Global Underfill Market

Market Size in USD Million

CAGR :

%

USD

517.92 Million

USD

1,051.08 Million

2025

2033

USD

517.92 Million

USD

1,051.08 Million

2025

2033

| 2026 –2033 | |

| USD 517.92 Million | |

| USD 1,051.08 Million | |

| % | |

|

Underfill Market Size

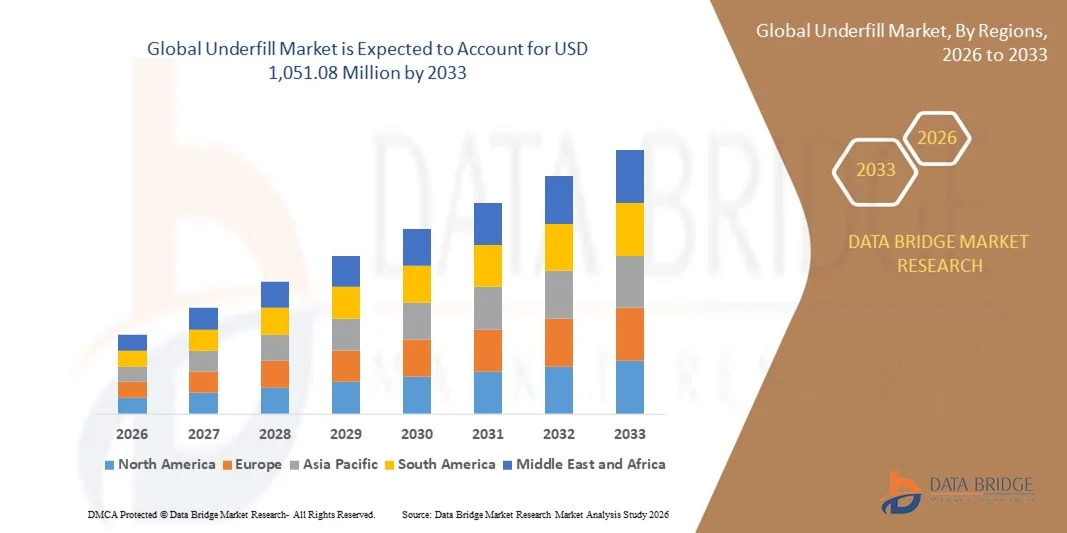

- The global underfill market size was valued at USD 517.92 million in 2025 and is expected to reach USD 1,051.08 million by 2033, at a CAGR of 9.25% during the forecast period

- The market growth is largely fuelled by the increasing demand for advanced electronic devices, miniaturization of components, and rising adoption of flip-chip packaging in consumer electronics and automotive applications

- Growing need for thermal management, mechanical protection, and enhanced reliability of semiconductor devices is further driving the adoption of underfill materials across various industries

Underfill Market Analysis

- Increasing consumer demand for compact, high-performance electronics and wearable devices is pushing manufacturers to adopt underfill solutions for reliability and durability

- The surge in automotive electronics, including advanced driver-assistance systems (ADAS) and electric vehicles (EVs), is creating significant growth opportunities for underfill materials

- North America dominated the underfill market with the largest revenue share in 2025, driven by the growing demand for high-reliability electronic devices, miniaturization, and advanced packaging technologies

- Asia-Pacific region is expected to witness the highest growth rate in the global underfill market, driven by increasing electronics production, growing consumer electronics and automotive sectors, and supportive government policies in countries such as China, Japan, and South Korea

- The Capillary Underfill Material (CUF) segment held the largest market revenue share in 2025, driven by its widespread use in flip-chip assemblies and compatibility with automated dispensing systems. CUF provides excellent mechanical support and thermal stress management, making it a preferred choice for high-density electronics and consumer devices

Report Scope and Underfill Market Segmentation

|

Attributes |

Underfill Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Underfill Market Trends

Rise of Advanced Underfill Solutions in Electronics Packaging

- The growing shift toward advanced underfill materials is transforming the electronics packaging landscape by enhancing chip reliability, reducing thermal stress, and improving mechanical stability. These materials enable higher-density packaging and prolong device lifespan, resulting in improved overall performance and lower failure rates. In addition, they support emerging high-speed, high-frequency applications by minimizing signal distortion and thermal mismatch issues. Adoption of these materials is increasingly driven by OEMs aiming to enhance device longevity and reduce warranty claims

- The high demand for underfill in flip-chip, CSP, and BGA applications is accelerating adoption across consumer electronics, automotive, and industrial sectors. Underfill materials help manage thermal expansion differences between chips and substrates, reducing solder joint fatigue and enhancing product durability. Growing trends in electric vehicles, IoT devices, and 5G technology are further boosting the need for reliable underfill solutions capable of supporting high thermal loads and mechanical stress

- The versatility and ease of application of modern underfill formulations are making them attractive for diverse packaging technologies, enabling manufacturers to optimize production yield and device performance. This improves time-to-market and ensures consistent product quality. Manufacturers are increasingly preferring low-viscosity, fast-curing underfills that are compatible with automated dispensing systems, reducing cycle times and improving assembly efficiency

- For instance, in 2023, several North American and Asian electronics manufacturers reported improved reliability and reduced defect rates after integrating next-generation underfill resins in high-density packaging assemblies, supporting greater device longevity and performance. These companies also experienced fewer field returns and reduced thermal fatigue issues, strengthening customer confidence in their products. The implementation of advanced underfills contributed to better compliance with international quality standards and automotive electronics reliability benchmarks

- While advanced underfill solutions are accelerating device reliability and production efficiency, sustained growth depends on continued material innovation, process optimization, and cost-effectiveness. Companies must focus on high-performance, scalable formulations to meet growing industry requirements. Collaboration between material suppliers and device manufacturers is also crucial to develop application-specific underfill solutions that address unique challenges in miniaturized and high-power electronics

Underfill Market Dynamics

Driver

Rising Demand for High-Reliability Electronics and Miniaturization

- The push for smaller, high-performance electronic devices is driving demand for advanced underfill materials that provide superior mechanical support and thermal management. This trend is particularly prominent in smartphones, wearables, and automotive electronics. Manufacturers are also leveraging underfill solutions to improve solder joint reliability in high-density packages and reduce risk of device failure under extreme environmental conditions

- Electronics manufacturers are focusing on improving device reliability, preventing solder joint failures, and enhancing thermal cycling performance. High-quality underfill materials help maintain product integrity, reduce warranty costs, and improve customer satisfaction. In addition, underfill adoption is helping manufacturers meet stringent automotive and aerospace reliability standards, opening up opportunities in safety-critical applications

- Industry standards and quality regulations further support adoption, as manufacturers seek solutions that meet stringent reliability requirements in critical applications, including automotive, aerospace, and industrial electronics. Compliance with JEDEC and IPC standards for underfill materials ensures device reliability and long-term performance. Regulatory pressure is encouraging wider implementation in high-reliability sectors such as electric vehicles and defense electronics

- For instance, in 2022, several European and U.S. semiconductor companies upgraded to high-performance underfill resins for BGA and flip-chip packages, improving device reliability and production yields while reducing field failures. These upgrades also enabled faster production cycles, lower rework rates, and minimized thermal-induced warpage, positively impacting operational efficiency and profitability

- While demand for reliability and miniaturization is driving the market, there is a need for cost-effective, process-compatible underfill solutions that can be scaled across various packaging technologies to ensure sustained adoption. Innovation in low-temperature curing, rapid flow, and environmentally friendly underfill formulations will further enhance market growth

Restraint/Challenge

High Material Costs and Complex Application Processes

- The high price of advanced underfill materials, including epoxy and anisotropic formulations, limits adoption for small-scale electronics manufacturers. Cost remains a significant barrier to widespread utilization, particularly in consumer-grade devices. The need for specialized curing equipment and process controls further increases operational expenses, discouraging some manufacturers from adopting cutting-edge underfills

- In many regions, there is a lack of trained personnel capable of applying underfill materials consistently and managing curing processes. Improper application can lead to voids, delamination, or device failure, restricting market penetration. Training programs and process standardization are essential to ensure quality and reliability in high-volume manufacturing lines

- Complex integration with automated assembly lines and equipment compatibility issues can hinder adoption, requiring specialized dispensing and curing systems. Retrofitting existing production lines often increases operational costs and complexity. Challenges include precise alignment, controlling underfill viscosity, and ensuring complete coverage without introducing defects in miniaturized packages

- For instance, in 2023, several electronics manufacturers in Asia-Pacific reported production slowdowns due to challenges in integrating new underfill resins into automated flip-chip assembly processes, affecting yield and throughput. These delays also led to temporary supply chain disruptions for downstream consumer electronics manufacturers, highlighting the importance of skilled process management

- While material innovation continues to improve performance and ease of use, addressing cost, skill gaps, and process complexity remains crucial for long-term market scalability and widespread adoption of underfill solutions. Investments in training, process automation, and collaborative development of application-specific underfills are key strategies to overcome these challenges and maintain industry growth

Underfill Market Scope

The market is segmented on the basis of product and application.

- By Product

On the basis of product, the underfill market is segmented into Capillary Underfill Material (CUF), No Flow Underfill Material (NUF), and Molded Underfill Material (MUF). The Capillary Underfill Material (CUF) segment held the largest market revenue share in 2025, driven by its widespread use in flip-chip assemblies and compatibility with automated dispensing systems. CUF provides excellent mechanical support and thermal stress management, making it a preferred choice for high-density electronics and consumer devices.

The No Flow Underfill Material (NUF) segment is expected to witness the fastest growth rate from 2026 to 2033, driven by its suitability for high-volume BGA and CSP packaging applications. NUF enables simplified assembly processes and reduces void formation, making it ideal for manufacturers seeking higher yield and enhanced device reliability.

- By Application

On the basis of application, the underfill market is segmented into Flip Chips, Ball Grid Array (BGA), and Chip Scale Packaging (CSP). The Flip Chips segment accounted for the largest revenue share in 2025, owing to the increasing demand for miniaturized and high-performance electronic devices. Flip-chip assemblies benefit from underfill materials that reduce solder joint fatigue and improve thermal cycling performance.

The Ball Grid Array (BGA) segment is projected to witness the fastest growth rate from 2026 to 2033, driven by its expanding adoption in automotive, consumer electronics, and industrial applications. Underfill integration in BGA packages ensures better mechanical stability, higher reliability, and longer operational lifespan, making it a critical solution for next-generation electronic products.

Underfill Market Regional Analysis

- North America dominated the underfill market with the largest revenue share in 2025, driven by the growing demand for high-reliability electronic devices, miniaturization, and advanced packaging technologies

- Electronics manufacturers in the region highly value the performance, thermal management, and reliability enhancements provided by advanced underfill materials, which help reduce solder joint failures and improve product durability

- This widespread adoption is further supported by strong R&D capabilities, high disposable incomes, and a technologically advanced manufacturing ecosystem, establishing underfill materials as a critical component in semiconductor assembly

U.S. Underfill Market Insight

The U.S. underfill market captured the largest revenue share in 2025 within North America, fueled by rapid adoption of flip-chip, BGA, and CSP packaging in consumer electronics, automotive, and industrial applications. Electronics companies are increasingly prioritizing high-performance materials to enhance device reliability and thermal management. The growing demand for miniaturized and high-density packages, combined with strict quality and reliability standards, further propels the underfill market. Moreover, the integration of advanced underfill resins into automated assembly lines is significantly contributing to improved production yields and reduced field failures.

Europe Underfill Market Insight

The Europe underfill market is expected to witness the fastest growth rate from 2026 to 2033, primarily driven by rising demand for high-reliability electronics in automotive, aerospace, and industrial applications. The increase in semiconductor manufacturing and the push for advanced packaging technologies are fostering the adoption of underfill materials. European electronics manufacturers are also drawn to the reliability, thermal performance, and process compatibility these materials offer. The region is experiencing significant growth across flip-chip and BGA applications, with underfill materials being incorporated into both new product designs and retrofitted packages.

U.K. Underfill Market Insight

The U.K. underfill market is expected to witness a high growth rate from 2026 to 2033, driven by the increasing trend of miniaturized electronics and the demand for improved device reliability. In addition, stringent quality regulations and consumer expectations for durable electronic products are encouraging manufacturers to adopt advanced underfill solutions. The UK’s robust semiconductor R&D ecosystem and manufacturing infrastructure, along with growing adoption of IoT devices, are expected to continue stimulating market growth.

Germany Underfill Market Insight

The Germany underfill market is expected to witness a significant growth rate from 2026 to 2033, fueled by increasing awareness of thermal and mechanical stress management in high-performance electronics. Germany’s advanced manufacturing infrastructure, emphasis on precision engineering, and focus on eco-friendly materials promote the adoption of underfill solutions, particularly in automotive and industrial electronics. Integration of underfill materials into high-density packaging processes is becoming increasingly prevalent, with strong demand for solutions that enhance reliability, durability, and long-term performance.

Asia-Pacific Underfill Market Insight

The Asia-Pacific underfill market is expected to witness the fastest growth rate from 2026 to 2033, driven by rapid semiconductor manufacturing expansion, rising disposable incomes, and growing demand for miniaturized electronic devices in countries such as China, Japan, South Korea, and India. The region's inclination toward high-performance electronics, supported by government initiatives in semiconductor and electronics manufacturing, is driving underfill adoption. Furthermore, APAC’s role as a major hub for electronics assembly and packaging is expanding the accessibility and affordability of advanced underfill materials for a wider range of applications.

Japan Underfill Market Insight

The Japan underfill market is expected to witness high growth from 2026 to 2033 due to the country’s high-tech culture, rapid adoption of miniaturized electronics, and focus on device reliability. Japanese electronics manufacturers prioritize thermal management, solder joint reliability, and long-term performance, driving demand for advanced underfill solutions. Integration of underfill materials with flip-chip, BGA, and CSP applications, along with compatibility with automated assembly lines, is further fueling market expansion. Japan’s aging population and increasing use of connected devices are likely to increase the need for durable, reliable, and easy-to-assemble electronics.

China Underfill Market Insight

The China underfill market accounted for the largest revenue share in Asia-Pacific in 2025, attributed to the country’s booming electronics manufacturing sector, rapid urbanization, and high adoption of consumer and industrial electronics. China is a major hub for semiconductor assembly, and underfill materials are becoming increasingly essential in high-density packaging processes. The push toward advanced packaging technologies, government support for electronics manufacturing, and the presence of strong domestic underfill suppliers are key factors propelling market growth in China.

Underfill Market Share

The Underfill industry is primarily led by well-established companies, including:

- Henkel Adhesives Technologies India Private Limited (India)

- Wonchemical (U.S.)

- Epoxy Technology, Inc (U.S.)

- AIM Metals & Alloys LP (U.S.)

- H.B. Fuller Company (U.S.)

- John Wiley & Sons, Inc (U.S.)

- Nordson Corporation (U.S.)

- Master Bond Inc (U.S.)

- NAMICS (U.S.)

- YINCAE Advanced Materials, LLC (U.S.)

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Underfill Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Underfill Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Underfill Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.