Global Wearable Ecg Monitors Market

Market Size in USD Billion

CAGR :

%

USD

5.01 Billion

USD

27.82 Billion

2025

2033

USD

5.01 Billion

USD

27.82 Billion

2025

2033

| 2026 - 2033 | |

| USD 5.01 Billion | |

| USD 27.82 Billion | |

| % | |

|

Wearable Electrocardiogram (ECG) Monitors Market Overview

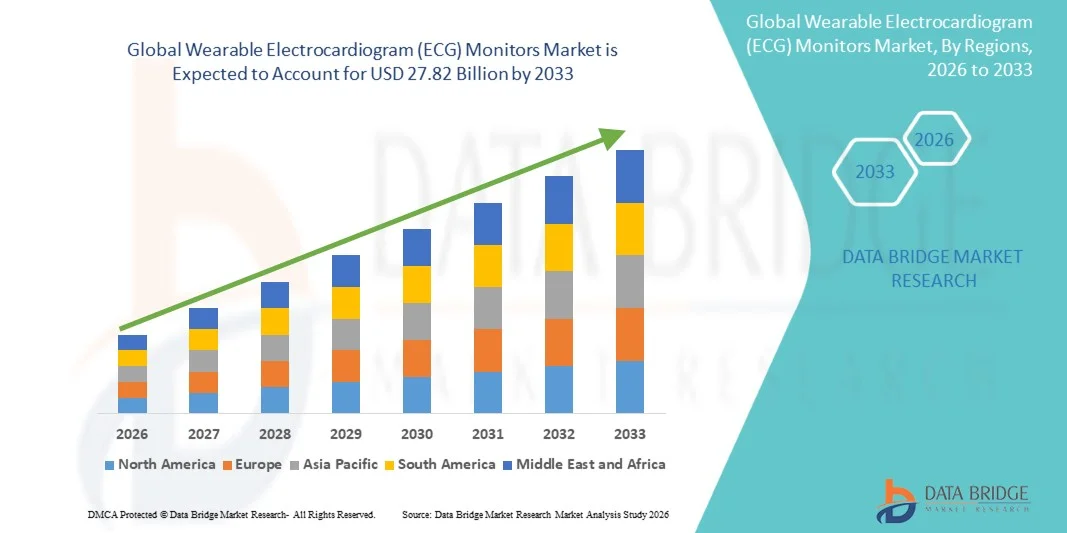

The Wearable Electrocardiogram (ECG) Monitors Market was valued at USD 5.01 billion in 2025 and is projected to reach USD 27.82 billion by 2033, growing at a CAGR of 23.90% from 2026 to 2033. The Wearable Electrocardiogram (ECG) Monitors Market is experiencing strong and consistent growth driven by the rising global burden of cardiovascular diseases, increasing demand for continuous cardiac monitoring, and rapid expansion of digital health and Remote Patient Monitoring (RPM) systems. Healthcare providers, hospitals, and consumers are increasingly adopting wearable ECG devices such as smartwatches, patches, and handheld monitors to enable early detection of arrhythmias, atrial fibrillation (AFib), and other cardiac abnormalities. The integration of wearable ECG systems with smartphones, cloud platforms, and AI-powered analytics is significantly improving real-time diagnostics and preventive care outcomes.

The increasing prevalence of cardiovascular disorders, combined with growing awareness of preventive healthcare and rising healthcare digitization initiatives, is compelling hospitals, clinics, and homecare users to adopt advanced wearable ECG monitoring technologies. Continuous ECG monitoring devices are increasingly replacing traditional episodic testing methods, offering real-time, long-duration cardiac tracking that enhances early diagnosis and reduces emergency cardiac events. In addition, advancements in sensor miniaturization, AI-based arrhythmia detection algorithms, and integration with telehealth platforms are further accelerating the adoption of wearable ECG monitors across both developed and emerging healthcare markets.

Key Market Trends & Insights

- North America dominated the Wearable Electrocardiogram (ECG) Monitors Market and accounted for a significant revenue share of 2% in 2025, supported by high adoption of AI-enabled wearable cardiac monitoring devices, strong penetration of Remote Patient Monitoring (RPM) programs, advanced healthcare infrastructure, and increasing focus on early diagnosis and preventive cardiac care across hospitals and homecare settings.

- The Wireless Wearable ECG Monitors segment dominated the market with a 62.84% share in 2025, owing to rapid adoption of remote patient monitoring systems and increasing demand for continuous, real-time cardiac tracking outside hospital settings

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 1% from 2026 to 2033, fueled by rising prevalence of cardiovascular diseases, increasing healthcare digitization, expanding telehealth adoption, and growing demand for affordable wearable ECG monitoring devices across China, India, and Japan.

- Wireless ECG devices dominated the product type segment with a share of 7% in 2025, owing to increasing demand for real-time cardiac monitoring, ease of use, smartphone connectivity, and seamless integration with cloud-based digital health platforms and mobile applications.

- Atrial Fibrillation (AFib) application segment led the market with a share of 9% in 2025, driven by the rising global incidence of irregular heart rhythms, increasing risk of stroke, and growing demand for continuous long-term ECG monitoring for early detection and management of arrhythmias.

- Hospitals dominated the end-user segment with a revenue share of 3% in 2025, due to high utilization of wearable ECG devices for continuous cardiac monitoring, post-operative surveillance, emergency care, and chronic cardiovascular disease management.

- Homecare settings are expected to be the fastest-growing end-user segment at a CAGR of 8% from 2026 to 2033, driven by increasing adoption of remote patient monitoring solutions, growing elderly population, and rising shift toward decentralized and preventive healthcare models supported by wearable digital health technologies.

Market Size & Forecast

- Global Market Value (2025): USD 5.01 Billion

- Expected Market Value (2033): USD 27.82 Billion

- Forecast CAGR (2026–2033): 23.90%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Wearable Electrocardiogram (ECG) Monitors Market Segmentation

|

Attributes |

Wearable Electrocardiogram (ECG) Monitors Key Market Insights |

|

Segments Covered |

· By Type: Wired Wearable ECG Monitors, Wireless Wearable ECG Monitors · By Application: Atrial Fibrillation, Angina, Atherosclerosis, Cardiac Dysrhythmia, Congestive Heart Failure (CHF), Coronary Artery Disease, Heart Attack, Bradycardia, Tachycardia · By End User: Hospitals, Homecare Settings, Diagnostic Centers & Clinics |

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

• iRhythm Technologies Inc. (U.S.) |

|

Market Opportunities |

· Rising demand for remote cardiac monitoring and home-based healthcare · Expansion of AI-powered diagnostic and predictive analytics · Growth in preventive healthcare and fitness-focused cardiac monitoring |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Wearable Electrocardiogram (ECG) Monitors Market Trends

Trend: Growth in Remote Patient Monitoring & Sports Performance Tracking

Wearable ECG monitors are witnessing increasing adoption beyond hospitals into sports science, professional athletics, and endurance training programs. Elite sports teams and marathon training academies are using wearable ECG devices to continuously monitor heart rate variability, detect early fatigue signals, and optimize athlete performance during high-intensity training sessions. These devices provide real-time telemetry data, enabling coaches and medical staff to assess cardiovascular stress and prevent sudden cardiac events during extreme physical exertion.

For instance, in 2023–2024, several professional football clubs in Europe and major endurance sports programs integrated wearable cardiac monitoring systems to track athlete load management and recovery patterns during training camps. Similarly, wearable ECG patches and chest-strap monitors are increasingly used in cycling and motorsports training environments to analyze physiological responses under simulated race conditions.

Wearable Electrocardiogram (ECG) Monitors Market Dynamics

Key Market Driver: Rising Burden of Cardiovascular Diseases and Expansion of Remote Monitoring Programs

The increasing prevalence of cardiovascular diseases (CVDs) globally is a major driver for wearable ECG monitor adoption. According to global health estimates, CVDs account for nearly 17.9 million deaths annually, making continuous cardiac monitoring a critical healthcare priority. This has significantly boosted demand for wearable ECG devices that enable early detection of arrhythmias, atrial fibrillation, and ischemic events.

Healthcare systems across the U.S., Europe, and Asia-Pacific are increasingly integrating remote patient monitoring (RPM) programs into standard care models. Devices such as patch-based ECG monitors and wireless Holter systems are being deployed for post-discharge cardiac patients to reduce hospital readmission rates. For example, large-scale cardiac monitoring programs in the United States Medicare system have expanded reimbursement coverage for wearable ECG devices, accelerating adoption among aging populations and high-risk patients.

Key Restraint/Challenge: High Cost and Regulatory Compliance Barriers

A key challenge in the global wearable ECG monitors market is the relatively high cost of advanced devices and associated monitoring services. Continuous ECG monitoring systems often require subscription-based analytics platforms, cloud storage, and physician review services, increasing the total cost of ownership for healthcare providers and patients.

In addition, strict regulatory approvals from agencies such as the U.S. FDA and European CE authorities significantly extend product launch timelines. Companies must demonstrate long-term clinical accuracy, data security compliance, and interoperability with hospital systems, which increases development costs and delays commercialization, particularly for smaller medical device manufacturers.

Key Market Opportunity: AI-Enabled Predictive Cardiac Monitoring and Digital Health Ecosystems

The integration of artificial intelligence and machine learning is creating significant opportunities in the wearable ECG monitors market. AI-powered ECG platforms can detect subtle cardiac anomalies, predict atrial fibrillation episodes, and generate early warning alerts before critical cardiac events occur. For instance, AI-based cardiac monitoring solutions have demonstrated improved detection accuracy for atrial fibrillation compared to traditional Holter monitoring in clinical studies conducted between 2022 and 2024. Companies such as iRhythm Technologies Inc. and AliveCor Inc. have expanded AI-driven ECG analysis platforms integrated with cloud-based dashboards for physicians.

In addition, the growth of digital health ecosystems, telemedicine platforms, and smartphone-integrated ECG devices is expanding access in emerging markets across Asia-Pacific, Latin America, and the Middle East, where healthcare infrastructure is rapidly digitizing.

Electrocardiogram (ECG) Monitors Market Scope

The Wearable Electrocardiogram (ECG) Monitors market is segmented on the basis of type, application, and end user.

- By Type

On the basis of type, the Wearable Electrocardiogram (ECG) Monitors Market is segmented into Wired Wearable ECG Monitors and Wireless Wearable ECG Monitors. The Wireless Wearable ECG Monitors segment dominated the market with a 62.84% share in 2025, owing to rapid adoption of remote patient monitoring systems and increasing demand for continuous, real-time cardiac tracking outside hospital settings. The segment benefits from growing integration with smartphones, cloud-based healthcare platforms, and AI-driven diagnostic tools that enhance early disease detection. Wireless devices such as ECG patches, wearable chest straps, and smartwatch-based ECG systems are increasingly preferred due to their comfort, mobility, and ease of long-term monitoring. In addition, rising prevalence of cardiovascular diseases, especially atrial fibrillation and arrhythmias, is significantly boosting adoption. Expanding telehealth infrastructure and reimbursement support in developed markets further strengthen market penetration. Hospitals and homecare providers are increasingly shifting toward wireless systems to reduce hospitalization costs. Growing awareness of preventive healthcare is also encouraging adoption among high-risk patients. Technological advancements in battery life, sensor accuracy, and wireless connectivity are further improving device performance.

The Wireless Wearable ECG Monitors segment is expected to be the fastest growing segment, registering a CAGR of 8.2% from 2026 to 2033, driven by rapid expansion of telemedicine and remote cardiac monitoring programs globally. Increasing digital health adoption, especially in North America, Europe, and Asia-Pacific, is accelerating demand for connected ECG solutions. The growth is further supported by AI-enabled ECG interpretation systems that provide predictive cardiac risk alerts and real-time analytics. Rising elderly population and increasing incidence of chronic cardiovascular conditions are major growth drivers. Integration with wearable ecosystems such as smartwatches and fitness trackers is expanding consumer adoption. Healthcare providers are increasingly deploying wireless ECG devices for post-discharge monitoring to reduce readmission rates. The growing penetration of 5G and cloud healthcare platforms is improving data transmission efficiency. In addition, cost-effective subscription-based monitoring models are increasing accessibility in emerging economies. Continuous innovation in miniaturized sensors and patch-based ECG devices is also driving segment expansion.

- By Application

On the basis of application, the Wearable Electrocardiogram (ECG) Monitors Market is segmented into Atrial Fibrillation, Angina, Atherosclerosis, Cardiac Dysrhythmia, Congestive Heart Failure (CHF), Coronary Artery Disease, Heart Attack, Bradycardia, and Tachycardia. The Atrial Fibrillation segment dominated the market with a 28.45% share in 2025, primarily due to its high global prevalence and strong clinical need for continuous cardiac rhythm monitoring. Atrial fibrillation is one of the most common cardiac arrhythmias and significantly increases the risk of stroke and heart failure, driving demand for early detection solutions. Wearable ECG monitors enable continuous and non-invasive rhythm tracking, improving diagnosis accuracy compared to traditional Holter monitoring. Increasing aging population globally is a major contributing factor to rising AF incidence. Hospitals and cardiology clinics are widely adopting wearable ECG systems for long-term patient monitoring. Integration of AI-based ECG interpretation has further improved detection efficiency. Rising awareness among patients regarding preventive cardiac care is also supporting adoption. Government healthcare programs promoting early diagnosis of cardiovascular diseases are accelerating usage. Expanding outpatient monitoring programs are further strengthening segment dominance.

The Atrial Fibrillation segment is expected to be the fastest growing segment, registering a CAGR of 8.6% from 2026 to 2033, driven by increasing cardiovascular disease burden and growing adoption of AI-enabled diagnostic tools. Rising global geriatric population is significantly increasing incidence rates of arrhythmias. Expansion of remote patient monitoring programs in the U.S. and Europe is accelerating early detection and treatment. Increasing use of wearable ECG patches in ambulatory care is improving patient compliance. Technological advancements in real-time cardiac analytics are enhancing diagnostic accuracy. Integration of ECG devices with mobile health apps is enabling continuous patient engagement. Growing healthcare expenditure in emerging economies is expanding access to cardiac monitoring technologies. Pharmaceutical and medtech collaborations are supporting AI-based arrhythmia detection solutions. Rising awareness campaigns about sudden cardiac arrest prevention are also contributing to growth.

- By End User

On the basis of end user, the Wearable Electrocardiogram (ECG) Monitors Market is segmented into Hospitals, Homecare Settings, and Diagnostic Centers/Clinics. The Hospitals segment dominated the market with a 45.12% share in 2025, due to high patient inflow and extensive use of continuous cardiac monitoring in emergency, intensive care, and post-operative settings. Hospitals rely on wearable ECG devices for real-time cardiac telemetry and early detection of life-threatening arrhythmias. Increasing adoption of centralized monitoring systems integrated with hospital information systems is strengthening usage. Growing burden of cardiovascular emergencies is further increasing demand in hospital settings. Availability of skilled healthcare professionals ensures accurate interpretation of ECG data. Hospitals also benefit from advanced reimbursement frameworks in developed regions. Integration with electronic health records (EHR) improves patient management efficiency. Increasing deployment in cardiac ICUs and emergency departments supports segment dominance. Technological advancements in multi-lead wearable ECG systems are further enhancing clinical adoption.

The Homecare segment is expected to be the fastest growing segment, registering a CAGR of 9.1% from 2026 to 2033, driven by the shift toward decentralized healthcare and remote patient monitoring. Increasing aging population and rising prevalence of chronic cardiac diseases are key growth drivers. Patients are increasingly preferring home-based monitoring solutions to reduce hospital visits. Expansion of telehealth platforms is enabling real-time physician-patient connectivity. Subscription-based wearable ECG services are improving affordability and accessibility. Integration with smartphones and cloud dashboards is enhancing usability. Healthcare systems are focusing on reducing hospital readmission rates through remote monitoring. Growth in preventive healthcare awareness is encouraging early diagnosis at home. Advancements in lightweight and comfortable wearable ECG patches are improving patient compliance. Rising healthcare digitization in emerging markets is further accelerating adoption.

Wearable Electrocardiogram (ECG) Monitors Market Regional Analysis

North America dominated the Wearable Electrocardiogram (ECG) Monitors Market and accounted for the largest revenue share of 33.84% in 2025, supported by high adoption of AI-enabled wearable cardiac monitoring devices, advanced healthcare infrastructure, strong penetration of remote patient monitoring (RPM) programs, and increasing focus on preventive cardiology. The region benefits from widespread use of digital health platforms, strong reimbursement frameworks, and early adoption of connected medical devices across hospitals and homecare settings. Increasing prevalence of cardiovascular diseases and growing geriatric population are further accelerating demand. Integration of wearable ECG devices with smartphones and cloud-based analytics platforms is enhancing real-time monitoring capabilities. In addition, strong presence of key market players and continuous product innovation is reinforcing North America’s leadership in the global market.

U.S. Wearable Electrocardiogram (ECG) Monitors Market Insight

The U.S. Wearable Electrocardiogram (ECG) Monitors market is witnessing strong growth due to rising prevalence of atrial fibrillation and coronary artery disease, increasing healthcare digitization, and rapid expansion of remote patient monitoring programs. The country has a highly developed healthcare system supported by advanced insurance coverage and reimbursement policies that encourage adoption of wearable cardiac devices. Growing integration of AI-based ECG interpretation platforms is improving early diagnosis and reducing hospital readmission rates. Major hospitals and cardiology centers are increasingly deploying patch-based and wireless ECG monitors for continuous patient tracking. Rising investments in digital health startups and telehealth platforms are further supporting market expansion. In addition, increasing consumer awareness about preventive heart health and fitness monitoring is driving adoption among non-hospital users. Strong regulatory support from FDA for wearable medical devices is also accelerating commercialization.

Europe Wearable Electrocardiogram (ECG) Monitors Market Insight

The Europe Wearable Electrocardiogram (ECG) Monitors market remains a major contributor to global revenue, driven by strong healthcare systems, strict regulatory frameworks, and high awareness of cardiovascular disease prevention. Countries such as Germany, France, and the U.K. are leading adopters of advanced wearable cardiac monitoring technologies in both clinical and homecare environments. The region benefits from government-supported digital health initiatives and increasing deployment of telemedicine platforms. Growing aging population and rising incidence of heart-related disorders are significantly boosting demand. European healthcare providers are increasingly integrating wearable ECG devices into chronic disease management programs. Expansion of AI-powered diagnostic tools and cloud-based cardiac monitoring platforms is further improving healthcare efficiency. In addition, strong collaborations between medtech companies and research institutions are driving innovation in device accuracy and usability.

U.K. Wearable Electrocardiogram (ECG) Monitors Market Insight

The U.K. Wearable Electrocardiogram (ECG) Monitors market is experiencing steady growth, supported by increasing adoption of digital health solutions and NHS-driven remote monitoring initiatives. Rising cardiovascular disease burden and government focus on early diagnosis are key growth drivers. The National Health Service (NHS) is actively promoting wearable cardiac devices to reduce hospital admissions and improve patient outcomes. Increasing use of smartphone-connected ECG devices is enabling wider access to cardiac monitoring in homecare settings. Integration of AI-based diagnostic platforms is improving detection accuracy for arrhythmias and atrial fibrillation. In addition, growing investments in telehealth infrastructure and digital hospital programs are strengthening adoption. The presence of leading medtech companies and strong clinical research ecosystem is further supporting innovation in wearable ECG technologies.

Germany Wearable Electrocardiogram (ECG) Monitors Market Insight

The Germany Wearable Electrocardiogram (ECG) Monitors market is expanding steadily due to strong healthcare infrastructure, high technological adoption, and increasing burden of cardiovascular diseases. Germany has a well-established medical device industry that supports rapid integration of wearable ECG solutions into clinical workflows. Hospitals and diagnostic centers are increasingly adopting continuous cardiac monitoring systems for high-risk patients. Strong government focus on digital healthcare transformation is further supporting market growth. The country is also witnessing increasing use of AI-powered ECG interpretation systems in cardiology departments. Rising demand for preventive healthcare and early diagnosis is boosting adoption among aging population groups. In addition, collaborations between German medtech firms and research institutions are driving innovation in sensor accuracy and wearable device design.

Asia-Pacific Wearable Electrocardiogram (ECG) Monitors Market Insight

The Asia-Pacific Wearable Electrocardiogram (ECG) Monitors market is expected to witness rapid growth, driven by rising cardiovascular disease prevalence, expanding healthcare infrastructure, and increasing adoption of digital health technologies. Countries such as China, India, and Japan are experiencing strong demand for affordable and scalable wearable cardiac monitoring solutions. Growing investments in telemedicine and remote patient monitoring programs are significantly supporting market expansion. Increasing awareness about preventive healthcare and early disease detection is boosting adoption in both urban and semi-urban regions. The region is also witnessing rapid growth in smartphone penetration, enabling wider use of connected ECG devices. Government initiatives to improve healthcare accessibility are further accelerating adoption. In addition, expansion of local medtech manufacturing is reducing device costs and improving availability.

Japan Wearable Electrocardiogram (ECG) Monitors Market Insight

The Japan Wearable Electrocardiogram (ECG) Monitors market is witnessing consistent growth due to its rapidly aging population and high prevalence of cardiovascular disorders. Japan has one of the most advanced healthcare systems, enabling early adoption of wearable medical technologies. Hospitals and clinics are increasingly integrating ECG monitoring devices into routine cardiac care and post-operative monitoring. Strong emphasis on preventive healthcare and early diagnosis is driving demand for continuous monitoring solutions. Integration of AI and IoT-based health platforms is improving real-time cardiac analytics. Japan’s strong electronics and semiconductor industry also supports innovation in compact and highly accurate wearable ECG devices. In addition, increasing collaboration between healthcare providers and technology companies is accelerating digital health transformation.

China Wearable Electrocardiogram (ECG) Monitors Market Insight

The China Wearable Electrocardiogram (ECG) Monitors market is growing rapidly due to rising urbanization, increasing healthcare digitization, and strong government support for smart healthcare initiatives. China has a large patient population suffering from cardiovascular diseases, significantly driving demand for continuous cardiac monitoring solutions. Expansion of telehealth platforms and AI-based diagnostic systems is accelerating adoption of wearable ECG devices. Domestic manufacturers are playing a key role in reducing device costs and increasing accessibility. Hospitals are increasingly deploying wireless ECG systems for remote monitoring and emergency care. Growing awareness of preventive healthcare among the population is further supporting market penetration. In addition, government initiatives such as “Healthy China 2030” are promoting widespread adoption of digital health technologies. The country is also emerging as a major hub for innovation in wearable medical devices globally.

Wearable Electrocardiogram (ECG) Monitors Market Share

The Wearable Electrocardiogram (ECG) Monitors industry is primarily led by well-established companies, including:

- iRhythm Technologies Inc. (U.S.)

- AliveCor Inc. (U.S.)

- Medtronic plc (Ireland)

- GE HealthCare Technologies Inc. (U.S.)

- Philips Healthcare (Netherlands)

- Biosense Webster Inc. (U.S.)

- Biotronik SE & Co. KG (Germany)

- Hillrom (Baxter) (U.S.)

- OMRON Healthcare Co., Ltd. (Japan)

- Schiller AG (Switzerland)

- BPL Medical Technologies (India)

- Cardiac Insight Inc. (U.S.)

- Spacelabs Healthcare (U.S.)

- Alive Technologies Pty Ltd (Australia)

- Nihon Kohden Corporation (Japan)

- Shenzhen Mindray Bio-Medical Electronics Co., Ltd. (China)

- Samsung Medison (South Korea)

- General Electric Company (U.S.)

- Boston Scientific Corporation (U.S.)

- ZOLL Medical Corporation (U.S.)

- Shenzhen Comen Medical Instruments Co., Ltd. (China)

- Wellysis Corp. (South Korea)

- Fukuda Denshi Co., Ltd. (Japan)

Latest Developments in Wearable Electrocardiogram (ECG) Monitors Market

- In February 2021, iRhythm Technologies, Inc. (U.S.) expanded its AI-driven cardiac monitoring ecosystem with continued scaling of its Zio patch platform in the U.S. market, strengthening adoption of long-term wearable ECG monitoring for atrial fibrillation detection and post-acute cardiac care. The company reported increased deployment of its patch-based ECG system across hospitals and ambulatory settings, reinforcing its leadership in extended cardiac rhythm monitoring

- In February 2022, AliveCor Inc. (U.S.) received U.S. FDA clearance for its KardiaMobile Card, a credit-card-sized personal ECG device designed for single-lead cardiac rhythm recording in 30 seconds. The device represented a major step in consumer-grade ECG innovation, enabling portable, on-demand detection of arrhythmias including atrial fibrillation outside clinical environments

- In July 2022, iRhythm Technologies, Inc. (U.S.) received FDA clearance for its ZEUS (Zio ECG Utilization Software) System, developed in collaboration with Verily (Alphabet), integrating AI-based algorithms for improved atrial fibrillation detection and clinical workflow integration with wearable Zio ECG monitors

- In May 2023, AliveCor Inc. (U.S.) expanded its KardiaMobile ecosystem with broader clinical adoption of its KardiaMobile 6L device, which enables six-lead ECG recordings for improved arrhythmia detection accuracy. The solution gained increasing use in remote cardiac monitoring programs and psychiatric QT interval screening applications across healthcare systems in the U.S. and U.K.

- In June 2024, AliveCor Inc. (U.S.) received dual FDA clearance for its Kardia 12L ECG System and KAI 12L AI technology, enabling the first handheld 12-lead ECG device with AI capability to detect up to 35 cardiac conditions including heart attacks and arrhythmias. This marked a significant advancement in AI-enabled wearable cardiac diagnostics

- In October 2024, iRhythm Technologies, Inc. (U.S.) received FDA clearance for design modifications to its Zio AT wearable cardiac monitoring system, improving device reliability and data quality for long-term ECG monitoring applications in ambulatory and post-hospital care settings

- In May 2024, WearLinq (U.S.) expanded access to its FDA-cleared eWave wearable ECG system through acquisition of AMI Cardiac Monitoring, enhancing ambulatory cardiac monitoring services and strengthening its clinical delivery network for multi-lead wearable ECG monitoring solutions

- In July 2024, AliveCor Inc. (U.S.) introduced its InstantQT AI solution in Europe, expanding digital ECG interpretation capabilities for QT interval monitoring and enhancing early detection of cardiac risk conditions through wearable ECG platforms integrated with cloud-based analytics

- In October 2024, iRhythm Technologies, Inc. (U.S.) reported continued regulatory progress and commercialization momentum for its upgraded Zio AT patch ECG system, supporting improved ambulatory cardiac monitoring workflows and strengthening adoption in healthcare systems across North America and Europe

- In June 2025, research and development in wearable ECG systems highlighted next-generation innovations in wireless chest patches and fabric-based electrodes aimed at improving long-term monitoring comfort and signal accuracy, with emphasis on low-power IoT-enabled ECG devices for continuous cardiac health tracking

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.