Global Urolithiasis Management Devices Market

Market Size in USD Billion

CAGR :

%

USD

1.86 Billion

USD

2.94 Billion

2025

2033

USD

1.86 Billion

USD

2.94 Billion

2025

2033

| 2026 –2033 | |

| USD 1.86 Billion | |

| USD 2.94 Billion | |

| % | |

|

Urolithiasis Management Devices Market Size

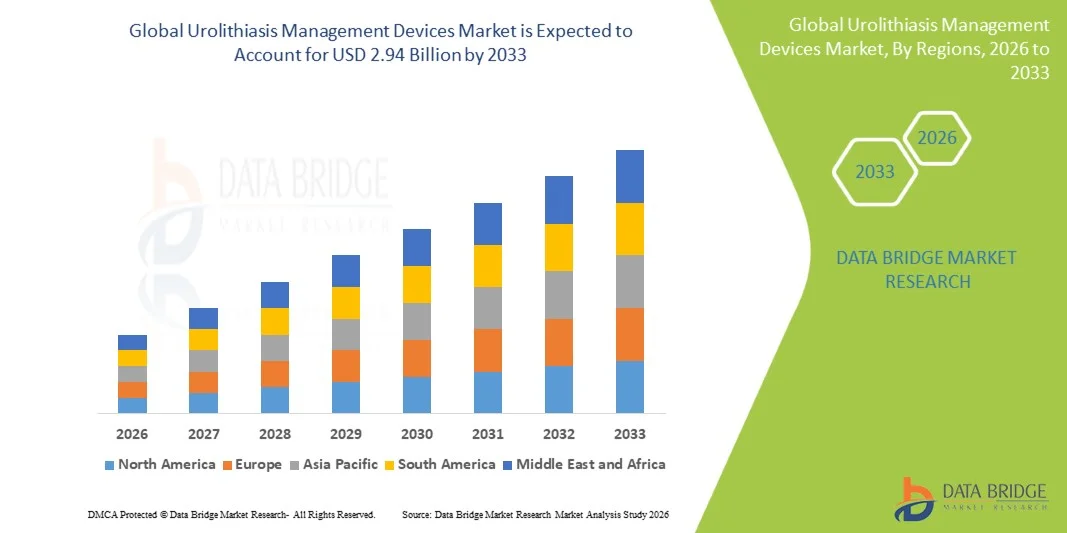

- The global urolithiasis management devices market size was valued at USD 1.86 billion in 2025and is expected to reach USD 2.94 billion by 2033, at a CAGR of 5.90% during the forecast period

- The market growth is largely driven by the rising prevalence of kidney stones, increasing sedentary lifestyles, dehydration-related disorders, and growing geriatric population, along with continuous advancements in minimally invasive and non-invasive stone removal technologies across healthcare systems

- Furthermore, increasing patient preference for faster recovery procedures, improved clinical outcomes, and the widespread adoption of laser lithotripsy, ureteroscopy, and extracorporeal shock wave lithotripsy is establishing advanced urolithiasis management devices as the preferred treatment approach, thereby significantly boosting the industry's growth

Urolithiasis Management Devices Market Analysis

- Urolithiasis management devices, used for breaking, removing, and treating kidney stones, are increasingly important in modern urology due to their ability to support minimally invasive procedures, reduce surgical complications, and improve patient recovery outcomes across hospitals and specialty clinics

- The growing demand for these devices is primarily driven by the rising global incidence of kidney stones due to dietary changes, obesity, dehydration, and metabolic disorders, along with increasing preference for minimally invasive and highly effective treatment options

- North America dominated the urolithiasis management devices market with the largest revenue share of 38.6% in 2025, supported by advanced healthcare infrastructure, high procedural adoption rates, and strong presence of leading medical device companies, with the U.S. showing significant uptake of advanced lithotripsy and endoscopic stone management technologies

- Asia-Pacific is expected to be the fastest growing region in the urolithiasis management devices market during the forecast period due to rising patient burden, improving healthcare infrastructure, increasing awareness of kidney stone treatment, and expanding access to minimally invasive urology procedures

- Extracorporeal Shock Wave Lithotripsy (ESWL) segment dominated the urolithiasis management devices market with a significant share of 44.1% in 2025, driven by its non-invasive nature, high patient acceptance, and effectiveness in fragmenting kidney stones without surgical intervention

Report Scope and Urolithiasis Management Devices Market Segmentation

|

Attributes |

Urolithiasis Management Devices Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

|

|

Market Opportunities |

· Growing opportunity in AI-assisted and image-guided lithotripsy systems · Expansion of ambulatory surgical centers (ASCs) |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Urolithiasis Management Devices Market Trends

“Advancement Toward Minimally Invasive and Laser-Based Stone Treatment”

- A significant and accelerating trend in the global urolithiasis management devices market is the shift toward minimally invasive and laser-based technologies, such as intracorporeal lithotripsy and advanced ureteroscopic procedures, improving stone fragmentation efficiency and patient recovery outcomes in hospital and outpatient settings

- For instance, Holmium:YAG and newer Thulium Fiber Laser systems are increasingly used in intracorporeal lithotripsy procedures, enabling precise stone dusting and fragmentation with reduced complication rates compared to conventional surgical approaches

- Technological advancements in urology devices are enabling real-time imaging integration, improved scope flexibility, and higher energy efficiency in lithotripsy systems, thereby enhancing procedural accuracy and reducing operative time and hospital stay duration

- Furthermore, the integration of digital imaging systems with ureteroscopes and lithotripters is allowing urologists to perform more precise stone localization and fragmentation through unified visualization platforms across treatment workflows

- This trend toward highly efficient, image-guided, and minimally invasive stone management systems is reshaping clinical expectations, with companies such as Boston Scientific and Olympus developing next-generation laser lithotripsy and advanced ureteroscopy platforms

- The demand for minimally invasive urolithiasis management solutions is growing rapidly across hospitals and ambulatory surgical centers, as healthcare providers increasingly prioritize faster recovery, reduced complications, and improved patient throughput

- Furthermore, the emergence of robot-assisted endourology is enhancing precision in stone retrieval procedures, supporting better clinical outcomes and reduced surgeon fatigue

Urolithiasis Management Devices Market Dynamics

Driver

“Rising Prevalence of Kidney Stones and Increasing Preference for Non-Invasive Treatments”

- The increasing prevalence of kidney stone disease globally, coupled with lifestyle changes such as dehydration, high-sodium diets, and rising obesity rates, is a significant driver for the growing demand for urolithiasis management devices across healthcare systems

- For instance, in April 2025, several urology centers expanded adoption of advanced ESWL and laser lithotripsy systems to manage rising patient inflow, reflecting growing reliance on minimally invasive stone treatment technologies

- As patients and healthcare providers increasingly prioritize non-invasive and low-risk treatment options, devices such as ESWL systems and flexible ureteroscopes are becoming widely preferred for effective stone management with reduced recovery time

- Furthermore, increasing awareness of early diagnosis and treatment of kidney stones is driving higher procedural volumes in hospitals, specialty urology clinics, and ambulatory surgical centers globally

- The convenience of outpatient-based procedures, shorter hospitalization periods, and improved clinical outcomes are key factors accelerating the adoption of advanced urolithiasis management devices in both developed and emerging healthcare market

- In addition, expanding healthcare insurance coverage for endoscopic and laser-based stone removal procedures is further supporting higher treatment accessibility and adoption rates

- Moreover, growing investment in hospital urology departments and surgical infrastructure upgrades is enabling wider deployment of advanced lithotripsy systems

Restraint/Challenge

“High Procedure Costs and Limited Access to Advanced Urology Infrastructure”

- Concerns surrounding the high cost of advanced urolithiasis treatment devices and procedures, including laser lithotripsy systems and flexible ureteroscopes, pose a significant challenge to wider market adoption, particularly in cost-sensitive healthcare regions

- For instance, many healthcare facilities in developing regions still rely on conventional surgical methods due to the limited affordability and availability of advanced ESWL and intracorporeal lithotripsy systems

- The requirement for specialized infrastructure, skilled urologists, and high maintenance costs for advanced devices further restricts adoption, especially in smaller hospitals and rural healthcare settings

- In addition, reimbursement limitations and inconsistent insurance coverage for advanced kidney stone procedures can reduce patient accessibility to modern treatment options in certain regions

- While technological advancements are gradually improving device efficiency and cost-effectiveness, the relatively high initial investment continues to hinder rapid penetration of advanced urolithiasis management solutions in emerging markets

- Furthermore, uneven distribution of trained urology specialists limits the effective utilization of advanced lithotripsy and ureteroscopy technologies in low-resource healthcare systems

- Moreover, supply chain constraints and dependence on imported high-end devices can delay adoption timelines and increase overall procedural costs in several regions

Urolithiasis Management Devices Market Scope

The market is segmented on the basis of treatment type, product type, and end user.

- By Treatment Type

On the basis of treatment type, the urolithiasis management devices market is segmented into Extracorporeal Shock Wave Lithotripsy (ESWL), Intracorporeal Lithotripsy, Percutaneous Nephrolithotomy, and Others. Extracorporeal Shock Wave Lithotripsy (ESWL) dominated the market with the largest revenue share of 44.1% in 2025, driven by its non-invasive nature and ability to fragment kidney stones without surgical intervention. ESWL is widely preferred in both hospital and outpatient settings due to reduced recovery time and minimal complications. It is particularly effective for small to medium-sized renal stones, making it a first-line treatment option in many clinical guidelines. The procedure also requires comparatively lower hospitalization, which supports its strong adoption in cost-sensitive healthcare systems. In addition, continuous improvements in shock wave targeting and imaging guidance have enhanced its clinical efficiency. Its established presence and widespread availability further strengthen its dominance across global healthcare facilities.

Intracorporeal Lithotripsy is expected to witness the fastest growth rate of 8.9% from 2026 to 2033, driven by increasing adoption of laser-based technologies and minimally invasive endoscopic procedures. This method allows direct visualization and fragmentation of stones, leading to higher precision and improved stone-free rates. The growing use of Holmium and Thulium fiber lasers has significantly improved treatment efficiency and reduced operative time. It is increasingly preferred for complex and hard-to-treat stones located in the ureter and kidney. Rising demand for outpatient procedures and shorter hospital stays is further supporting its expansion. In addition, technological advancements in flexible ureteroscopes are enhancing procedural success rates, accelerating its adoption globally.

- By Product Type

On the basis of product type, the market is segmented into lithotripters and ureteroscopes. Lithotripters dominated the market with the largest revenue share of 57.6% in 2025, supported by their extensive use in ESWL and intracorporeal stone fragmentation procedures. Lithotripters are widely adopted in hospitals due to their effectiveness in breaking kidney stones non-invasively or minimally invasively. The availability of advanced laser and electromagnetic lithotripters has significantly improved treatment outcomes and procedural accuracy. These devices are preferred for their ability to handle a wide range of stone sizes and compositions. Increasing hospital investments in advanced urology equipment further support segment dominance. Moreover, growing procedural volumes globally continue to drive strong demand for lithotripter systems.

Ureteroscopes are expected to witness the fastest growth rate of 9.4% from 2026 to 2033, driven by rising preference for minimally invasive endoscopic stone removal procedures. Flexible ureteroscopes are increasingly used for precise visualization and direct stone extraction from the urinary tract. Continuous advancements in digital imaging and disposable ureteroscope technology are improving procedural safety and efficiency. Their ability to reduce infection risks and cross-contamination is further boosting adoption in high-volume surgical centers. Growing demand for outpatient urological procedures is also accelerating their use. In addition, improved ergonomics and enhanced maneuverability are making ureteroscopes more efficient for complex stone cases.

- By End User

On the basis of end user, the market is segmented into hospitals and clinics, and ambulatory surgical centers. Hospitals and Clinics dominated the market with the largest revenue share of 66.8% in 2025, driven by the availability of advanced surgical infrastructure and skilled urologists. Hospitals handle a high volume of complex kidney stone cases requiring ESWL, lithotripsy, and percutaneous procedures. The presence of comprehensive diagnostic and surgical facilities supports higher adoption of advanced urolithiasis devices. These settings also benefit from better reimbursement frameworks and patient trust in specialized care. Increasing investments in hospital-based urology departments further strengthen segment leadership. In addition, rising patient inflow for emergency stone treatments contributes significantly to hospital dominance.

Ambulatory Surgical Centers (ASCs) are expected to witness the fastest growth rate of 10.2% from 2026 to 2033, driven by the increasing shift toward outpatient and same-day surgical procedures. ASCs offer cost-effective treatment options with reduced hospital stay and faster recovery times. The growing adoption of minimally invasive lithotripsy and ureteroscopy procedures is well aligned with ASC capabilities. These centers are increasingly equipped with advanced laser and endoscopic systems for kidney stone management. Patient preference for quick, convenient treatment is further accelerating ASC utilization. In addition, rising healthcare cost pressures are encouraging migration from hospital-based care to ambulatory settings.

Urolithiasis Management Devices Market Regional Analysis

- North America dominated the urolithiasis management devices market with the largest revenue share of 38.6% in 2025, supported by advanced healthcare infrastructure, high procedural adoption rates, and strong presence of leading medical device companies

- Patients and healthcare providers in the region highly value the availability of advanced treatment options such as ESWL, laser lithotripsy, and flexible ureteroscopy, which offer higher success rates and faster recovery compared to traditional surgical methods

- This strong market adoption is further supported by high healthcare expenditure, early adoption of innovative medical technologies, and the presence of leading medical device companies, establishing urolithiasis devices as a standard of care in both hospital and outpatient settings

U.S. Urolithiasis Management Devices Market Insight

The U.S. urolithiasis management devices market captured the largest revenue share of 79% in North America in 2025, fueled by the high prevalence of kidney stone disease and strong adoption of advanced minimally invasive treatment procedures. Patients and healthcare providers are increasingly prioritizing effective stone management through ESWL, laser lithotripsy, and ureteroscopy systems due to their higher precision and faster recovery outcomes. The growing focus on outpatient-based procedures, combined with robust healthcare infrastructure and high procedural volumes, further propels the market. Moreover, continuous technological advancements in laser systems and endoscopic devices are significantly contributing to the market’s expansion.

Europe Urolithiasis Management Devices Market Insight

The Europe urolithiasis management devices market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by rising kidney stone incidence and increasing preference for minimally invasive urological procedures. The region benefits from strong healthcare systems, established reimbursement structures, and growing adoption of advanced lithotripsy and endoscopic technologies in hospitals. In addition, increasing awareness of early diagnosis and effective stone treatment is fostering higher procedural uptake across both public and private healthcare facilities.

United Kingdom Urolithiasis Management Devices Market Insight

The U.K. urolithiasis management devices market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by rising kidney stone cases and increasing demand for minimally invasive and outpatient treatment options. Growing pressure on the National Health Service (NHS) to improve efficiency is encouraging adoption of advanced ESWL and ureteroscopy systems. In addition, rising preference for faster recovery and reduced hospital stay is further supporting market growth across hospitals and specialized urology centers.

Germany Urolithiasis Management Devices Market Insight

The Germany urolithiasis management devices market is expected to expand at a considerable CAGR during the forecast period, fueled by strong healthcare infrastructure, high technological adoption, and increasing use of laser-based lithotripsy systems. The country’s emphasis on precision medicine and minimally invasive surgery is driving adoption of advanced intracorporeal lithotripsy and digital ureteroscopy solutions. Furthermore, well-developed hospital facilities and a strong focus on clinical efficiency are supporting wider integration of modern urology devices.

Asia-Pacific Urolithiasis Management Devices Market Insight

The Asia-Pacific urolithiasis management devices market is poised to grow at the fastest CAGR of 9.6% during the forecast period of 2026 to 2033, driven by rising kidney stone prevalence, rapid urbanization, and improving healthcare access. Increasing adoption of modern urology procedures in countries such as China, India, and Japan is significantly boosting demand for ESWL, lithotripsy, and ureteroscopy devices. In addition, expanding hospital infrastructure, rising medical tourism, and increasing affordability of minimally invasive treatments are accelerating market growth across the region.

Japan Urolithiasis Management Devices Market Insight

The Japan urolithiasis management devices market is gaining momentum due to advanced healthcare infrastructure, high technological adoption, and strong preference for minimally invasive surgical procedures. Increasing integration of digital imaging and laser-based lithotripsy systems is improving procedural accuracy and treatment outcomes. Moreover, the country’s aging population is driving demand for safer, low-risk, and faster-recovery kidney stone treatment options across hospitals and specialized clinics.

India Urolithiasis Management Devices Market Insight

The India urolithiasis management devices market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to rising kidney stone prevalence, rapid urbanization, and expanding access to healthcare services. Growing awareness of minimally invasive treatment options and increasing availability of cost-effective lithotripsy and ureteroscopy devices are supporting strong market growth. In addition, government initiatives promoting healthcare infrastructure development and the rapid expansion of private hospitals and diagnostic centers are significantly driving adoption of advanced urology devices across the country.

Urolithiasis Management Devices Market Share

The Urolithiasis Management Devices industry is primarily led by well-established companies, including:

- Medtronic (Ireland)

- Siemens Healthineers AG (Germany)

- Boston Scientific Corporation (U.S.)

- Olympus Corporation (Japan)

- Cook (U.S.)

- Karl Storz SE & Co. KG (Germany)

- Richard Wolf GmbH (Germany)

- Dornier MedTech GmbH (Germany)

- EDAP TMS S.A. (France)

- EMS Electro Medical Systems SA (Switzerland)

- Storz Medical AG (Switzerland)

- Coloplast A/S (Denmark)

- Allengers Medical Systems Limited (India)

- DirexGroup SA (Germany)

- Elmed Medical Systems Ltd. (Turkey)

- Lumenis Ltd. (Israel)

- C. R. Bard Inc. (U.S.)

- Stryker (U.S.)

- Medispec Ltd. (Israel)

- Allium Medical Solutions Ltd. (Israel)

What are the Recent Developments in Global Urolithiasis Management Devices Market?

- In March 2026, Boston Scientific received FDA 510(k) clearance for its Asurys Fluid Management System, designed to improve irrigation control and intrarenal pressure monitoring during ureteroscopy-based kidney stone procedures. The system enhances safety and procedural efficiency when used alongside LithoVue Elite ureteroscopes, strengthening integrated minimally invasive stone management workflows. This development highlights the growing focus on precision and real-time monitoring in endourology

- In February 2024, Olympus received FDA clearance for its RenaFlex single-use flexible ureteroscope, developed for kidney stone diagnosis and treatment through minimally invasive ureteroscopy procedures. The device offers high-definition imaging and eliminates cross-contamination risks associated with reusable scopes. This launch reflects the increasing shift toward disposable endoscopic devices in urology practice

- In January 2024, Medtronic announced regulatory approval for its advanced ESWL-based lithotripsy system designed for non-invasive kidney stone fragmentation. The system improves shock wave precision and treatment efficiency, supporting broader adoption of extracorporeal shock wave lithotripsy in hospitals. This development strengthens Medtronic’s position in energy-based urology treatment solutions

- In June 2023, Boston Scientific expanded its kidney stone management portfolio through collaboration initiatives focused on next-generation ureteroscopy technologies with enhanced imaging and navigation capabilities. The effort aims to improve visualization and access in complex urinary tract stone cases. This reflects the industry’s increasing focus on integrated digital endoscopic solutions for urology

- In May 2022, Dornier MedTech received regulatory clearance for its AXIS II URS SLIM ureteroscope, designed for improved maneuverability and precision in minimally invasive kidney stone removal procedures. The device enhances access to difficult anatomical regions and supports high-definition visualization during surgery. This development supports the ongoing shift toward advanced, compact endoscopic systems in urology care

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.