Middle East And Africa Glass Packaging Market

Market Size in USD Billion

CAGR :

%

USD

5.55 Billion

USD

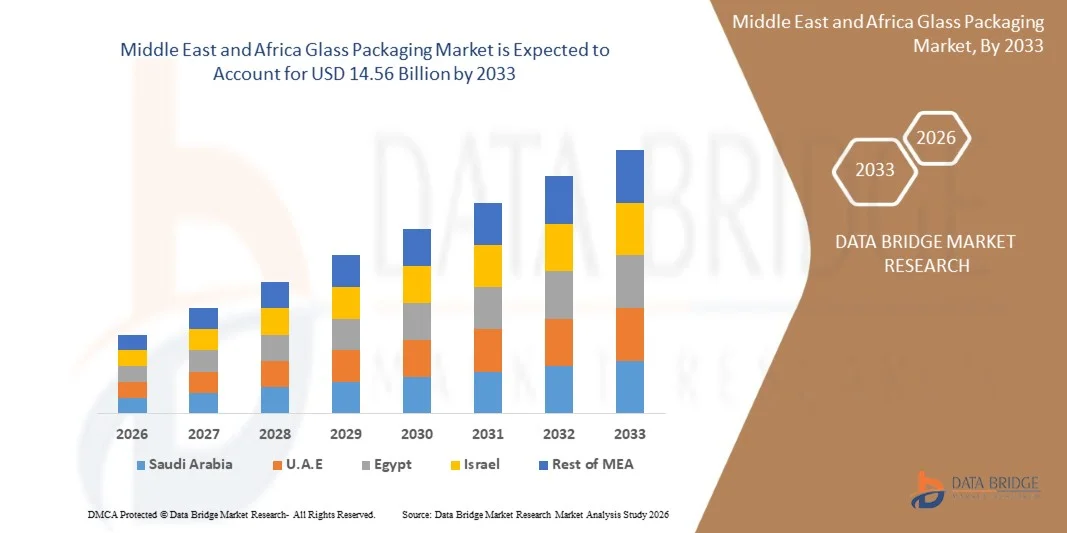

14.56 Billion

2025

2033

USD

5.55 Billion

USD

14.56 Billion

2025

2033

| 2026 –2033 | |

| USD 5.55 Billion | |

| USD 14.56 Billion | |

| % | |

|

Middle East and Africa Glass Packaging Market Size

- The Middle East and Africa glass packaging market size was valued at USD 5.55 billion in 2025 and is expected to reach USD 14.56 billion by 2033, at a CAGR of 5.00% during the forecast period

- The market growth is largely fuelled by the rising demand for sustainable and recyclable packaging solutions across food and beverage, pharmaceuticals, cosmetics, and personal care industries, alongside increasing consumer preference for premium and environmentally responsible packaging materials

- Expanding alcoholic and non-alcoholic beverage industries, growing pharmaceutical manufacturing, and increasing urbanization across Middle East and Africa are significantly driving the adoption of glass packaging due to its superior product protection, chemical stability, and premium brand positioning

Middle East and Africa Glass Packaging Market Analysis

- Glass packaging plays a vital role in preserving product quality, extending shelf life, and supporting premium product branding, particularly in beverages, pharmaceuticals, cosmetics, and specialty food applications across Middle East and Africa

- The market is witnessing stable growth due to increasing sustainability awareness, rising demand for recyclable packaging alternatives, and expanding industrial production capacities across emerging economies in the region

- South Africa glass packaging market accounted for the largest revenue share in Africa in 2025, attributed to its well-established beverage industry, strong presence of wineries and breweries, and growing pharmaceutical manufacturing base

- U.A.E. is expected to witness the highest compound annual growth rate (CAGR) in the Middle East and Africa glass packaging market due to rapid expansion of the food and beverage industry, rising demand for premium packaging formats, strong retail and hospitality growth, and increasing focus on sustainable packaging initiatives

- The Type III segment held the largest market revenue share in 2025 driven by its extensive use in food, beverage, and personal care packaging due to its cost-effectiveness, chemical durability, and versatility. Type III glass is widely preferred for commercial packaging applications across the region because it offers reliable strength and broad compatibility with a wide range of products

Report Scope and Middle East and Africa Glass Packaging Market Segmentation

|

Attributes |

Middle East and Africa Glass Packaging Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Middle East and Africa

|

|

Key Market Players |

• Saudi Glass Company (Saudi Arabia) |

|

Market Opportunities |

• Expansion Of Sustainable And Recyclable Packaging Infrastructure |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Middle East and Africa Glass Packaging Market Trends

“Rising Demand for Sustainable, Premium, and Recyclable Packaging Solutions”

• The growing focus on environmentally responsible packaging and premium product presentation is significantly shaping the Middle East and Africa glass packaging market, as manufacturers and consumers increasingly prefer packaging materials that are recyclable, chemically stable, and capable of preserving product integrity. Glass packaging is gaining substantial traction due to its superior barrier properties, premium appearance, and alignment with sustainability goals without compromising product quality. This trend is strengthening adoption across beverage, food, pharmaceutical, cosmetics, and personal care industries, encouraging manufacturers to innovate with lightweight, decorative, and energy-efficient glass packaging solutions that meet evolving market expectations

• Increasing awareness around environmental sustainability, product safety, and premium consumption has accelerated demand for glass packaging across alcoholic beverages, non-alcoholic beverages, pharmaceuticals, and luxury cosmetic products. Consumers and businesses are actively seeking packaging solutions that support recyclability, product preservation, and premium brand differentiation, prompting manufacturers to prioritize sustainable production practices and advanced packaging designs. This has also led to collaborations between glass manufacturers, consumer brands, and recycling organizations to enhance supply chain efficiency and environmental performance

• Sustainability and premiumization trends are strongly influencing purchasing decisions, with manufacturers emphasizing eco-friendly manufacturing, recycled content integration, lightweight product development, and advanced decorative packaging capabilities. These factors are helping companies differentiate offerings in a competitive market while strengthening consumer trust and regulatory compliance. Businesses are increasingly leveraging sustainability certifications and marketing campaigns to reinforce product positioning and attract environmentally conscious consumers

• For instance, in 2024, major beverage and pharmaceutical packaging companies across Saudi Arabia, South Africa, and the U.A.E. expanded their glass packaging portfolios by introducing lightweight, recyclable, and premium-designed bottles and containers for beverages, medicines, and personal care products. These product launches were introduced in response to rising regional demand for sustainable and high-quality packaging solutions, with broad distribution across retail, healthcare, and industrial channels. The products were also marketed as environmentally responsible alternatives, enhancing brand reputation and customer loyalty

• While demand for glass packaging is steadily growing, sustained market expansion depends on continuous manufacturing innovation, cost-efficient production, and maintaining supply chain reliability amid energy-intensive production requirements. Manufacturers are also focusing on improving recyclability, operational scalability, and production efficiency to support broader adoption across regional industries

Middle East and Africa Glass Packaging Market Dynamics

Driver

“Growing Preference for Sustainable and Premium Packaging Materials”

• Rising consumer and industrial demand for recyclable, chemically inert, and premium packaging materials is a major driver for the Middle East and Africa glass packaging market. Manufacturers are increasingly replacing plastic and other packaging materials with glass alternatives to meet sustainability targets, improve product safety, and strengthen premium brand appeal. This trend is also accelerating research into lightweight glass production, recycled material integration, and energy-efficient manufacturing technologies, supporting product diversification

• Expanding applications in beverages, pharmaceuticals, food products, cosmetics, and personal care are significantly influencing market growth. Glass packaging helps preserve flavor, stability, and product quality while supporting sustainability positioning and premium consumer experiences. The increasing regional focus on environmental regulations, consumer safety, and premium product branding further reinforces this trend

• Packaging manufacturers and consumer brands are actively promoting glass packaging solutions through product innovation, sustainability initiatives, and advanced decorative technologies. These efforts are supported by the growing consumer preference for eco-friendly and premium products, alongside increasing investments in regional manufacturing and recycling infrastructure. Collaborations between glass producers, brand owners, and distribution networks are also improving product competitiveness and sustainability outcomes

• For instance, in 2023, leading packaging manufacturers in the Middle East and Africa reported expanded production of recyclable and premium glass packaging solutions for beverage, pharmaceutical, and cosmetic applications. This expansion followed rising demand for sustainable packaging, increasing premium product consumption, and stronger environmental commitments from major consumer brands. Companies also emphasized traceability, recycling capabilities, and aesthetic innovation to strengthen competitive positioning and long-term market growth

• Although rising sustainability and premiumization trends strongly support growth, broader market expansion depends on energy cost optimization, raw material availability, and scalable manufacturing processes. Continued investment in sustainable production technologies, recycling systems, and operational efficiency will be critical for meeting regional demand and maintaining competitive advantage

Restraint/Challenge

“High Production Costs and Energy-Intensive Manufacturing Processes”

• The relatively high production and transportation costs associated with glass packaging compared to alternative materials remain a key challenge, limiting broader adoption among cost-sensitive manufacturers. Energy-intensive manufacturing processes, heavy product weight, and logistical complexities contribute to elevated operational expenses. In addition, fluctuating energy prices and raw material costs can further impact production economics and market competitiveness

• Consumer and manufacturer adoption remains uneven in certain emerging markets where lower-cost packaging alternatives such as plastics continue to dominate. Limited awareness of long-term sustainability and premium benefits can restrict broader market penetration across price-sensitive industries. This also slows the adoption of innovative glass packaging technologies in some developing economies

• Supply chain and recycling infrastructure challenges also impact market growth, as glass packaging requires robust collection systems, recycling investments, and efficient transportation networks. Manufacturers must invest in sustainable logistics, advanced recycling technologies, and production modernization to maintain product affordability and competitiveness

• For instance, in 2024, several packaging distributors and manufacturers across Africa and the Middle East reported operational pressures due to rising fuel costs, limited recycling infrastructure, and fluctuating raw material expenses. Premium pricing and logistical burdens created barriers for certain food and beverage manufacturers, while energy-intensive production requirements increased supply chain complexity. These factors also affected pricing flexibility and broader market accessibility

• Overcoming these challenges will require energy-efficient manufacturing, expanded recycling ecosystems, and stronger awareness initiatives for both manufacturers and consumers. Collaboration with governments, recycling organizations, consumer brands, and logistics providers can help unlock the long-term growth potential of the Middle East and Africa glass packaging market. Furthermore, strengthening cost competitiveness, production scalability, and sustainability alignment will be essential for widespread regional adoption

Middle East and Africa Glass Packaging Market Scope

The market is segmented on the basis of glass type, jar size, raw material, and application.

• By Glass Type

On the basis of glass type, the Middle East and Africa glass packaging market is segmented into Type I, Type II, Type III, and Others. The Type III segment held the largest market revenue share in 2025 driven by its extensive use in food, beverage, and personal care packaging due to its cost-effectiveness, chemical durability, and versatility. Type III glass is widely preferred for commercial packaging applications across the region because it offers reliable strength and broad compatibility with a wide range of products.

The Type I segment is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing demand from the pharmaceutical and healthcare sectors where superior chemical resistance and product safety are critical. Type I borosilicate glass is gaining strong adoption for premium pharmaceutical containers and specialized packaging solutions due to its high thermal resistance and durability.

• By Jar Size

On the basis of jar size, the Middle East and Africa glass packaging market is segmented into 20-50 mL, 51-100 mL, 101-250 mL, 251-500 mL, and Above 500 mL. The Above 500 mL segment held the largest market revenue share in 2025 driven by strong demand from alcoholic beverages, non-alcoholic beverages, and bulk food storage applications. Larger glass containers are widely utilized for beverage bottling and large-volume food packaging due to their convenience, durability, and ability to preserve product quality over extended periods.

The 101-250 mL segment is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing consumer demand for compact pharmaceutical packaging, cosmetics, and premium personal care products. Mid-sized jars are becoming increasingly popular due to their portability, product differentiation, and suitability for specialized packaging applications.

• By Raw Material

On the basis of raw material, the Middle East and Africa glass packaging market is segmented into Cullet, Selenium, Cobalt Oxide, Limestone, Dolomite, Coloring Material, and Others. The Cullet segment held the largest market revenue share in 2025 driven by rising emphasis on sustainable manufacturing practices and the increasing use of recycled glass in production processes. Cullet significantly reduces energy consumption and raw material costs while supporting environmental sustainability initiatives across the region.

The Coloring Material segment is expected to witness the fastest growth rate from 2026 to 2033, driven by growing demand for differentiated packaging designs and enhanced product branding in beverage, beauty, and personal care industries. Colored glass packaging is increasingly adopted for aesthetic appeal, UV protection, and premium product positioning.

• By Application

On the basis of application, the Middle East and Africa glass packaging market is segmented into Alcoholic Beverage, Non-Alcoholic Beverage, Food, Pharmaceutical, Personal Care, Beauty Products, and Others. The Alcoholic Beverage segment held the largest market revenue share in 2025 driven by the strong presence of beverage manufacturers and increasing consumer preference for premium glass bottles for spirits, wine, and specialty drinks. Glass packaging remains highly preferred in this segment due to its premium appearance, recyclability, and ability to maintain product integrity.

The Pharmaceutical segment is expected to witness the fastest growth rate from 2026 to 2033, driven by expanding healthcare infrastructure, rising pharmaceutical production, and increasing demand for secure and chemically stable packaging solutions. Glass packaging is gaining substantial importance in pharmaceutical applications because it ensures product safety, sterility, and long-term preservation.

Middle East and Africa Glass Packaging Market Regional Analysis

- South Africa glass packaging market accounted for the largest revenue share in Africa in 2025, attributed to its well-established beverage industry, strong presence of wineries and breweries, and growing pharmaceutical manufacturing base

- The country’s mature retail sector and rising demand for premium packaging formats are further supporting market growth

- In addition, increasing recycling initiatives and sustainability regulations are strengthening the adoption of glass packaging across multiple end-use industries

U.A.E. Glass Packaging Market Insight

The U.A.E. glass packaging market is expected to witness the fastest growth rate from 2026 to 2033, driven by the country’s strong retail sector, high consumption of imported food and beverages, and rapid expansion of luxury hospitality services. The U.A.E.’s focus on sustainability and circular economy initiatives is further accelerating the shift toward recyclable glass packaging. In addition, the presence of multinational food and beverage brands is supporting consistent demand for high-quality glass containers.

Middle East and Africa Glass Packaging Market Share

The Middle East and Africa glass packaging industry is primarily led by well-established companies, including:

• Saudi Glass Company (Saudi Arabia)

• Middle East Glass Manufacturing Company (Egypt)

• AGI Glasspack (Egypt)

• Nampak Glass (South Africa)

• Consol Glass (South Africa)

• Emirates Glass LLC (U.A.E.)

• Oman Glass Company (Oman)

• Qatar Glass Industries (Qatar)

• Arab Union Glass Company (Egypt)

• Jordan Glass Industries Company (Jordan)

• Syrian Glass Company (Syria)

• Tunisian Glass Industries Company (Tunisia)

• Moroccan Glass Container Company (Morocco)

• Bahrain Glass Manufacturing Company (Bahrain)

• Sudan Glass Works Company (Sudan)

Latest Developments in Middle East and Africa Glass Packaging Market

• In May 2021, Consol Glass launched a multi-faceted campaign under its “I Changed 2050” initiative aimed at reducing ocean pollution and promoting a shift from single-use to reusable packaging. The development focused on increasing environmental awareness and encouraging sustainable consumer behaviour. This initiative is expected to strengthen brand positioning in eco-friendly packaging and accelerate demand for recyclable glass solutions in the region, positively impacting the overall sustainability-driven growth of the glass packaging market

• In August 2021, Castle Lager introduced Castle Double Malt, a premium double malt lager available in a 410 ml pearl, green, and gold can as well as a 340 ml green bottle. The development marked an expansion in premium beverage offerings within South Africa. It is expected to enhance demand for high-quality glass and metal packaging formats while supporting growth in the premium alcoholic beverage segment of the Middle East and Africa glass packaging market

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Middle East And Africa Glass Packaging Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Middle East And Africa Glass Packaging Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Middle East And Africa Glass Packaging Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.