Global Ultrafiltration Market

Market Size in USD Billion

CAGR :

%

USD

3.49 Billion

USD

10.73 Billion

2025

2033

USD

3.49 Billion

USD

10.73 Billion

2025

2033

| 2026 –2033 | |

| USD 3.49 Billion | |

| USD 10.73 Billion | |

| % | |

|

Ultrafiltration Market Size

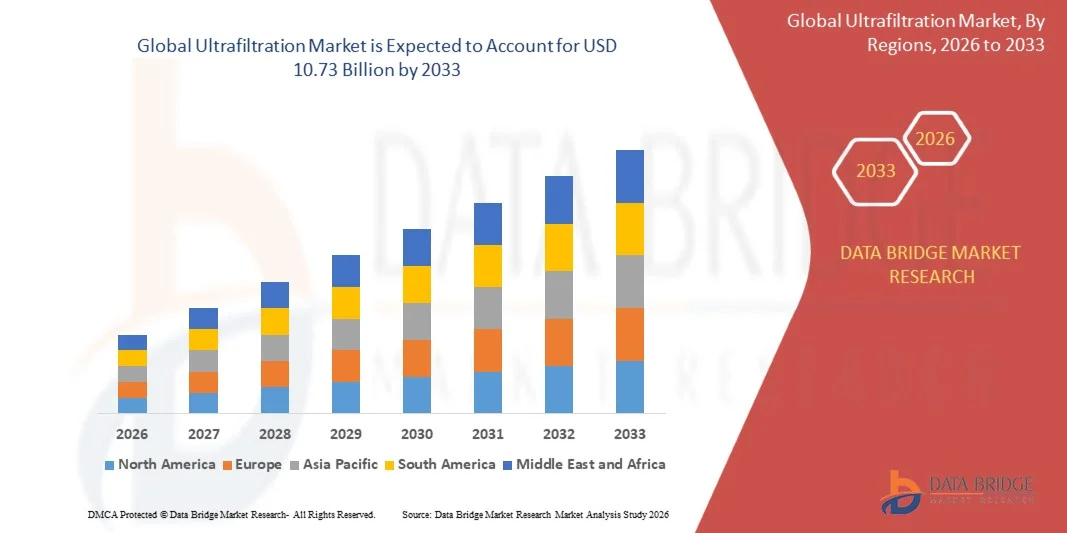

- The global ultrafiltration market size was valued at USD 3.49 billion in 2025 and is expected to reach USD 10.73 billion by 2033, at a CAGR of 15.05% during the forecast period

- The market growth is largely fuelled by the increasing demand for clean water and wastewater treatment solutions, rising adoption of advanced filtration technologies across industrial and municipal sectors, and growing emphasis on sustainability and water conservation

Ultrafiltration Market Analysis

- Ultrafiltration is a membrane filtration process widely used across industries for the separation of particles, bacteria, and macromolecules from liquids, offering high efficiency, low energy consumption, and compact design. It plays a vital role in water and wastewater treatment, food and beverage processing, pharmaceuticals, and chemical manufacturing, ensuring product purity and process reliability

- The market is primarily driven by increasing global concerns over water scarcity, stringent environmental regulations, and rising demand for high-quality filtration systems in industrial and municipal applications. Technological advancements in membrane materials and configurations, including hollow fiber and polymeric modules, are further propelling the adoption of ultrafiltration systems

- North America dominated the ultrafiltration market with the largest revenue share of 38.5% in 2025, driven by increasing demand for clean water, stringent regulations on water quality, and growing industrial and municipal water treatment requirements

- Asia-Pacific region is expected to witness the highest growth rate in the global ultrafiltration market, driven by expanding industrial activities, rising population, increasing need for clean water, and strong investments in municipal and industrial water treatment facilities

- The polymeric segment held the largest market revenue share in 2025 driven by its cost-effectiveness, ease of manufacturing, and versatility across municipal and industrial water treatment applications. Polymeric membranes are widely used for their high flux rates, chemical resistance, and compatibility with large-scale operations, making them a preferred choice for water purification systems. In addition, polymeric membranes are easier to replace and maintain, which reduces operational downtime and overall lifecycle costs. Their adaptability to hybrid systems with reverse osmosis and nanofiltration further strengthens their market dominance

Report Scope and Ultrafiltration Market Segmentation

|

Attributes |

Ultrafiltration Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Ultrafiltration Market Trends

“Increasing Demand for Clean Water and Advanced Filtration Technologies”

• The growing need for clean and safe water is significantly shaping the ultrafiltration market, as consumers and industries increasingly prioritize water purification and wastewater treatment. Ultrafiltration systems are gaining traction due to their ability to remove suspended solids, bacteria, viruses, and colloidal particles efficiently without the use of chemicals, supporting both municipal and industrial water management objectives

• Rising awareness of health, hygiene, and environmental sustainability has accelerated the adoption of ultrafiltration in food and beverage processing, pharmaceuticals, and chemical industries. Organizations are actively seeking solutions that ensure water quality compliance while reducing environmental impact, prompting manufacturers to develop advanced membranes and modular systems that cater to evolving operational needs

• Water quality regulations and sustainability trends are influencing purchasing decisions, with governments and private enterprises emphasizing eco-friendly operations, regulatory compliance, and water reuse initiatives. These factors are helping vendors differentiate offerings in a competitive market while driving the adoption of certified and high-performance ultrafiltration membranes

• For instance, in 2024, Suez in France and Pentair in the U.S. expanded their ultrafiltration product portfolios with next-generation membrane modules for municipal water treatment and industrial applications. These deployments addressed rising demand for efficient water purification solutions and were marketed as sustainable, cost-effective, and energy-efficient, enhancing adoption across utilities and commercial sectors

• While the ultrafiltration market is growing, sustained expansion depends on continuous R&D, membrane durability, and maintaining filtration efficiency comparable to alternative water treatment technologies. Manufacturers are also focusing on improving scalability, reducing operational costs, and developing innovative solutions that balance performance, energy efficiency, and sustainability

Ultrafiltration Market Dynamics

Driver

“Rising Adoption of Advanced Water Treatment Solutions”

• Increasing demand for safe, purified water is a major driver for the ultrafiltration market. Industries and municipalities are replacing conventional filtration methods with ultrafiltration to meet stringent water quality standards, improve operational efficiency, and reduce chemical usage. This trend is also promoting research into novel membrane materials and modular designs, supporting product innovation

• Expanding applications across municipal water treatment, food and beverage processing, pharmaceuticals, and chemicals are influencing market growth. Ultrafiltration improves water clarity, safety, and consistency while supporting sustainability initiatives, enabling organizations to comply with regulatory requirements and meet consumer expectations for high-quality water

• Industry players are actively promoting ultrafiltration solutions through product innovation, technology upgrades, and strategic partnerships with utilities and industrial operators. Growing emphasis on water conservation and operational efficiency is encouraging adoption, while collaborative efforts with membrane manufacturers enhance system performance and reliability

• For instance, in 2023, Dow Water & Process Solutions in the U.S. and GE Water & Process Technologies in Germany reported expanded use of ultrafiltration modules in industrial and municipal applications. These expansions followed increased investment in water treatment infrastructure, stricter water quality regulations, and rising demand for energy-efficient filtration systems, driving broader adoption and customer trust

• Although rising demand supports growth, wider adoption depends on cost-effectiveness, membrane life, and ease of integration with existing water treatment systems. Investment in R&D, supply chain efficiency, and energy-efficient technologies will be critical for meeting global demand and maintaining competitive advantage

Restraint/Challenge

“High Installation Costs and Operational Complexity”

• The relatively high capital expenditure for ultrafiltration systems compared to conventional filtration methods remains a key challenge, limiting adoption among cost-sensitive operators. High upfront costs for membranes, modules, and auxiliary equipment, along with energy requirements, contribute to elevated investment

• Operational complexity and maintenance requirements, such as membrane cleaning, replacement, and monitoring, can restrict uptake in smaller industrial setups or municipalities with limited technical expertise. Insufficient awareness of ultrafiltration benefits further affects adoption in emerging markets

• Supply chain and logistical challenges also impact market growth, as ultrafiltration membranes require careful handling, storage, and compliance with quality standards. Shorter membrane lifespan and sensitivity to feedwater quality can increase operational costs and reduce system reliability

• For instance, in 2024, water treatment facilities in Southeast Asia deploying ultrafiltration systems for small-scale industrial and municipal operations reported slower adoption due to higher installation costs and maintenance complexity. These challenges also led some operators to continue using conventional sand or cartridge filtration despite lower performance

• Overcoming these challenges will require cost-optimized solutions, simplified installation, robust maintenance support, and focused educational initiatives for operators and municipalities. Collaboration with technology providers, equipment integrators, and certification bodies can help unlock the long-term growth potential of the global ultrafiltration market while improving system efficiency and reliability

Ultrafiltration Market Scope

The market is segmented on the basis of type, module, and application.

• By Type

On the basis of type, the ultrafiltration market is segmented into polymeric and ceramic. The polymeric segment held the largest market revenue share in 2025 driven by its cost-effectiveness, ease of manufacturing, and versatility across municipal and industrial water treatment applications. Polymeric membranes are widely used for their high flux rates, chemical resistance, and compatibility with large-scale operations, making them a preferred choice for water purification systems. In addition, polymeric membranes are easier to replace and maintain, which reduces operational downtime and overall lifecycle costs. Their adaptability to hybrid systems with reverse osmosis and nanofiltration further strengthens their market dominance.

The ceramic segment is expected to witness the fastest growth rate from 2026 to 2033, driven by its superior durability, thermal and chemical stability, and longer lifespan. Ceramic ultrafiltration membranes are particularly popular for industrial applications requiring harsh operating conditions, providing reliable performance and reduced maintenance requirements. They are also highly resistant to fouling and can withstand frequent cleaning cycles, making them suitable for applications with challenging feed water. Growing awareness of long-term cost savings and efficiency benefits is encouraging industries to adopt ceramic membranes in water-intensive processes.

• By Module

On the basis of module, the market is segmented into hollow fiber and others. The hollow fiber segment held the largest market revenue share in 2025 due to its high surface area-to-volume ratio, efficient filtration performance, and ease of scaling for both municipal and industrial treatment systems. Hollow fiber modules are flexible in design, allowing for compact installations and modular expansion based on capacity needs. They are also highly effective in removing suspended solids, bacteria, and viruses, which ensures consistent water quality and compliance with regulations. In addition, hollow fiber modules support both gravity-fed and pressurized systems, enhancing their versatility across different applications.

The others segment, including tubular and flat-sheet modules, is projected to register the fastest growth from 2026 to 2033, driven by their specialized applications in chemical processing, pharmaceuticals, and high-purity water production. These modules offer enhanced mechanical strength and the ability to handle high-temperature or high-viscosity fluids, which makes them suitable for demanding industrial environments. Their precise separation capabilities and compatibility with advanced hybrid treatment systems are driving adoption in sectors with stringent water quality requirements. Continuous innovation in module design is expected to further increase efficiency and reduce operational costs, supporting market growth.

• By Application

On the basis of application, the market is segmented into municipal treatment and industrial treatment. The municipal treatment segment held the largest market revenue share in 2025, fueled by the growing demand for safe drinking water, stringent water quality regulations, and increasing investment in urban water infrastructure. Municipal ultrafiltration systems are widely deployed for surface water and groundwater treatment, providing consistent purification and reducing dependence on chemical disinfectants. The ease of integration with distribution networks and ability to deliver high-quality water for large populations further strengthens market adoption.

The industrial treatment segment is expected to witness the fastest growth rate from 2026 to 2033, driven by rising water reuse initiatives, stringent effluent discharge standards, and increasing adoption of ultrafiltration for food and beverage, pharmaceuticals, and chemical processing industries. Industries are leveraging ultrafiltration to recycle process water, reduce operational costs, and meet environmental compliance standards. The technology is particularly valued for its ability to remove fine particles, bacteria, and colloids, ensuring product quality and safety. Growing focus on sustainable manufacturing and circular water use is expected to accelerate demand in the industrial sector.

Ultrafiltration Market Regional Analysis

• North America dominated the ultrafiltration market with the largest revenue share of 38.5% in 2025, driven by increasing demand for clean water, stringent regulations on water quality, and growing industrial and municipal water treatment requirements

• Consumers and industries in the region highly value reliable, high-performance filtration systems that ensure safe drinking water, wastewater reuse, and process water quality

• This widespread adoption is further supported by advanced infrastructure, high investment in water treatment technologies, and the preference for energy-efficient and sustainable water purification solutions, establishing ultrafiltration as a key technology for municipal and industrial applications

U.S. Ultrafiltration Market Insight

The U.S. ultrafiltration market captured the largest revenue share in 2025 within North America, fueled by the increasing focus on water conservation, reuse initiatives, and the modernization of municipal water treatment facilities. Industries are prioritizing high-quality water for food, beverage, and pharmaceutical production, which drives demand for ultrafiltration systems. In addition, technological advancements, such as high-flux polymeric membranes and modular filtration units, along with integration with reverse osmosis and nanofiltration, further support market growth. Regulatory emphasis on reducing contaminants and ensuring safe drinking water is significantly contributing to the market expansion.

Europe Ultrafiltration Market Insight

The Europe ultrafiltration market is expected to witness the fastest growth rate from 2026 to 2033, primarily driven by stringent water quality regulations, increasing urbanization, and rising demand for sustainable water treatment solutions. Municipalities and industries are investing in advanced filtration technologies to comply with environmental and health standards. European consumers and businesses are drawn to the energy efficiency, reliability, and eco-friendly advantages offered by ultrafiltration systems. The region is experiencing growing deployment in both new infrastructure projects and retrofitting of existing water treatment plants.

Germany Ultrafiltration Market Insight

The Germany ultrafiltration market is expected to witness the fastest growth rate from 2026 to 2033, fueled by increasing awareness of water safety, demand for advanced industrial water treatment, and focus on sustainability. The country’s well-developed industrial and municipal infrastructure, combined with strong regulatory compliance, promotes the adoption of ultrafiltration technology. Integration with smart water management systems and the emphasis on reducing chemical usage further strengthens market growth, particularly in residential, commercial, and industrial applications.

Asia-Pacific Ultrafiltration Market Insight

The Asia-Pacific ultrafiltration market is expected to witness the fastest growth rate from 2026 to 2033, driven by rapid urbanization, industrial expansion, and rising demand for clean water in countries such as China, India, and Japan. Government initiatives promoting water treatment and smart city projects are accelerating the adoption of ultrafiltration technologies. Furthermore, the region’s growing manufacturing base for filtration systems, coupled with increasing affordability and accessibility, is expanding ultrafiltration deployment across municipal and industrial sectors.

China Ultrafiltration Market Insight

The China ultrafiltration market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to rapid industrialization, urban population growth, and increased investment in municipal water treatment facilities. The country is focusing on improving water quality standards and implementing large-scale water purification projects, driving the demand for ultrafiltration membranes and systems. Growing awareness of water reuse and sustainability, along with local manufacturing of ultrafiltration technologies, is supporting broader adoption across residential, commercial, and industrial applications.

Japan Ultrafiltration Market Insight

The Japan ultrafiltration market is expected to witness the fastest growth rate from 2026 to 2033 due to high technological adoption, urban infrastructure modernization, and increasing demand for safe and sustainable water solutions. Japanese municipalities and industries are leveraging ultrafiltration for efficient water treatment, process water quality, and wastewater reuse. Integration with advanced monitoring systems and the emphasis on reducing environmental impact further propels market growth, making ultrafiltration a preferred solution for municipal and industrial water management.

Ultrafiltration Market Share

The Ultrafiltration industry is primarily led by well-established companies, including:

- Koch Membrane Systems, Inc. (U.S.)

- Pall Corporation (U.S.)

- SUEZ (France)

- 3M (U.S.)

- TORAY INDUSTRIES, INC. (Japan)

- ALFA LAVAL (Sweden)

- Beijing Originwater Technology Co., Ltd. (China)

- Beijing OriginWater Technology Co., Ltd. (China)

- GEA Group Aktiengesellschaft (Germany)

- Markel Group Inc. (U.S.)

- Membranium (Russia)

- MANN+HUMMEL Water & Fluid Solutions GmbH (Germany)

- Parker Hannifin Corp (U.S.)

- PCI Membranes (U.K.)

- Beijing Sino Water Technology Co., Ltd. (China)

- Synder Filtration, Inc. (U.S.)

- TOYOBO CO., LTD (Japan)

- Veolia (France)

Latest Developments in Global Ultrafiltration Market

- In April 2024, QUA, facility expansion, announced the opening of a new advanced membrane manufacturing center in Pune, India to strengthen production capacity for high-performance ultrafiltration and water treatment membranes. The facility aims to support rising global demand for efficient water purification technologies across municipal and industrial sectors. This expansion enhances regional manufacturing capabilities, improves supply chain efficiency, and supports wider adoption of advanced filtration solutions, strengthening the company’s position in the global ultrafiltration market

- In September 2024, Sartorius, product launch, introduced the Vivaflow SU system designed for laboratory-scale tangential flow filtration (TFF). The solution enables more efficient ultrafiltration and diafiltration processes for feed volumes ranging from 100 to 1,000 mL while improving operational flexibility and sustainability. The innovation enhances laboratory filtration efficiency and supports research and bioprocessing applications, reinforcing the company’s leadership in advanced laboratory filtration technologies

- In April 2024, Michael Lesniak, industry insight and investment discussion, highlighted Taiwan’s USD 13 billion investment in semiconductor water treatment infrastructure during an interview with Smart Water Magazine. The initiative emphasizes the increasing importance of advanced water management solutions within semiconductor manufacturing. This large-scale investment is expected to drive demand for high-performance filtration systems such as ultrafiltration, supporting technological innovation and market growth in industrial water treatment

- In September 2020, DuPont in collaboration with Sun Chemical, strategic partnership, initiated joint efforts to develop advanced water treatment solutions by combining chemical expertise and filtration technologies. The collaboration aimed to improve efficiency and sustainability in water purification processes for industrial and municipal applications. This partnership strengthened research capabilities and supported the development of next-generation filtration technologies, contributing to long-term innovation in the ultrafiltration market

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Ultrafiltration Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Ultrafiltration Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Ultrafiltration Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.