Middle East Africa Mea Hemostats Market

Market Size in USD Million

USD

348.28 Million

USD

685.86 Million

2025

2033

USD

348.28 Million

USD

685.86 Million

2025

2033

| 2026 - 2033 | |

| USD 348.28 Million | |

| USD 685.86 Million | |

| % | |

|

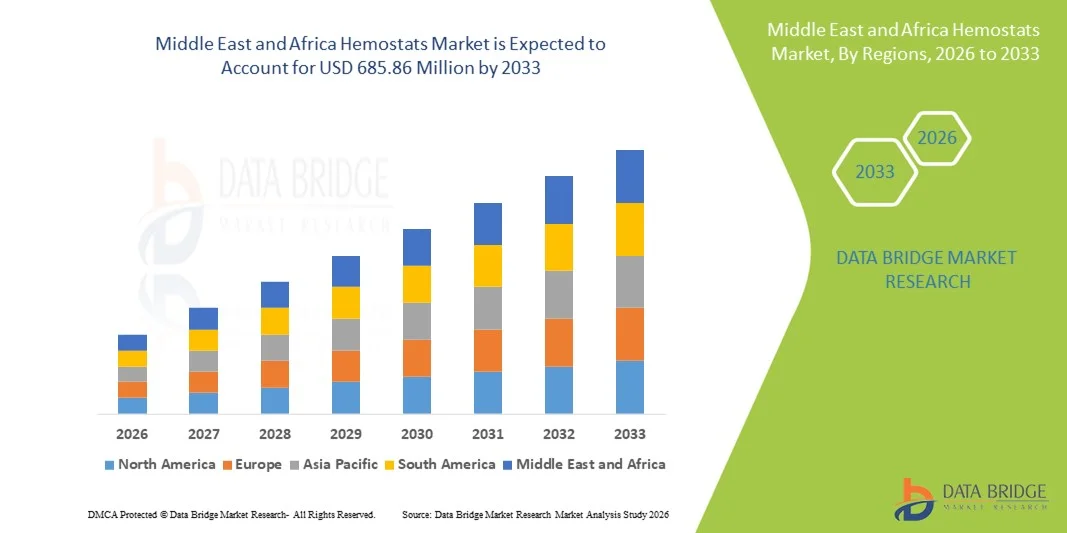

Middle East and Africa Hemostats Market Size

- The Middle East and Africa hemostats market size was valued at USD 348.28 million in 2025 and is expected to reach USD 685.86 million by 2033, at a CAGR of 8.84% during the forecast period

- The market growth is largely fueled by the rising number of surgical procedures, increasing incidence of trauma injuries, and expanding healthcare infrastructure across key countries in the region, leading to greater demand for effective bleeding control solutions in hospitals and ambulatory settings

- Furthermore, growing awareness regarding advanced wound care products, improving access to healthcare services, and the presence of multinational medical device manufacturers are establishing hemostats as an essential component of modern surgical practice. These converging factors are accelerating the adoption of hemostatic agents and products, thereby significantly boosting the regional market’s growth

Middle East and Africa Hemostats Market Analysis

- Hemostats, designed to control bleeding during surgical procedures and trauma care, are increasingly critical components of modern operating rooms and emergency settings across hospitals and ambulatory surgical centers due to their ability to reduce intraoperative blood loss, enhance surgical precision, and support faster patient recovery across multiple specialties

- The escalating demand for hemostats is primarily fueled by the rising volume of orthopedic, cardiovascular, and general surgeries, increasing prevalence of chronic disorders requiring operative intervention, and a growing number of trauma cases across the Middle East and Africa region

- Saudi Arabia dominated the Middle East and Africa hemostats market with the largest revenue share of 28.6% in 2025, characterized by expanding tertiary healthcare infrastructure, rising government healthcare expenditure under national transformation programs, and increased procurement of advanced surgical consumables

- South Africa is expected to be the fastest growing country during the forecast period due to improving access to surgical care, growing private healthcare investments, and expanding hospital capacity to manage trauma and emergency cases

- The thrombin based segment dominated the Middle East and Africa hemostats market with a market share of 34.1% in 2025, driven by its strong efficacy in rapid coagulation, wide usage across cardiovascular and neurological surgeries, and growing preference among surgeons for active hemostatic agents in high-risk procedures

Report Scope and Middle East and Africa Hemostats Market Segmentation

|

Attributes |

Middle East and Africa Hemostats Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Middle East and Africa

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Middle East and Africa Hemostats Market Trends

Rising Adoption of Advanced Combination and Thrombin-Based Hemostats in Complex Surgeries

- A significant and accelerating trend in the Middle East and Africa hemostats market is the growing preference for advanced thrombin-based and combination hemostats across tertiary hospitals and specialty surgical centers. This shift is significantly enhancing surgical efficiency and intraoperative bleeding management

- For instance, leading hospitals in Saudi Arabia and the UAE are increasingly incorporating combination hemostats in cardiovascular and neurological procedures to improve coagulation control and reduce operative time. Similarly, private hospital networks in South Africa are expanding the use of collagen and oxidized regenerated cellulose based products in general surgeries

- The integration of active hemostats in complex surgical workflows enables faster clot formation, improved precision in minimally invasive procedures, and reduced dependency on traditional suturing techniques. For instance, thrombin based products are widely utilized in cardiovascular surgery due to their rapid action and strong adhesion properties. Furthermore, matrix and gel hemostats offer surgeons improved handling characteristics and targeted application in delicate operative fields

- The growing availability of advanced formulations through multinational medical device manufacturers is facilitating broader product penetration across high-income Middle Eastern countries. Through centralized procurement systems, hospitals can standardize the use of premium hemostatic agents across multiple surgical departments, improving overall clinical outcomes

- The expansion of specialized surgical training programs and adoption of evidence-based bleeding management protocols are further supporting the integration of advanced hemostats into routine surgical practice across major metropolitan hospitals

- This trend toward technologically advanced and procedure-specific hemostatic solutions is reshaping surgical standards across the region. Consequently, companies are strengthening their regional distribution partnerships and introducing innovative formulations tailored to high-volume surgical specialties

- The demand for high-efficacy hemostats is expanding steadily across both public and private healthcare sectors, as providers increasingly prioritize patient safety, reduced blood loss, and shorter hospital stays

Middle East and Africa Hemostats Market Dynamics

Driver

Increasing Surgical Volume and Expanding Healthcare Infrastructure

- The rising incidence of chronic diseases requiring surgical intervention, coupled with expanding healthcare infrastructure investments, is a significant driver for the heightened demand for hemostats in the region

- For instance, ongoing healthcare transformation initiatives in Saudi Arabia and infrastructure expansion programs in the UAE are increasing the number of complex surgical procedures performed annually, thereby boosting demand for advanced bleeding control products. Such strategies by regional healthcare authorities are expected to drive the hemostats market growth in the forecast period

- As healthcare systems modernize and surgical capacities expand, hospitals are increasingly adopting active and combination hemostats to improve clinical efficiency and minimize postoperative complications

- Furthermore, the increasing focus on trauma management and emergency preparedness across Middle Eastern and African countries is positioning hemostats as essential consumables in operating rooms and emergency departments

- The growing presence of private hospitals, medical tourism in Gulf countries, and enhanced insurance coverage are key factors propelling the adoption of advanced hemostatic solutions. The trend toward minimally invasive and high-precision surgeries further contributes to sustained market expansion

- Rising government initiatives aimed at strengthening domestic healthcare manufacturing capabilities are also encouraging local distribution and availability of surgical consumables, including hemostatic agents

- Strategic collaborations between hospitals and multinational medical device companies are improving access to innovative formulations and clinical training, thereby accelerating product adoption across advanced care facilities

Restraint/Challenge

High Product Costs and Limited Access in Low-Income Regions

- Concerns surrounding the relatively high cost of advanced hemostatic agents, including thrombin based and combination products, pose a significant challenge to broader market penetration across price-sensitive African economies

- For instance, budget constraints in public healthcare facilities in parts of Sub-Saharan Africa can limit procurement of premium hemostatic formulations, restricting their widespread availability

- Addressing cost-related barriers through localized manufacturing, strategic pricing, and bulk procurement agreements is crucial for expanding accessibility. Companies operating in the region are increasingly focusing on distributor partnerships and tiered pricing strategies to improve market reach. In addition, disparities in healthcare infrastructure and limited surgical capacity in rural areas can hinder consistent demand for advanced hemostats

- Limited reimbursement frameworks and delayed payment cycles in certain public healthcare systems may further discourage procurement of higher-priced active hemostats

- Variability in regulatory standards and approval timelines across different African countries can create entry barriers for new product launches and slow overall market penetration

- While healthcare investments are gradually increasing, uneven resource distribution and reimbursement limitations may continue to restrict adoption in certain low-income settings

- Overcoming these challenges through policy support, training programs for surgical teams, and improved supply chain efficiency will be vital for sustained market growth across the Middle East and Africa

Middle East and Africa Hemostats Market Scope

The market is segmented on the basis of type, product, formulation, application, indication, and end-user.

- By Type

On the basis of type, the Middle East and Africa hemostats market is segmented into thrombin based, combination, oxidized regenerated cellulose based, gelatin based, and collagen based hemostat. The thrombin based segment dominated the market with the largest revenue share of 34.1% in 2025, driven by its rapid clotting capability and strong efficacy in controlling moderate to severe bleeding during complex surgical procedures. Thrombin based hemostats are widely preferred in cardiovascular and neurological surgeries due to their active mechanism of action and reliable performance in high-risk cases. Major tertiary hospitals in Saudi Arabia and the UAE increasingly procure thrombin formulations to enhance surgical efficiency and reduce intraoperative blood loss. Their compatibility with minimally invasive techniques and strong surgeon preference further strengthen their dominant position. In addition, growing awareness regarding advanced bleeding management solutions continues to support segment leadership across high-income Middle Eastern countries.

The combination segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by its dual-action mechanism that integrates active and passive components for enhanced hemostatic effectiveness. Combination products provide improved adhesion and faster coagulation, making them suitable for complex orthopedic and reconstructive surgeries. Increasing adoption of advanced surgical protocols in private hospitals across South Africa and the Gulf region is accelerating demand for these products. Their versatility across multiple surgical specialties enhances procurement preference among hospital administrators. Furthermore, continuous product innovation and rising clinical evidence supporting superior outcomes are contributing to strong projected growth.

- By Product

On the basis of product, the market is segmented into active hemostats, passive hemostats, combination hemostats, and others. The active hemostats segment dominated the market in 2025 due to their ability to directly stimulate the coagulation cascade and provide rapid bleeding control. These products are highly utilized in cardiovascular, neurological, and trauma surgeries where immediate hemostasis is critical. Hospitals across the UAE and Saudi Arabia prefer active formulations to minimize surgical complications and reduce operative time. Their strong clinical efficacy and increasing surgeon familiarity further reinforce market dominance. Growing investments in advanced surgical consumables also contribute to sustained segment demand.

The combination hemostats segment is expected to register the fastest CAGR during the forecast period, driven by rising demand for multi-functional bleeding control solutions. These products combine mechanical barriers with active clotting agents, offering superior performance in complex surgical environments. Expanding private healthcare infrastructure and increasing high-value surgical procedures in the region are supporting rapid adoption. Surgeons are increasingly favoring combination products for their enhanced safety and effectiveness profile. Ongoing technological advancements and new product launches further strengthen their growth trajectory.

- By Formulation

On the basis of formulation, the market is segmented into matrix and gel hemostats, sheet and pad hemostats, sponge hemostats, and powder hemostats. The matrix and gel hemostats segment dominated the market in 2025, owing to their superior conformability and ease of application in irregular wound surfaces. These formulations are widely used in minimally invasive and delicate surgeries due to precise application capability. Their effectiveness in controlling active bleeding makes them a preferred choice in cardiovascular and neurological procedures. Hospitals in high-income Middle Eastern countries increasingly standardize gel-based products across surgical departments. Strong product availability and clinical reliability contribute to their leading position.

The powder hemostats segment is projected to grow at the fastest rate from 2026 to 2033, driven by increasing use in emergency and trauma care settings. Powder formulations are easy to store, apply rapidly, and require minimal preparation time. Growing trauma incidence and emergency preparedness initiatives across African countries are supporting higher adoption. Their cost-effectiveness compared to advanced gel products enhances penetration in resource-limited healthcare facilities. Rising awareness and improved distribution networks are expected to accelerate segment expansion

- By Application

On the basis of application, the market is segmented into orthopedic, general surgery, neurological surgery, cardiovascular surgery, reconstructive surgery, and gynecological surgery. The general surgery segment dominated the market in 2025 due to the high volume of routine surgical procedures performed across hospitals in the region. Hemostats are extensively utilized in abdominal and soft tissue surgeries to control bleeding efficiently. Increasing surgical admissions and expanding hospital infrastructure drive segment demand. Public and private hospitals alike rely on hemostatic agents to enhance patient safety and reduce complications. The broad scope of general surgery procedures ensures sustained consumption levels.

The cardiovascular surgery segment is expected to witness the fastest growth during the forecast period, fueled by rising prevalence of cardiovascular diseases in Middle Eastern countries. Complex cardiac procedures require highly effective bleeding control solutions, increasing adoption of advanced hemostats. Expanding specialized cardiac centers and improving diagnostic rates contribute to higher surgical volumes. Surgeons increasingly demand high-efficacy thrombin and combination products in these procedures. Continued investments in tertiary cardiac care facilities are anticipated to support rapid segment growth.

- By Indication

On the basis of indication, the market is segmented into wound closure and surgery. The surgery segment dominated the market in 2025, driven by increasing procedural volumes across multiple specialties. Hemostats are routinely used during operative interventions to minimize blood loss and improve clinical outcomes. Expanding hospital capacity and rising elective surgical procedures strengthen segment leadership. Growing medical tourism in Gulf countries also supports higher surgical demand. The essential role of hemostats in operative settings sustains dominant revenue contribution.

The wound closure segment is projected to grow at the fastest pace from 2026 to 2033, supported by increasing trauma cases and outpatient procedures. Rising awareness regarding advanced wound care management enhances adoption. Community healthcare centers and ambulatory facilities are incorporating hemostatic agents for minor procedures. Expanding emergency response systems across African nations further stimulate demand. Improved product accessibility and affordability contribute to accelerating growth.

- By End-User

On the basis of end-user, the market is segmented into hospitals, clinics, ambulatory centers, community healthcare, and others. The hospitals segment dominated the market in 2025 due to the high concentration of surgical procedures performed in tertiary and secondary care facilities. Hospitals account for the majority of complex surgeries requiring advanced bleeding management solutions. Strong procurement capabilities and access to premium hemostatic products reinforce segment dominance. Government investments in hospital expansion across Saudi Arabia and the UAE further strengthen demand. The presence of specialized surgical departments ensures consistent product utilization.

The ambulatory centers segment is anticipated to witness the fastest growth during the forecast period, driven by the increasing shift toward outpatient and minimally invasive procedures. Ambulatory facilities prioritize efficient and quick-acting hemostatic agents to reduce patient recovery time. Expanding private healthcare infrastructure in urban centers supports segment expansion. Cost-effective treatment models and shorter hospital stays encourage outpatient surgical adoption. Continuous growth in day-care surgical services is expected to propel demand for hemostats in this segment.

Middle East and Africa Hemostats Market Regional Analysis

- Saudi Arabia dominated the Middle East and Africa hemostats market with the largest revenue share of 28.6% in 2025, characterized by expanding tertiary healthcare infrastructure, rising government healthcare expenditure under national transformation programs, and increased procurement of advanced surgical consumables

- Healthcare providers in the country highly prioritize advanced bleeding management solutions, clinical efficiency, and improved surgical outcomes, increasing the adoption of thrombin based and combination hemostats across cardiovascular, orthopedic, and neurological procedures

- This widespread adoption is further supported by growing healthcare expenditure, the presence of well-equipped specialty hospitals, and increasing medical tourism, establishing advanced hemostatic products as a preferred solution for complex surgical interventions across major healthcare facilities

The Saudi Arabia Hemostats Market Insight

The Saudi Arabia hemostats market captured the largest revenue share of 28.6% in 2025 within the Middle East and Africa, fueled by expanding tertiary healthcare infrastructure and rising volumes of complex surgical procedures. Healthcare providers are increasingly prioritizing advanced bleeding management solutions to enhance surgical precision and patient outcomes. The growing prevalence of cardiovascular and orthopedic conditions, combined with substantial government healthcare investments under national transformation programs, further propels market growth. Moreover, the increasing adoption of thrombin based and combination hemostats in specialized hospitals is significantly contributing to the country’s market expansion.

UAE Hemostats Market Insight

The UAE hemostats market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by advanced healthcare facilities and increasing demand for minimally invasive surgical procedures. In addition, the country’s position as a medical tourism hub is encouraging hospitals to adopt premium bleeding control solutions. The UAE’s strong regulatory framework and high per capita healthcare spending are expected to continue stimulating market growth. Growing partnerships with multinational medical device manufacturers further support access to innovative formulations.

South Africa Hemostats Market Insight

The South Africa hemostats market is expected to expand at a considerable CAGR during the forecast period, fueled by improving access to surgical care and increasing private healthcare investments. South Africa’s relatively developed healthcare infrastructure within Sub-Saharan Africa supports broader adoption of advanced hemostatic agents. The rising burden of trauma injuries and chronic diseases requiring operative management is promoting demand across public and private hospitals. The integration of active hemostats into trauma and emergency care protocols is also becoming increasingly prevalent, aligning with the country’s efforts to strengthen surgical capacity.

Egypt Hemostats Market Insight

The Egypt hemostats market accounted for a significant market revenue share in the region in 2025, attributed to its large patient population and expanding network of public and private hospitals. Egypt stands as one of the key healthcare markets in North Africa, and hemostatic products are becoming increasingly utilized in general and orthopedic surgeries. The push toward upgrading surgical infrastructure and improving access to advanced medical consumables, alongside partnerships with international suppliers, are key factors propelling the market in Egypt.

Middle East and Africa Hemostats Market Share

The Middle East and Africa Hemostats industry is primarily led by well-established companies, including:

- Johnson & Johnson Services, Inc. (U.S.)

- Baxter (U.S.)

- Pfizer Inc. (U.S.)

- B. Braun SE (Germany)

- Medtronic (Ireland)

- Stryker (U.S.)

- Advanced Medical Solutions Group plc (U.K.)

- Integra LifeSciences Holdings Corporation (U.S.)

- GELITA Medical GmbH (Germany)

- Marine Polymer Technologies, Inc. (U.S.)

- CELOX Medical Ltd (U.K.)

- Meril Life Sciences Pvt. Ltd. (India)

- Aegis Lifesciences Pvt. Ltd (India)

- 3-D Matrix Medical Technology Co., Ltd. (Japan)

- Haemonetics Corp (U.S.)

- Zimmer Biomet. (U.S.)

- CryoLife, Inc. (U.S.)

- BD (U.S.)

- Teleflex Incorporated (U.S.)

What are the Recent Developments in Middle East and Africa Hemostats Market?

- In July 2025, BloodSTOP® iX was reported to have gained traction in Algeria, where surgeons are using the product as an innovative hemostatic aid for bleeding control, signaling broader adoption of advanced hemostatic agents within North African clinical practice

- In May 2025, Merit Medical Systems, Inc. acquired Biolife Delaware, LLC, a manufacturer of StatSeal® and WoundSeal® hemostatic devices, expanding its portfolio of bleeding control products used in interventional radiology, cardiology, dialysis and other procedures

- In May 2025, industry news confirmed that Merit Medical’s acquisition of Biolife intended to broaden hemostatic solutions such as StatSeal and WoundSeal will contribute to enhancing patient care and clinician options worldwide

- In May 2023, KITSS Therapeutics introduced BloodSTOP® iX Advanced Hemostat with WoundHEAL technology to Ghana, a plant-based hemostatic solution designed to rapidly control bleeding and promote wound healing in surgical, trauma, and burn care settings, marking expanded regional access to innovative bleeding control products

- In April 2023, Olympus launched a portfolio of EndoClot hemostatic agents, including EndoClot Adhesive, Polysaccharide Hemostatic Spray (PHS), and Submucosal Injection Solution (SIS), across the Europe, Middle East & Africa (EMEA) region to improve bleeding control in gastrointestinal procedures

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.