Middle East And Africa Automotive Sensors Market

Market Size in USD Billion

CAGR :

%

USD

1.37 Billion

USD

2.21 Billion

2025

2033

USD

1.37 Billion

USD

2.21 Billion

2025

2033

| 2026 –2033 | |

| USD 1.37 Billion | |

| USD 2.21 Billion | |

| % | |

|

What is the Middle East and Africa Automotive Sensors Market Size and Growth Rate?

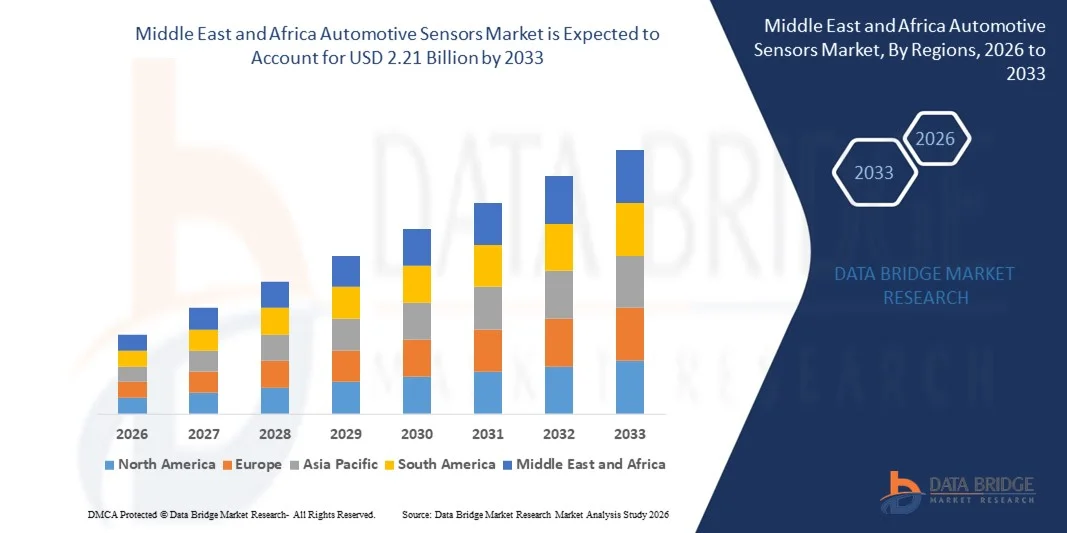

- The Middle East and Africa automotive sensors market size was valued at USD 1.37 billion in 2025 and is expected to reach USD 2.21 billion by 2033, at a CAGR of 6.1% during the forecast period

- This growth is driven by factors such as the advancements in automotive technology, rising demand for advanced driver assistance systems (ADAS), and proliferation of electric vehicles (EVs) technology

What are the Major Takeaways of Automotive Sensors Market?

- Automotive sensors are the sensors that are scan the surrounding environment and then detect, measure, and transmit the information as an electric or optical signal to the concerned component. The automotive sensors are capable of sensing heat, light, motion, moisture, and pressure

- Surging number of collaborations among vehicle original equipment manufacturers and sensor manufacturers, rise in the advancements in production technology and increasing application of automotive sensors for a wide range of applications such as powertrain, chassis, exhaust, safety and control, body electronics, telematics, and others are the major factors attributable to the growth of automotive sensors market

- U.A.E. dominated the Middle East and Africa automotive sensors market with the largest revenue share of 38.9% in 2025, supported by the country’s rapid development of smart transportation infrastructure, strong automotive aftermarket demand, and increasing adoption of connected vehicle technologies

- Saudi Arabia is witnessing the fastest growth rate of 11.8% in the Middle East and Africa region, driven by increasing investments in automotive manufacturing, smart transportation infrastructure, and electric vehicle adoption

- The Pressure Sensors segment dominated the market with the largest market revenue share of 22.8% in 2024, primarily due to their extensive use in engine management systems, tire pressure monitoring systems (TPMS), fuel systems, and braking systems

Report Scope and Automotive Sensors Market Segmentation

|

Attributes |

Automotive Sensors Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Middle East and Africa

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

What is the Key Trend in the Automotive Sensors Market?

Increasing Integration of Advanced Sensors for Autonomous and Connected Vehicles

- The automotive sensors market is witnessing a strong trend toward the increasing integration of advanced sensing technologies that support autonomous driving, vehicle connectivity, and enhanced safety systems in modern vehicles

- Sensors such as radar, LiDAR, camera sensors, pressure sensors, and temperature sensors are being widely deployed to enable real-time vehicle monitoring, object detection, and environment sensing for advanced driver assistance systems (ADAS)

- For instance, Bosch has introduced next-generation radar and environmental sensors designed to improve collision avoidance, adaptive cruise control, and lane-keeping assistance in connected vehicles

- Automotive manufacturers are increasingly integrating multi-sensor fusion technologies, where data from multiple sensors is combined to improve vehicle perception accuracy and decision-making capabilities

- For instance, Continental AG has developed advanced sensor platforms that combine camera, radar, and ultrasonic sensors to support autonomous driving and vehicle safety functions

- Another key aspect of this trend is the integration of automotive sensors with artificial intelligence and edge computing, enabling vehicles to process environmental data in real time and respond more effectively to dynamic driving conditions

- The adoption of intelligent sensor technologies is expected to expand further as automotive manufacturers accelerate the development of autonomous vehicles, connected mobility solutions, and smart transportation systems

What are the Key Drivers of Automotive Sensors Market?

- The growing demand for vehicle safety systems and advanced driver assistance technologies is one of the primary drivers accelerating the adoption of automotive sensors across global vehicle production

- Governments and regulatory authorities worldwide are implementing strict vehicle safety regulations that require the integration of sensors for functions such as automatic emergency braking, lane departure warning, blind spot detection, and parking assistance

- For instance, DENSO Corporation has introduced advanced automotive sensors designed to improve vehicle stability control, collision prevention systems, and engine performance monitoring

- The rapid growth of electric vehicles (EVs) and connected cars is further driving demand for sensors that monitor battery systems, thermal management, vehicle positioning, and driver behavior

- In addition, the increasing adoption of vehicle electrification, smart mobility technologies, and in-vehicle electronics is encouraging automotive manufacturers to integrate a higher number of sensors within modern vehicle architectures

- For instance, Texas Instruments provides advanced semiconductor-based sensor solutions that support battery management systems, powertrain monitoring, and vehicle safety applications

- These technological advancements are expected to continue driving the demand for automotive sensors as the industry shifts toward autonomous mobility, connected vehicles, and intelligent transportation systems

Which Factor is Challenging the Growth of the Automotive Sensors Market?

- One of the major challenges in the automotive sensors market is the high cost associated with advanced sensor technologies, particularly those used in autonomous vehicles and high-end driver assistance systems

- The integration of multiple sensors such as LiDAR, radar, cameras, and ultrasonic sensors requires sophisticated electronic architectures and complex calibration processes, increasing overall vehicle production costs

- For instance, advanced automotive sensing solutions developed by companies such as Infineon Technologies require specialized semiconductor components and precise manufacturing processes, which can increase system costs

- In addition, automotive manufacturers must invest heavily in software development, sensor fusion algorithms, and testing infrastructure to ensure reliable sensor performance under diverse driving conditions

- Another challenge is the complexity of integrating multiple sensors within vehicle electronic control units (ECUs) while maintaining system reliability, safety, and data accuracy

- Supply chain disruptions and shortages of semiconductor components and sensing devices can also impact production timelines and increase manufacturing costs

- Addressing these challenges through cost-efficient semiconductor technologies, improved sensor integration platforms, and scalable manufacturing solutions will be crucial for sustaining long-term growth in the automotive sensors market

How is the Automotive Sensors Market Segmented?

The market is segmented on the basis of sensor type, vehicle type, application, and technology.

- By Sensor Type

On the basis of sensor type, the automotive sensors market is segmented into Temperature Sensors, Pressure Sensors, Position Sensors, Oxygen Sensors, NOx Sensors, Speed Sensors, Inertial Sensors, Image Sensors, and Other Sensors. The Pressure Sensors segment dominated the market with the largest market revenue share of 22.8% in 2024, primarily due to their extensive use in engine management systems, tire pressure monitoring systems (TPMS), fuel systems, and braking systems. Pressure sensors play a critical role in monitoring fuel injection pressure, oil pressure, and air intake levels, ensuring optimal engine performance and vehicle efficiency. With increasing emphasis on fuel efficiency, emission reduction, and vehicle safety, automakers are widely integrating pressure sensors across modern vehicle platforms. Continuous advancements in semiconductor sensor technology and MEMS-based pressure sensors have improved accuracy, durability, and real-time monitoring capabilities.

The Image Sensors segment is expected to witness the fastest CAGR of 10.9% from 2025 to 2032, driven by the rapid expansion of advanced driver assistance systems (ADAS), autonomous driving technologies, and vehicle safety features. Image sensors enable object detection, lane monitoring, driver assistance, and environment perception, making them essential components in modern connected and autonomous vehicles.

- By Vehicle Type

On the basis of vehicle type, the automotive sensors market is segmented into Passenger Car, Light Commercial Vehicles, and Heavy Commercial Vehicles. The Passenger Car segment dominated the market with the largest revenue share of 63.5% in 2024, driven by the high global production of passenger vehicles and the increasing integration of advanced safety systems, emission control technologies, and vehicle electronics. Modern passenger cars are equipped with a wide range of sensors used for engine management, braking systems, vehicle stability control, airbag deployment, and driver assistance systems. Growing consumer demand for connected vehicles, electric vehicles, and intelligent safety technologies has significantly increased the number of sensors used per vehicle, strengthening the segment’s market dominance.

The Light Commercial Vehicles segment is expected to witness the fastest CAGR of 9.7% from 2025 to 2032, supported by the rapid expansion of e-commerce logistics, urban delivery networks, and fleet management systems. These vehicles increasingly adopt advanced sensor technologies for vehicle tracking, fuel efficiency monitoring, driver safety, and predictive maintenance.

- By Application

On the basis of application, the automotive sensors market is segmented into Powertrain, Chassis, Exhaust, Safety and Control, Body Electronics, Telematics, and Others. The Powertrain segment dominated the market with the largest revenue share of 28.9% in 2024, driven by the extensive use of sensors in engine management, fuel injection systems, transmission control, and thermal monitoring. Automotive sensors play a crucial role in optimizing engine efficiency, fuel consumption, and emission control, which is increasingly important as governments worldwide implement stricter vehicle emission regulations. Sensors used in powertrain systems help monitor temperature, pressure, speed, and air-fuel ratios, enabling improved vehicle performance and regulatory compliance.

The Safety and Control segment is expected to witness the fastest CAGR of 11.2% from 2025 to 2032, supported by the rapid adoption of ADAS technologies, collision avoidance systems, and autonomous driving features. Safety sensors such as radar, cameras, and inertial sensors enable real-time vehicle monitoring and improved road safety.

- By Technology

On the basis of technology, the automotive sensors market is segmented into Micro-Electro-Mechanical Systems (MEMS) and Nano-Electro-Mechanical Systems (NEMS). The Micro-Electro-Mechanical Systems (MEMS) segment dominated the market with the largest revenue share of 71.4% in 2024, primarily due to the widespread use of MEMS-based sensors in automotive applications such as accelerometers, gyroscopes, pressure sensors, and inertial measurement units. MEMS technology offers advantages such as compact size, high sensitivity, low power consumption, and cost-effective mass production, making it highly suitable for modern vehicle electronic systems. Automakers widely adopt MEMS sensors in airbag deployment systems, electronic stability control, tire pressure monitoring systems, and navigation systems.

The Nano-Electro-Mechanical Systems (NEMS) segment is expected to witness the fastest CAGR of 12.3% from 2025 to 2032, driven by ongoing advancements in nanotechnology and next-generation sensing technologies. NEMS sensors offer ultra-high sensitivity, faster response times, and improved performance, supporting future developments in autonomous vehicles and advanced automotive electronics.

Which Region Holds the Largest Share of the Automotive Sensors Market?

- U.A.E. dominated the Middle East and Africa automotive sensors market with the largest revenue share of 38.9% in 2025, supported by the country’s rapid development of smart transportation infrastructure, strong automotive aftermarket demand, and increasing adoption of connected vehicle technologies. The U.A.E. has emerged as a regional hub for automotive innovation and intelligent mobility solutions, with growing integration of advanced driver assistance systems (ADAS), vehicle monitoring technologies, and electronic control systems in modern vehicles. Automotive manufacturers and mobility solution providers are increasingly incorporating temperature sensors, pressure sensors, inertial sensors, and image sensors to enhance vehicle safety, efficiency, and performance. The presence of strong automotive service networks, luxury vehicle markets, and technology-driven transportation projects is significantly accelerating the adoption of automotive sensors across the country

- In the country, the increasing deployment of sensor-based vehicle safety technologies, telematics platforms, and fleet management systems is significantly boosting the demand for automotive sensors. Automotive service providers and fleet operators are integrating advanced sensing technologies to support predictive maintenance, vehicle diagnostics, and driver safety monitoring, which improves operational efficiency and reduces maintenance costs

- In the U.A.E., the rising focus on smart mobility, connected vehicle infrastructure, and intelligent transportation systems further strengthens the country’s leadership position within the Middle East and Africa Automotive Sensors market

Saudi Arabia Automotive Sensors Market Insight

Saudi Arabia is witnessing the fastest growth rate of 11.8% in the Middle East and Africa region, driven by increasing investments in automotive manufacturing, smart transportation infrastructure, and electric vehicle adoption. The country’s automotive sector is undergoing transformation under Vision 2030, which encourages the development of advanced mobility technologies and intelligent transportation networks. Automotive manufacturers and suppliers are increasingly integrating sensor-based safety systems, engine monitoring technologies, and vehicle control solutions into modern vehicles. Major cities such as Riyadh, Jeddah, and Dammam are witnessing growing demand for vehicles equipped with ADAS, telematics platforms, and electronic safety systems. In addition, the expansion of logistics fleets, public transportation modernization, and connected vehicle initiatives is further strengthening the demand for advanced automotive sensors across the country.

South Africa Automotive Sensors Market Insight

In South Africa, the automotive sensors market is expanding steadily, supported by the growing adoption of vehicle safety technologies, automotive electronics, and intelligent fleet management systems. The country has a well-established automotive manufacturing sector, with major vehicle assembly plants and component suppliers operating across the region. Automotive manufacturers are increasingly integrating engine sensors, pressure sensors, speed sensors, and emission monitoring sensors to improve vehicle performance and comply with evolving emission standards. Major urban centers such as Johannesburg, Cape Town, and Durban are witnessing increased demand for vehicles equipped with advanced safety and control technologies. In addition, rising adoption of connected vehicle solutions, predictive maintenance platforms, and digital fleet monitoring systems is encouraging automotive companies to incorporate advanced sensor technologies, positioning South Africa as a key contributor to the regional Automotive Sensors market growth.

Which are the Top Companies in Automotive Sensors Market?

The automotive sensors industry is primarily led by well-established companies, including:

- NXP Semiconductors (Netherlands)

- STMicroelectronics (Switzerland)

- Infineon Technologies AG (Germany)

- TE Connectivity (Switzerland)

- Texas Instruments Incorporated (U.S.)

- Sensata Technologies, Inc. (U.S.)

- Littelfuse Inc. (U.S.)

- Robert Bosch GmbH (Germany)

- Continental AG (Germany)

- BorgWarner Inc. (U.S.)

- Analog Devices, Inc. (U.S.)

- Sensata Technologies, Inc. (U.S.)

- DENSO CORPORATION (Japan)

- Autoliv Inc. (Sweden)

- Maxim Integrated (U.S.)

- Hitachi Astemo Americas, Inc. (U.S.)

- GMS Instruments BV (Netherlands)

- Broadcom Inc. (U.S.)

- Piher Sensors & Controls (Spain)

- Elmos Semiconductor SE (Germany)

What are the Recent Developments in Global Automotive Sensors Market?

- In October 2024, Infineon unveiled the CYFP10020A00 and CYFP10020S00 automotive-grade fingerprint sensor ICs. These sensors are specifically designed to work seamlessly with Infineon's TRAVEO™ T2G microcontrollers, providing accurate fingerprint identification for enhanced in-vehicle personalization and secure payment authentication. Compliant with AEC-Q100 standards, these sensors feature encrypted data output through an SPI interface, ensuring a high level of data security and reliability in automotive applications

- In December 2023, Continental introduced a valve cap sensor designed for commercial vehicle tires. This new sensor enables real-time tire pressure monitoring and is compatible with tires from all major manufacturers. The sensor integrates smoothly with Continental’s ContiConnect platform, which helps fleet operators monitor tire health, optimize maintenance schedules, and improve vehicle uptime by preventing tire-related issues

- At CES 2024, Texas Instruments launched the AWR2544, a 77GHz millimeter-wave radar sensor chip that introduces a new level of vehicle sensing capabilities. This cutting-edge chip extends detection ranges beyond 200 meters, significantly improving the performance of Advanced Driver Assistance Systems (ADAS) by enhancing situational awareness. In addition, TI introduced DRV3946-Q1 and DRV3901-Q1 driver chips for battery management and powertrain systems, offering built-in diagnostics and ensuring functional safety compliance, crucial for reliable electric vehicle operations

- In April 2024, Infineon expanded its portfolio with the launch of the PSoC™ 4 HVMS family of programmable microcontrollers. These new microcontrollers integrate advanced high-voltage features and analog capabilities, making them suitable for applications such as touch-enabled human-machine interfaces (HMIs) and other smart sensing technologies. With AEC-Q100 certification and ISO26262 compliance, these microcontrollers are built to meet stringent safety and reliability requirements for automotive applications

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.