Global Wearable Blood Pressure Monitors Market

Market Size in USD Billion

CAGR :

%

USD

1.90 Billion

USD

16.00 Billion

2025

2033

USD

1.90 Billion

USD

16.00 Billion

2025

2033

| 2026 - 2033 | |

| USD 1.90 Billion | |

| USD 16.00 Billion | |

| % | |

|

Wearable Blood Pressure Monitors Market Overview

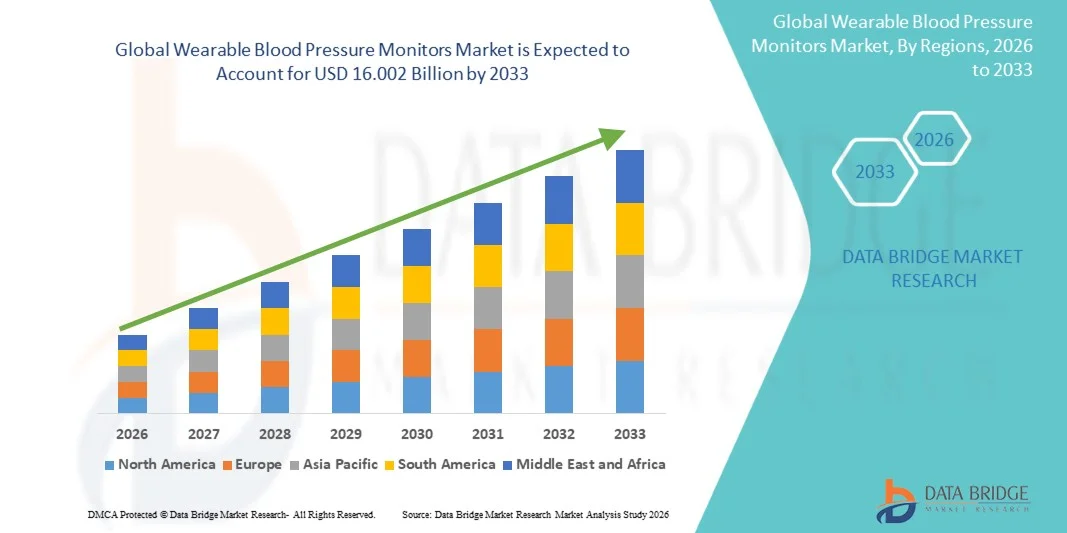

The Wearable Blood Pressure Monitors Market was valued at USD 1.90 billion in 2025 and is projected to reach USD 16.002 billion by 2033, growing at a CAGR of 16.00% from 2026 to 2033. The Wearable Blood Pressure Monitors market is experiencing consistent growth driven by the rising prevalence of hypertension and cardiovascular diseases, increasing consumer awareness regarding preventive healthcare, and growing demand for continuous remote patient monitoring solutions. Rapid advancements in wearable sensor technologies, wireless connectivity, artificial intelligence-based health analytics, and miniaturized medical electronics are significantly improving the accuracy, convenience, and adoption of wearable blood pressure monitoring devices across both clinical and homecare settings. In addition, the growing aging population, increasing lifestyle-related disorders, and rising healthcare expenditure are accelerating demand for real-time health tracking solutions globally.

The increasing focus on personalized healthcare and early disease detection, combined with expanding adoption of telehealth and digital health platforms, is compelling healthcare providers and consumers to adopt advanced wearable blood pressure monitoring technologies. Smartwatches, wrist-worn monitors, patch-based sensors, and cuffless monitoring devices are increasingly replacing traditional episodic blood pressure measurement methods in many healthcare environments, offering continuous, non-invasive, and real-time monitoring capabilities. Furthermore, integration of cloud connectivity, smartphone applications, AI-powered analytics, and remote physician access is enabling improved hypertension management, patient engagement, and chronic disease monitoring across hospitals, ambulatory care centers, and home healthcare markets worldwide.

Key Market Trends & Insights

- North America dominated the Wearable Blood Pressure Monitors Market with the largest revenue share of 38.74% in 2025, supported by advanced healthcare infrastructure, high adoption of remote patient monitoring technologies, increasing prevalence of hypertension and cardiovascular diseases, and strong presence of leading digital health and wearable medical device manufacturers.

- The oscillometric method dominated the market with an estimated share of 63.4% in 2025, owing to its clinical validation, high accuracy, and widespread adoption in medical devices

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 8.4% from 2026 to 2033, fueled by rising healthcare awareness, increasing prevalence of lifestyle-related diseases, expanding telehealth adoption, and growing demand for wearable healthcare devices across China, India, and Japan.

- The Bluetooth-Based segment is the fastest-growing connecting technology category, projected to register a CAGR of 8.1% from 2026 to 2033, reflecting rising adoption of smartphone-connected wearable monitoring systems and increasing demand for seamless wireless health data synchronization.

- The Sensors segment dominates the component category with a 29.68% revenue share in 2025, led by increasing demand for highly accurate biosensors, miniaturized monitoring technologies, and continuous blood pressure tracking capabilities in wearable medical devices.

- The Oscillometric Method segment accounted for 47.83% of the market in 2025, owing to its high measurement accuracy, non-invasive functionality, widespread clinical acceptance, and growing integration into wearable and cuffless blood pressure monitoring systems.

- The Home Healthcare segment dominated the application category with a 46.37% revenue share in 2025, supported by rising preference for self-monitoring solutions, increasing geriatric population, growing chronic disease burden, and expanding adoption of remote healthcare management technologies.

- The Online Mode segment is projected to witness the fastest growth at a CAGR of 8.3% from 2026 to 2033, driven by rapid expansion of e-commerce healthcare platforms, increasing consumer preference for direct-to-consumer wearable devices, and growing accessibility of digital health products globally.

- The Home Care Settings segment held the largest share of 42.91% in 2025, owing to increasing adoption of remote patient monitoring, rising demand for continuous cardiovascular health tracking, and growing emphasis on reducing hospital visits and long-term healthcare costs.

- The Pulse Transit Time Method segment is expected to register the fastest CAGR of 8.0% from 2026 to 2033, driven by increasing development of cuffless blood pressure monitoring technologies, AI-enabled wearable devices, and demand for continuous, real-time cardiovascular monitoring solutions.

Market Size & Forecast

- Global Market Value (2025): USD 1.90 Billion

- Expected Market Value (2033): USD 16.002 Billion

- Forecast CAGR (2026–2033): 16.00%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Wearable Blood Pressure Monitors Market Segmentation

|

Attributes |

Wearable Blood Pressure Monitors Key Market Insights |

|

Segments Covered |

· By Product Type: Wrist Blood Pressure Monitor, Upper Arm Blood Pressure Monitor, and Finger Blood Pressure Monitor · By Connecting Technology: WiFi Based, Bluetooth Based · By Component: Battery, Bluetooth IC, Display, Memory, Processor, and Sensor · By Measurement: Arterial Tonometry, Oscillometric Method, and Pulse Transit Time Method · By Distribution Channel: Offline Mode, and Online Mode · By Application: Home Healthcare, Remote Patient Monitoring, Sports and Fitness · By End User: Hospital, Clinic, Ambulatory Care, and Home Care Settings |

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

• OMRON Healthcare, Inc. (Japan) |

|

Market Opportunities |

· Expansion of Remote Patient Monitoring (RPM) and Telehealth Ecosystems · Integration of AI, Cuffless Monitoring, and Advanced Biosensor Technologies · Rising Demand from Home Healthcare and Preventive Wellness Markets |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Wearable Blood Pressure Monitors Market Trends

Trend: Rising Adoption of Continuous Remote Cardiovascular Monitoring and Digital Health Integration

The Wearable Blood Pressure Monitors Market is witnessing strong growth driven by the shift toward continuous, non-invasive cardiovascular monitoring and digital health ecosystems. Hospitals, homecare providers, and consumers are increasingly adopting wearable blood pressure monitoring devices integrated with smartphones and cloud platforms to enable real-time hypertension tracking and early disease detection. According to the World Health Organization (WHO), hypertension affects more than 1.28 billion adults globally, with nearly 46% unaware of their condition, significantly increasing demand for continuous monitoring solutions. Devices such as wrist-based BP monitors, smartwatch-integrated sensors, and cuffless wearable patches are gaining traction due to their convenience and ability to provide 24/7 health insights. Companies such as OMRON Healthcare, Withings, and Samsung Electronics are expanding AI-enabled wearable BP monitoring ecosystems that combine ECG, SpO₂, and blood pressure tracking for holistic cardiovascular health management. Increasing telehealth adoption and smartphone penetration—exceeding 6.9 billion users globally in 2024—is further accelerating market penetration across both developed and emerging economies.

Wearable Blood Pressure Monitors Market Dynamics

Key Market Driver: Increasing Prevalence of Hypertension and Expansion of Remote Patient Monitoring (RPM)

The rising global burden of cardiovascular diseases and hypertension is a primary driver of the Wearable Blood Pressure Monitors Market. Hypertension contributes to nearly 10 million deaths annually worldwide, making early detection and continuous monitoring critical for preventive healthcare. Healthcare systems in the U.S., Europe, China, and Japan are increasingly adopting Remote Patient Monitoring (RPM) programs to reduce hospital readmissions and improve chronic disease management efficiency by up to 20–30%, according to healthcare digitalization studies. Wearable blood pressure monitors are being integrated into RPM platforms to allow physicians to track patient vitals in real time, enabling timely intervention and personalized treatment adjustments. Leading companies such as Philips Healthcare, GE HealthCare, and OMRON are actively expanding connected health portfolios that support home-based cardiovascular monitoring. In addition, government initiatives promoting digital health infrastructure and reimbursement support for RPM services are further accelerating adoption globally.

Key Restraint/Challenge: Accuracy Limitations, Clinical Validation Barriers, and Regulatory Compliance

A major challenge in the Wearable Blood Pressure Monitors Market is achieving clinically validated accuracy, particularly for cuffless and wrist-based monitoring technologies. Unlike traditional upper-arm sphygmomanometers, wearable devices using methods such as Pulse Transit Time (PTT), optical sensors, and arterial tonometry often face challenges related to calibration drift, motion artifacts, and environmental variability. Regulatory bodies such as the U.S. FDA, European CE authorities, and China NMPA require extensive clinical validation before approval, which increases development timelines and costs. For example, several cuffless BP monitoring technologies are still undergoing multi-phase clinical trials to demonstrate equivalence with standard clinical devices. In addition, data privacy concerns related to continuous health tracking and cloud-based transmission under frameworks such as GDPR in Europe and HIPAA in the U.S. create compliance burdens for manufacturers. High device costs and limited insurance reimbursement in developing regions further restrict widespread adoption, particularly among price-sensitive consumer groups.

Key Market Opportunity: AI-Enabled Cuffless Monitoring and Integration with Digital Healthcare Ecosystems

The integration of artificial intelligence, machine learning, and cuffless monitoring technologies presents a significant opportunity in the Wearable Blood Pressure Monitors Market. AI-enabled wearable devices are increasingly capable of predicting hypertension risks, detecting arrhythmias, and providing personalized cardiovascular insights based on continuous biometric data. Companies are developing advanced cuffless technologies using arterial tonometry and pulse transit time algorithms, eliminating the need for traditional inflatable cuffs while improving user comfort and compliance. In 2024, multiple digital health firms expanded wearable ecosystems combining blood pressure, ECG, and activity tracking into unified platforms, improving early risk detection accuracy in pilot studies by over 85%. The growing adoption of smartwatches and health wearables—shipments exceeding 500 million units annually across global wearable devices—is significantly expanding the addressable market. Furthermore, rising investments in telehealth infrastructure, especially in Asia-Pacific and North America, are enabling seamless integration of wearable BP monitors with electronic health records (EHRs), remote diagnostics, and AI-powered clinical decision support systems, creating strong long-term growth potential.

Wearable Blood Pressure Monitors Market Scope

The Wearable Blood Pressure Monitors market is segmented on the basis of product type, connecting technology, component, measurement method, distribution channel, application, and end user.

- By Product Type

On the basis of product type, the Wearable Blood Pressure Monitors Market is segmented into wrist blood pressure monitors, upper arm blood pressure monitors, and finger blood pressure monitors. The upper arm blood pressure monitors segment dominated the market with an estimated share of 43.2% in 2025, owing to its high clinical accuracy, strong physician recommendation, and widespread adoption in hospitals and diagnostic centers. These devices are considered the gold standard for hypertension monitoring due to consistent measurement reliability. They are extensively used in chronic disease management and long-term patient monitoring programs. Increasing prevalence of cardiovascular diseases and hypertension is significantly driving demand. Hospitals and clinics continue to prefer upper arm devices for diagnostic accuracy and regulatory compliance. Technological advancements such as automated inflation and digital displays are improving usability. Integration with digital health platforms is further strengthening adoption. Rising geriatric population globally is also boosting demand. Home healthcare adoption is increasing steadily for this category. Insurance-supported monitoring programs are expanding usage. Overall clinical trust keeps this segment dominant globally.

The wrist blood pressure monitors segment is expected to be the fastest-growing, registering a CAGR of 8.1% from 2026 to 2033, driven by portability, ease of use, and rising consumer health awareness. These devices are widely adopted in home healthcare and fitness monitoring applications. Increasing smartphone connectivity and mobile health app integration are accelerating adoption. Wrist devices are preferred by elderly users due to convenience and minimal discomfort. Rising trend of wearable health technology is boosting demand. Technological improvements in accuracy and calibration are reducing earlier limitations. Growing preventive healthcare awareness is increasing usage in urban populations. Expansion of e-commerce medical device sales is supporting market penetration. Integration with AI-based health tracking is enhancing functionality. Demand from sports and fitness users is also rising rapidly. Lower cost compared to upper arm devices supports adoption. Continuous innovation is expected to sustain high growth momentum.

- By Connecting Technology

On the basis of connecting technology, the market is segmented into WiFi-based and Bluetooth-based wearable blood pressure monitors. The Bluetooth-based segment dominated the market with an estimated share of 58.6% in 2025, owing to seamless smartphone integration, low energy consumption, and compatibility with digital health ecosystems. Bluetooth-enabled devices allow real-time monitoring and easy synchronization with mobile applications. They are widely used in home healthcare and fitness tracking applications. Increasing penetration of smartphones globally is a major growth driver. Integration with platforms such as Apple Health and Google Fit is expanding usability. These devices are preferred for personal health tracking due to convenience and affordability. Manufacturers are focusing on compact and wearable-friendly designs. Continuous connectivity improvements are enhancing user experience. Data encryption features are improving patient privacy and security. Growing consumer preference for self-monitoring is strengthening demand. Ease of setup and usage is increasing adoption among elderly users. Strong ecosystem compatibility ensures market dominance.

The WiFi-based segment is expected to be the fastest-growing, registering a CAGR of 8.3% from 2026 to 2033, driven by rising adoption in remote patient monitoring and hospital-connected systems. WiFi-enabled devices support continuous cloud-based data transmission for real-time clinical monitoring. They are increasingly used in telehealth and chronic disease management programs. Hospitals prefer WiFi systems for centralized patient data access. Integration with electronic health records (EHR) is boosting adoption. Growing telemedicine infrastructure is supporting expansion. These devices enable multi-patient monitoring across healthcare networks. Increasing demand for connected healthcare ecosystems is driving growth. Cloud analytics integration improves clinical decision-making. Government support for digital health is accelerating deployment. Higher reliability in long-term monitoring strengthens adoption. Expansion of smart hospitals is further boosting demand.

- By Component

On the basis of component, the market is segmented into battery, Bluetooth IC, display, memory, processor, and sensor. The sensor segment dominated the market with an estimated share of 32.8% in 2025, owing to its critical role in accurate blood pressure measurement and signal detection. Advanced pressure sensors enable precise and real-time cardiovascular monitoring. MEMS-based sensor technology is widely used in wearable devices. Increasing demand for cuffless monitoring is driving sensor innovation. Integration of optical and pressure-based sensing improves accuracy. Sensors are essential for continuous health tracking applications. Rising prevalence of hypertension is boosting demand for advanced sensors. Miniaturization of components is enhancing wearable comfort. R&D investments in biosensor technology are accelerating innovation. Clinical reliability depends heavily on sensor performance. Growing use in remote monitoring systems is expanding adoption. Sensor improvements are enabling next-generation wearable devices.

The processor segment is expected to be the fastest-growing, registering a CAGR of 8.5% from 2026 to 2033, driven by increasing demand for AI-enabled health analytics and real-time data processing. Advanced processors enable continuous monitoring and predictive health insights. Integration with machine learning algorithms improves diagnostic accuracy. Wearable devices are becoming more computationally advanced. Edge computing adoption is accelerating in healthcare wearables. Energy-efficient processors are improving battery performance. Growing need for real-time alerts is boosting demand. Smart healthcare ecosystems rely heavily on processing capabilities. Continuous software upgrades are increasing processing requirements. Miniaturized chipsets are enabling compact device design. Rising adoption of smart wearables is fueling growth. Innovation in semiconductor technology is strengthening this segment.

- By Measurement Method

On the basis of measurement method, the market is segmented into arterial tonometry, oscillometric method, and pulse transit time (PTT) method. The oscillometric method dominated the market with an estimated share of 63.4% in 2025, owing to its clinical validation, high accuracy, and widespread adoption in medical devices. It is the most commonly used method in hospitals and diagnostic centers. Regulatory approvals support its dominance in clinical applications. It provides reliable non-invasive blood pressure measurement. Widely used in both professional and home healthcare devices. Standardization across global healthcare systems supports adoption. Increasing hypertension cases are driving demand for accurate monitoring. Integration with digital displays enhances usability. Cost-effectiveness compared to advanced methods supports adoption. Strong physician preference ensures market leadership. Continuous technological improvements maintain reliability. It remains the gold standard in BP measurement.

The pulse transit time (PTT) method is expected to be the fastest-growing, registering a CAGR of 9.0% from 2026 to 2033, driven by demand for cuffless and continuous monitoring technologies. It enables non-invasive, real-time blood pressure estimation using wearable sensors. Increasing adoption in smartwatches and fitness devices is boosting growth. Integration with AI algorithms enhances measurement accuracy. Rising demand for continuous health tracking is supporting expansion. Growing preference for wearable medical devices is accelerating adoption. It eliminates the need for inflatable cuffs, improving comfort. Strong innovation in digital health technologies is driving development. Remote patient monitoring applications are expanding rapidly. Increasing investment in wearable health tech is supporting growth. Clinical research adoption is increasing globally. It represents the future of blood pressure monitoring technology.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into offline and online modes. The offline segment dominated the market with an estimated share of 60.1% in 2025, owing to strong hospital procurement systems, pharmacy distribution networks, and clinical purchasing preferences. Hospitals and clinics prefer offline channels for quality assurance and regulatory compliance. Medical device distributors play a major role in supply chains. Offline purchasing ensures product verification before use. Strong presence of healthcare procurement frameworks supports dominance. Insurance-linked healthcare purchases favor offline channels. Clinics rely on established supplier relationships. Regulatory requirements influence procurement decisions. Bulk institutional purchasing supports offline dominance. Trust and reliability drive channel preference. Availability of after-sales service strengthens offline sales. Strong distributor networks ensure market reach.

The online segment is expected to be the fastest-growing, registering a CAGR of 8.8% from 2026 to 2033, driven by rising e-commerce penetration and increasing consumer preference for direct-to-home healthcare devices. Online platforms offer convenience, discounts, and wider product availability. Growing telehealth adoption is boosting online sales. Smartphone usage is enabling digital healthcare purchasing. Platforms like Amazon and health-focused e-commerce sites are expanding reach. Subscription-based health monitoring services are increasing adoption. Direct-to-consumer medical device sales are rising rapidly. Increasing awareness of preventive healthcare is driving demand. Digital payment systems are supporting growth. Online channels are especially strong in home healthcare. Marketing through digital health apps is increasing visibility. Convenience and affordability are key growth drivers.

- By Application

On the basis of application, the market is segmented into home healthcare, remote patient monitoring, and sports & fitness. The home healthcare segment dominated the market with an estimated share of 47.5% in 2025, owing to rising elderly population and increasing prevalence of hypertension. Patients prefer at-home monitoring for convenience and cost reduction. Growing chronic disease burden is driving adoption. Hospitals are encouraging home monitoring to reduce readmissions. Increasing health awareness supports demand. Easy-to-use wearable devices are boosting adoption. Insurance-supported home care programs are expanding usage. Integration with mobile apps enhances usability. Family-based health monitoring is increasing. Preventive healthcare trends are supporting growth. Rising digital health adoption is strengthening this segment. Continuous monitoring improves patient outcomes.

The remote patient monitoring segment is expected to be the fastest-growing, registering a CAGR of 9.2% from 2026 to 2033, driven by rapid expansion of telemedicine services. Healthcare systems are increasingly adopting digital monitoring solutions. Chronic disease management programs are boosting demand. Real-time patient tracking improves clinical efficiency. Hospitals are shifting toward decentralized care models. Government support for digital health is increasing adoption. AI-based analytics improve monitoring accuracy. Cloud-connected devices are expanding capabilities. Growing healthcare digitization is supporting growth. Demand for continuous monitoring is rising globally. Integration with EHR systems enhances utility. Remote care infrastructure is expanding rapidly.

- By End User

On the basis of end user, the market is segmented into hospitals, clinics, ambulatory care centers, and home care settings. The home care settings segment dominated the market with an estimated share of 44.3% in 2025, owing to increasing adoption of self-monitoring devices and rising geriatric population. Patients prefer home-based monitoring for convenience and cost savings. Growing hypertension prevalence is boosting demand. Chronic disease management is shifting toward home care. Easy-to-use wearable devices are supporting adoption. Telehealth integration is strengthening home monitoring. Insurance support for home care is increasing usage. Rising awareness of preventive healthcare is driving demand. Families are actively monitoring elderly patients. Digital health platforms are enhancing engagement. Remote monitoring reduces hospital burden. Home care is becoming a key healthcare model globally.

The ambulatory care segment is expected to be the fastest-growing, registering a CAGR of 8.7% from 2026 to 2033, driven by increasing outpatient care services. Ambulatory centers are adopting wearable monitoring devices for efficient patient tracking. Rising preference for cost-effective healthcare is supporting growth. Increasing patient volume in outpatient centers is boosting demand. Integration with digital health systems enhances efficiency. Government healthcare reforms are supporting ambulatory care expansion. Focus on early diagnosis is increasing usage. Chronic disease screening programs are expanding. Hospitals are shifting toward outpatient treatment models. Wearable devices improve workflow efficiency. Real-time monitoring improves patient outcomes. Technological advancements are accelerating adoption.

Wearable Blood Pressure Monitors Market Regional Analysis

North America dominated the Wearable Blood Pressure Monitors Market with the largest revenue share of 38.74% in 2025, supported by advanced healthcare infrastructure, high adoption of remote patient monitoring technologies, increasing prevalence of hypertension and cardiovascular diseases, and strong presence of leading digital health and wearable medical device manufacturers. The region benefits from strong healthcare digitization, widespread insurance coverage, and early adoption of AI-enabled and connected medical devices. Rising demand for home-based healthcare solutions and preventive health monitoring is further accelerating market expansion. In addition, growing integration of wearable devices with telemedicine platforms and electronic health records (EHR) systems is improving patient outcomes and clinical decision-making. Strong regulatory frameworks from the FDA supporting digital health innovation are also driving market growth. Increasing investment in chronic disease management programs continues to strengthen regional dominance.

U.S. Wearable Blood Pressure Monitors Market Insight

The U.S. Wearable Blood Pressure Monitors market is witnessing strong growth due to rising cases of hypertension, obesity, and cardiovascular disorders, along with increasing adoption of remote patient monitoring systems. The country’s advanced healthcare ecosystem, strong presence of MedTech companies, and high consumer awareness of preventive healthcare are driving demand. Hospitals and healthcare providers are increasingly adopting wearable BP monitors to reduce hospital readmissions and improve chronic disease management. The expansion of telehealth platforms and insurance-backed home monitoring programs is further boosting adoption. Integration of wearable devices with AI-based health analytics and mobile applications is enhancing patient engagement and real-time monitoring. Additionally, increasing investments in digital health startups and connected healthcare ecosystems are accelerating market growth across clinical and homecare settings.

Europe Wearable Blood Pressure Monitors Market Insight

The Europe Wearable Blood Pressure Monitors market remains a major contributor to global revenue, driven by strong public healthcare systems, high adoption of digital health technologies, and increasing prevalence of cardiovascular diseases across aging populations. Countries such as Germany, France, and the U.K. are leading adoption due to advanced healthcare infrastructure and supportive government initiatives for telemedicine and remote monitoring. Growing emphasis on preventive healthcare and early diagnosis is encouraging the use of wearable medical devices. Integration of digital therapeutics and remote monitoring platforms is improving patient management efficiency. Strict regulatory standards from the European Medicines Agency (EMA) are ensuring high device quality and reliability. Increasing investments in healthcare digitalization and chronic disease management programs are further supporting regional growth.

U.K. Wearable Blood Pressure Monitors Market Insight

The U.K. Wearable Blood Pressure Monitors market is experiencing steady growth, supported by the National Health Service (NHS) initiatives promoting remote patient monitoring and digital healthcare adoption. Rising prevalence of hypertension and cardiovascular diseases is driving demand for continuous monitoring solutions. Increasing use of wearable devices in home healthcare and outpatient management is contributing to market expansion. The country’s strong focus on preventive healthcare and early diagnosis is accelerating adoption. Integration of AI-powered health platforms and mobile applications is improving patient tracking and data accuracy. Growing investments in digital health infrastructure and telemedicine services are further strengthening market growth. The U.K. is emerging as a key innovation hub for connected healthcare technologies in Europe.

Germany Wearable Blood Pressure Monitors Market Insight

The Germany Wearable Blood Pressure Monitors market is expanding steadily due to strong healthcare infrastructure, high prevalence of cardiovascular diseases, and increasing adoption of digital health technologies. German hospitals and clinics are increasingly integrating wearable monitoring devices for chronic disease management and patient monitoring. Strong emphasis on precision healthcare and medical technology innovation is driving demand. Government support for healthcare digitalization and smart hospital initiatives is further boosting adoption. Rising elderly population is increasing demand for home-based monitoring solutions. Germany’s strong MedTech manufacturing ecosystem is also supporting domestic innovation. Increasing integration of wearable devices with hospital IT systems is improving healthcare efficiency and patient outcomes.

Asia-Pacific Wearable Blood Pressure Monitors Market Insight

The Asia-Pacific Wearable Blood Pressure Monitors market is expected to witness rapid growth at a CAGR of 8.4% from 2026 to 2033, fueled by rising healthcare awareness, increasing prevalence of hypertension and lifestyle diseases, expanding telehealth adoption, and growing demand for affordable wearable healthcare devices. Rapid urbanization and improving healthcare infrastructure in countries such as China, India, and Japan are driving market expansion. Governments are increasingly investing in digital health ecosystems and chronic disease management programs. Growing smartphone penetration and mobile health app adoption are further supporting growth. The region is witnessing strong expansion of e-commerce-based medical device sales. Increasing adoption of remote patient monitoring solutions is transforming healthcare delivery models. Rising middle-class population and healthcare spending are further accelerating demand.

Japan Wearable Blood Pressure Monitors Market Insight

The Japan Wearable Blood Pressure Monitors market is witnessing consistent growth due to its aging population, high prevalence of hypertension, and strong focus on preventive healthcare. Japanese healthcare providers are increasingly adopting wearable monitoring devices for elderly care and chronic disease management. The country’s advanced technology ecosystem supports integration of AI and IoT-enabled health devices. Strong emphasis on home healthcare and hospital-at-home models is driving demand. Increasing adoption of remote monitoring systems is improving patient care efficiency. Government initiatives promoting digital health transformation are further supporting market growth. Japan’s focus on precision healthcare and innovation is strengthening wearable device adoption.

China Wearable Blood Pressure Monitors Market Insight

The China Wearable Blood Pressure Monitors market is growing rapidly, driven by increasing urbanization, rising prevalence of cardiovascular diseases, expanding healthcare infrastructure, and strong government support for digital health transformation. Hospitals and clinics are increasingly adopting wearable devices for remote patient monitoring and chronic disease management. Growing middle-class population and rising health awareness are boosting demand for home healthcare solutions. Strong adoption of smartphones and health apps is accelerating wearable integration. China’s expanding telemedicine ecosystem is further supporting market growth. Increasing investments in domestic MedTech innovation are strengthening local manufacturing capabilities. Rapid digitalization of healthcare services is positioning China as one of the fastest-growing markets globally.

Wearable Blood Pressure Monitors Market Share

The Wearable Blood Pressure Monitors industry is primarily led by well-established companies, including:

- OMRON Healthcare, Inc. (Japan)

- Koninklijke Philips N.V. (Netherlands)

- A&D Company, Limited (Japan)

- Withings S.A. (France)

- Samsung Electronics Co., Ltd. (South Korea)

- Apple Inc. (U.S.)

- Huawei Technologies Co., Ltd. (China)

- Fitbit LLC (U.S.)

- Garmin Ltd. (Switzerland)

- Xiaomi Corporation (China)

- Qardio, Inc. (U.S.)

- iHealth Labs Inc. (U.S.)

- Beurer GmbH (Germany)

- Medisana GmbH (Germany)

- SunTech Medical, Inc. (U.S.)

- Biobeat Technologies Ltd. (Israel)

- Aktiia SA (Switzerland)

- Tenet Healthcare Corporation (U.S.)

- Welch Allyn, Inc. (U.S.)

- Microlife Corporation (Switzerland)

- GE HealthCare Technologies Inc. (U.S.)

- Smiths Medical, Inc. (U.S.)

- Viatom Technology Co., Ltd. (China)

- Yuwell-Jiangsu Yuyue Medical Equipment & Supply Co., Ltd. (China)

- Shenzhen Mindray Bio-Medical Electronics Co., Ltd. (China)

- Rossmax International Ltd. (Taiwan)

- Transtek Medical Electronics Co., Ltd. (China)

- AliveCor, Inc. (U.S.)

- Polar Electro Oy (Finland)

- ForaCare Suisse AG (Switzerland)

- Nissei (Nihon Seimitsu Sokki Co., Ltd.) (Japan)

- Spacelabs Healthcare, Inc. (U.S.)

- Bosch + Sohn GmbH & Co. KG (Germany)

- Vivalnk, Inc. (U.S.)

Latest Developments in Wearable Blood Pressure Monitors Market

- In September 2021, Aktiia (Switzerland) announced the commercial expansion of its cuffless blood pressure monitoring bracelet across multiple European markets. The device uses optical sensors and proprietary algorithms to provide continuous, calibration-free blood pressure tracking, marking one of the earliest large-scale consumer deployments of wearable BP monitoring technology in Europe. This expansion highlighted growing demand for continuous hypertension management solutions outside traditional cuff-based devices

- In June 2022, OMRON Healthcare (Japan) expanded its connected health ecosystem by enhancing integration between its wearable and home blood pressure monitoring devices with the OMRON Connect mobile application. The upgrade enabled users to track long-term cardiovascular trends through cloud-based analytics, reinforcing OMRON’s leadership in digital hypertension management solutions and strengthening remote patient monitoring capabilities globally

- In January 2023, Samsung Electronics (South Korea) advanced its wearable health technology ecosystem by expanding blood pressure monitoring functionality on its Galaxy Watch series in additional global markets through its Samsung Health Monitor app. While regulatory approvals vary by region, this development demonstrated increasing convergence of consumer wearables and medical-grade cardiovascular monitoring features, accelerating competition in the wearable BP monitoring segment

- In July 2025, Aktiia (Switzerland) announced that its Hilo Band became the first cuffless blood pressure monitoring wearable to receive U.S. FDA clearance for over-the-counter use, enabling broader consumer access to continuous blood pressure tracking without prescription requirements. This milestone marked a major regulatory breakthrough for cuffless wearable BP technology and strengthened the clinical credibility of wearable hypertension monitoring solutions

- In March 2025, OMRON Healthcare (Japan) expanded its manufacturing footprint in India by strengthening local production capabilities for blood pressure monitoring devices in Chennai. The initiative was aimed at improving accessibility and affordability of BP monitoring solutions in high-growth emerging markets with rising hypertension prevalence, particularly across South Asia

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.