. Strong future commercialization prospects continue to drive rapid expansion.

- By Route of Administration

On the basis of route of administration, the Phenylketonuria (PKU) Treatment market is segmented into Oral, Intravenous, Subcutaneous, and Others. The Oral segment dominated the largest market revenue share of 53.3% in 2025, driven by strong usage of oral drugs, nutritional supplements, and medical foods in daily PKU management. Oral therapies are convenient, non-invasive, and suitable for long-term adherence across pediatric and adult patients. Widespread use of sapropterin-based treatment further supports dominance. Home-based administration improves compliance and continuity of care. Availability of patient-friendly formulations boosts acceptance. Strong physician preference for first-line oral management reinforces leadership.

The Subcutaneous segment is expected to witness the fastest CAGR of 24.4% from 2026 to 2033, driven by increasing use of injectable biologic therapies such as pegvaliase. These therapies are highly valuable for patients with persistent elevated phenylalanine levels. Rising demand for advanced treatment options is accelerating growth. Better self-injection training programs are supporting adoption. Expansion of specialty metabolic clinics enhances accessibility. Growing patient acceptance of biologics in rare diseases boosts uptake. Continued innovation in drug delivery devices supports segment growth.

- By End-User

On the basis of end-user, the Phenylketonuria (PKU) Treatment market is segmented into Hospitals, Homecare, Specialty Clinics, and Others. The Homecare segment held the largest market revenue share of 40.2% in 2025, driven by the chronic nature of PKU management requiring daily nutritional therapy and regular medication outside hospital settings. Most patients manage low-protein diets, supplements, and oral therapies at home for extended periods. Rising preference for convenient long-term care supports leadership. Strong parental involvement in pediatric PKU treatment boosts demand. Telehealth nutrition counseling services further strengthen homecare adoption. Lower treatment costs compared with repeated hospital visits support segment dominance.

The Specialty Clinics segment is expected to witness the fastest CAGR of 23.9% from 2026 to 2033, driven by increasing establishment of metabolic disorder centers offering personalized PKU care. These clinics provide expert monitoring, dietary counseling, advanced diagnostics, and access to innovative therapies. Growing awareness of specialized rare disease treatment is supporting demand. Expansion of multidisciplinary care models accelerates adoption. Improved outcomes through expert disease management strengthen growth. Rising referrals from hospitals and pediatricians further boost volumes. Continuous rare disease infrastructure development supports rapid expansion.

Transcatheter Mitral Valve Repair Devices Market Regional Analysis

- North America dominated the transcatheter mitral valve repair devices market with the largest revenue share of approximately 46.1% in 2025, characterized by advanced cardiac care infrastructure, strong adoption of minimally invasive heart procedures, favorable reimbursement systems, and the presence of leading medical device manufacturers, particularly in the U.S. The region has also witnessed increasing preference for catheter-based mitral valve repair procedures among high-risk and elderly patients unsuitable for open-heart surgery

- Cardiologists and healthcare providers in the region highly value the reduced procedural risk, shorter recovery time, improved quality of life, and clinical efficacy offered by transcatheter mitral valve repair devices. Growing preference for minimally invasive structural heart interventions continues to strengthen market demand

- This widespread adoption is further supported by high healthcare expenditure, advanced hospital networks, strong clinical expertise in interventional cardiology, and increasing prevalence of mitral regurgitation, establishing transcatheter mitral valve repair devices as a preferred treatment solution in leading cardiac centers

U.S. Transcatheter Mitral Valve Repair Devices Market Insight

The U.S. transcatheter mitral valve repair devices market captured the largest revenue share in 2025 within North America, fueled by strong adoption of minimally invasive cardiac technologies, favorable reimbursement coverage, and high incidence of structural heart disease. Physicians are increasingly prioritizing transcatheter mitral valve repair for patients at elevated surgical risk and those requiring faster recovery pathways. The growing preference for advanced catheter-based procedures, combined with robust demand across tertiary hospitals, cardiac specialty centers, and academic institutions, further propels the market. Moreover, increasing integration of imaging-guided procedures and multidisciplinary heart team approaches is significantly contributing to market expansion.

Europe Transcatheter Mitral Valve Repair Devices Market Insight

The Europe transcatheter mitral valve repair devices market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by rising prevalence of valvular heart disease, growing elderly population, and increasing adoption of minimally invasive cardiovascular treatments. The region’s strong healthcare systems and established structural heart programs are fostering demand for advanced mitral repair devices. European clinicians are also drawn to the clinical outcomes, reduced hospitalization, and suitability for high-risk patients offered by these procedures. The market is experiencing significant growth across university hospitals, specialty cardiac centers, and public healthcare institutions.

U.K. Transcatheter Mitral Valve Repair Devices Market Insight

The U.K. transcatheter mitral valve repair devices market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by increasing awareness of minimally invasive valve repair options and rising demand for advanced cardiac interventions. In addition, growing NHS focus on reducing surgical burden and improving patient recovery outcomes is encouraging broader adoption. The UK’s expanding structural heart treatment capacity and strong cardiology networks are expected to continue stimulating market growth.

Germany Transcatheter Mitral Valve Repair Devices Market Insight

The Germany transcatheter mitral valve repair devices market is expected to expand at a considerable CAGR during the forecast period, fueled by strong cardiac care infrastructure, increasing prevalence of valvular disease, and demand for technologically advanced treatment solutions. Germany’s well-developed hospital systems and leadership in interventional cardiology promote the adoption of transcatheter mitral valve repair procedures. Integration of advanced imaging systems and hybrid operating rooms is also becoming increasingly prevalent, supporting procedural growth.

Asia-Pacific Transcatheter Mitral Valve Repair Devices Market Insight

The Asia-Pacific transcatheter mitral valve repair devices market is poised to grow at the fastest CAGR during the forecast period of 2026 to 2033, driven by rising cardiovascular disease burden, improving hospital infrastructure, increasing healthcare expenditure, growing awareness of structural heart interventions, and expanding access to advanced cardiac technologies across China, Japan, India, and Southeast Asia. The region’s growing elderly population and rising prevalence of heart valve disorders are accelerating demand. Furthermore, increasing government healthcare investments and expansion of specialized cardiac centers are improving patient access to minimally invasive procedures.

Japan Transcatheter Mitral Valve Repair Devices Market Insight

The Japan transcatheter mitral valve repair devices market gaining momentum due to the country’s aging population, advanced healthcare system, and growing burden of degenerative heart valve disease. Japanese clinicians place significant emphasis on minimally invasive treatment pathways, driving adoption of catheter-based mitral valve repair procedures. Integration of advanced imaging technologies and precision-guided interventions is fueling market growth.

China Transcatheter Mitral Valve Repair Devices Market Insight

The China Transcatheter Mitral Valve Repair Devices market accounted for the largest market revenue share in Asia Pacific in 2025, attributed to the country’s expanding hospital infrastructure, rising cardiovascular disease burden, increasing healthcare expenditure, and growing adoption of advanced interventional cardiology technologies. China is witnessing increasing use of structural heart procedures in major urban hospitals. Government healthcare reforms, domestic innovation in medical devices, and rising access to specialty cardiac care are key factors propelling market growth in China.

Transcatheter Mitral Valve Repair Devices Market Share

The Transcatheter Mitral Valve Repair Devices industry is primarily led by well-established companies, including:

- Abbott (U.S.)

- Edwards Lifesciences Corporation (U.S.)

- Medtronic plc (Ireland)

- Boston Scientific Corporation (U.S.)

- Johnson & Johnson (U.S.)

- Cardioband (Germany)

- NeoChord, Inc. (U.S.)

- HighLife SAS (France)

- Micro Interventional Devices, Inc. (U.S.)

- Ancora Heart, Inc. (U.S.)

- Venus Medtech (China)

- JenaValve Technology, Inc. (Germany)

- Colibri Heart Valve LLC (U.S.)

- Peijia Medical Limited (China)

- Meril Life Sciences Pvt. Ltd. (India)

- Lepu Medical Technology Co., Ltd. (China)

- Artivion, Inc. (U.S.)

- LivaNova PLC (U.K.)

- L. Gore & Associates, Inc. (U.S.)

- Biotronik SE & Co. KG (Germany)

Latest Developments in Global Transcatheter Mitral Valve Repair Devices Market

- In October 2021, Abbott announced new clinical data reinforcing the long-term effectiveness of its MitraClip transcatheter edge-to-edge repair (TEER) system for patients with mitral regurgitation. The results supported sustained symptom improvement, reduced hospitalizations, and continued global adoption of minimally invasive mitral valve repair procedures

- In September 2022, Edwards Lifesciences presented pivotal CLASP IID trial data showing that the PASCAL transcatheter mitral valve repair system was noninferior to Abbott’s MitraClip in patients with degenerative mitral regurgitation who were at prohibitive surgical risk. This marked a major competitive milestone in the transcatheter mitral valve repair devices market

- In October 2023, Edwards Lifesciences announced continued expansion of its PASCAL Precision platform in international markets, featuring enhanced steering control and broader implant options for complex mitral anatomies. The development strengthened competition in next-generation TEER devices

- In January 2024, healthcare providers worldwide increased adoption of transcatheter mitral valve repair procedures due to rising preference for minimally invasive therapies among elderly and high-risk surgical patients. Market demand was further supported by growing heart valve disease prevalence and shorter recovery times versus open surgery

- In May 2024, Abbott highlighted that more than 200,000 patients worldwide had been treated with MitraClip, underscoring the device’s position as the most widely used transcatheter mitral valve repair therapy globally. This milestone reflected strong physician confidence and mature commercial penetration

- In May 2025, Abbott received U.S. FDA approval for the Tendyne transcatheter mitral valve replacement system for patients with severe mitral annular calcification who were unsuitable for surgery or transcatheter repair. Although a replacement device, the approval expanded Abbott’s structural heart portfolio adjacent to the mitral repair segment

- In July 2025, industry market analyses estimated that transcatheter mitral valve repair devices accounted for the largest share of the broader transcatheter mitral valve market, driven by lower procedural risk, expanding reimbursement support, and strong clinical acceptance in treating mitral regurgitation

- In October 2025, Abbott showcased next-generation MitraClip and mitral therapy innovations at TCT 2025, emphasizing broader treatment pathways across mitral and tricuspid structural heart disease. This reflected continued investment in catheter-based valve repair technologies

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.