Global Wireless Connectivity Market

Market Size in USD Billion

CAGR :

%

USD

115.10 Billion

USD

354.55 Billion

2025

2033

USD

115.10 Billion

USD

354.55 Billion

2025

2033

| 2026 –2033 | |

| USD 115.10 Billion | |

| USD 354.55 Billion | |

| % | |

|

What is the Global Wireless Connectivity Market Size and Growth Rate?

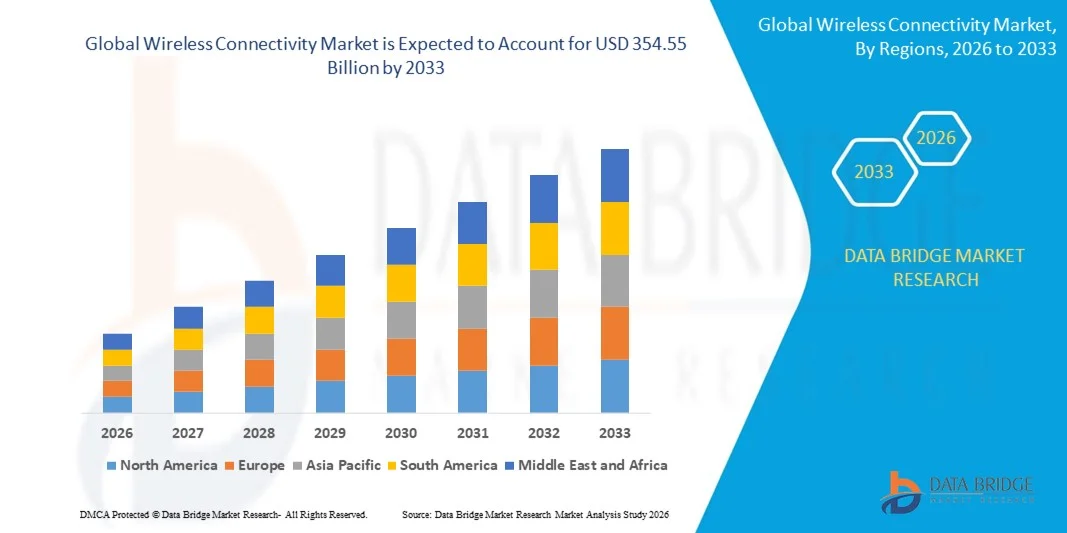

- The global wireless connectivity market size was valued at USD 115.10 billion in 2025 and is expected to reach USD 354.55 billion by 2033, at a CAGR of15.10% during the forecast period

- The increase in the demand for wireless sensor networks in the development of smart infrastructure acts as one of the major factors driving the wireless connectivity market

- The rise in the demand for smart phones and other wireless technology devices such as Wi-Fi, Bluetooth and ZigBee, and increase in trends such as work from home and virtual learning pertaining to the COVID-19 pandemic within the region drive the market growth

What are the Major Takeaways of Wireless Connectivity Market?

- The increase in demand for low-power wide-area (LPWA) networks in the IoT applications and rise in the internet penetration rate, further influence the market

- In addition, urbanization and digitization, adoption of the Internet of Things (IoT), and advent of and rapid advancements in radio frequencies positively affect the wireless connectivity market. Furthermore, development of 5G network and support from governments across the world for R&D in the Internet of Things extend profitable opportunities to the market players

- North America dominated the wireless connectivity market with a 40.8% revenue share in 2025, driven by strong deployment of Wi-Fi 6/6E, Bluetooth 5X, 5G infrastructure, and advanced IoT ecosystems across the U.S. and Canada

- Asia-Pacific is projected to register the fastest CAGR of 9.36% from 2026 to 2033, fueled by rapid semiconductor manufacturing expansion, large-scale 5G rollouts, and strong consumer electronics production across China, Japan, India, South Korea, and Southeast Asia

- The Wi-Fi segment dominated the market with an estimated 34.7% share in 2025, driven by widespread deployment in smartphones, laptops, smart TVs, industrial gateways, and enterprise networking systems

Report Scope and Wireless Connectivity Market Segmentation

|

Attributes |

Wireless Connectivity Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

What is the Key Trend in the Wireless Connectivity Market?

Accelerating Integration of High-Speed, Low-Power, and Multi-Protocol Wireless Technologies

- The wireless connectivity market is witnessing rapid integration of Wi-Fi 6/6E, Bluetooth Low Energy (BLE), 5G, Zigbee, and UWB into compact chipsets designed for IoT devices, smart homes, industrial automation, and consumer electronics

- Manufacturers are focusing on low-power architectures, edge intelligence, and multi-protocol System-on-Chip (SoC) solutions that enable seamless connectivity, reduced latency, and enhanced device interoperability

- Growing demand for compact, battery-efficient, and high-throughput wireless modules is driving adoption across smart wearables, connected vehicles, healthcare devices, and industrial IoT deployments

- For instance, companies such as Qualcomm Technologies, Inc., MediaTek Inc., NXP Semiconductors, and Nordic Semiconductor ASA have introduced advanced multi-standard wireless SoCs supporting AI-enabled edge processing and secure connectivity

- Increasing deployment of smart infrastructure, Industry 4.0 solutions, and connected consumer ecosystems is accelerating the shift toward high-speed and scalable wireless communication platforms

- As digital ecosystems expand globally, Wireless Connectivity technologies will remain critical for enabling real-time data exchange, device interoperability, and next-generation smart applications

What are the Key Drivers of Wireless Connectivity Market?

- Rising demand for IoT-enabled devices, smart consumer electronics, connected healthcare equipment, and EV telematics systems is significantly boosting wireless chipset and module adoption

- For instance, in 2025, leading companies such as Broadcom Inc., Texas Instruments Incorporated, and Renesas Electronics Corporation expanded their connectivity portfolios with enhanced Wi-Fi, BLE, and sub-GHz solutions for industrial and automotive applications

- Growing rollout of 5G networks, smart city projects, and cloud-connected industrial systems across the U.S., Europe, and Asia-Pacific is driving large-scale wireless infrastructure deployment

- Advancements in low-latency communication, mesh networking, beamforming, and spectrum efficiency have strengthened performance, reliability, and coverage

- Rising adoption of AI-powered edge devices, high-speed data transfer protocols, and secure wireless authentication technologies is creating demand for advanced connectivity solutions

- Supported by steady investments in semiconductor R&D, telecom infrastructure, and digital transformation initiatives, the Wireless Connectivity market is projected to experience sustained long-term growth

Which Factor is Challenging the Growth of the Wireless Connectivity Market?

- High development and integration costs associated with advanced 5G, Wi-Fi 6/6E, and multi-protocol chipsets limit adoption among small-scale device manufacturers

- For instance, during 2024–2025, fluctuations in semiconductor supply chains and RF component pricing impacted production timelines and overall device costs for several global vendors

- Increasing complexity in managing interference, spectrum congestion, cybersecurity threats, and regulatory compliance raises technical and operational challenges

- Limited network infrastructure in certain emerging economies restricts high-speed wireless technology penetration

- Competition among connectivity standards and rapid technology evolution create short product life cycles and pricing pressure for chipset manufacturers

- To address these issues, companies are investing in cost-optimized chip designs, enhanced security frameworks, energy-efficient architectures, and cross-platform interoperability solutions to strengthen global adoption of Wireless Connectivity technologies

How is the Wireless Connectivity Market Segmented?

The market is segmented on the basis of connectivity technology, type, and end use.

- By Connectivity Technology

On the basis of connectivity technology, the wireless connectivity market is segmented into Wi-Fi, Bluetooth Classic, Bluetooth 4X, Bluetooth 5X, ZigBee, Z-Wave, Thread, NFC, GNSS, EnOcean, Cellular M2M Technologies, UWB, LoRa, SigFox, NB-IoT, LTE CAT-M1, and Others. The Wi-Fi segment dominated the market with an estimated 34.7% share in 2025, driven by widespread deployment in smartphones, laptops, smart TVs, industrial gateways, and enterprise networking systems. Continuous advancements such as Wi-Fi 6 and Wi-Fi 6E have enhanced throughput, reduced latency, and improved spectrum efficiency, making Wi-Fi the backbone of high-speed wireless communication. Strong adoption across smart homes, offices, and public infrastructure further supports segment leadership.

The Cellular M2M Technologies segment is projected to grow at the fastest CAGR from 2026 to 2033, fueled by rising deployment of connected vehicles, smart meters, industrial IoT, asset tracking, and remote healthcare monitoring. Expansion of 5G, NB-IoT, and LTE CAT-M1 networks is accelerating large-scale machine-to-machine communication globally.

- By Type

On the basis of type, the wireless connectivity market is segmented into WLAN, WPAN, Satellite, LPWAN, and Cellular M2M. The WLAN segment dominated the market with a 38.9% share in 2025, primarily due to strong reliance on Wi-Fi-based local area networks in residential, commercial, and industrial environments. WLAN technologies provide high data transfer rates, low latency, and seamless integration with enterprise IT infrastructure. Increasing cloud adoption, hybrid work models, and smart device penetration continue to drive WLAN demand across developed and emerging economies.

The LPWAN segment is expected to grow at the fastest CAGR from 2026 to 2033, supported by expanding IoT deployments requiring long-range, low-power communication. Technologies such as LoRa and SigFox are gaining momentum in smart agriculture, smart cities, logistics, and utility monitoring, where extended battery life and wide-area coverage are critical.

- By End Use

On the basis of end use, the wireless connectivity market is segmented into Wearable Devices, Healthcare, Consumer Electronics, Building Automation, Automotive & Transportation, and Others. The Consumer Electronics segment dominated the market with a 41.3% share in 2025, driven by high penetration of smartphones, tablets, smart home devices, gaming consoles, and wireless audio systems. Rapid product innovation, rising internet penetration, and growing demand for seamless device interoperability significantly contribute to segment growth. Integration of Wi-Fi, Bluetooth 5X, and UWB in next-generation devices further strengthens connectivity adoption.

The Automotive & Transportation segment is projected to grow at the fastest CAGR from 2026 to 2033, propelled by increasing integration of connected car platforms, V2X communication, EV telematics, ADAS systems, and in-vehicle infotainment. Rising digitalization of vehicle architectures and regulatory emphasis on vehicle connectivity are accelerating wireless technology deployment in the automotive sector.

Which Region Holds the Largest Share of the Wireless Connectivity Market?

- North America dominated the wireless connectivity market with a 40.8% revenue share in 2025, driven by strong deployment of Wi-Fi 6/6E, Bluetooth 5X, 5G infrastructure, and advanced IoT ecosystems across the U.S. and Canada. High adoption of connected devices, smart home technologies, industrial IoT platforms, and cloud-integrated communication systems continues to fuel regional demand

- Leading companies such as Qualcomm Technologies, Inc., Broadcom Inc., and Texas Instruments Incorporated are continuously introducing advanced multi-protocol chipsets, RF front-end modules, and secure connectivity platforms, strengthening technological leadership

- Strong telecom infrastructure, early 5G rollout, high R&D spending, and rapid digital transformation across enterprises further reinforce North America’s dominant market position

U.S. Wireless Connectivity Market Insight

The U.S. represents the largest contributor within North America, supported by extensive semiconductor innovation, large-scale 5G deployment, and widespread integration of wireless modules in automotive, healthcare, consumer electronics, and industrial automation sectors. Increasing development of AI-enabled edge devices, EV connectivity systems, smart city networks, and enterprise cloud platforms intensifies demand for high-speed, low-latency wireless solutions. Presence of leading chipset manufacturers, strong startup ecosystems, and continuous investments in next-generation telecom infrastructure drive sustained market expansion.

Canada Wireless Connectivity Market Insight

Canada contributes significantly to regional growth, driven by expanding IoT adoption, telecom modernization, and increasing deployment of smart infrastructure projects. Rising use of wireless modules in healthcare monitoring, industrial automation, and energy management systems supports steady demand. Government-backed digital transformation initiatives, strong research universities, and growing 5G coverage further accelerate Wireless Connectivity adoption across commercial and public-sector applications.

Asia-Pacific Wireless Connectivity Market

Asia-Pacific is projected to register the fastest CAGR of 9.36% from 2026 to 2033, fueled by rapid semiconductor manufacturing expansion, large-scale 5G rollouts, and strong consumer electronics production across China, Japan, India, South Korea, and Southeast Asia. Massive production of smartphones, IoT devices, automotive electronics, and industrial sensors significantly increases demand for cost-efficient and scalable wireless technologies. Rising investments in AI hardware, smart manufacturing, and digital infrastructure further accelerate regional market growth.

China Wireless Connectivity Market Insight

China leads the Asia-Pacific region due to its dominant electronics manufacturing base and aggressive 5G infrastructure expansion. Strong government support for semiconductor self-reliance, IoT development, and smart city initiatives drives high adoption of Wi-Fi, cellular M2M, and LPWAN technologies. Competitive production capabilities and large domestic demand strengthen China’s position in the global Wireless Connectivity ecosystem.

Japan Wireless Connectivity Market Insight

Japan demonstrates steady growth supported by advanced telecom networks, automotive innovation, and robotics development. Increasing integration of wireless communication in connected vehicles, smart factories, and healthcare systems fuels demand. Focus on reliability, high-speed communication standards, and precision engineering sustains long-term market expansion.

India Wireless Connectivity Market Insight

India is emerging as a high-growth market driven by expanding smartphone penetration, government-backed digital programs, and rising IoT deployment. Growth in telecom infrastructure, EV connectivity, and industrial automation strengthens demand for wireless chipsets and modules. Expanding semiconductor design centers and startup ecosystems further support market acceleration.

South Korea Wireless Connectivity Market Insight

South Korea contributes significantly due to strong 5G leadership, advanced semiconductor manufacturing, and high adoption of smart consumer electronics. Rapid innovation in AI processors, memory devices, and connected automotive platforms increases reliance on high-performance wireless solutions. Technological advancement and export-oriented electronics production continue to reinforce regional growth.

Which are the Top Companies in Wireless Connectivity Market?

The wireless connectivity industry is primarily led by well-established companies, including:

- Intel Corporation (U.S.)

- Texas Instruments Incorporated (U.S.)

- Qualcomm Technologies, Inc. (U.S.)

- Broadcom Inc. (U.S.)

- STMicroelectronics (Switzerland)

- NXP Semiconductors (Netherlands)

- Microchip Technology Inc. (U.S.)

- MediaTek Inc. (Taiwan)

- Cypress Semiconductor Corporation (U.S.)

- Renesas Electronics Corporation (Japan)

- EnOcean GmbH (Germany)

- NEXCOM International Co., Ltd. (Taiwan)

- Skyworks Solutions, Inc. (U.S.)

- Murata Manufacturing Co., Ltd. (Japan)

- Marvell Technology, Inc. (U.S.)

- Nordic Semiconductor ASA (Norway)

- ESPRESSIF SYSTEMS (SHANGHAI) CO., LTD. (China)

- CEVA, Inc. (U.S.)

- Quantenna Communications, Inc. (U.S.)

- PERASO TECHNOLOGIES INC. (Canada)

- Panasonic Corporation (Japan)

What are the Recent Developments in Global Wireless Connectivity Market?

- In May 2024, AST SpaceMobile announced plans to deploy five commercial satellites into low Earth orbit to enable a space-based broadband network that connects directly to mobile phones through AT&T’s network, strengthening global direct-to-device connectivity and expanding coverage in remote and underserved regions, thereby accelerating the evolution of satellite-enabled wireless communication worldwide

- In May 2024, Lightstorm entered into a strategic collaboration with Console Connect to deliver enhanced network connectivity and seamless cloud access across more than 180 data centers globally, improving enterprise-grade digital infrastructure and enabling scalable, on-demand connectivity solutions for businesses worldwide

- In May 2024, Elisa revealed its plan to introduce new 5G standalone network broadband subscriptions for enterprises and consumers, unlocking advanced 5G capabilities such as ultra-low latency and network slicing, thereby creating stronger commercial opportunities and accelerating next-generation wireless adoption

- In May 2024, Blues, in partnership with Arduino, launched the “Blues Wireless for Arduino Opta” expansion module at Automate in Chicago, enhancing connectivity capabilities for the Arduino Opta micro-PLC and enabling more efficient industrial IoT integration, thereby strengthening wireless-enabled automation solutions across smart manufacturing environments

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Wireless Connectivity Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Wireless Connectivity Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Wireless Connectivity Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.