Global Tubeless Insulin Pumps Market

Market Size in USD Billion

CAGR :

%

USD

3.04 Billion

USD

17.12 Billion

2025

2033

USD

3.04 Billion

USD

17.12 Billion

2025

2033

| 2026 –2033 | |

| USD 3.04 Billion | |

| USD 17.12 Billion | |

| % | |

|

Tubeless Insulin Pump Market Size

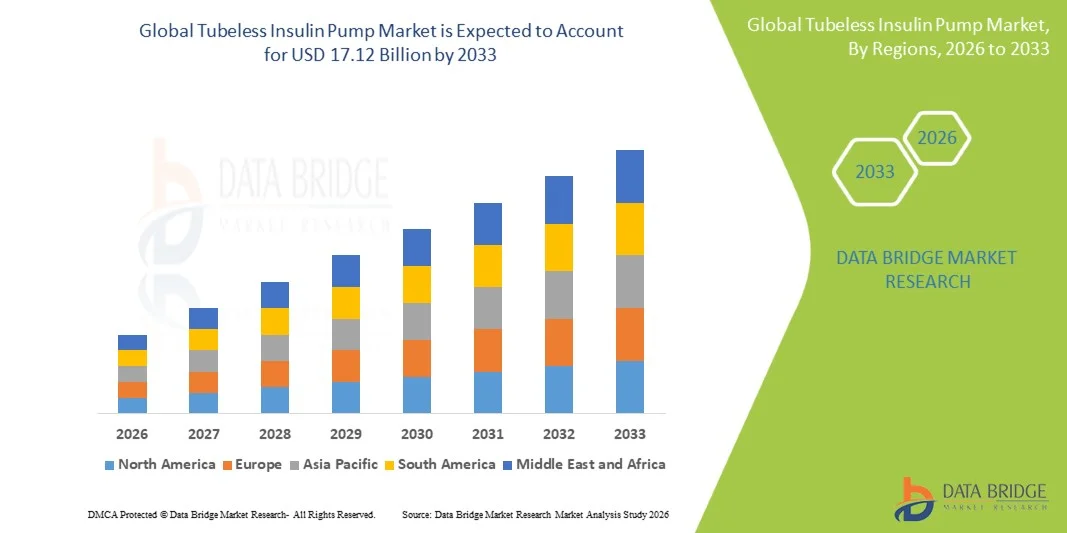

- The global tubeless insulin pump market size was valued at USD 3.04 billion in 2025and is expected to reach USD 17.12 billion by 2033, at a CAGR of 24.12% during the forecast period

- The market growth is primarily driven by the rising prevalence of diabetes globally, coupled with increasing adoption of advanced insulin delivery technologies that improve glycemic control and reduce the burden of multiple daily injections

- Furthermore, growing patient preference for discreet, wearable, and automated drug delivery systems, along with continuous innovations in patch-based and connected insulin pump devices, is positioning tubeless insulin pumps as a preferred solution in diabetes management, thereby significantly accelerating market expansion

Tubeless Insulin Pump Market Analysis

- Tubeless insulin pumps, which deliver continuous subcutaneous insulin through discreet, patch-based wearable devices without traditional tubing, are becoming increasingly important in diabetes management due to their improved mobility, enhanced comfort, and integration with digital glucose monitoring systems

- The growing demand for tubeless insulin pumps is primarily driven by the rising global burden of diabetes, increasing preference for minimally invasive and automated insulin delivery solutions, and advancements in closed-loop and smartphone-connected diabetes management technologies

- North America dominated the tubeless insulin pump market with the largest revenue share of 42.6% in 2025, supported by high diabetes prevalence, strong healthcare spending, and rapid adoption of advanced diabetes technologies, with the U.S. leading due to widespread use of wearable insulin delivery systems and continuous innovation by major medical device manufacturers

- Asia-Pacific is expected to be the fastest growing region in the tubeless insulin pump market during the forecast period due to rising diabetes incidence, improving healthcare infrastructure, growing awareness of advanced insulin therapies, and increasing affordability of next-generation wearable medical devices

- Pod/Patch segment dominated the market with a share of 46.8% in 2025, driven by its ease of use, discreet design, and strong patient preference for tubeless, wearable systems that offer greater lifestyle flexibility and improved adherence to insulin therapy

Report Scope and Tubeless Insulin Pump Market Segmentation

|

Attributes |

Tubeless Insulin Pump Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

|

|

Market Opportunities |

· Integration of tubeless insulin pumps with AI-driven predictive glucose analytics and closed-loop “artificial pancreas” systems · Expansion into emerging markets through cost-reduced, subscription-based or reimbursement-supported wearable insulin delivery models |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Tubeless Insulin Pump Market Trends

“Integration of Smart Connectivity and Automated Insulin Delivery Systems”

- A significant and accelerating trend in the global tubeless insulin pump market is the integration of wearable patch pumps with continuous glucose monitoring (CGM) systems and smartphone-based digital health platforms, enabling real-time insulin adjustments and improved glycemic control in diabetes management

- For instance, the Omnipod 5 system integrates with Dexcom CGM to automate insulin delivery based on glucose readings, reducing the need for manual intervention and improving patient convenience and outcomes

- Advanced connectivity in tubeless insulin pumps enables features such as automated insulin dosing algorithms, predictive glucose trend alerts, and cloud-based data sharing with healthcare providers for remote monitoring and therapy optimization

- The seamless integration of tubeless insulin pumps with mobile applications and digital ecosystems allows users to track insulin usage, monitor glucose trends, and receive personalized therapy insights through a unified digital interface

- This trend toward highly automated, connected, and data-driven insulin delivery solutions is reshaping expectations in diabetes care, with companies such as Insulet Corporation advancing AI-enabled algorithms and interoperable patch pump systems

- The demand for connected tubeless insulin pumps is growing rapidly across both Type 1 and insulin-dependent Type 2 diabetes populations, as patients increasingly prioritize precision, automation, and lifestyle flexibility in diabetes management

- Furthermore, increasing collaboration between insulin pump manufacturers and digital health companies is accelerating the creation of integrated diabetes management ecosystems combining hardware, software, and analytics

Tubeless Insulin Pump Market Dynamics

Driver

“Rising Diabetes Burden and Shift Toward Automated Insulin Therapy”

- The increasing prevalence of diabetes globally, coupled with the growing clinical need for improved long-term glycemic control, is a major driver accelerating the adoption of tubeless insulin pump systems

- For instance, in March 2025, Insulet Corporation expanded its Omnipod platform in multiple international markets, focusing on increasing access to automated tubeless insulin delivery for Type 1 and insulin-dependent Type 2 diabetes patients

- As patients and healthcare providers seek better alternatives to multiple daily injections, tubeless insulin pumps offer precise, continuous insulin delivery that improves adherence and reduces hypoglycemia risks

- Furthermore, the rising shift toward outpatient and home-based diabetes management is driving demand for user-friendly wearable devices that enable independent and flexible insulin therapy without hospital dependency

- The convenience of patch-based insulin delivery, reduced tubing complications, and compatibility with digital glucose monitoring systems are key factors propelling adoption across pediatric and adult diabetic populations

- In addition, increasing physician preference for data-driven insulin titration supported by connected devices is strengthening clinical adoption of tubeless insulin pump technologies

- Moreover, growing awareness campaigns by healthcare organizations regarding early insulin intensification in diabetes care are further supporting market expansion

Restraint/Challenge

“High Device Cost and Limited Reimbursement Coverage Barriers”

- Concerns related to the high cost of tubeless insulin pump systems and limited reimbursement coverage in several regions pose a significant challenge to widespread market adoption

- For instance, in many developing healthcare systems, patients face financial barriers as advanced patch pump systems and associated consumables remain significantly more expensive than conventional insulin delivery methods

- Addressing affordability challenges through expanded insurance coverage, government reimbursement programs, and cost-effective manufacturing strategies is crucial for improving accessibility and adoption rates

- In addition, limited awareness and insufficient training among patients and healthcare providers regarding the proper use of tubeless insulin pump technology further restrict market penetration in emerging economies

- While companies such as Insulet Corporation and Medtronic are expanding patient support programs, the perceived high recurring cost of consumables continues to hinder large-scale adoption among price-sensitive populations

- Furthermore, stringent regulatory approval processes for advanced closed-loop insulin delivery systems can delay product launches and slow down market expansion

- In addition, concerns regarding device reliability, skin adhesion issues, and pump failure risks in real-world usage conditions also act as barriers to consistent long-term adoption

Tubeless Insulin Pump Market Scope

The market is segmented on the basis of type, component, and distribution channel.

- By Type

On the basis of type, the tubeless insulin pump market is segmented into insulin patch pump and traditional pump. The insulin patch pump segment dominated the market with the largest revenue share of 72.4% in 2025, driven by its tubeless, wearable design that enhances patient comfort and supports discreet insulin delivery without external tubing. Patients increasingly prefer patch pumps due to their ease of use, improved mobility, and ability to integrate with continuous glucose monitoring systems for automated insulin delivery. The growing adoption of advanced systems such as Omnipod has strengthened the dominance of this segment in both Type 1 and insulin-dependent Type 2 diabetes management. Furthermore, rising demand for minimally invasive and lifestyle-friendly diabetes care solutions is significantly boosting patch pump utilization. Healthcare providers also favor patch pumps due to improved adherence rates and better glycemic control outcomes. In addition, continuous innovation in adhesive technology and extended wear duration is further consolidating its leading market position.

The traditional pump segment is expected to witness the fastest growth rate of 18.9% from 2026 to 2033, driven by its continued clinical use in complex diabetes cases requiring highly customizable insulin dosing. Despite being less discreet, traditional pumps offer advanced programming flexibility and are often preferred in hospital-managed diabetes care settings. Increasing adoption in developing healthcare systems, where cost-effective insulin delivery options remain important, is supporting segment growth. Moreover, technological upgrades such as improved interface design and partial integration with digital monitoring systems are enhancing usability. The segment is also benefiting from physician familiarity and long-standing clinical trust in conventional pump therapy. Furthermore, gradual incorporation of hybrid closed-loop features is improving its relevance in modern diabetes management.

- By Component

On the basis of component, the tubeless insulin pump market is segmented into pod/patch, remote, and accessories. The pod/patch segment dominated the market with the largest revenue share of 46.8% in 2025, driven by its critical role as the primary insulin delivery unit in tubeless pump systems. The patch component directly enables continuous subcutaneous insulin infusion, making it essential for system functionality and patient adoption. Rising demand for disposable, easy-to-replace pods with improved adhesive performance is strengthening segment dominance. Furthermore, innovations in miniaturization and extended wear duration are enhancing patient convenience and reducing replacement frequency. Integration of pods with automated insulin dosing algorithms and CGM systems is further improving clinical outcomes. Increasing preference for all-in-one wearable solutions is also significantly contributing to its leading market position.

The remote segment is expected to witness the fastest growth rate of 21.3% from 2026 to 2033, driven by rising demand for smartphone-based and handheld controllers that enable precise insulin dosing adjustments. Remote devices enhance user control by allowing real-time monitoring, dose customization, and alerts without direct pump interaction. Growing adoption of mobile app-based diabetes management platforms is further accelerating this segment. In addition, advancements in wireless connectivity and Bluetooth-enabled control systems are improving usability and responsiveness. Patients increasingly prefer remote interfaces for their convenience, especially in pediatric and elderly populations. Moreover, integration with digital health ecosystems and AI-based recommendations is significantly boosting adoption rates.

- By Distribution Channel

On the basis of distribution channel, the tubeless insulin pump market is segmented into hospitals, pharmacies, and e-commerce. The hospitals segment dominated the market with the largest revenue share of 55.6% in 2025, driven by the high rate of initial insulin pump adoption through clinical diagnosis and physician-guided therapy initiation. Hospitals play a key role in prescribing and training patients on tubeless insulin pump usage, ensuring proper device handling and dosing accuracy. Increasing hospitalization rates for diabetes-related complications are also supporting segment dominance. Furthermore, strong reimbursement frameworks in developed healthcare systems favor hospital-based procurement and distribution. Hospitals also act as primary centers for transitioning patients from injection therapy to advanced pump systems. In addition, the presence of endocrinology specialists and structured diabetes education programs further strengthens hospital dominance in this segment.

The e-commerce segment is expected to witness the fastest growth rate of 24.5% from 2026 to 2033, driven by increasing digitalization of healthcare purchasing and rising consumer preference for online medical device procurement. Patients are increasingly opting for online platforms due to convenience, wider product availability, and competitive pricing. The expansion of telemedicine and digital prescription services is further supporting online distribution. In addition, growing awareness of diabetes management devices through digital health platforms is boosting online adoption. Direct-to-consumer delivery models and subscription-based supply systems are also gaining traction. Furthermore, improved logistics and secure medical e-commerce regulations are enhancing trust and accelerating segment growth.

Tubeless Insulin Pump Market Regional Analysis

- North America dominated the tubeless insulin pump market with the largest revenue share of 42.6% in 2025, supported by high diabetes prevalence, strong healthcare spending, and rapid adoption of advanced diabetes technologies

- Consumers and healthcare providers in the region highly value the clinical benefits of tubeless insulin pumps, including automated insulin delivery, improved glycemic control, and seamless integration with continuous glucose monitoring systems

- This widespread adoption is further supported by strong reimbursement frameworks, high awareness of diabetes management solutions, and the presence of leading medical device companies such as Insulet Corporation, establishing tubeless insulin pumps as a standard of care in advanced diabetes therapy

U.S. Tubeless Insulin Pump Market Insight

The U.S. tubeless insulin pump market captured the largest revenue share of 78% in 2025 within North America, driven by high diabetes prevalence, strong healthcare spending, and rapid adoption of advanced wearable insulin delivery systems. Patients in the country increasingly prioritize automated, discreet, and connected insulin management solutions that improve glycemic control and reduce daily injection burden. The growing preference for integrated digital health ecosystems, combined with strong physician adoption of continuous glucose monitoring-linked insulin pumps, further propels market growth. Moreover, the presence of leading players such as Insulet Corporation and advanced reimbursement coverage significantly contributes to widespread adoption across both Type 1 and insulin-dependent Type 2 diabetes populations.

Europe Tubeless Insulin Pump Market Insight

The Europe tubeless insulin pump market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by rising diabetes incidence, strong public healthcare systems, and increasing adoption of advanced insulin delivery technologies. The demand for minimally invasive and automated diabetes management solutions is fostering the adoption of tubeless insulin pumps across hospitals and homecare settings. European patients are also increasingly drawn to the convenience, improved safety, and better quality-of-life outcomes offered by patch-based pump systems. Furthermore, growing integration of digital health platforms and supportive regulatory frameworks for medical devices are accelerating market penetration across major European countries.

U.K. Tubeless Insulin Pump Market Insight

The U.K. tubeless insulin pump market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by increasing diabetes burden and rising demand for advanced, user-friendly insulin delivery solutions. Growing awareness of automated insulin therapy and strong preference for wearable diabetes management devices are encouraging adoption among both pediatric and adult populations. The NHS support for diabetes care and gradual inclusion of advanced insulin pump technologies are further supporting market expansion. In addition, increasing focus on remote patient monitoring and digital diabetes management is strengthening the integration of tubeless insulin pumps into routine care pathways.

Germany Tubeless Insulin Pump Market Insight

The Germany tubeless insulin pump market is expected to expand at a considerable CAGR during the forecast period, fueled by high healthcare standards, strong adoption of digital medical technologies, and increasing diabetes prevalence. German patients and healthcare providers emphasize precision, safety, and long-term glycemic control, which supports the shift toward advanced patch-based insulin delivery systems. The country’s well-established healthcare infrastructure and reimbursement support for chronic disease management are also promoting adoption. Moreover, increasing integration of tubeless insulin pumps with CGM systems and hospital diabetes care programs is further strengthening market growth.

Asia-Pacific Tubeless Insulin Pump Market Insight

The Asia-Pacific tubeless insulin pump market is poised to grow at the fastest CAGR of 25% during the forecast period of 2026 to 2033, driven by rising diabetes prevalence, rapid urbanization, and improving healthcare infrastructure in countries such as China, Japan, and India. Increasing awareness of advanced diabetes management technologies and growing affordability of wearable medical devices are accelerating adoption across the region. Government initiatives supporting digital healthcare transformation are also boosting market penetration. Furthermore, the region’s expansion as a manufacturing hub for medical devices is improving accessibility and reducing costs of tubeless insulin pump systems.

Japan Tubeless Insulin Pump Market Insight

The Japan tubeless insulin pump market is gaining momentum due to the country’s aging population, high healthcare standards, and strong demand for advanced, minimally invasive diabetes management solutions. Patients increasingly prefer discreet and automated insulin delivery systems that reduce daily management complexity and improve quality of life. The integration of tubeless insulin pumps with continuous glucose monitoring and IoT-based healthcare platforms is further driving adoption. Moreover, Japan’s strong focus on technological innovation in healthcare is supporting the development and uptake of next-generation insulin delivery systems.

India Tubeless Insulin Pump Market Insight

The India tubeless insulin pump market accounted for the largest market revenue share in Asia Pacific in 2025, attributed to the rapidly growing diabetic population, expanding middle class, and increasing adoption of advanced medical technologies. Rising awareness of diabetes management and growing preference for wearable, easy-to-use insulin delivery systems are driving demand. Government initiatives promoting digital healthcare and smart medical infrastructure are further supporting market growth. In addition, increasing availability of cost-effective insulin pump solutions and expanding private healthcare access are enabling broader adoption across urban populations.

Tubeless Insulin Pump Market Share

The Tubeless Insulin Pump industry is primarily led by well-established companies, including:

- Medtronic (Ireland)

- Insulet Corporation (U.S.)

- Tandem Diabetes Care, Inc. (U.S.)

- Abbott (U.S.)

- Ypsomed AG (Switzerland)

- Dexcom, Inc. (U.S.)

- Bigfoot Biomedical, Inc. (U.S.)

- Diabeloop S.A. (France)

- BD (U.S.)

- Novo Nordisk A/S (Denmark)

- Sanofi (France)

- Eli Lilly and Company (U.S.)

- Fresenius Kabi AG (Germany)

- Ascensia Diabetes Care Holdings AG (Switzerland)

- Beta Bionics, Inc. (U.S.)

- SOOIL Development Co., Ltd. (South Korea)

- Cellnovo Group S.A. (France)

- D. Medical Industries Ltd. (Israel)

- Medtrum Technologies Inc. (China)

What are the Recent Developments in Global Tubeless Insulin Pump Market?

- In December 2025, Insulet Corporation announced the FDA clearance of enhanced algorithm updates for its Omnipod 5 tubeless insulin pump system, improving automated insulin delivery precision, expanding glucose target settings, and strengthening integration with continuous glucose monitoring (CGM) systems. This advancement further enhances closed-loop diabetes management and personalized insulin dosing for patients with Type 1 and Type 2 diabetes

- In April 2025, Insulet Corporation launched the Omnipod 5 automated insulin delivery system in Canada, enabling individuals aged two years and older with Type 1 diabetes to access tubeless, wearable insulin therapy. The launch strengthened North America’s leadership in advanced diabetes technologies and expanded access to CGM-integrated insulin automation

- In March 2025, Insulet Corporation expanded its Omnipod 5 tubeless insulin pump system into additional international markets including Australia, Belgium, Canada, and Switzerland, significantly increasing global accessibility of automated insulin delivery technology. The system’s integration with Dexcom CGM devices enabled real-time insulin adjustments, improving diabetes management outcomes across diverse patient populations.

- In August 2024, the U.S. FDA approved the Omnipod 5 tubeless insulin pump system for use in adults with insulin-requiring Type 2 diabetes, marking a major expansion of the device’s indication beyond Type 1 diabetes. This approval significantly widened the patient base eligible for automated, patch-based insulin delivery, reinforcing its role in mainstream diabetes care.

- In February 2024, Insulet Corporation announced the expansion of Omnipod DASH and Omnipod ecosystem support across new digital health integrations, improving connectivity with diabetes management apps and remote monitoring platforms. This development strengthened the foundation for future tubeless automated insulin delivery systems and enhanced patient engagement through data-driven diabetes care solutions

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.