Middle East And Africa Medical Display Market

Market Size in USD Million

CAGR :

%

USD

35.04 Million

USD

48.32 Million

2025

2033

USD

35.04 Million

USD

48.32 Million

2025

2033

| 2026 –2033 | |

| USD 35.04 Million | |

| USD 48.32 Million | |

| % | |

|

Middle East and Africa Medical Display Market Size

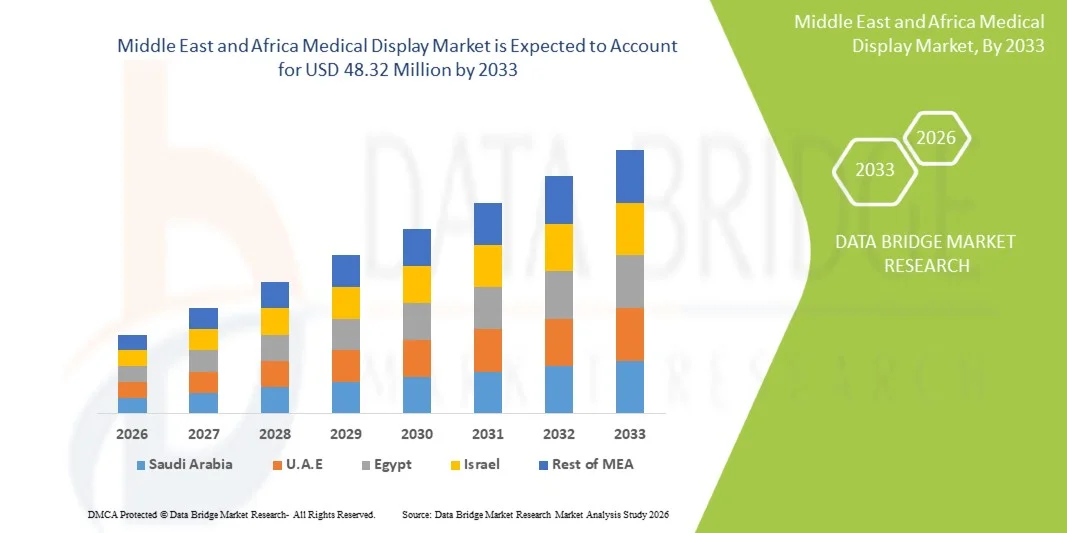

- The Middle East and Africa medical display market size was valued at USD 35.04 million in 2025 and is expected to reach USD 48.32 million by 2033, at a CAGR of 4.1% during the forecast period

- The market growth is largely driven by increasing investments in healthcare infrastructure, rising adoption of advanced diagnostic imaging systems, and the growing digital transformation of hospitals and diagnostic centers across the region, leading to higher demand for high-resolution medical displays

- Furthermore, the rising focus on early disease detection, expansion of telemedicine and digital radiology, and the need for accurate, high-quality imaging in clinical decision-making are accelerating the adoption of medical display solutions, thereby significantly boosting the industry's growth

Middle East and Africa Medical Display Market Analysis

- Medical displays, specialized high-resolution monitors designed for diagnostic imaging and clinical visualization, are increasingly becoming essential in modern healthcare systems across the Middle East and Africa due to their ability to deliver precise image clarity, support digital diagnostics, and enhance workflow efficiency in radiology and surgical applications

- The escalating demand for medical displays is primarily driven by the rapid expansion of healthcare infrastructure, increasing adoption of digital imaging systems such as MRI, CT, and ultrasound, and a growing shift toward paperless, fully digitized hospital environments across the region

- Saudi Arabia dominated the Middle East and Africa medical display market with the largest revenue share of 34.6% in 2025, supported by strong government healthcare investments under national transformation programs, rapid hospital modernization, and widespread deployment of advanced diagnostic imaging technologies in major medical cities and tertiary care centers

- The United Arab Emirates is expected to be the fastest growing country in the Middle East and Africa medical display market during the forecast period due to increasing medical tourism, strong adoption of AI-enabled healthcare systems, and continuous upgrades of hospital IT infrastructure and imaging capabilities

- The Diagnostic segment dominated the Middle East and Africa medical display market with a market share of 46.8% in 2025, driven by strong usage in radiology, high demand for grayscale accuracy, and increasing reliance on high-performance displays for precise clinical interpretation

Report Scope and Middle East and Africa Medical Display Market Segmentation

|

Attributes |

Middle East and Africa Medical Display Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Middle East and Africa

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Middle East and Africa Medical Display Market Trends

“Rising Integration of AI and Advanced Imaging Visualization Systems”

- A significant and accelerating trend in the Middle East and Africa medical display market is the increasing integration of AI-enabled imaging platforms and advanced diagnostic visualization systems with high-resolution medical displays, improving diagnostic accuracy and workflow efficiency across hospitals and imaging centers

- For instance, Barco and Eizo diagnostic displays are increasingly being used with AI-powered radiology software in major UAE and Saudi hospitals, enabling enhanced image interpretation for CT, MRI, and X-ray applications with improved clarity and precision

- AI integration in medical displays enables features such as automated image enhancement, lesion detection support, and intelligent calibration for consistent diagnostic quality, helping radiologists reduce interpretation time and improve clinical decision-making accuracy

- The seamless integration of medical displays with hospital PACS systems and digital health platforms allows centralized access to imaging data, enabling physicians to review, compare, and analyze patient scans across departments in real time for faster diagnosis

- This trend towards more intelligent, high-resolution, and interoperable display systems is fundamentally reshaping clinical imaging workflows, with companies such as Samsung Healthcare and LG developing AI-enhanced diagnostic monitors tailored for hospital environments in the MEA region

- The demand for advanced medical displays with AI-assisted imaging and integrated workflow compatibility is growing rapidly across both public and private healthcare sectors as hospitals increasingly prioritize precision diagnostics and digital transformation

- Additionally, increasing use of 3D and 4K/8K imaging displays in surgical and radiology applications is enhancing visualization quality, supporting minimally invasive procedures and improving overall patient outcomes

Middle East and Africa Medical Display Market Dynamics

Driver

“Growing Need Due to Rising Healthcare Digitalization and Diagnostic Imaging Demand”

- The increasing expansion of healthcare infrastructure, coupled with rapid digitalization of hospital systems, is a significant driver for the rising demand for medical displays across the Middle East and Africa region

- For instance, in March 2025, Saudi Arabia’s Ministry of Health expanded its digital hospital program by deploying advanced imaging systems integrated with high-resolution diagnostic displays to improve radiology and surgical outcomes

- As healthcare providers increasingly adopt digital imaging technologies such as CT, MRI, and ultrasound, medical displays play a critical role in ensuring accurate visualization and improved diagnostic confidence for clinicians

- Furthermore, the growing emphasis on early disease detection and preventive healthcare is encouraging hospitals to upgrade from conventional monitors to medical-grade displays for enhanced image precision and consistency

- The increasing adoption of telemedicine, teleradiology, and cloud-based imaging platforms is further propelling demand for medical displays, enabling remote diagnosis and collaboration between specialists across regions

- The transition toward fully digitized healthcare ecosystems and rising investments in smart hospitals are key factors accelerating the adoption of advanced medical display solutions in both urban and emerging healthcare markets

- Additionally, government-led healthcare modernization initiatives and public-private partnerships are further accelerating the installation of advanced diagnostic imaging infrastructure across major MEA countries

- Moreover, the rising prevalence of chronic diseases such as cancer and cardiovascular disorders is increasing diagnostic imaging volumes, thereby boosting demand for high-performance medical displays

Restraint/Challenge

“High Equipment Costs and Limited Healthcare Infrastructure in Emerging Regions”

- Concerns surrounding the high initial cost of advanced medical display systems and limited healthcare infrastructure in certain parts of Africa pose a significant challenge to broader market penetration across the region

- As medical-grade displays require strict compliance with diagnostic standards and advanced calibration technologies, their procurement and maintenance costs remain relatively high compared to conventional display systems used in general healthcare settings

- For instance, smaller hospitals and diagnostic centers in low-income African regions often rely on basic imaging monitors due to budget constraints, limiting the adoption of high-end diagnostic display solutions

- Addressing these cost-related barriers through affordable product offerings, government healthcare funding programs, and strategic partnerships is crucial for expanding market access and adoption

- Additionally, limited availability of trained radiology professionals and technical expertise in certain regions further restricts the effective utilization of advanced medical display technologies

- Overcoming these challenges through infrastructure development, cost optimization strategies, and enhanced training programs will be vital for sustaining long-term market growth in the Middle East and Africa medical display industry

- Furthermore, inconsistent electricity supply and underdeveloped digital infrastructure in certain rural areas hinder the reliable deployment and operation of advanced medical imaging display systems

- In addition, slow procurement cycles in public healthcare systems can delay the adoption of new medical display technologies, impacting overall market expansion speed

Middle East and Africa Medical Display Market Scope

The market is segmented on the basis of technology, panel size, viewing mode, megapixel, resolution, display type, imaging technology, display color, aspect ratio, component, application, end user, and distribution channel.

- By Technology

On the basis of technology, the market is segmented into LED-Backlit LCD Display, CCFL-Backlit LCD Display, TFT LCD Display, and OLED Display. The LED-Backlit LCD Display segment dominated the market with the largest revenue share of 52.4% in 2025, driven by its superior brightness, energy efficiency, and long operational lifespan, making it highly suitable for continuous diagnostic imaging environments in hospitals and radiology centers. These displays are widely preferred across MEA healthcare facilities due to their consistent image quality and lower maintenance requirements compared to older technologies. Additionally, the ongoing replacement of CCFL systems with LED-based solutions is further strengthening market dominance. Their compatibility with PACS and hospital IT systems also supports widespread adoption in both public and private hospitals. Growing digital transformation initiatives in Gulf countries are further accelerating LED display deployment.

The OLED Display segment is expected to witness the fastest growth rate of 19.8% from 2026 to 2033, driven by its superior contrast ratio, deeper black levels, and enhanced color accuracy essential for advanced diagnostic imaging. OLED technology is increasingly used in high-end diagnostic centers and specialized hospitals for oncology, neurology, and surgical imaging applications. Its ability to deliver precise visualization of subtle tissue differences significantly improves clinical decision-making. Declining production costs and technological advancements are making OLED displays more accessible in the region. Rising investments in premium healthcare infrastructure across Saudi Arabia and the UAE are further boosting adoption.

- By Panel Size

On the basis of panel size, the market is segmented into Under 22.9" Inch Panels, 23.0"–32.0" Inch Panels, 27.0–41.9 Inch Panels, and Above 42 Inch Panels. The 23.0"–32.0" Inch Panels segment dominated the market with a revenue share of 46.1% in 2025, driven by its optimal balance between screen size and diagnostic efficiency, making it the standard for radiology workstations. These panels are widely used in hospitals and diagnostic imaging centers for CT, MRI, and ultrasound interpretation due to their ergonomic design and high compatibility with clinical workflows. They also support multi-modality imaging, which enhances diagnostic productivity. Their cost-effectiveness compared to larger panels further supports their dominance. Continuous upgrades in hospital imaging departments are reinforcing demand for this segment.

The Above 42 Inch Panels segment is expected to witness the fastest growth rate of 18.5% from 2026 to 2033, driven by increasing use in advanced surgical suites and centralized diagnostic command centers. Large displays allow multi-image comparison, real-time surgical visualization, and improved collaboration among medical teams. These systems are increasingly being deployed in smart hospitals and tertiary care centers across the Middle East. Their ability to enhance visualization in complex procedures such as minimally invasive surgeries is a key growth driver. Rising healthcare investments in Gulf countries are further accelerating adoption of large-format displays.

- By Viewing Mode

On the basis of viewing mode, the market is segmented into 2D and 3D. The 2D segment dominated the market with the largest revenue share of 68.7% in 2025, driven by its extensive use in routine diagnostic imaging such as X-rays, CT scans, and ultrasound applications. 2D displays remain the standard across most healthcare facilities in MEA due to their affordability, reliability, and compatibility with existing imaging infrastructure. They are widely deployed in both public hospitals and private diagnostic centers. Their lower processing requirements make them suitable for high-volume diagnostic environments. Continuous demand for conventional imaging ensures sustained dominance of this segment.

The 3D segment is expected to witness the fastest growth rate of 22.3% from 2026 to 2033, driven by increasing adoption in surgical planning, oncology, and orthopedic imaging applications. 3D visualization provides depth perception, which significantly improves diagnostic precision and procedural accuracy. Hospitals in the UAE and Saudi Arabia are increasingly integrating 3D imaging into advanced surgical workflows. AI-powered imaging software is further enhancing 3D display performance. Rising demand for minimally invasive surgeries is also accelerating segment growth.

- By Megapixel

On the basis of megapixel, the market is segmented into Up to 2MP, 2.1–4MP, 4.1–8MP, and Above 8MP. The 2.1–4MP segment dominated the market with a revenue share of 41.9% in 2025, driven by its optimal balance between resolution quality and affordability for routine diagnostic imaging. These displays are widely used in radiology departments for general imaging interpretation across hospitals and diagnostic centers. They provide sufficient clarity for most clinical applications without significantly increasing system costs. Their compatibility with existing hospital infrastructure supports widespread adoption. This segment remains the preferred choice for mid-tier healthcare facilities in the region.

The Above 8MP segment is expected to witness the fastest growth rate of 24.1% from 2026 to 2033, driven by rising demand for ultra-high-resolution imaging in complex diagnostic procedures. These displays are increasingly used in oncology, neurosurgery, and cardiovascular imaging where fine detail visualization is critical. Advanced hospitals are adopting high-megapixel displays to support AI-assisted diagnostics and precision medicine. Their ability to display extremely detailed images improves diagnostic confidence. Continuous technological advancements are reducing costs and expanding adoption across premium healthcare institutions.

- By Resolution

On the basis of resolution, the market is segmented into 4K, Ultra Full HD, Full HD, and Others. The Full HD segment dominated the market with a revenue share of 44.6% in 2025, driven by its widespread availability, cost efficiency, and adequate performance for standard diagnostic imaging applications. Full HD displays are extensively used in hospitals and diagnostic laboratories across MEA for routine radiology workflows. They offer a balance between image quality and affordability, making them suitable for large-scale deployment. Their compatibility with existing imaging systems further supports market leadership. Continuous demand from mid-level healthcare facilities sustains segment dominance.

The 4K segment is expected to witness the fastest growth rate of 23.5% from 2026 to 2033, driven by increasing demand for high-definition imaging in advanced diagnostic and surgical applications. 4K displays provide significantly improved image sharpness, enabling better visualization of fine anatomical structures. They are increasingly being adopted in smart hospitals and specialized imaging centers across Gulf countries. Integration with AI-based diagnostic systems further enhances their clinical value. Rising investments in advanced healthcare infrastructure are accelerating 4K adoption across the region.

- By Display Type

On the basis of display type, the market is segmented into wall mounted, portable, and modular. The Wall Mounted segment dominated the market with the largest revenue share of 49.3% in 2025, driven by its extensive use in radiology rooms, operating theaters, and diagnostic imaging departments where fixed high-performance visualization systems are required. These displays are preferred in hospitals due to their stability, space efficiency, and ability to support continuous high-resolution imaging workflows. They also ensure optimal ergonomic positioning for radiologists, improving diagnostic accuracy and workflow efficiency. Increasing hospital infrastructure development across Saudi Arabia and the UAE is further reinforcing adoption of wall-mounted systems. Their integration with PACS and HIS systems also strengthens their dominance in clinical environments.

The Portable segment is expected to witness the fastest growth rate of 21.4% from 2026 to 2033, driven by increasing demand for mobility in emergency care, bedside diagnostics, and field hospitals. Portable medical displays enable real-time imaging access in critical care settings such as ICUs and ambulances, improving response times and clinical decision-making. Rising adoption of point-of-care diagnostics in remote and underserved regions of Africa is further supporting growth. Technological advancements in lightweight, high-resolution panels are enhancing usability and performance. Additionally, expanding telemedicine and mobile healthcare initiatives are accelerating demand for portable solutions.

- By Imaging Technology

On the basis of imaging technology, the market is segmented into touch screen, scratch resistant front glass, failsafe mode, cleanable options, softglow & spotview, and others. The Scratch Resistant Front Glass segment dominated the market with a revenue share of 37.8% in 2025, driven by its importance in maintaining durability, hygiene, and long-term performance in clinical environments. Medical displays in hospitals and diagnostic labs are frequently exposed to continuous use and cleaning, making scratch-resistant surfaces essential for operational reliability. These displays also ensure consistent image clarity over extended usage periods. Increasing infection control standards in MEA healthcare facilities are further boosting adoption. Their compatibility with sterile environments supports widespread usage in operating rooms and radiology departments.

The Softglow & Spotview segment is expected to witness the fastest growth rate of 23.2% from 2026 to 2033, driven by increasing demand for enhanced visualization techniques that improve diagnostic precision. These technologies help radiologists highlight specific areas of interest without compromising overall image quality, improving detection accuracy for subtle abnormalities. They are increasingly being used in oncology and complex diagnostic imaging workflows. Integration with AI-assisted imaging systems is further enhancing their effectiveness. Rising adoption in advanced hospitals and specialty diagnostic centers across the Gulf region is accelerating segment growth.

- By Display Color

On the basis of display color, the market is segmented into color and monochrome. The Color segment dominated the market with the largest revenue share of 61.5% in 2025, driven by its extensive use in general diagnostic imaging, surgical visualization, and multi-modality imaging applications. Color displays provide enhanced visualization of anatomical structures, making them highly suitable for CT, MRI, and ultrasound interpretation. Hospitals across MEA increasingly prefer color displays due to their versatility and compatibility with modern imaging systems. Their ability to support advanced imaging workflows contributes significantly to clinical efficiency. Continuous upgrades in hospital diagnostic infrastructure are further strengthening dominance of this segment.

The Monochrome segment is expected to witness the fastest growth rate of 18.9% from 2026 to 2033, driven by its critical use in radiology applications requiring high grayscale precision, such as mammography and X-ray interpretation. Monochrome displays offer superior contrast resolution, enabling detection of subtle tissue variations essential for early diagnosis. They are widely used in specialized diagnostic centers and radiology departments. Increasing prevalence of cancer screening programs across MEA countries is further boosting demand. Their cost-effectiveness compared to advanced color systems also supports adoption in mid-tier healthcare facilities.

- By Aspect Ratio

On the basis of aspect ratio, the market is segmented into 16:9, 21:9, and 4:3. The 16:9 segment dominated the market with a revenue share of 54.2% in 2025, driven by its compatibility with most modern imaging software, PACS systems, and diagnostic applications. This widescreen format allows efficient multitasking and side-by-side image comparison, which is essential in radiology workflows. Hospitals across MEA prefer 16:9 displays due to their standardization and ease of integration with existing IT infrastructure. Their versatility across multiple imaging modalities further supports widespread adoption. Continuous modernization of healthcare facilities is reinforcing segment dominance.

The 21:9 segment is expected to witness the fastest growth rate of 20.6% from 2026 to 2033, driven by increasing demand for ultra-wide displays in advanced diagnostic and surgical environments. These displays allow simultaneous viewing of multiple imaging datasets, improving workflow efficiency for radiologists and surgeons. They are increasingly being adopted in smart hospitals and imaging command centers across Gulf countries. Enhanced visualization capabilities support complex procedures and multi-disciplinary collaboration. Rising investments in digital healthcare transformation are accelerating adoption of ultra-wide aspect ratio displays.

- By Component

On the basis of component, the market is segmented into hardware and services. The Hardware segment dominated the market with the largest revenue share of 78.6% in 2025, driven by the strong demand for advanced medical-grade display units, high-resolution panels, calibration systems, and integrated imaging monitors across hospitals and diagnostic centers. Hardware forms the core of medical display systems, as hospitals prioritize high-performance visualization equipment for radiology, surgery, and diagnostic applications. Increasing procurement of advanced display monitors in smart hospitals across Saudi Arabia and the UAE is further strengthening segment dominance. Continuous upgrades from legacy systems to high-resolution digital displays are also fueling demand. The rising installation of PACS-integrated imaging hardware is further supporting market leadership.

The Services segment is expected to witness the fastest growth rate of 22.7% from 2026 to 2033, driven by increasing demand for installation, calibration, maintenance, and software integration services. Hospitals are increasingly relying on specialized service providers to ensure accurate display performance and compliance with diagnostic imaging standards. Growing adoption of AI-enabled imaging systems is also increasing the need for continuous software updates and system optimization. Service contracts are becoming essential for maintaining uptime and image accuracy in critical care environments. Expansion of healthcare IT infrastructure across MEA is further accelerating demand for managed services.

- By Application

On the basis of application, the market is segmented into consultation, diagnostic, surgical/interventional, telehealth, teaching/practice, fetal monitoring, dentistry, point of care, patient-worn monitoring, and others. The Diagnostic segment dominated the market with a revenue share of 46.8% in 2025, driven by the extensive use of medical displays in radiology, pathology, and imaging interpretation workflows. Hospitals and diagnostic centers across MEA rely heavily on high-resolution displays for CT, MRI, and X-ray analysis, ensuring accurate clinical decision-making. Rising burden of chronic diseases such as cancer and cardiovascular disorders is further increasing diagnostic imaging volumes. Expansion of hospital infrastructure and imaging departments is reinforcing segment dominance. Continuous digital transformation in healthcare systems is also supporting widespread adoption.

The Surgical/Interventional segment is expected to witness the fastest growth rate of 24.9% from 2026 to 2033, driven by increasing adoption of image-guided and minimally invasive surgical procedures. Medical displays are increasingly being used in operating rooms to provide real-time visualization during complex surgeries. Growing investments in advanced surgical suites across Gulf countries are further boosting demand. Integration of AI-assisted imaging and 3D visualization is enhancing surgical precision and outcomes. Rising focus on patient safety and procedural accuracy is accelerating adoption of high-performance surgical displays.

- By End User

On the basis of end user, the market is segmented into hospitals, clinics, nursing facilities, diagnostic laboratories, imaging/radiology labs, laboratories, rehabilitation centers, and others. The Hospitals segment dominated the market with the largest revenue share of 58.9% in 2025, driven by high patient volumes, advanced imaging infrastructure, and widespread adoption of digital diagnostic systems. Hospitals are the primary users of medical displays for radiology, surgery, and emergency care applications across MEA. Increasing investments in smart hospitals and healthcare modernization programs in Saudi Arabia and the UAE are further strengthening demand. Hospitals also benefit from integrated PACS systems, requiring high-performance displays for efficient workflows. Continuous expansion of tertiary care centers is further supporting segment dominance.

The Imaging/Radiology Labs segment is expected to witness the fastest growth rate of 23.6% from 2026 to 2033, driven by increasing demand for specialized diagnostic imaging services. These facilities rely heavily on high-resolution displays for accurate interpretation of medical images across multiple modalities. Rising outsourcing of diagnostic services and growth of standalone imaging centers are supporting segment expansion. Increasing prevalence of chronic diseases requiring advanced imaging is further fueling demand. Investments in private diagnostic networks across MEA are accelerating adoption of advanced medical display systems.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into direct tender, retail sales, and others. The Direct Tender segment dominated the market with a revenue share of 63.4% in 2025, driven by large-scale procurement of medical display systems by government hospitals, public healthcare institutions, and large private hospital chains. Direct procurement ensures standardized equipment, bulk pricing advantages, and compliance with healthcare regulations. Government-led healthcare modernization programs across MEA countries are significantly contributing to segment dominance. Long-term supply contracts with manufacturers and system integrators further strengthen this channel. Expansion of national healthcare infrastructure projects is also supporting continued growth.

The Retail Sales segment is expected to witness the fastest growth rate of 21.8% from 2026 to 2033, driven by increasing demand from small clinics, diagnostic centers, and private healthcare practitioners. Retail channels offer flexibility, faster procurement, and wider accessibility for mid-sized healthcare facilities. Growth of private healthcare providers and outpatient diagnostic services is further accelerating demand. E-commerce and specialized medical equipment distributors are expanding access to advanced display systems. Rising adoption of cost-effective medical imaging solutions in emerging MEA markets is also supporting segment growth.

Middle East and Africa Medical Display Market Regional Analysis

- Saudi Arabia dominated the Middle East and Africa medical display market with the largest revenue share of 34.6% in 2025, supported by strong government healthcare investments under national transformation programs, rapid hospital modernization, and widespread deployment of advanced diagnostic imaging technologies in major medical cities and tertiary care centers

- Healthcare providers in the country highly value high-resolution imaging accuracy, interoperability with digital hospital systems, and seamless integration of medical displays with PACS and AI-based diagnostic platforms, enabling faster and more precise clinical decision-making across radiology and surgical applications

- This widespread adoption is further supported by rising healthcare expenditure, increasing deployment of cutting-edge imaging modalities, and strong focus on early disease detection and digital healthcare transformation, establishing Saudi Arabia as the leading hub for advanced medical display adoption in the region

The South Africa Medical Display Market Insight

The South Africa medical display market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by increasing demand for improved diagnostic imaging capabilities and rising healthcare investments in urban medical centers. The growing burden of chronic diseases such as cancer and cardiovascular disorders is boosting the need for advanced radiology solutions. Additionally, the expansion of private healthcare facilities and diagnostic imaging centers is supporting adoption of medical-grade displays. The country’s gradual digital transformation in healthcare, along with increasing awareness of advanced imaging technologies, is further contributing to market growth.

Saudi Arabia Medical Display Market Insight

The Saudi Arabia medical display market is expected to expand at a considerable CAGR during the forecast period, fueled by large-scale healthcare infrastructure development under national transformation initiatives and rising adoption of smart hospital systems. The country places strong emphasis on high-precision diagnostic imaging, leading to widespread deployment of advanced medical displays in radiology, surgery, and telehealth applications. Integration of AI-powered imaging solutions and cloud-based healthcare platforms is further enhancing diagnostic efficiency. Moreover, continuous investments in hospital modernization and specialty care centers are strengthening the demand for high-performance medical display technologies.

Egypt Medical Display Market Insight

The Egypt medical display market is poised to grow at a strong CAGR during the forecast period, driven by expanding healthcare access, increasing government focus on hospital upgrades, and rising demand for advanced diagnostic imaging solutions. The country is witnessing gradual adoption of digital healthcare systems, particularly in major urban hospitals and diagnostic laboratories. Growing prevalence of chronic diseases and increasing need for early diagnosis are further boosting demand for medical displays. Additionally, international partnerships and healthcare development programs are supporting the introduction of modern imaging infrastructure across the country.

Nigeria Medical Display Market Insight

The Nigeria medical display market is gaining momentum due to improving healthcare infrastructure, rising private sector investment, and increasing awareness of advanced diagnostic imaging technologies. The country’s growing population and rising disease burden are driving demand for efficient diagnostic tools in hospitals and imaging centers. Adoption of medical displays is gradually increasing in urban healthcare facilities, supported by expansion of private diagnostic networks. Furthermore, ongoing healthcare modernization efforts and digital transformation initiatives are expected to further stimulate market growth in the coming years.

Middle East and Africa Medical Display Market Share

The Middle East and Africa Medical Display industry is primarily led by well-established companies, including:

- Barco NV (Belgium)

- EIZO Corporation (Japan)

- Siemens Healthineers AG (Germany)

- Koninklijke Philips N.V. (Netherlands)

- LG Electronics Inc. (South Korea)

- Sony Group Corporation (Japan)

- NEC Corporation (Japan)

- Advantech Co., Ltd. (Taiwan)

- BenQ Medical Technology Corp. (Taiwan)

- FSN Medical Technologies (U.S.)

- NDS Surgical Imaging (U.S.)

- Double Black Imaging Inc. (U.S.)

- Totoku Electric Co., Ltd. (Japan)

- Jusha Medical (China)

- Onyx Healthcare Inc. (Taiwan)

- Reshin Medical Display (China)

- Axiomtek Co., Ltd. (Taiwan)

- Panasonic Corporation (Japan)

- KARL STORZ SE & Co. KG (Germany)

- Steris plc (U.K.)

What are the Recent Developments in Middle East and Africa Medical Display Market?

- In January 2025, Philips showcased its advanced healthcare imaging and visualization solutions at Arab Health 2025 in Dubai, including AI-enabled diagnostic systems integrated with high-performance medical displays. The solutions focused on improving imaging precision, workflow efficiency, and real-time clinical decision-making in hospitals across the Middle East. The showcase highlighted cloud-based imaging, advanced visualization tools, and integrated hospital informatics systems

- In January 2025, LG Electronics introduced its latest suite of high-resolution medical display solutions at Arab Health in Dubai, featuring 8MP and 4K surgical monitors designed for advanced diagnostic and surgical imaging. The displays aim to enhance clinical accuracy, reduce radiation exposure, and support orthopedic and radiology applications. The launch strengthens LG’s presence in Middle Eastern healthcare digitalization initiatives

- In March 2024, EIZO Corporation showcased its CuratOR surgical visualization solutions at Arab Health in Dubai, highlighting 4K surgical monitors and integrated OR imaging systems for advanced hospital workflows. The solution focuses on improving real-time surgical visualization and endoscopy support in operating rooms. It reflects increasing adoption of integrated digital operating theaters across Middle Eastern hospitals

- In January 2024, EIZO Corporation exhibited its CuratOR surgical and RadiForce diagnostic display systems at Arab Health in Dubai, showcasing 4K surgical monitors and high-precision radiology displays for operating rooms. These systems were designed to improve surgical visualization, endoscopy imaging, and radiology workflows in advanced hospital environments. The presentation highlighted increasing demand for integrated OR visualization systems in MEA healthcare facilities

- In January 2023, Barco showcased its advanced diagnostic and surgical display systems at Arab Health in Dubai, emphasizing high-precision imaging solutions for radiology, mammography, pathology, and operating rooms. The company highlighted its next-generation display technologies designed to improve diagnostic accuracy and clinical efficiency in hospitals across the Middle East

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.