Global Green Food Packaging Market

Market Size in USD Million

USD

372.82 Million

USD

799.17 Million

2024

2032

USD

372.82 Million

USD

799.17 Million

2024

2032

| 2025 - 2032 | |

| USD 372.82 Million | |

| USD 799.17 Million | |

| % | |

|

What is the Global Green Food Packaging Market Size and Growth Rate?

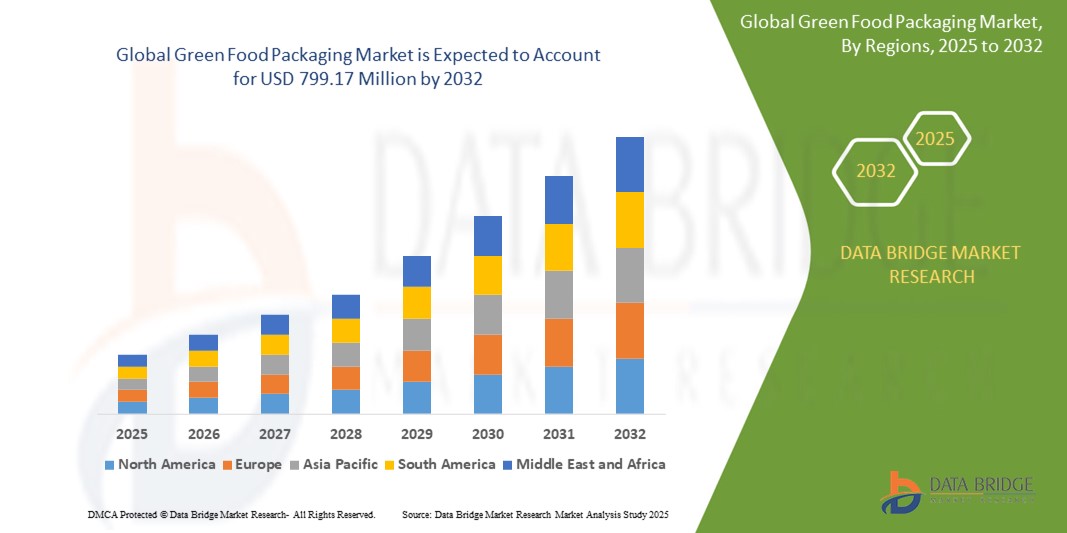

- The global green food packaging market size was valued at USD 372.82 million in 2024 and is expected to reach USD 799.17 million by 2032, at a CAGR of 10.00% during the forecast period

- Due to the growing environmental concerns, green packaging has gained traction in the majority of countries. Rising transportation and energy costs are also contributing to the market's expansion

- Furthermore, negative consumer perceptions of conventional packaging and government pressure to shift toward eco-friendly materials have fuelled market growth. Several brands have recently implemented green packaging solutions to reduce their carbon footprint

What are the Major Takeaways of Green Food Packaging Market?

- Stringent government regulations, packaging industry downsizing, and technological advancements in the packaging industry for the production of packaging using non-petroleum products are driving the market for eco-friendly food packaging

- In addition, innovative products such as edible packaging and water-soluble packaging are fuelling the market for eco-friendly food packaging

- Asia-Pacific dominated the green food packaging market with the largest revenue share of 31.7% in 2024, driven by growing consumer awareness of environmental sustainability, rapid urbanization, and favorable government initiatives promoting eco-friendly packaging alternatives

- North America green food packaging market is poised to grow at the fastest CAGR of 13.5% during the forecast period of 2025 to 2032, fueled by heightened environmental awareness, increasing regulations around single-use plastics, and the rising popularity of organic and sustainably packaged food products

- The Recycled Content segment dominated the market with the largest revenue share of 46.3% in 2024, driven by increased global emphasis on reducing plastic waste and the widespread availability of recycled materials such as paper, plastics, and metals

Report Scope and Green Food Packaging Market Segmentation

|

Attributes |

Green Food Packaging Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

What is the Key Trend in the Green Food Packaging Market?

“Rising Adoption of Biodegradable and Compostable Packaging Solutions”

- A significant and accelerating trend in the global green food packaging market is the increased use of biodegradable, compostable, and plant-based materials to replace conventional plastic packaging, driven by regulatory pressures and rising environmental awareness. These solutions reduce plastic waste, lower carbon footprints, and align with circular economy principles

- For instance, in March 2024, Tetra Pak announced the development of renewable plant-based beverage cartons using sugarcane-derived bioplastics, significantly reducing reliance on fossil-based resources and improving recyclability across global market

- Manufacturers are investing in materials such as polylactic acid (PLA), bagasse (sugarcane fiber), mushroom-based packaging, and seaweed-derived alternatives, which naturally degrade without harming ecosystems. Companies are also introducing compostable films and coatings to extend shelf life while maintaining eco-friendly credentials

- Brands are increasingly marketing their sustainable packaging to eco-conscious consumers, highlighting certifications such as OK Compost, FSC, and BPI to build consumer trust and meet evolving purchasing preferences

- The shift toward compostable and biodegradable solutions is reshaping food packaging design, with innovations focusing on durability, food safety, and performance while minimizing environmental impact

- This trend is fundamentally reshaping packaging strategies, especially in the food & beverage sector, with companies such as Amcor, Mondi, and Sealed Air leading the way in scalable, bio-based packaging alternatives

- The demand for sustainable, compostable, and eco-friendly packaging is expected to grow rapidly across ready-to-eat meals, fresh produce, bakery, and beverage segments, driven by consumer expectations and stringent regulations against single-use plastics

What are the Key Drivers of Green Food Packaging Market?

- The growing global focus on reducing plastic pollution, combined with rising consumer demand for sustainable alternatives, is a major force propelling the adoption of Green Food Packaging solutions

- For instance, in January 2024, Mondi Group launched recyclable paper-based food packaging with barrier properties suitable for perishable products, helping brands meet sustainability targets while ensuring product protection

- Stringent government regulations such as bans on single-use plastics, extended producer responsibility (EPR) policies, and carbon reduction mandates are encouraging manufacturers to adopt greener materials and packaging processes

- In addition, consumer preferences are shifting toward brands that demonstrate environmental responsibility, prompting food manufacturers and retailers to incorporate biodegradable, compostable, and recyclable packaging into their product lines

- The foodservice sector is also witnessing strong demand for sustainable packaging due to growth in takeaway, delivery, and ready-to-eat products, where eco-friendly materials provide differentiation and meet regulatory compliance

- Technological advancements in material science have made biodegradable and compostable packaging more affordable, durable, and functional, increasing their attractiveness for both large manufacturers and SMEs in the food industry

Which Factor is challenging the Growth of the Green Food Packaging Market?

- One of the key challenges limiting the growth of the green food packaging market is the higher cost of biodegradable and compostable packaging compared to conventional plastic alternatives, posing affordability concerns, especially for price-sensitive markets

- For instance, small food producers in developing regions often face budget constraints that make the switch to eco-friendly packaging difficult without government incentives or subsidies

- Performance limitations such as shorter shelf life, reduced barrier properties, or specific storage conditions required for some biodegradable materials can deter adoption in certain food categories, especially perishables

- Inadequate industrial composting infrastructure and limited consumer awareness regarding proper disposal of compostable packaging also hinder the full environmental benefits, leading to contamination of recycling streams or improper waste management

- Moreover, fragmented global regulations on compostability and recyclability create inconsistencies in material standards, making it challenging for manufacturers to scale solutions across multiple regions

- Overcoming these challenges will require continued material innovation, cost reductions through economies of scale, policy support, and consumer education to ensure widespread adoption and effectiveness of Green Food Packaging solutions globally

How is the Green Food Packaging Market Segmented?

The market is segmented on the basis of packaging type, material, application, and type.

• By Packaging Type

On the basis of packaging type, the green food packaging market is segmented into Recycled Content, Reusable Packaging, and Degradable Packaging. The Recycled Content segment dominated the market with the largest revenue share of 46.3% in 2024, driven by increased global emphasis on reducing plastic waste and the widespread availability of recycled materials such as paper, plastics, and metals. Governments and corporations asuch as are implementing mandates and sustainability goals that favor the use of packaging made from post-consumer recycled content, boosting market demand.

The Degradable Packaging segment is expected to witness the fastest growth rate from 2025 to 2032, fueled by rising consumer preference for biodegradable, compostable, and plant-based packaging alternatives. Increasing environmental awareness and regulatory restrictions on single-use plastics are accelerating the adoption of degradable solutions, especially across foodservice and convenience product sectors.

• By Material

On the basis of material, the green food packaging market is segmented into Glass, Paper & Paperboard, Plastic, and Metal. The Paper & Paperboard segment held the largest market revenue share of 39.5% in 2024, attributed to its renewable nature, biodegradability, and widespread use in packaging for foodservice, bakery, and takeaway products. Brands and consumers favor paper-based packaging due to its recyclability and alignment with sustainability initiatives.

The Glass segment is anticipated to experience the fastest CAGR from 2025 to 2032, supported by its premium appeal, excellent recyclability, and ability to preserve product quality, particularly in beverage, dairy, and condiment packaging. Growing demand for reusable and plastic-free alternatives is boosting the adoption of glass packaging across premium and eco-conscious food segments.

• By Application

On the basis of application, the green food packaging market is segmented into Bakery, Confectionery, Convenience Foods, Dairy Products, Fruits and Vegetables, Sauces, Dressing and Condiments, and Others. The Fruits and Vegetables segment accounted for the largest revenue share of 27.4% in 2024, driven by rising global consumption of fresh produce and the need for sustainable packaging that extends shelf life while reducing environmental impact. Retailers and producers are increasingly adopting biodegradable trays, compostable films, and recyclable containers for fruits and vegetables.

The Convenience Foods segment is projected to register the fastest growth rate from 2025 to 2032, supported by increased urbanization, busy lifestyles, and demand for ready-to-eat meals packaged in eco-friendly formats. The rise of takeaway, delivery services, and portable meal options is propelling demand for sustainable, functional packaging that reduces waste.

• By Type

On the basis of type, the green food packaging market is segmented into Bottles, Cans, Pouches, and Boxes. The Pouches segment dominated the market with the largest revenue share of 34.8% in 2024, driven by their lightweight nature, reduced material usage, and suitability for various food products such as snacks, condiments, and liquids. The convenience, resealability, and lower transportation emissions of pouches make them a preferred choice in sustainable packaging initiatives.

The Boxes segment is expected to witness the fastest CAGR from 2025 to 2032, fueled by increasing demand for recyclable and biodegradable cardboard boxes, especially in bakery, foodservice, and online grocery deliveries. The emphasis on reducing plastic use and enhancing brand visibility through printed, eco-friendly boxes is contributing to this segment's rapid growth.

Which Region Holds the Largest Share of the Green Food Packaging Market?

- Asia-Pacific dominated the green food packaging market with the largest revenue share of 31.7% in 2024, driven by growing consumer awareness of environmental sustainability, rapid urbanization, and favorable government initiatives promoting eco-friendly packaging alternatives

- Countries such as China, India, Japan, and Australia are witnessing significant demand for biodegradable, recyclable, and reusable packaging solutions across food and beverage industries. Rising disposable incomes, increased consumption of packaged food, and the shift towards sustainable living are major contributors to the region's leadership position

- Furthermore, the growing presence of regional and international packaging manufacturers, coupled with supportive policies on plastic waste reduction, is propelling the adoption of Green Food Packaging solutions across both developed and emerging markets within Asia-Pacific

China Green Food Packaging Market Insight

China green food packaging market captured the largest revenue share within Asia-Pacific in 2024, attributed to the country's expansive food manufacturing sector, surging middle-class population, and strict government regulations encouraging reduced plastic use. Major food and beverage companies in China are increasingly integrating recyclable, compostable, and plant-based packaging to meet both regulatory requirements and growing consumer expectations for eco-friendly products.

Japan Green Food Packaging Market Insight

Japan green food packaging market is witnessing steady growth, supported by a highly developed food processing industry, technological innovation, and growing emphasis on sustainability. The country’s strong recycling infrastructure and consumer preference for minimalistic, eco-conscious packaging designs are boosting demand for degradable and reusable packaging materials, particularly in urban areas.

Which Region is the Fastest Growing Region in the Green Food Packaging Market?

North America green food packaging market is poised to grow at the fastest CAGR of 13.5% during the forecast period of 2025 to 2032, fueled by heightened environmental awareness, increasing regulations around single-use plastics, and the rising popularity of organic and sustainably packaged food products. Consumers in the U.S. and Canada are increasingly prioritizing environmentally responsible purchasing decisions, driving demand for recyclable, compostable, and reusable food packaging across grocery, foodservice, and e-commerce channels. Moreover, major packaging companies and retailers are implementing aggressive sustainability targets, further accelerating the transition towards Green Food Packaging solutions.

U.S. Green Food Packaging Market Insight

U.S. green food packaging market accounted for the largest revenue share within North America in 2024, driven by growing regulatory pressure, corporate sustainability commitments, and increased consumer demand for environmentally friendly packaging in the food and beverage sector. Retailers and manufacturers are adopting plant-based plastics, recycled materials, and compostable packaging to align with market expectations and reduce environmental impact.

Which are the Top Companies in Green Food Packaging Market?

The green food packaging industry is primarily led by well-established companies, including:

- Mondi (U.K.)

- DuPont (U.S.)

- Sealed Air (U.S.)

- Tetra Pak International S.A. (Switzerland)

- UFlex Limited (India)

- R.S.C Luxembourg (Luxembourg)

- Plastipak Holdings, Inc. (U.S.)

- Elopak (Norway)

- BASF SE (Germany)

- Catalyst Paper (Canada)

- Clorox Company (U.S.)

- Berry Global Inc. (U.S.)

- Tetra Laval International S.A. (Switzerland)

- Ball Corporation (U.S.)

What are the Recent Developments in Global Green Food Packaging Market?

- In January 2024, SEE introduced a compostable protein packaging tray during IPPE 2024, crafted from bio-based, food-contact grade resin and USDA-certified with 54% bio-based content derived from renewable wood cellulose, supporting the company’s goal of advancing sustainable food packaging solutions

- In March 2023, Hinojosa Packaging Group unveiled its new line of 100% recyclable primary packaging products called Foodservice, designed specifically for hot and cold beverages as well as 4th and 5th range prepared foods, reinforcing its commitment to promoting sustainable consumption patterns within the food sector

- In February 2023, Sealed Air completed the acquisition of Liquibox, a manufacturer specializing in sustainable liquid packaging, a move that broadens Sealed Air’s product portfolio for food and beverage applications to address the increasing consumer demand for eco-friendly packaging alternatives

- In September 2022, Sealed Air expanded its product portfolio by launching a new line of protective packaging solutions under its Bubble Wrap brand, featuring more than 50% recycled plastic content, furthering its initiatives to provide circular and environmentally responsible packaging options

- In September 2020, Berry Global collaborated with Bhoomi to introduce a 100% sugarcane-based HDPE bottle made from I’m Green™ certified material by Braskem, a solution that is fully recyclable and offers environmental benefits such as reduced water consumption, lower greenhouse gas emissions, and elimination of fossil fuel reliance

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Green Food Packaging Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Green Food Packaging Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Green Food Packaging Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.