Middle East And Africa Healthcare It Integration Market

Market Size in USD Million

CAGR :

%

USD

128.86 Million

USD

290.60 Million

2025

2033

USD

128.86 Million

USD

290.60 Million

2025

2033

| 2026 –2033 | |

| USD 128.86 Million | |

| USD 290.60 Million | |

| % | |

|

Middle East and Africa Healthcare Information Technology (IT) Integration Market Size

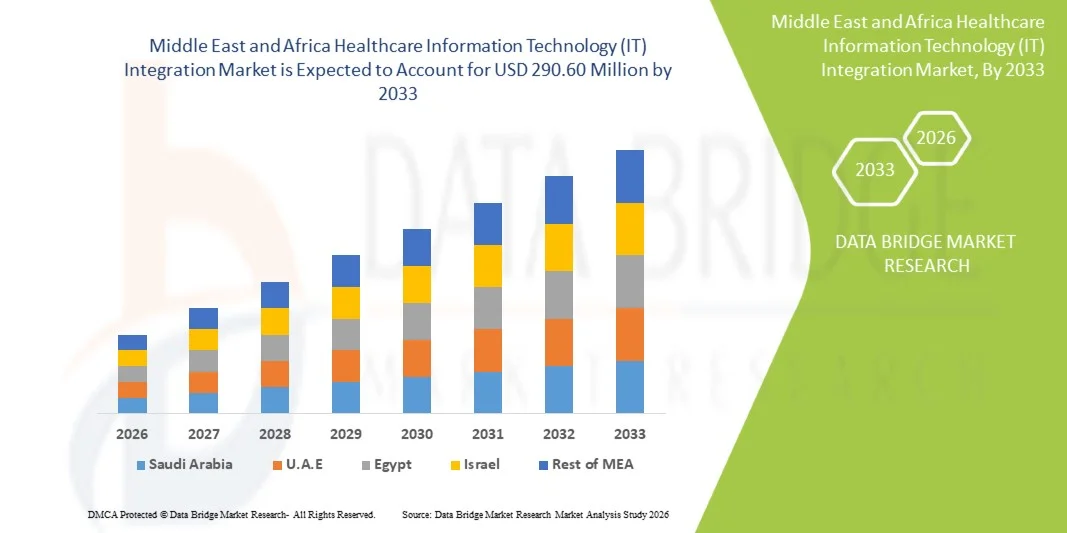

- The Middle East and Africa Healthcare Information Technology (IT) Integration Market size was valued at USD 128.86 Million in 2025 and is expected to reach USD 290.60 Million by 2033, at a CAGR of 10.70% during the forecast period

- The market growth is largely fueled by the increasing adoption of digital healthcare systems, rapid technological progress in cloud computing, AI, and connected medical devices, leading to greater digitalization across hospitals, clinics, laboratories, and healthcare networks

- Furthermore, rising demand for secure, interoperable, and efficient data management solutions among healthcare providers is establishing Healthcare Information Technology (IT) Integration solutions as a critical component of modern healthcare operations. These converging factors are accelerating the uptake of Healthcare Information Technology (IT) Integration solutions, thereby significantly boosting the industry's growth

Middle East and Africa Healthcare Information Technology (IT) Integration Market Analysis

- Healthcare Information Technology (IT) Integration solutions, including electronic health record interoperability, clinical workflow integration, data exchange platforms, cloud-based healthcare systems, and cybersecurity frameworks, are increasingly vital components of modern healthcare infrastructure due to their ability to enhance efficiency, improve patient outcomes, and streamline healthcare operations

- The escalating demand for Healthcare Information Technology (IT) Integration solutions is primarily fueled by the rapid adoption of digital health technologies, growing need for seamless patient data exchange, rising cybersecurity concerns, and increasing preference for connected and automated healthcare ecosystems

- Saudi Arabia dominated the Middle East and Africa Healthcare Information Technology (IT) Integration Market in Middle East with the largest revenue share of approximately 36.2% in 2025, characterized by rising healthcare digitization initiatives, strong government investments, expanding hospital networks, and increasing adoption of integrated health information systems across public and private healthcare facilities

- U.A.E. is expected to be the fastest-growing market in the Healthcare Information Technology (IT) Integration sector during the forecast period, projected to register a CAGR of approximately 10.4%, due to increasing smart healthcare investments, rapid adoption of AI-enabled hospital systems, expanding telehealth infrastructure, and growing demand for interoperable healthcare data platforms

- The individual segment dominated the market with 61.2% revenue share in 2025, driven by customized procurement preferences among hospitals and diagnostic chains

Report Scope and Middle East and Africa Healthcare Information Technology (IT) Integration Market Segmentation

|

Attributes |

Healthcare Information Technology (IT) Integration Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Middle East and Africa

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Middle East and Africa Healthcare Information Technology (IT) Integration Market Trends

“Accelerating Digital Transformation and Interoperable Healthcare Ecosystems”

- A significant and accelerating trend in the Middle East and Africa Healthcare Information Technology (IT) Integration Market is the rapid digital transformation of hospitals, clinics, laboratories, and public health systems. Governments and private healthcare providers are increasingly investing in integrated digital platforms to improve care coordination, operational efficiency, and patient outcomes

- For instance, healthcare organizations across the United Arab Emirates, Saudi Arabia, South Africa, and other regional markets are deploying integrated electronic health records (EHR), hospital information systems (HIS), laboratory information systems (LIS), and radiology information systems (RIS) to enable seamless data exchange between departments and care facilities. These implementations are strengthening demand for IT integration services

- Growing adoption of cloud computing, telehealth platforms, remote patient monitoring, and mobile health applications is further increasing the need for interoperable systems that can securely connect multiple data sources in real time. Providers are prioritizing unified patient records and faster clinical decision-making

- Another important trend is the use of analytics and automation tools to optimize scheduling, billing, inventory management, claims processing, and population health management. Integrated IT environments help reduce administrative burden while improving revenue cycle performance

- Public sector modernization programs and national digital health strategies are also reshaping the regional landscape, particularly in Gulf Cooperation Council countries, where smart healthcare infrastructure is a strategic priority

- Demand for scalable, secure, and interoperable healthcare IT integration solutions is rising steadily across the Middle East and Africa as healthcare systems seek modernization and better patient-centric care delivery

Middle East and Africa Healthcare Information Technology (IT) Integration Market Dynamics

Driver

“Growing Need Due to Rising Healthcare Digitization and Expanding Patient Volumes”

- Increasing patient volumes, growing chronic disease burdens, and the need for efficient healthcare delivery are major drivers for the Middle East and Africa Healthcare Information Technology (IT) Integration Market. Providers are adopting connected systems to manage rising clinical and administrative complexity

- For instance, Saudi Arabia’s healthcare transformation initiatives under Vision 2030, the UAE’s smart hospital programs, and South Africa’s investments in digital patient management systems are accelerating demand for healthcare IT integration solutions. Such initiatives are expected to support market growth during the forecast period

- As hospitals expand specialty services and multisite networks, integrated systems become essential for centralized scheduling, diagnostics sharing, billing accuracy, and continuity of care across locations

- Increasing adoption of telemedicine and hybrid care models is also creating demand for systems that connect physicians, pharmacies, laboratories, insurers, and patients through a unified digital ecosystem

- Furthermore, the need for regulatory compliance, accurate reporting, and real-time clinical data access is encouraging healthcare institutions to replace fragmented legacy software with integrated modern platforms

Restraint/Challenge

“High Implementation Costs, Cybersecurity Risks, and Legacy System Complexity”

- High upfront costs associated with software deployment, system customization, hardware upgrades, and staff training remain a significant challenge, particularly for smaller hospitals and budget-constrained healthcare facilities in developing markets

- For instance, many mid-sized hospitals across Africa may face delays in adopting enterprise EHR or integrated hospital management systems due to limited IT budgets and infrastructure constraints. Cost sensitivity can slow modernization projects

- Cybersecurity and data privacy concerns are another major restraint, as healthcare organizations handle sensitive patient information and increasingly face ransomware attacks, phishing threats, and unauthorized access risks

- Integration with outdated legacy systems can also be technically complex, leading to workflow disruption, interoperability gaps, and extended implementation timelines

- Shortages of skilled health informatics professionals, IT engineers, and system integration experts in certain countries may further hinder successful deployment and long-term optimization

- Overcoming these challenges through stronger cybersecurity frameworks, affordable cloud-based models, workforce training, and phased modernization strategies will be vital for sustained market growth in the Middle East and Africa

Middle East and Africa Healthcare Information Technology (IT) Integration Market Scope

The market is segmented on the basis of product & services, application, facility size, purchase mode, and end user.

• By Product & Services

On the basis of product & services, the Middle East and Africa Healthcare Information Technology (IT) Integration Market is segmented into product and services. The services segment dominated the largest market revenue share of 58.7% in 2025, driven by rising demand for consulting, implementation, maintenance, and managed integration solutions across healthcare systems. Hospitals and clinics increasingly rely on third-party vendors for seamless interoperability between legacy and modern IT systems. Growing adoption of cloud migration and cybersecurity services further supports segment leadership. Service providers help reduce downtime and improve workflow efficiency. Continuous software upgrades and regulatory compliance requirements sustain recurring service demand. Expansion of telehealth and remote care platforms increases integration complexity, boosting outsourced service adoption. Healthcare organizations prefer expert-led deployment to minimize operational disruptions. Large hospital networks also require ongoing support for multi-site integration. Demand for analytics configuration and training services contributes strongly to revenue growth. Increasing digitization of patient records worldwide reinforces service dominance.

The product segment is expected to witness the fastest CAGR of 14.2% from 2026 to 2033, driven by rising investments in middleware, interoperability platforms, interface engines, and data exchange software. Providers increasingly seek scalable in-house tools for long-term cost efficiency. Growing use of AI-enabled integration platforms supports adoption. Demand for real-time data synchronization solutions is accelerating. Product innovation in API management and cloud-native architecture drives growth. Hospitals are modernizing outdated systems with advanced software suites. Increased government support for health data exchange infrastructure further boosts uptake. Vendors are launching modular platforms suitable for small and mid-sized facilities. Enhanced security and automation features attract healthcare buyers. Expansion of subscription-based SaaS integration products also supports rapid growth.

• By Application

On the basis of application, the Middle East and Africa Healthcare Information Technology (IT) Integration Market is segmented into medical device integration, internal integration, hospital integration, lab integration, clinics integration, and radiology integration. The hospital integration segment accounted for the largest market revenue share of 31.4% in 2025, driven by the need to connect EHRs, billing systems, pharmacy systems, and patient monitoring tools within hospitals. Large healthcare facilities manage vast patient data volumes requiring unified workflows. Integration improves clinical decision-making and administrative efficiency. Rising patient admissions and multispecialty operations increase demand. Hospitals are heavily investing in smart infrastructure and automation. Regulatory pressure for accurate records further supports adoption. Need for coordinated care across departments boosts segment growth. Expansion of digital inpatient management systems adds momentum. Increasing use of connected medical devices strengthens hospital integration demand.

The medical device integration segment is projected to witness the fastest CAGR of 15.1% from 2026 to 2033, fueled by increasing use of IoT-enabled devices, bedside monitors, infusion pumps, and wearable diagnostics. Healthcare providers seek real-time data flow from devices into EHR systems. Automation reduces manual entry errors and enhances patient safety. Demand for ICU and emergency care connectivity solutions is increasing. Smart hospitals are prioritizing connected ecosystems. Growth in remote monitoring programs supports adoption. Vendors are developing standardized device communication protocols. AI-driven alert systems also rely on integrated device data. Rising chronic disease management needs further accelerate segment expansion.

• By Facility Size

On the basis of facility size, the Middle East and Africa Healthcare Information Technology (IT) Integration Market is segmented into large, medium, and small. The large segment held the largest market revenue share of 49.8% in 2025, driven by high IT budgets, extensive patient networks, and complex multi-department infrastructure. Large hospitals require advanced interoperability across numerous systems and locations. They are early adopters of cloud and AI technologies. Strong regulatory compliance spending supports investments. These facilities prioritize centralized data visibility and operational efficiency. Large enterprises often undertake full-scale digital transformation projects. Demand for enterprise-grade cybersecurity integration boosts revenue. Expansion of hospital chains globally supports dominance. Strategic partnerships with IT vendors further strengthen adoption.

The medium segment is expected to witness the fastest CAGR of 13.8% from 2026 to 2033, supported by increasing modernization of regional hospitals and multispecialty centers. Medium facilities are rapidly replacing paper-based and siloed systems. Affordable SaaS solutions make integration accessible. Rising competition encourages digital patient experience upgrades. Government funding programs support IT adoption in mid-sized facilities. Need for efficient referrals and diagnostics connectivity drives demand. Vendors are offering customized packages for this segment. Growing outpatient volumes further accelerate adoption. Medium facilities represent a large untapped customer base globally.

• By Purchase Mode

On the basis of purchase mode, the Middle East and Africa Healthcare Information Technology (IT) Integration Market is segmented into group purchase organization and individual. The individual segment dominated the market with 61.2% revenue share in 2025, driven by customized procurement preferences among hospitals and diagnostic chains. Direct purchases allow tailored vendor selection and flexible deployment models. Institutions often negotiate specific service-level agreements independently. Need for specialized integration tools boosts direct contracts. Faster implementation timelines also favor individual buying. Large organizations prefer direct strategic partnerships with software providers. Customized cybersecurity and analytics modules support growth. Rising digital transformation budgets contribute to segment leadership.

The group purchase organization segment is anticipated to grow at the fastest CAGR of 12.9% from 2026 to 2033, due to cost savings and bulk procurement advantages. Smaller hospitals increasingly use collective purchasing models. GPOs help standardize technology sourcing and reduce vendor risks. Budget constraints encourage collaborative buying. Expansion of regional healthcare alliances supports demand. Vendors are offering bundled service packages through GPO channels. Growing awareness of procurement efficiency further drives adoption. Need for economical modernization solutions accelerates growth globally.

• By End User

On the basis of end user, the Middle East and Africa Healthcare Information Technology (IT) Integration Market is segmented into hospitals, laboratory, diagnostic centers, radiology centers, and clinics. The hospitals segment accounted for the largest market revenue share of 46.9% in 2025, driven by high patient volumes and broad reliance on interconnected clinical and administrative systems. Hospitals require integration across departments such as pharmacy, imaging, labs, and billing. Increasing digitization of inpatient and outpatient services supports demand. Need for accurate care coordination boosts investment. Smart hospital initiatives strengthen market leadership. Rising mergers among hospital networks create integration opportunities. Hospitals remain primary adopters of enterprise IT platforms worldwide.

The diagnostic centers segment is projected to witness the fastest CAGR of 14.6% from 2026 to 2033, fueled by rising demand for connected testing workflows, digital reporting, and faster physician communication. Growth in preventive healthcare screening supports expansion. Diagnostic centers increasingly integrate LIS, RIS, and billing platforms. Need for rapid result sharing drives software adoption. Expansion of independent testing chains contributes strongly. Cloud-based solutions are particularly attractive in this segment. Rising demand for decentralized diagnostics further accelerates growth.

Middle East and Africa Healthcare Information Technology (IT) Integration Market Regional Analysis

- The Middle East Middle East and Africa Healthcare Information Technology (IT) Integration Market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by accelerating healthcare digitization, rising investments in smart hospitals, and increasing demand for interoperable clinical and administrative systems across the region

- Governments are prioritizing digital health transformation through national healthcare modernization strategies, electronic health record (EHR) deployment, and connected care infrastructure

- The growing need for efficient data exchange, improved patient outcomes, and streamlined hospital workflows is further supporting the adoption of healthcare IT integration solutions across public and private healthcare facilities

Saudi Arabia Middle East and Africa Healthcare Information Technology (IT) Integration Market Insight

Saudi Arabia Middle East and Africa Healthcare Information Technology (IT) Integration Market dominated the Middle East and Africa Healthcare Information Technology (IT) Integration Market in the Middle East with the largest revenue share of approximately 36.2% in 2025, characterized by rising healthcare digitization initiatives, strong government investments, expanding hospital networks, and increasing adoption of integrated health information systems across public and private healthcare facilities. The country’s healthcare transformation programs, along with rising investments in cloud-based hospital management systems and connected diagnostics platforms, are accelerating market growth. In addition, increasing focus on patient data management, cybersecurity, and operational efficiency is strengthening demand for advanced IT integration services.

U.A.E. Middle East and Africa Healthcare Information Technology (IT) Integration Market Insight

The U.A.E. Middle East and Africa Healthcare Information Technology (IT) Integration Market is expected to be the fastest-growing market in the Healthcare Information Technology (IT) Integration sector during the forecast period, projected to register a CAGR of approximately 10.4%, due to increasing smart healthcare investments, rapid adoption of AI-enabled hospital systems, expanding telehealth infrastructure, and growing demand for interoperable healthcare data platforms. The country’s position as a regional healthcare innovation hub, coupled with strong private sector participation, is encouraging deployment of next-generation digital health solutions. Furthermore, increasing use of predictive analytics, remote monitoring systems, and integrated patient engagement platforms is expected to accelerate future market expansion.

Middle East and Africa Healthcare Information Technology (IT) Integration Market Share

The Healthcare Information Technology (IT) Integration industry is primarily led by well-established companies, including:

- Oracle Health (U.S.)

- Epic Systems Corporation (U.S.)

- GE HealthCare Technologies Inc. (U.S.)

- Siemens Healthineers AG (Germany)

- Philips Healthcare (Netherlands)

- IBM Corporation (U.S.)

- Microsoft Corporation (U.S.)

- Cisco Systems, Inc. (U.S.)

- InterSystems Corporation (U.S.)

- Allscripts Healthcare Solutions, Inc. (U.S.)

- athenahealth, Inc. (U.S.)

- NextGen Healthcare, Inc. (U.S.)

- eClinicalWorks LLC (U.S.)

- Fujitsu Limited (Japan)

- Tata Consultancy Services Ltd. (India)

- Wipro Limited (India)

- Infosys Limited (India)

- Accenture plc (Ireland)

- Cognizant Technology Solutions Corporation (U.S.)

Latest Developments in Middle East and Africa Healthcare Information Technology (IT) Integration Market

- In April 2021, Microsoft Corporation completed its acquisition of Nuance Communications in a deal valued at approximately USD 19.7 billion, significantly expanding Microsoft’s healthcare cloud and AI capabilities. The acquisition strengthened healthcare IT integration through ambient clinical intelligence, speech recognition, and EHR workflow connectivity across provider systems

- In September 2021, Lyniate, a healthcare interoperability solutions provider, launched Lyniate Rapid, an API gateway and management platform designed to help healthcare organizations build and secure FHIR-based APIs. The launch supported growing demand for standardized data exchange and modern healthcare integration architecture

- In December 2021, Oracle Corporation announced its agreement to acquire Cerner Corporation for approximately USD 28.3 billion. The transaction marked one of the largest healthcare IT deals in history and significantly strengthened Oracle’s position in EHR systems, healthcare data integration, and cloud-based hospital IT infrastructure

- In June 2022, Oracle Corporation completed the acquisition of Cerner, later rebranding the business as Oracle Health. The acquisition accelerated integration of Cerner’s EHR platforms with Oracle Cloud Infrastructure, supporting next-generation connected healthcare ecosystems and large-scale interoperability modernization

- In January 2023, Oracle Health announced new cloud-enabled healthcare platform initiatives focused on unifying clinical, financial, and operational data across provider networks. These developments strengthened enterprise-wide IT integration for hospitals and health systems transitioning from legacy on-premise environments

- In March 2024, Oracle NetSuite launched SuiteSuccess Healthcare Edition, a cloud ERP solution tailored for healthcare organizations. The platform was designed to improve operational efficiency, compliance, finance integration, and connected decision-making across healthcare enterprises

- In March 2025, InterSystems launched IntelliCare, an AI-powered electronic health record and healthcare information system designed to improve interactions among clinicians, administrators, and patients. The launch reinforced demand for integrated AI-enabled clinical data systems in the healthcare IT market

- In April 2025, GE HealthCare unveiled an AI-driven smart operating room integration suite at Arab Health 2025, enabling connectivity between imaging systems, hospital information systems, and surgical workflows. The development highlighted rising investment in real-time clinical systems integration

- In July 2025, healthcare IT vendors accelerated adoption of FHIR-based APIs, cloud data lakes, and AI-assisted interoperability tools to comply with evolving payer-provider data sharing requirements and improve prior authorization workflows. This trend continued to drive expansion of the global healthcare IT integration market

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.