Global Veterinary Orthopedic Implants Market

Market Size in USD Million

CAGR :

%

USD

283.06 Million

USD

514.30 Million

2025

2033

USD

283.06 Million

USD

514.30 Million

2025

2033

| 2026 –2033 | |

| USD 283.06 Million | |

| USD 514.30 Million | |

| % | |

|

Veterinary Orthopedic Implants Market Size

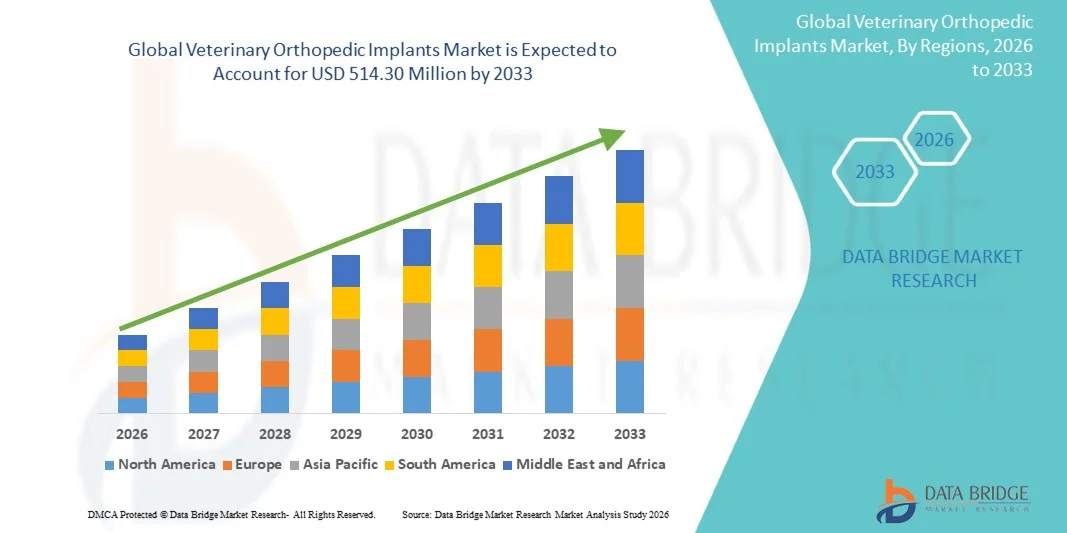

- The global veterinary orthopedic implants market size was valued at USD 283.06 million in 2025and is expected to reach USD 514.30 million by 2033, at a CAGR of 7.75% during the forecast period

- The market growth is largely fueled by the rising prevalence of orthopedic conditions in companion animals and increasing incidence of trauma, fractures, and degenerative joint diseases, alongside growing pet ownership and expenditure on advanced veterinary care

- Furthermore, continuous advancements in veterinary surgical techniques, biomaterials, and implant technologies, coupled with the expanding availability of specialized veterinary orthopedic services and growing awareness of animal health and mobility restoration, are significantly boosting the adoption of orthopedic implants, thereby accelerating the industry's growth

Veterinary Orthopedic Implants Market Analysis

- Veterinary orthopedic implants, including plates, screws, pins, and joint reconstruction devices, are increasingly critical in modern veterinary surgery for treating fractures, ligament injuries, and degenerative musculoskeletal conditions in companion and large animals, enabling improved mobility and quality of life

- The escalating demand for veterinary orthopedic implants is primarily driven by rising pet ownership, increasing expenditure on advanced animal healthcare, higher incidence of trauma and orthopedic disorders, and growing awareness among pet owners regarding specialized surgical treatment options

- North America dominated the veterinary orthopedic implants market with the largest revenue share of 42.9% in 2025, supported by a highly developed veterinary healthcare infrastructure, strong adoption of advanced surgical procedures, and significant presence of specialized veterinary clinics and implant manufacturers, particularly in the U.S.

- Asia-Pacific is expected to be the fastest growing region in the veterinary orthopedic implants market during the forecast period due to increasing companion animal population, rising disposable incomes, rapid urbanization, and improving access to veterinary surgical care and specialty services

- Plates segment dominated the veterinary orthopedic implants market with the largest market share of 50.4% in 2025, attributed to their widespread use in fracture fixation procedures, ease of application, versatility across animal sizes, and strong clinical preference in both routine and complex orthopedic surgeries

Report Scope and Veterinary Orthopedic Implants Market Segmentation

|

Attributes |

Veterinary Orthopedic Implants Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

|

|

Market Opportunities |

· Expanding adoption of 3D-printed, patient-specific veterinary implants · Growing penetration of pet insurance and financing options |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Veterinary Orthopedic Implants Market Trends

“Advancement Toward Biocompatible and 3D-Printed Implant Solutions”

- A significant and accelerating trend in the global veterinary orthopedic implants market is the shift toward biocompatible materials and patient-specific 3D-printed implants designed to improve surgical precision and recovery outcomes in animals

- For instance, companies and veterinary hospitals are increasingly adopting titanium and polymer-based customized implants produced through additive manufacturing for complex fracture and joint repair cases in companion animals

- 3D printing in veterinary orthopedics enables precise anatomical matching, reduced surgical time, and improved implant fit, while also minimizing post-operative complications and implant rejection risks in animals

- Furthermore, growing integration of advanced imaging technologies such as CT and MRI with implant design software is enabling veterinarians to create highly accurate pre-surgical planning models for orthopedic procedures

- Increasing adoption of minimally invasive orthopedic surgical techniques is reducing recovery time and post-operative complications, further supporting the shift toward advanced implant-based interventions in veterinary care

- This trend toward customized, technology-driven implant solutions is reshaping veterinary orthopedic surgery practices by improving treatment success rates and expanding options for complex cases in both small and large animals

- The demand for advanced veterinary orthopedic implants is growing rapidly across companion animal hospitals and specialty clinics as pet owners increasingly seek advanced, human-grade surgical care for their animals

Veterinary Orthopedic Implants Market Dynamics

Driver

“Increasing Pet Humanization and Rising Demand for Advanced Veterinary Surgery”

- The increasing humanization of pets, coupled with rising expenditure on advanced veterinary healthcare, is a significant driver for the growing demand for veterinary orthopedic implants in complex fracture and joint repair procedures

- For instance, in 2025, several veterinary hospital networks expanded orthopedic surgery capabilities to include advanced implant-based treatments for cruciate ligament repair and hip dysplasia in dogs and cats

- As pet owners increasingly view animals as family members, there is a growing willingness to invest in advanced surgical interventions, driving higher adoption of orthopedic implants in veterinary practices

- Furthermore, rising incidence of obesity-related joint disorders and trauma cases in companion animals is increasing the need for surgical orthopedic interventions supported by implants

- Expanding veterinary health insurance penetration is improving affordability of advanced orthopedic procedures, thereby supporting higher treatment volumes in developed and emerging markets

- The expanding availability of specialized veterinary orthopedic surgeons and improved clinical infrastructure is further accelerating implant utilization across developed and emerging markets

- Growing awareness of animal mobility restoration and quality-of-life improvement is making implant-based orthopedic treatment a preferred standard of care in veterinary medicine

Restraint/Challenge

“High Treatment Cost and Limited Access to Specialized Veterinary Infrastructure”

- The high cost of veterinary orthopedic implant procedures remains a significant challenge, limiting adoption among pet owners in price-sensitive and developing regions despite rising demand for advanced care

- For instance, complex fracture repair surgeries involving implants can be significantly expensive due to surgical expertise requirements, implant costs, and post-operative care needs

- Limited availability of specialized veterinary orthopedic surgeons and advanced surgical infrastructure in rural and underdeveloped regions restricts market penetration and timely treatment access

- Furthermore, variability in regulatory standards for veterinary implants across regions can delay product approvals and increase compliance complexity for manufacturers

- Lack of standardized implant pricing and reimbursement frameworks across veterinary healthcare systems further contributes to uneven adoption rates globally

- The need for highly skilled surgical handling and post-operative monitoring also increases overall treatment dependency on specialized veterinary centers, limiting mass accessibility

- Addressing cost barriers through insurance coverage expansion, financing options, and broader clinical infrastructure development will be essential for sustained market growth

Veterinary Orthopedic Implants Market Scope

The market is segmented on the basis of product, animal type, implant type, and end user.

- By Product

On the basis of product, the veterinary orthopedic implants market is segmented into plates, screws, jigs, pins and wires. The plates segment dominated the market with the largest revenue share of 50.4% in 2025, driven by their extensive use in fracture fixation and reconstruction procedures across small and large animals. Plates provide strong mechanical stability and are widely preferred in complex orthopedic surgeries such as long bone fractures in dogs and cats. Their versatility in combination with screws and compatibility with locking systems further strengthens their adoption in veterinary hospitals. In addition, continuous improvements in titanium-based plates and locking compression designs are enhancing surgical outcomes, supporting their dominance in the market. Increasing incidence of traumatic injuries in companion animals is further reinforcing demand for plate-based fixation systems.

The pins and wires segment is anticipated to witness the fastest growth rate of 11% from 2026 to 2033, driven by their cost-effectiveness and growing use in minimally invasive and temporary fixation procedures. These implants are widely used in pediatric and small animal orthopedic cases where less rigid fixation is required. Their simplicity of application and reduced surgical time make them highly suitable for emergency trauma cases in veterinary clinics. Increasing adoption in emerging markets, where affordability is a key factor, is also boosting growth. Furthermore, advancements in stainless steel and bio-compatible wire materials are improving clinical outcomes and driving wider acceptance.

- By Animal

On the basis of animal, the veterinary orthopedic implants market is segmented into dog, cat, horse, and others. The dog segment dominated the market with the largest revenue share of 60% in 2025, driven by the high global population of companion dogs and their higher susceptibility to fractures, ligament injuries, and joint disorders such as cranial cruciate ligament rupture. Dogs are more frequently exposed to trauma due to outdoor activity, increasing the need for orthopedic interventions. Strong pet humanization trends and willingness of owners to spend on advanced surgical procedures further support segment dominance. Veterinary hospitals also report a higher volume of orthopedic surgeries in dogs compared to other animals. Continuous innovation in breed-specific implant designs is further strengthening market leadership of this segment.

The cat segment is expected to witness the fastest growth rate of 12% from 2026 to 2033, driven by rising adoption of cats as companion animals in urban households. Increasing awareness of feline orthopedic conditions, including fractures caused by falls and degenerative joint diseases, is boosting treatment rates. Improved diagnostic capabilities and growing availability of specialized feline orthopedic care are supporting higher implant adoption. Cats are also benefiting from advancements in minimally invasive surgical techniques, reducing recovery time. Rising veterinary expenditure per cat in developed and emerging markets is further accelerating growth in this segment.

- By Type

On the basis of type, the market is segmented into advanced locking plate system, tibial plateau leveling osteotomy (TPLO) implants, tibial tuberosity advancement (TTA) implants, total elbow replacement, total hip replacement, total knee replacement, and trauma fixations. The advanced locking plate system segment dominated the market with the largest revenue share of 32% in 2025, driven by its superior biomechanical stability and ability to treat complex fractures in both small and large animals. These systems are widely preferred due to their angular stability, reduced risk of implant loosening, and compatibility with osteoporotic bone conditions in older animals. Veterinary surgeons increasingly rely on locking plate systems for high-precision fracture repair procedures. Growing adoption of titanium locking plates and improved surgical instrumentation further supports segment dominance. High clinical success rates and versatility across multiple fracture types make it the most widely used implant type globally.

The tibial plateau leveling osteotomy (TPLO) implants segment is expected to witness the fastest growth rate of 13% from 2026 to 2033, driven by rising cases of cranial cruciate ligament rupture in dogs. TPLO procedures are increasingly considered the gold standard for treating ligament injuries in active and large-breed dogs. Growing awareness among pet owners regarding long-term mobility restoration is boosting procedure volumes. Advancements in surgical techniques and implant design are improving recovery outcomes and reducing complications. Increasing availability of specialized orthopedic veterinary surgeons is further accelerating adoption of TPLO implants globally.

- By End User

On the basis of end user, the market is segmented into veterinary hospitals, veterinary clinics, veterinary surgical centers, and others. The veterinary hospitals segment dominated the market with the largest revenue share of 52% in 2025, driven by their advanced surgical infrastructure, availability of specialized orthopedic surgeons, and capacity to handle complex implant-based procedures. These hospitals are equipped with advanced diagnostic imaging systems and operating facilities required for high-precision orthopedic surgeries. They also handle a high patient volume of severe trauma and chronic orthopedic cases requiring implants. Strong referral networks from clinics further increase patient inflow. Continuous investment in advanced veterinary surgical technologies is strengthening hospital dominance in this market.

The veterinary surgical centers segment is anticipated to witness the fastest growth rate of 12% from 2026 to 2033, driven by increasing specialization in orthopedic and minimally invasive veterinary procedures. These centers are gaining popularity due to focused expertise, shorter waiting times, and advanced surgical capabilities. Rising demand for high-end elective orthopedic surgeries such as hip and knee replacements in pets is supporting growth. Increasing collaboration between general clinics and specialized surgical centers is improving patient access to advanced implant procedures. Expanding presence of standalone veterinary specialty centers in urban regions is further accelerating segment growth globally.

Veterinary Orthopedic Implants Market Regional Analysis

- North America dominated the veterinary orthopedic implants market with the largest revenue share of 42.9% in 2025, supported by a highly developed veterinary healthcare infrastructure, strong adoption of advanced surgical procedures, and significant presence of specialized veterinary clinics and implant manufacturers

- Consumers and pet owners in the region highly value advanced orthopedic treatments, including fracture fixation, joint replacement, and minimally invasive surgical solutions, supported by strong willingness to spend on premium veterinary care

- This widespread adoption is further supported by high pet ownership rates, strong penetration of pet insurance, advanced veterinary specialization, and the presence of leading implant manufacturers and specialty animal hospitals, establishing veterinary orthopedic implants as a standard of care in complex animal orthopedic cases

U.S. Veterinary Orthopedic Implants Market Insight

The U.S. veterinary orthopedic implants market captured the largest revenue share of 85% within North America in 2025, driven by advanced veterinary clinical infrastructure and strong penetration of pet insurance. High pet ownership and increasing willingness to spend on specialized surgical care are significantly boosting demand for implants used in fracture fixation and joint reconstruction procedures. The country benefits from early adoption of innovative technologies such as locking plate systems, TPLO implants, and 3D-printed orthopedic solutions. Furthermore, the presence of leading global veterinary device manufacturers and specialty animal hospitals continues to strengthen market expansion across both companion and performance animals.

Europe Veterinary Orthopedic Implants Market Insight

The Europe veterinary orthopedic implants market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by rising awareness of animal welfare and increasing demand for advanced veterinary surgical care. Strict regulatory standards and high clinical quality expectations are encouraging the use of certified, biocompatible implant systems. Growing pet ownership and increasing incidence of orthopedic disorders in aging companion animals are also supporting market growth. Furthermore, expansion of veterinary referral centers and growing adoption of minimally invasive orthopedic procedures are accelerating implant usage across both companion and equine applications in the region.

U.K. Veterinary Orthopedic Implants Market Insight

The U.K. veterinary orthopedic implants market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by rising expenditure on companion animal healthcare and increasing demand for advanced orthopedic surgeries. Concerns regarding mobility disorders, fractures, and ligament injuries in pets are encouraging adoption of implant-based treatments. The country’s strong network of veterinary clinics and referral hospitals supports high procedure volumes. In addition, growing integration of pet insurance coverage is improving affordability of complex orthopedic surgeries, further boosting demand for implants in both urban and suburban regions.

Germany Veterinary Orthopedic Implants Market Insight

The Germany veterinary orthopedic implants market is expected to expand at a considerable CAGR during the forecast period, fueled by strong emphasis on technological innovation and high standards of veterinary care. Increasing awareness of advanced surgical solutions for fracture repair and joint replacement in companion animals is supporting market adoption. Germany’s well-established veterinary infrastructure and preference for precision-based orthopedic procedures are key growth drivers. Furthermore, rising focus on biocompatible and long-lasting implant materials, along with growing adoption of specialized veterinary orthopedic centers, is strengthening market penetration across the country.

Asia-Pacific Veterinary Orthopedic Implants Market Insight

The Asia-Pacific veterinary orthopedic implants market is poised to grow at the fastest CAGR of 12% during the forecast period of 2026 to 2033, driven by rapid urbanization, rising disposable incomes, and increasing pet adoption in countries such as China, India, and Japan. Growing awareness of advanced veterinary treatments and expanding access to specialized animal healthcare services are accelerating implant demand. In addition, the region is emerging as a key manufacturing hub for cost-effective veterinary implant systems, improving affordability and accessibility. Government initiatives supporting animal health infrastructure development are further boosting regional market growth.

Japan Veterinary Orthopedic Implants Market Insight

The Japan veterinary orthopedic implants market is gaining momentum due to its advanced veterinary healthcare system, high-tech medical culture, and increasing demand for precision-based orthopedic treatments. The country places strong emphasis on animal welfare and minimally invasive surgical procedures, supporting adoption of advanced implant technologies. Rising pet ownership among aging populations is also contributing to higher demand for orthopedic interventions. Furthermore, integration of digital imaging and surgical planning systems with implant procedures is improving clinical outcomes and driving steady market expansion in both companion animal and specialty veterinary practices.

India Veterinary Orthopedic Implants Market Insight

The India veterinary orthopedic implants market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to rapid urbanization, expanding middle-class pet ownership, and increasing awareness of advanced veterinary care. Growing incidence of trauma and orthopedic disorders in companion animals is driving demand for implant-based surgical solutions. The expansion of veterinary hospitals and specialty clinics in urban centers is improving access to orthopedic procedures. In addition, the availability of cost-effective implant systems and rising penetration of pet insurance are key factors supporting strong market growth across the country.

Veterinary Orthopedic Implants Market Share

The Veterinary Orthopedic Implants industry is primarily led by well-established companies, including:

- Movora (U.S.)

- Veterinary Orthopedic Implants (U.S.)

- BioMedtrix (U.S.)

- IMEX Veterinary, Inc. (U.S.)

- KYON AG (Switzerland)

- Arthrex Vet Systems (U.S.)

- B. Braun SE (Germany)

- Orthomed (U.K.)

- Securos Surgical (U.S.)

- Veterinary Instrumentation (U.K.)

- Rita Leibinger GmbH (Germany)

- Integra LifeSciences Corporation (U.S.)

- GerVetUSA (U.S.)

- Fusion Implants (U.S.)

- Intrauma S.p.A (Italy)

- Narang Medical Limited (India)

- GPC Medical Limited (India)

- Everost Inc. (U.S.)

- Scil Animal Care (Germany)

What are the Recent Developments in Global Veterinary Orthopedic Implants Market?

- In October 2025, Vimian Group’s veterinary division Movora strengthened its position in advanced orthopedic implant systems by expanding its total hip replacement offerings for dogs across key global markets. The development focuses on improving surgical precision, implant durability, and long-term mobility outcomes for companion animals suffering from severe hip dysplasia and trauma-related conditions

- In August 2025, Industry updates confirmed rising use of tibial plateau leveling osteotomy (TPLO) implants and bone plate systems as standard treatment for cranial cruciate ligament injuries in dogs. The report emphasized that plates continue to dominate orthopedic fixation procedures due to their versatility and mechanical stability in fracture repair cases

- In April 2024, MaxPetZ announced the integration of advanced 3D printing technology for pre-surgical planning and custom implant development in veterinary orthopedic and reconstructive procedures. The initiative focuses on creating patient-specific prosthetics and implants for complex bone deformities and fracture corrections in animals

- In April 2024, Onkos Surgical received FDA De Novo approval for its novel antibacterial coated orthopaedic implants, designed to reduce implant-associated infections in high-risk surgical cases. The technology is particularly relevant for complex bone reconstruction and revision surgeries, where infection risk is significantly higher

- In February 2024, Industry experts highlighted ongoing challenges related to limited global standardization of veterinary orthopedic implant regulations compared to human medical devices. Concerns regarding variability in implant quality and material consistency have increased focus on testing and validation processes

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.