Global Vacuum Packaging Market

Market Size in USD Billion

CAGR :

%

USD

23.27 Billion

USD

34.52 Billion

2025

2033

USD

23.27 Billion

USD

34.52 Billion

2025

2033

| 2026 –2033 | |

| USD 23.27 Billion | |

| USD 34.52 Billion | |

| % | |

|

Vacuum Packaging Market Size

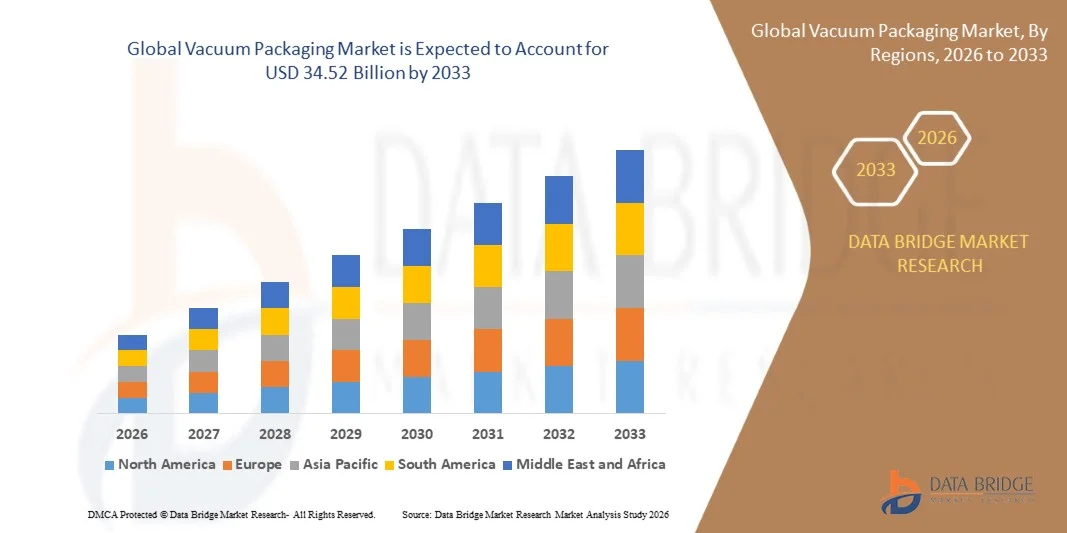

- The global vacuum packaging market size was valued at USD 23.27 billion in 2025 and is expected to reach USD 34.52 billion by 2033, at a CAGR of 5.05% during the forecast period

- The market growth is largely fueled by the rising demand for extended shelf life and improved food preservation across the global food supply chain, leading to increased adoption of vacuum packaging in processed, frozen, and ready-to-eat food categories

- Furthermore, growing consumer preference for hygienic, contamination-free, and convenience-oriented packaged food products is establishing vacuum packaging as a preferred solution for modern food storage and distribution systems. These converging factors are accelerating the uptake of vacuum packaging solutions, thereby significantly boosting the industry’s growth

Vacuum Packaging Market Analysis

- Vacuum packaging is a preservation technique that removes air from packaging before sealing, thereby reducing oxidation, microbial growth, and moisture-related spoilage while extending product shelf life across food and non-food applications

- The escalating demand for vacuum packaging is primarily fueled by the expansion of the food processing industry, increasing consumption of packaged meat and seafood, and rising emphasis on reducing food waste through advanced packaging technologies

- North America dominated the vacuum packaging market with a share of 37.6% in 2025, due to strong demand for packaged food, convenience products, and advanced food preservation technologies

- Asia-Pacific is expected to be the fastest growing region in the vacuum packaging market during the forecast period due to rapid urbanization, rising disposable incomes, and expanding food processing industries in countries such as China, India, and Japan

- Flexible packaging segment dominated the market with a market share of 78.93% in 2025, due to its lightweight nature, cost efficiency, and ease of storage and transportation. It is widely used in food applications due to its ability to extend shelf life while reducing material usage. Flexible formats also support high-speed automated packaging processes, improving production efficiency

Report Scope and Vacuum Packaging Market Segmentation

|

Attributes |

Vacuum Packaging Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Vacuum Packaging Market Trends

“Increasing Adoption of Sustainable and High-Barrier Vacuum Packaging Materials”

- A significant trend in the vacuum packaging market is the increasing shift toward sustainable, recyclable, and high-barrier packaging materials, driven by rising environmental regulations and consumer demand for eco-friendly food packaging solutions. This trend is reshaping packaging design strategies, encouraging manufacturers to develop multilayer films that maintain oxygen and moisture resistance while reducing environmental impact

- For instance, companies such as Coveris Holdings SA have introduced recyclable monoflex thermoform packaging films designed with mono-material structures to support circular packaging initiatives. Such innovations enhance sustainability performance while maintaining sealing strength and product protection in vacuum packaging applications

- The adoption of high-barrier vacuum packaging materials is growing rapidly as food manufacturers prioritize extended shelf life and reduced spoilage in meat, seafood, and dairy products. This is strengthening the use of advanced polymer films that offer superior protection against oxygen and external contaminants

- The demand for lightweight and resource-efficient packaging is also increasing as retailers and food processors aim to reduce packaging waste and logistics costs. This is leading to wider use of thinner yet stronger vacuum films that maintain product integrity during storage and transportation

- The integration of recyclable and bio-based materials is gaining momentum across developed markets, supported by stricter environmental compliance frameworks and corporate sustainability commitments. This is encouraging continuous innovation in material science within the vacuum packaging industry

- The market is witnessing strong transformation as manufacturers invest in next-generation film technologies that balance performance, cost efficiency, and environmental responsibility. This rising focus on sustainable packaging solutions is reinforcing long-term structural growth in the vacuum packaging market

Vacuum Packaging Market Dynamics

Driver

“Rising Demand for Extended Shelf Life and Food Preservation Efficiency”

- The rising demand for extended shelf life and improved food preservation efficiency is a key driver of the vacuum packaging market, supported by increasing consumption of processed, frozen, and ready-to-eat food products. This demand is pushing food manufacturers to adopt vacuum packaging solutions that reduce oxidation, microbial growth, and spoilage while maintaining product quality

- For instance, Sealed Air Corporation provides advanced vacuum packaging systems widely used in meat and poultry processing industries to enhance freshness retention and reduce food waste. These solutions enable food producers to maintain consistent quality across long distribution cycles and global supply chains

- The expansion of global food supply chains and cross-border trade in perishable goods is further increasing reliance on vacuum packaging technologies. This is helping manufacturers maintain hygiene standards and product integrity during long-distance transportation

- The growing urban population and changing dietary habits are driving higher consumption of packaged foods with longer shelf stability. This is encouraging food processors to adopt vacuum packaging as a standard preservation method across multiple product categories

- The continuous need for safe, fresh, and long-lasting food products is reinforcing the importance of vacuum packaging systems in modern food processing and distribution networks. This sustained demand is significantly contributing to overall market expansion

Restraint/Challenge

“High Cost of Advanced Vacuum Packaging Machinery and Materials”

- The vacuum packaging market faces challenges due to the high cost of advanced packaging machinery and specialized high-barrier materials, which increases initial investment requirements for manufacturers. This cost burden limits adoption among small and medium-sized food processing companies, particularly in developing regions

- For instance, companies such as Multivac Group provide high-end thermoforming vacuum packaging machines that require significant capital investment and technical expertise for installation and operation. These systems, while highly efficient, present affordability challenges for smaller production units

- The use of advanced multilayer films and specialized barrier materials also increases overall packaging costs, impacting profit margins for manufacturers. This creates pricing pressure across the supply chain, especially in cost-sensitive food segments

- Maintenance and operational costs associated with automated vacuum packaging systems further add to the financial burden. Regular servicing and skilled labor requirements increase long-term operational expenditures

- The market continues to face cost-related constraints that affect large-scale adoption, particularly in emerging economies. These financial challenges remain a key factor influencing investment decisions in vacuum packaging technologies

Vacuum Packaging Market Scope

The market is segmented on the basis of material type, machinery, process, packaging, and application.

- By Material Type

On the basis of material type, the vacuum packaging market is segmented into polyethylene, polypropylene, polyamide, ethylene vinyl alcohol, and others. The polyethylene segment dominated the largest market revenue share in 2025, driven by its cost-effectiveness, high flexibility, and extensive use in food packaging applications. Manufacturers prefer polyethylene due to its strong sealing properties and compatibility with high-volume production lines. It also offers good moisture resistance, making it suitable for perishable food products. The widespread availability and ease of processing further strengthen its dominance across retail and industrial packaging.

The ethylene vinyl alcohol (EVOH) segment is anticipated to witness the fastest growth rate from 2026 to 2033, driven by rising demand for high-barrier packaging solutions. EVOH is increasingly used to enhance oxygen resistance and extend product shelf life, especially in processed food and pharmaceutical packaging. Its ability to maintain product freshness under varying storage conditions supports its adoption in premium applications. Growing focus on reducing food waste and improving preservation efficiency is accelerating its uptake. The material’s compatibility with multilayer structures further supports its rapid expansion.

- By Machinery

On the basis of machinery, the vacuum packaging market is segmented into thermoformers, external vacuum sealers, tray sealing machines, and others. The thermoformers segment held the largest market revenue share in 2025, driven by its high-speed production capability and efficiency in large-scale food processing operations. These machines are widely used in industrial packaging lines due to their ability to form, fill, and seal in a continuous process. Their strong automation features reduce labor dependency and improve output consistency. The growing demand for packaged meat and dairy products further supports their dominance in the market.

The tray sealing machines segment is expected to witness the fastest growth rate from 2026 to 2033, fueled by increasing demand for ready-to-eat meals and convenience food packaging. These machines offer strong sealing integrity and visual appeal, making them suitable for retail-ready packaging formats. Their adaptability to different tray sizes and materials enhances operational flexibility for manufacturers. Rising consumption of portion-controlled meals in urban markets is also contributing to growth. The expansion of food delivery and supermarket chains further strengthens adoption.

- By Process

On the basis of process, the vacuum packaging market is segmented into skin vacuum packaging, shrink vacuum packaging, and others. The shrink vacuum packaging segment dominated the largest market revenue share in 2025, driven by its cost efficiency and widespread use in bulk food packaging. This process ensures tight sealing and product protection during transportation and storage. It is widely adopted in meat, seafood, and dairy packaging due to its ability to reduce spoilage. Strong compatibility with automated packaging lines further supports its leading position. The process remains a preferred choice for large-scale food processors.

The skin vacuum packaging segment is projected to witness the fastest growth rate from 2026 to 2033, driven by rising demand for premium product presentation and extended shelf life. This method enhances visual appeal by tightly conforming the film to the product surface, improving shelf visibility in retail environments. It is increasingly used for high-value foods such as fresh meat and seafood. Growing consumer preference for attractive and hygienic packaging formats supports adoption. Advancements in packaging films are further accelerating market expansion.

- By Packaging

On the basis of packaging, the vacuum packaging market is segmented into rigid packaging, flexible packaging, and semi-rigid packaging. The flexible packaging segment dominated the largest market revenue share of 78.93% in 2025, driven by its lightweight nature, cost efficiency, and ease of storage and transportation. It is widely used in food applications due to its ability to extend shelf life while reducing material usage. Flexible formats also support high-speed automated packaging processes, improving production efficiency. Strong demand from retail and e-commerce food distribution further reinforces its dominance. The segment continues to benefit from sustainability-driven material innovations.

The semi-rigid packaging segment is expected to witness the fastest growth rate from 2026 to 2033, fueled by increasing demand for ready meal trays and premium packaged foods. It offers a balance between durability and presentation, making it ideal for retail display applications. The segment is gaining traction in chilled and frozen food categories due to its structural strength. Rising urbanization and changing consumption patterns are accelerating adoption. Growth in organized retail and convenience food markets further supports expansion.

- By Application

On the basis of application, the vacuum packaging market is segmented into food, pharmaceuticals, industrial goods, and others. The food segment dominated the largest market revenue share in 2025, driven by strong demand for extended shelf life and reduced food spoilage. Vacuum packaging is widely used for meat, seafood, dairy, and processed foods due to its ability to preserve freshness and flavor. Expanding global food distribution networks further strengthen its dominance. Increasing consumer preference for packaged and ready-to-eat foods continues to support growth. The segment remains central to overall market expansion.

The pharmaceuticals segment is anticipated to witness the fastest growth rate from 2026 to 2033, driven by rising demand for contamination-free and moisture-resistant packaging solutions. Vacuum packaging helps maintain drug stability and protects sensitive formulations during storage and transport. Increasing regulatory focus on product safety and quality further supports adoption in this segment. Growth in biologics and temperature-sensitive drugs is also contributing to demand. Expansion of global pharmaceutical manufacturing is accelerating the segment’s rapid growth trajectory.

Vacuum Packaging Market Regional Analysis

- North America dominated the vacuum packaging market with the largest revenue share of 37.6% in 2025, driven by strong demand for packaged food, convenience products, and advanced food preservation technologies

- The region benefits from a highly developed food processing industry and widespread adoption of automated packaging systems. Consumers prioritize longer shelf life, hygiene, and product safety, which supports consistent demand for vacuum packaging solutions

- High penetration of modern retail chains and e-commerce grocery platforms further strengthens market growth. Increasing focus on reducing food waste and improving supply chain efficiency continues to reinforce regional dominance

U.S. Vacuum Packaging Market Insight

The U.S. vacuum packaging market captured the largest revenue share in North America in 2025, driven by high consumption of packaged meat, seafood, and ready-to-eat meals. The country’s advanced food manufacturing infrastructure supports large-scale adoption of vacuum packaging technologies across industrial operations. Strong demand from supermarkets, quick-service restaurants, and online grocery delivery platforms further accelerates market expansion. Increasing consumer preference for extended shelf life and contamination-free food products is also contributing to growth. The presence of major packaging equipment manufacturers continues to strengthen market development.

Europe Vacuum Packaging Market Insight

The Europe vacuum packaging market is projected to expand at a substantial CAGR throughout the forecast period, driven by stringent food safety regulations and rising demand for sustainable packaging solutions. The region places strong emphasis on reducing food waste, which supports adoption of high-barrier vacuum packaging materials. Growing consumption of processed and convenience foods is further accelerating demand across retail and foodservice sectors. Technological advancements in packaging machinery are also improving efficiency and product protection. The market continues to benefit from strong regulatory support for recyclable and eco-friendly packaging formats.

U.K. Vacuum Packaging Market Insight

The U.K. vacuum packaging market is anticipated to grow at a notable CAGR during the forecast period, driven by increasing demand for fresh and packaged food products across urban populations. Rising preference for convenience foods and meal kits is supporting wider adoption of vacuum packaging solutions. Retail expansion and growth in online grocery delivery services are further boosting market penetration. Strong focus on food hygiene and shelf-life extension continues to encourage usage across food processing industries. Increasing sustainability awareness is also influencing packaging material selection.

Germany Vacuum Packaging Market Insight

The Germany vacuum packaging market is expected to expand at a considerable CAGR during the forecast period, driven by strong industrial food processing capabilities and high demand for quality preservation solutions. The country’s emphasis on efficiency and sustainability supports adoption of advanced vacuum packaging technologies. Growing consumption of meat, dairy, and processed food products is further strengthening market demand. Automation in packaging operations is widely implemented across manufacturing facilities. Increasing focus on recyclable materials and waste reduction continues to shape market growth.

Asia-Pacific Vacuum Packaging Market Insight

The Asia-Pacific vacuum packaging market is poised to grow at the fastest CAGR from 2026 to 2033, driven by rapid urbanization, rising disposable incomes, and expanding food processing industries in countries such as China, India, and Japan. Increasing demand for packaged and ready-to-eat food products is significantly boosting adoption across the region. The growth of modern retail infrastructure and e-commerce food delivery platforms is further accelerating market expansion. Government initiatives supporting food safety and industrial modernization are also contributing to demand. The region is emerging as a major manufacturing hub for vacuum packaging materials and machinery, improving affordability and accessibility.

Japan Vacuum Packaging Market Insight

The Japan vacuum packaging market is gaining momentum due to strong demand for high-quality, hygienically packaged food products and advanced preservation technologies. The country’s aging population and preference for convenient meal solutions are supporting increased adoption of vacuum packaging. High standards for food safety and quality control further strengthen market penetration. Technological advancements in packaging machinery and automation are widely implemented across the food industry. Integration with modern retail systems continues to enhance efficiency and product freshness.

China Vacuum Packaging Market Insight

The China vacuum packaging market accounted for the largest market revenue share in Asia-Pacific in 2025, driven by rapid urbanization, expanding food processing industries, and strong consumer demand for packaged food products. The country’s growing middle-class population is increasing consumption of meat, seafood, and convenience foods. Strong domestic manufacturing capabilities and cost-effective production are supporting large-scale adoption. Expansion of e-commerce grocery platforms and modern retail chains is further boosting demand. Government focus on food safety and supply chain modernization continues to support market growth.

Vacuum Packaging Market Share

The vacuum packaging industry is primarily led by well-established companies, including:

- Amcor plc (Switzerland)

- Berry Global, Inc. (U.S.)

- CVP Systems, Inc. (U.S.)

- Sealed Air (U.S.)

- Linpac Packaging Limited (U.K.)

- Multisorb (U.S.)

- Coveris (Austria)

- ULMA Packaging (Spain)

- Sealer Sales, Inc. (U.S.)

- US Packaging & Wrapping LLC (U.S.)

- Kite Packaging Ltd (U.K.)

Latest Developments in Global Vacuum Packaging Market

- In December 2025, Amcor announced a USD 180 million expansion of its Ghent, Belgium flexible packaging facility, adding three high-speed thermoform lines scheduled for completion by Q3 2027. This development is expected to significantly strengthen Amcor’s production capacity in high-performance vacuum packaging solutions, particularly for food and protein applications. The expansion will enhance operational efficiency, support rising demand for automated packaging systems, and reinforce the company’s competitive position in the European vacuum packaging market through increased scalability and technological advancement

- In December 2023, Südpack introduced the Multifol Extreme packaging film designed specifically for fish products, offering high protection performance despite reduced material thickness. The film is optimized for use in Modified Atmosphere Packaging (MAP) and vacuum packaging, improving food safety and extending shelf life for seafood products. This innovation is expected to positively influence the vacuum packaging market by enhancing sustainability through material reduction while maintaining strong barrier properties. It also supports the growing demand for advanced packaging solutions in the seafood industry

- In December 2023, Coveris Holdings SA launched a recyclable monoflex thermoform packaging film developed using high-performance mono-material structures. This eco-friendly solution is designed to reduce environmental impact while maintaining strong sealing and durability characteristics required for vacuum packaging applications. The development is expected to accelerate the shift toward sustainable packaging in the food sector, driven by increasing regulatory pressure and consumer preference for recyclable materials. It further strengthens the adoption of low-carbon footprint solutions across vacuum packaging markets

- In July 2023, Klöckner Pentaplast, in collaboration with Dow, introduced kp Flexivac, a fully recyclable vacuum film engineered for high tensile strength and superior hermetic sealing performance. The film is particularly suited for bone-in cuts of fresh meat and poultry, ensuring enhanced product protection and extended shelf life. This development is expected to drive greater adoption of recyclable vacuum packaging solutions in the meat industry. It also supports the broader transition toward circular packaging systems within the vacuum packaging market

- In May 2023, Amcor acquired Moda Systems, a company specializing in advanced protein packaging machinery and automated packaging solutions. This acquisition strengthens Amcor’s vacuum packaging capabilities across poultry, meat, dairy, and convenience food segments. The integration of Moda Systems’ technology is expected to enhance innovation in high-efficiency packaging systems and improve production automation. It further reinforces Amcor’s leadership position in the global vacuum packaging market by expanding its technological portfolio and end-use application reach

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Vacuum Packaging Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Vacuum Packaging Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Vacuum Packaging Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.