Global Video Endoscopy Devices Market

Market Size in USD Billion

USD

52.93 Billion

USD

81.35 Billion

2025

2033

USD

52.93 Billion

USD

81.35 Billion

2025

2033

| 2026 - 2033 | |

| USD 52.93 Billion | |

| USD 81.35 Billion | |

| % | |

|

Video Endoscopy Devices Market Overview

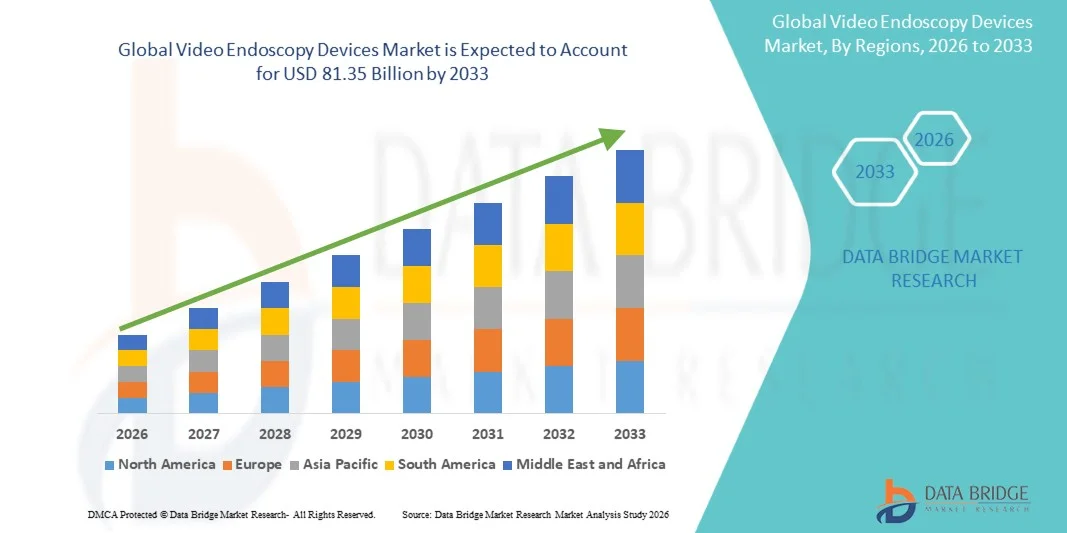

The Video Endoscopy Devices Market was valued at USD 52.93 billion in 2025 and is projected to reach USD 81.35 billion by 2033, growing at a CAGR of 5.52% from 2026 to 2033. The market is witnessing steady expansion driven by rising preference for minimally invasive surgeries, continuous improvements in high-definition imaging technologies, and growing adoption of advanced endoscopic systems across hospitals and specialty clinics.

The increasing global burden of gastrointestinal, respiratory, and urological disorders, along with a rising aging population, is significantly boosting demand for diagnostic and therapeutic endoscopy procedures. In addition, technological advancements such as 4K visualization, flexible endoscopes, capsule endoscopy, and AI-assisted image interpretation are enhancing diagnostic accuracy and procedural efficiency. Growing investments in healthcare infrastructure and the expansion of ambulatory surgical centers are further supporting the adoption of video endoscopy devices worldwide.

Key Market Trends & Insights

- North America dominated the Video Endoscopy Devices Market with the largest revenue share of 38.40% in 2025, supported by advanced healthcare infrastructure, high procedure volumes, and strong adoption of minimally invasive surgical systems.

- The Flexible Endoscopes segment led the market with a 45.48% share in 2025, driven by its widespread use in gastrointestinal, respiratory, and urology diagnostics and therapeutic procedures.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 7.5% from 2026 to 2033, fueled by rising healthcare investments, expanding hospital capacity, and growing awareness of early disease detection in emerging economies.

- Capsule Endoscope are the fastest-growing type, projected to register a CAGR of 8.1%, reflecting the surge in demand for non-invasive gastrointestinal diagnostics.

- The Biopsy Forceps segment dominated the devices category with a 30.35% revenue share in 2025, led by its critical role in tissue sampling during diagnostic endoscopy procedures.

- Reprocessing segment accounted for 55.60% of the market, preferred by the widespread use of reusable endoscopes in hospitals and diagnostic centers.

- The Bronchoscopy segment is the fastest-growing application category, with a CAGR of 8.9%, driven by the rising respiratory diseases such as COPD, lung cancer, and infections.

Market Size & Forecast

- Global Market Value (2025): USD 52.93 Billion

- Expected Market Value (2033): USD 81.35 Billion

- Forecast CAGR (2026–2033): 5.52%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia Pacific

Report Scope and Video Endoscopy Devices Market Segmentation

|

Attributes |

Video Endoscopy Devices Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Olympus Corporation (Japan) · KARL STORZ SE & Co. KG (Germany) · FUJIFILM Holdings Corporation (Japan) · HOYA Corporation (Japan) · Boston Scientific Corporation (U.S.) · Medtronic (Ireland) · Stryker (U.S.) · Smith+Nephew plc (U.K.) · CONMED Corporation (U.S.) · Ambu A/S (Denmark) · Richard Wolf GmbH (Germany) · B. Braun SE (Germany) · Schoelly Fiberoptic GmbH (Germany) · HOLOGIC, Inc. (U.S.) · Medtronic Minimally Invasive Therapies Group (U.S.) · Arthrex, Inc. (U.S.) · EndoMed Systems GmbH (Germany) · SonoScape Medical Corp. (China) · Shenzhen Mindray Bio-Medical Electronics Co., Ltd. (China) · Hunan Vathin Medical Instrument Co., Ltd. (China) |

|

Market Opportunities |

· Rising demand for AI-assisted endoscopy platforms · Expanding adoption of single-use (disposable) video endoscopes to reduce cross-contamination risks · Growing penetration of video capsule endoscopy in remote and outpatient setting |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Video Endoscopy Devices Market Trends

Trend: Expansion of AI-Guided and High-Resolution Imaging Endoscopy

Hospitals are increasingly adopting AI-assisted video endoscopy systems with HD and 4K imaging capabilities to enhance real-time lesion detection, improve diagnostic accuracy, and support early-stage disease identification in gastrointestinal and respiratory procedures. Integration of digital imaging platforms with cloud-based reporting and smart visualization tools is enabling faster clinical decision-making and standardized diagnostic workflows across healthcare facilities. For instance, AI-based endoscopy systems are being used to automatically highlight suspicious tissue patterns during colonoscopy and gastroscopy procedures, reducing missed lesion rates and improving screening efficiency.

Video Endoscopy Devices Market Dynamics

Key Market Driver: Rising Demand for Minimally Invasive Diagnostic and Surgical Procedures

The increasing preference for minimally invasive surgeries is significantly driving the adoption of video endoscopy devices, as they offer reduced patient recovery time, lower complication risks, and improved clinical outcomes compared to open surgical procedures. Growing prevalence of gastrointestinal cancers, respiratory disorders, and urological conditions is further accelerating procedure volumes in hospitals and ambulatory surgical centers. For instance, video-assisted endoscopic systems are widely used in colon cancer screening programs and laparoscopic surgeries, enabling precise internal visualization without large incisions and improving overall patient care efficiency.

Key Restraint/Challenge: High Cost of Advanced Video Endoscopy Systems and Maintenance

A major challenge in the video endoscopy devices market is the high acquisition cost of advanced systems, particularly HD, 4K, and AI-integrated platforms, along with significant expenses related to maintenance, sterilization, and upgrades. Smaller healthcare facilities and clinics often face budget constraints that limit adoption of cutting-edge endoscopic technologies despite their clinical benefits. For instance, advanced robotic and high-definition endoscopy suites require substantial capital investment and recurring service costs, making them less accessible in low- and middle-income healthcare settings, thereby slowing widespread adoption across developing regions.

Key Market Opportunity: Expansion of Disposable Endoscopy and Remote Diagnostic Platforms

The growing demand for infection-free, cost-effective, and high-efficiency diagnostic solutions is creating strong opportunities for single-use (disposable) video endoscopy devices and remote endoscopic diagnostic platforms. Healthcare systems are increasingly shifting toward disposable scopes to reduce cross-contamination risks and hospital-acquired infections, while tele-endoscopy and cloud-connected imaging systems are enabling remote consultation and diagnosis support in underserved regions. For instance, disposable bronchoscopy and gastrointestinal endoscopy devices are being adopted in emergency care and intensive care units to ensure rapid, sterile procedures without the need for reprocessing infrastructure.

Video Endoscopy Devices Market Scope

The video endoscopy devices market is segmented on the basis of type, devices, hygiene, application, and end-use.

- By Type

On the basis of type, the Video Endoscopy Devices Market is segmented into endoscope devices, flexible endoscopes, ENT endoscopes, bronchoscopes, ultrasound endoscopes, other flexible endoscopes, capsule endoscopes, robot-assisted endoscopes, and mechanical endoscopic equipment. The Flexible Endoscopes segment dominated the market with a 45.48% share in 2025, owing to its widespread use in gastrointestinal, respiratory, and urology diagnostics and therapeutic procedures. These devices offer high maneuverability, improved patient comfort, and broad clinical applicability across multiple specialties. Increasing prevalence of chronic diseases such as colorectal cancer and GERD is significantly driving procedure volumes. Continuous advancements in high-definition imaging and flexible fiber-optic technology are enhancing diagnostic precision. Hospitals and specialty clinics heavily rely on flexible endoscopes for routine and emergency diagnostics. Their cost-effectiveness compared to robotic or capsule-based systems further strengthens market dominance.

The Capsule Endoscope segment is projected to register the fastest growth at a CAGR of 8.1% from 2026 to 2033, driven by rising demand for non-invasive gastrointestinal diagnostics. These devices enable painless, swallowable imaging of the small intestine, improving patient compliance significantly. Increasing use in obscure gastrointestinal bleeding and Crohn’s disease diagnosis is supporting adoption. Technological advancements in miniaturized cameras and wireless data transmission are improving image quality and reliability. Growing preference for outpatient and home-based diagnostic procedures is further accelerating demand. Expanding availability in emerging markets is also contributing to rapid growth.

- By Devices

On the basis of devices, the Video Endoscopy Devices Market is segmented into endoscopic implants, trocars, graspers, snares, biopsy forceps, and others. The Biopsy Forceps segment dominated the market with a 30.35% share in 2025, due to its critical role in tissue sampling during diagnostic endoscopy procedures. These devices are extensively used in gastrointestinal and pulmonary examinations for early cancer detection. Rising global cancer screening programs are significantly boosting demand. Hospitals and diagnostic centers prefer biopsy forceps due to their precision and compatibility with multiple endoscope systems. Continuous improvements in tip design and material strength are enhancing sampling accuracy. Their recurring usage in routine diagnostic workflows ensures sustained demand across healthcare settings.

The Graspers segment is expected to witness the fastest growth at a CAGR of 7.8% from 2026 to 2033, driven by increasing demand for minimally invasive therapeutic procedures. These devices are widely used in foreign body removal, polyp retrieval, and surgical assistance during endoscopy. Rising adoption of advanced endoscopic surgeries is boosting utilization rates. Technological improvements in ergonomics and control precision are improving procedural efficiency. Expanding surgical applications in ambulatory centers are further supporting growth. Increasing procedural volumes in emergency care units are also accelerating demand.

- By Hygiene

On the basis of hygiene, the Video Endoscopy Devices Market is segmented into single-use, reprocessing, and sterilization. The Reprocessing segment dominated the market with a 55.60% share in 2025, due to the widespread use of reusable endoscopes in hospitals and diagnostic centers. This approach remains cost-effective for high-volume healthcare facilities performing frequent endoscopic procedures. Established sterilization infrastructure supports large-scale adoption. Hospitals prefer reprocessing to reduce per-procedure costs and maximize equipment utilization. Strict regulatory guidelines ensure safe reuse practices and infection control. Continuous improvements in automated endoscope reprocessors are enhancing workflow efficiency.

The Single-use Endoscopes segment is projected to register the fastest growth at a CAGR of 10.2% from 2026 to 2033, driven by rising concerns over cross-contamination and hospital-acquired infections. These devices eliminate the need for cleaning and sterilization, reducing infection risks significantly. Increasing adoption in ICU, emergency, and bronchoscopy applications is accelerating demand. Regulatory support for infection prevention is further strengthening market growth. Technological advancements are improving image quality in disposable systems. Expanding use in outpatient and low-resource settings is also boosting penetration.

- By Application

On the basis of application, the Video Endoscopy Devices Market is segmented into bronchoscopy, arthroscopy, laparoscopy, urology endoscopy, neuroendoscopy, gastrointestinal endoscopy, ENT endoscopy, and others. The Gastrointestinal Endoscopy segment dominated the market with a 35.40% share in 2025, driven by high prevalence of colorectal cancer, ulcers, and digestive disorders. This segment benefits from widespread screening programs and preventive diagnostics initiatives. Increasing geriatric population is further boosting procedure volumes. Hospitals extensively use GI endoscopy for both diagnostic and therapeutic interventions. Advancements in high-definition visualization are improving early lesion detection rates. Strong clinical guidelines supporting routine screening are reinforcing dominance.

The Bronchoscopy segment is expected to witness the fastest growth at a CAGR of 8.9% from 2026 to 2033, driven by rising respiratory diseases such as COPD, lung cancer, and infections. Increasing air pollution levels and smoking prevalence are further contributing to demand. Growing use in ICU and critical care settings is accelerating adoption. Technological advancements in flexible bronchoscopes are improving accessibility and diagnostic accuracy. Expanding use in minimally invasive lung biopsies is supporting growth. Rising awareness of early lung cancer detection is further strengthening the segment.

- By End-Use

On the basis of end-use, the Video Endoscopy Devices Market is segmented into hospitals, ambulatory surgery centers, clinics, and others. The Hospitals segment dominated the market with a 55.60% share in 2025, due to high patient inflow, advanced surgical infrastructure, and availability of specialized endoscopy units. Hospitals perform a large volume of diagnostic and therapeutic procedures across multiple specialties. Integration of AI-enabled imaging systems is enhancing clinical efficiency. Strong reimbursement frameworks support high adoption rates. Continuous investments in surgical infrastructure are strengthening dominance. Hospitals also serve as key centers for complex and emergency procedures.

The Ambulatory Surgery Centers (ASCs) segment is expected to witness the fastest growth at a CAGR of 7.9% from 2026 to 2033, driven by the shift toward outpatient and cost-efficient surgical care. ASCs offer faster patient turnaround and lower procedural costs compared to hospitals. Increasing preference for minimally invasive procedures is boosting adoption. Technological advancements in portable endoscopy systems are supporting expansion. Rising healthcare decentralization is further accelerating growth. Growing insurance coverage for outpatient procedures is also contributing to demand.

Video Endoscopy Devices Market Regional Analysis

North America dominated the Video Endoscopy Devices Market with the largest revenue share of 38.40% in 2025, supported by advanced healthcare infrastructure, high procedure volumes, and strong adoption of minimally invasive surgical systems. The region benefits from a high volume of gastrointestinal, pulmonary, and urological diagnostic procedures, along with favorable reimbursement policies and early adoption of advanced imaging technologies such as HD, 4K, and AI-assisted endoscopy systems. Increasing prevalence of chronic diseases, strong screening programs, and continuous investments in hospital surgical infrastructure further strengthen North America’s leadership position in the global market..

U.S. Video Endoscopy Devices Market Insight

The U.S. video endoscopy devices market is witnessing strong growth due to rising prevalence of gastrointestinal, respiratory, and colorectal diseases, along with high adoption of minimally invasive surgical procedures. The country’s advanced healthcare infrastructure, strong reimbursement policies, and early adoption of AI-integrated HD and 4K endoscopy systems are driving demand across hospitals and ambulatory surgical centers. In addition, increasing investments in cancer screening programs, robotic-assisted endoscopy, and digital imaging technologies is accelerating procedural volumes across diagnostic and therapeutic applications.

Europe Video Endoscopy Devices Market Insight

The Europe video endoscopy devices market remains a major contributor to global revenue, driven by strong healthcare systems, rising aging population, and high demand for early disease detection procedures. The widespread use of endoscopic technologies in gastroenterology, pulmonology, and urology is supporting market expansion across the region. Increasing investments in minimally invasive surgery infrastructure, strict infection control regulations, and growing adoption of advanced imaging systems such as capsule and AI-assisted endoscopy continue to enhance market penetration throughout Europe.

U.K. Video Endoscopy Devices Market Insight

The U.K. video endoscopy devices market is experiencing steady growth, supported by rising demand for early cancer diagnosis, expanding NHS screening programs, and increasing adoption of minimally invasive procedures. Growing investments in hospital modernization and endoscopy suite upgrades are contributing to market expansion. Furthermore, integration of AI-based diagnostic tools, high-definition imaging systems, and single-use endoscopes is improving clinical efficiency and infection control standards across healthcare facilities in the country.

Germany Video Endoscopy Devices Market Insight

The Germany video endoscopy devices market is expanding steadily due to strong medical device manufacturing capabilities, advanced hospital infrastructure, and increasing focus on precision diagnostics. German hospitals and clinics are increasingly adopting high-performance endoscopy systems for gastrointestinal and surgical applications. Continuous innovation in imaging technologies, robotics-assisted endoscopy, and sterilization systems, along with strong regulatory emphasis on quality and patient safety, is further driving market growth in Germany.

Asia-Pacific Video Endoscopy Devices Market Insight

The Asia-Pacific video endoscopy devices market is expected to witness rapid growth, driven by rising healthcare expenditure, expanding hospital infrastructure, and increasing prevalence of chronic diseases across China, India, and Japan. Growing awareness regarding early disease detection and increasing adoption of minimally invasive surgical techniques are supporting regional market expansion. In addition, rising investments in medical technology, expanding diagnostic centers, and growing penetration of advanced endoscopic systems are accelerating market adoption across both public and private healthcare sectors.

Japan Video Endoscopy Devices Market Insight

The Japan video endoscopy devices market is witnessing consistent growth due to high demand for advanced diagnostic technologies, aging population, and strong focus on early disease detection. Japanese healthcare providers are widely adopting high-definition and capsule endoscopy systems for gastrointestinal and respiratory diagnostics. Furthermore, integration of robotic-assisted endoscopy, AI-based imaging analysis, and minimally invasive surgical techniques is enhancing procedural accuracy and efficiency across hospitals and specialized clinics.

China Video Endoscopy Devices Market Insight

The China video endoscopy devices market is growing rapidly, driven by expanding healthcare infrastructure, rising burden of gastrointestinal and respiratory diseases, and increasing government focus on early cancer screening programs. Rapid adoption of AI-enabled, HD, and disposable endoscopy systems across hospitals and diagnostic centers is significantly boosting market demand. In addition, increasing investments in domestic medical device manufacturing, hospital modernization, and rural healthcare expansion are positioning China as one of the fastest-growing markets globally.

Video Endoscopy Devices Market Share

The video endoscopy devices industry is primarily led by well-established companies, including:

- Olympus Corporation (Japan)

- KARL STORZ SE & Co. KG (Germany)

- FUJIFILM Holdings Corporation (Japan)

- HOYA Corporation (Japan)

- Boston Scientific Corporation (U.S.)

- Medtronic (Ireland)

- Stryker (U.S.)

- Smith+Nephew plc (U.K.)

- CONMED Corporation (U.S.)

- Ambu A/S (Denmark)

- Richard Wolf GmbH (Germany)

- Braun SE (Germany)

- Schoelly Fiberoptic GmbH (Germany)

- HOLOGIC, Inc. (U.S.)

- Medtronic Minimally Invasive Therapies Group (U.S.)

- Arthrex, Inc. (U.S.)

- EndoMed Systems GmbH (Germany)

- SonoScape Medical Corp. (China)

- Shenzhen Mindray Bio-Medical Electronics Co., Ltd. (China)

- Hunan Vathin Medical Instrument Co., Ltd. (China)

Latest Developments in Video Endoscopy Devices Market

- In January 2023, Fujifilm Healthcare introduced enhancements to its ELUXEO endoscopy platform in the U.S. market, focusing on improved imaging resolution, light spectrum control, and diagnostic precision. The upgraded system supports a wide range of gastrointestinal and pulmonary applications, enabling better lesion detection and procedural efficiency. This development further strengthened Fujifilm’s position in advanced diagnostic and therapeutic endoscopy solutions globally

- In April 2022, Olympus Corporation expanded its advanced gastrointestinal endoscopy portfolio with continued global rollout of its EVIS X1 endoscopy system, featuring enhanced imaging capabilities and improved diagnostic support tools. The system is designed to improve visualization and detection of gastrointestinal diseases, supporting clinicians in achieving higher diagnostic confidence during procedures. This expansion reinforced Olympus’ leadership in high-performance endoscopic imaging technologies

- In November 2021, Boston Scientific announced the acquisition of Apollo Endosurgery, a company specializing in minimally invasive endoscopic devices used in gastrointestinal procedures and bariatric treatments. The acquisition aimed to expand Boston Scientific’s endoscopy portfolio and strengthen its presence in the growing therapeutic endoscopy market. This strategic move enhanced the company’s capabilities in advanced gastrointestinal intervention technologies

- In March 2021, Medtronic, a global leader in medical technology, received FDA clearance for its GI Genius™ intelligent endoscopy module, an AI-powered colonoscopy system designed to improve polyp detection rates during gastrointestinal screening procedures. The system uses real-time artificial intelligence to highlight suspicious lesions, supporting physicians in early colorectal cancer detection and improving diagnostic accuracy. This approval marked a major milestone in integrating AI into routine endoscopic workflows, strengthening Medtronic’s position in the advanced endoscopy segment

- In February 2021, Ambu A/S, a leading single-use endoscopy company, launched the aScope™ 5 Broncho single-use bronchoscope system, designed for pulmonary procedures in intensive care units and emergency settings. The device enables high-quality visualization while eliminating cross-contamination risks associated with reusable bronchoscopes. This launch significantly strengthened Ambu’s portfolio in disposable endoscopy solutions, supporting growing demand for infection-free diagnostic procedures

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.