Middle East And Africa Orthopedic Surgical Energy Devices Market

Market Size in USD Million

CAGR :

%

USD

32.64 Million

USD

50.85 Million

2025

2033

USD

32.64 Million

USD

50.85 Million

2025

2033

| 2026 –2033 | |

| USD 32.64 Million | |

| USD 50.85 Million | |

| % | |

|

Middle East and Africa Orthopedic Surgical Energy Devices Market Overview

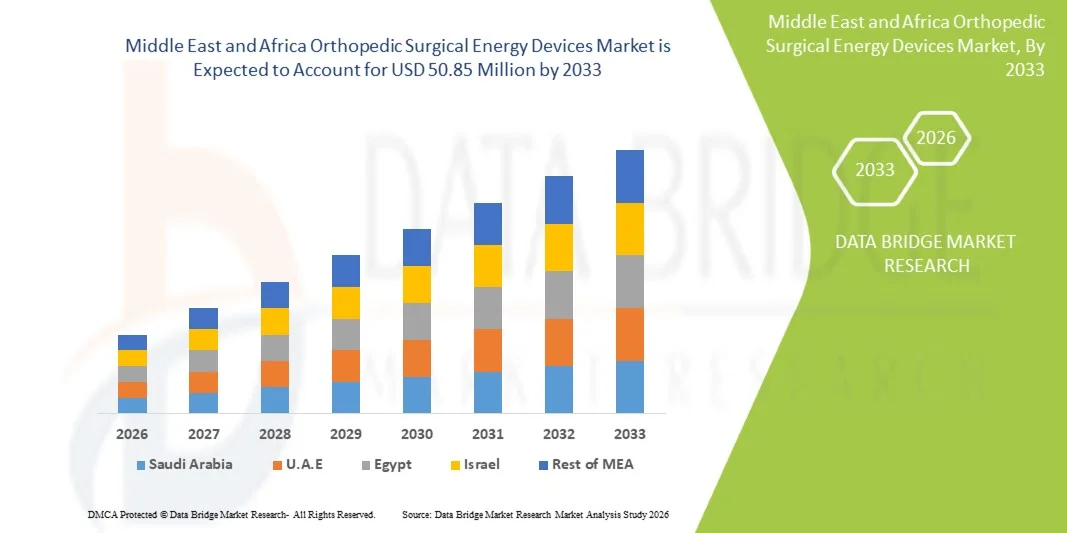

The Middle East and Africa orthopedic surgical energy devices market was valued at USD 32.64 million in 2025 and is projected to reach USD 50.85 million by 2033, growing at a CAGR of 5.70% from 2026 to 2033. The market is witnessing steady expansion driven by increasing prevalence of musculoskeletal disorders, rising geriatric population, and growing adoption of minimally invasive orthopedic procedures across major healthcare systems in the region.

The market growth is further supported by improving healthcare infrastructure, expanding medical tourism in countries such as the UAE and Saudi Arabia, and rising investments in advanced surgical technologies by both public and private hospitals. The increasing burden of sports injuries, road accidents, and osteoarthritis is accelerating demand for precision-based surgical energy devices, including radiofrequency, ultrasound, and electrosurgical systems, as surgeons shift toward safer, faster, and more efficient orthopedic interventions.

Key Market Trends & Insights

- Saudi Arabia dominated the Middle East and Africa orthopedic surgical energy devices market with the largest revenue share of 33.12% in 2025, supported by advanced hospital infrastructure, strong government healthcare investments, and increasing adoption of minimally invasive orthopedic procedures.

- The Handpieces segment led the market with a 42.56% share in 2025, driven by cost-effectiveness, ease of use in surgical settings, and widespread application in complex orthopedic procedures.

- United Arab Emirates is expected to be the fastest-growing country at a CAGR of 6.9% from 2026 to 2033, fueled by rising healthcare modernization initiatives, expansion of tertiary care hospitals, and growing medical tourism inflows.

- Knee is the fastest-growing segment, projected to register a CAGR of 6.9%, driven by increasing sports injuries, obesity-related joint disorders, and rising demand for arthroscopic knee surgeries

- The Hip segment dominates the application category with a 46.18% revenue share in 2025, supported by rising osteoarthritis cases, aging population, and growing demand for hip replacement surgeries.

- The Radiation segment accounts for 48.7% of the market in 2025, driven by its established clinical reliability in orthopedic procedures, enabling precise tissue cutting, effective energy delivery, and widespread adoption across advanced surgical centers.

- Ultrasound segment is the fastest-growing technology category, with a CAGR of 6.8% from 2026 to 2033, supported by improved surgical precision, reduced tissue damage, and growing adoption in minimally invasive orthopedic procedures.

Market Size & Forecast

- Global Market Value (2025): USD 32.64 Million

- Expected Market Value (2033): USD 50.85 Million

- Forecast CAGR (2026–2033): 5.70%

- Leading Country in 2025: Saudi Arabia

- Fastest Growing Country: United Arab Emirates

Report Scope and Middle East and Africa Orthopedic Surgical Energy Devices Market Segmentation

|

Attributes |

Middle East and Africa Orthopedic Surgical Energy Devices Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa |

|

Key Market Players |

· Stryker (U.S.) · Medtronic (Ireland) · Johnson & Johnson Services, Inc. (U.S.) · Smith & Nephew (U.K.) · Olympus Corporation (Japan) · B. Braun SE (Germany) · CONMED Corporation (U.S.) · Zimmer Biomet. (U.S.) · Boston Scientific Corporation (U.S.) · Karl Storz SE & Co. KG (Germany) · Erbe Elektromedizin GmbH (Germany) · KLS Martin Group (Germany) · Aesculap AG (Germany) · Applied Medical Resources Corporation (U.S.) · Integra LifeSciences Holdings Corporation (U.S.) · Richard Wolf GmbH (Germany) · Apyx Medical Corporation (U.S.) · BOWA-electronic GmbH & Co. KG (Germany) · Misonix, Inc. (Bioventus Inc.) (U.S.) · De Soutter Medical (U.K.) |

|

Market Opportunities |

· Rising demand for minimally invasive orthopedic procedures · Increasing adoption of hybrid energy platforms combining radiofrequency and ultrasound technologies · Expansion of ambulatory surgical centers (ASCs) is driving demand for compact, cost-efficient orthopedic surgical energy devices |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Middle East and Africa Orthopedic Surgical Energy Devices Market Trends

Trend: Growth in Minimally Invasive Orthopedic Surgeries

Hospitals and orthopedic centers across the Middle East and Africa are increasingly adopting minimally invasive surgical techniques using advanced energy devices to improve precision, reduce operative trauma, and shorten patient recovery times. The integration of radiofrequency, ultrasonic, and electrosurgical technologies enables surgeons to perform complex bone and soft tissue procedures with greater accuracy. Training institutions and specialized hospitals are also leveraging advanced surgical energy platforms to standardize procedures and improve surgical outcomes across orthopedic applications such as hip and spine surgeries.

Middle East and Africa Orthopedic Surgical Energy Devices Market Dynamics

Key Market Driver: Rising Burden of Musculoskeletal Disorders and Trauma Cases

The growing prevalence of osteoarthritis, osteoporosis, sports injuries, and road traffic accidents is significantly increasing the demand for orthopedic surgical interventions across the region. Hospitals are increasingly deploying advanced energy devices to support high surgical volumes and improve procedural efficiency. Government investments in healthcare infrastructure, particularly in Saudi Arabia, the United Arab Emirates, and South Africa, are further strengthening adoption by enabling access to modern operating rooms and advanced surgical technologies.

Key Restraint/Challenge: High Cost of Advanced Surgical Energy Systems

A major restraint in the Middle East and Africa orthopedic surgical energy devices market is the high acquisition and maintenance cost of advanced surgical energy systems. These technologies require significant capital investment, continuous consumable usage, and skilled surgical training, making adoption challenging for smaller hospitals and public healthcare facilities in low- and middle-income countries. Limited reimbursement frameworks in certain African nations further restrict widespread penetration of premium surgical energy platforms.

For instance, many public hospitals in countries such as Kenya, Nigeria, and Ethiopia continue to depend on conventional electrosurgical units and basic orthopedic tools due to procurement delays, limited capital funding, and lack of specialized training infrastructure. Even in relatively developed healthcare systems within the region, some secondary care facilities face challenges in upgrading to advanced energy platforms due to budget prioritization toward essential medical services.

Key Market Opportunity: Expansion of Advanced Surgical Infrastructure and Medical Training Programs

The increasing development of specialized orthopedic centers, expansion of private hospital networks, and rising medical tourism in Gulf countries are creating strong growth opportunities for surgical energy device manufacturers. Substantial investments in surgeon training programs, simulation-based education, and international collaborations are improving skill availability and accelerating technology adoption. Furthermore, the integration of digital surgical planning tools, AI-assisted orthopedic navigation systems, and connected operating room technologies is enhancing procedural precision and efficiency. These advancements are expected to expand market penetration across both high-income Gulf nations and emerging African healthcare markets, where demand for advanced orthopedic care continues to rise.

Middle East and Africa Orthopedic Surgical Energy Devices Market Scope

The Middle East and Africa Orthopedic Surgical Energy Devices market is segmented on the basis of product, technology, application, end user, and distribution channel

- By Product

On the basis of product, the Middle East and Africa orthopedic surgical energy devices market is segmented into handpieces and accessories. The Handpieces segment dominated the market with a 42.56% share in 2025, owing to its critical role in delivering precise energy for cutting, coagulation, and tissue dissection during orthopedic procedures. These devices are widely used across hip, knee, and spine surgeries due to their reliability, ergonomic design, and compatibility with multiple energy platforms. Increasing surgical volumes in tertiary care hospitals and growing preference for minimally invasive techniques further strengthen the dominance of this segment. Handpieces also benefit from frequent utilization across multiple procedures, making them a core component in hospital procurement strategies.

The Accessories segment is expected to register the fastest growth at a CAGR of 6.7% from 2026 to 2033, driven by rising procedural volumes and increasing demand for disposable and single-use components. Accessories such as probes, tips, and connectors are essential for ensuring precision, sterility, and operational efficiency in orthopedic surgeries. Growing concerns regarding infection control and hospital-acquired infections are accelerating the shift toward disposable accessory adoption. In addition, expanding hospital infrastructure and increasing installation of advanced energy systems are further boosting recurring demand for compatible accessory products.

- By Technology

On the basis of technology, the market is segmented into radiation, radiofrequency, ultrasound, microwave, and others. The Radiation segment dominated the market with a 48.7% share in 2025, supported by its widespread clinical adoption in orthopedic procedures requiring high precision and controlled energy delivery. Radiation-based systems are extensively used in advanced hospital settings for complex surgeries due to their ability to enhance surgical accuracy and reduce intraoperative complications. Established infrastructure in major Gulf hospitals and high surgeon familiarity with radiation-assisted techniques further reinforce its leading position.

The Ultrasound segment is expected to witness the fastest growth at a CAGR of 6.8% from 2026 to 2033, driven by its ability to provide high-precision cutting with minimal thermal damage to surrounding tissues. Surgeons increasingly prefer ultrasound-based systems for minimally invasive orthopedic procedures, particularly in joint and soft tissue surgeries. Advancements in ultrasonic device design and improved procedural outcomes are accelerating adoption across both public and private healthcare facilities. Rising focus on faster recovery times and reduced postoperative complications is further strengthening segment growth.

- By Application

On the basis of application, the market is segmented into hip and knee procedures. The Hip segment dominated the market with a 54.3% revenue share in 2025, driven by the high prevalence of osteoarthritis, aging population, and increasing demand for hip replacement surgeries across major hospitals. Hip procedures often require advanced energy devices for precise bone cutting and tissue management, making them a major contributor to device utilization. Growth in orthopedic specialty centers and rising surgical awareness among patients further support this dominance.

The Knee segment is expected to register the fastest growth at a CAGR of 6.9% from 2026 to 2033, driven by increasing sports injuries, obesity-related joint disorders, and rising demand for arthroscopic knee surgeries. Improvements in minimally invasive surgical techniques are enabling faster recovery and reduced hospital stays, encouraging wider adoption of energy-based devices in knee procedures. Expanding access to orthopedic care in emerging African markets is also contributing to rapid growth in this segment.

- By End User

On the basis of end user, the market is segmented into hospitals & clinics, ambulatory surgical centers (ASCs), and others. The Hospital & Clinics segment dominated the market with a 62.85% share in 2025, supported by high patient inflow, availability of advanced surgical infrastructure, and presence of skilled orthopedic surgeons. Hospitals remain the primary centers for complex orthopedic surgeries requiring advanced energy systems, particularly in urban healthcare hubs across the region. Government investments in public healthcare systems further reinforce hospital dominance.

The Ambulatory Surgical Centers (ASCs) segment is expected to grow at the fastest rate with a CAGR of 6.6% from 2026 to 2033, driven by increasing preference for outpatient surgeries, cost efficiency, and shorter patient recovery times. ASCs are increasingly adopting compact and efficient surgical energy devices to perform minimally invasive orthopedic procedures. Rising healthcare privatization and expansion of day-care surgical facilities in Gulf countries are further accelerating segment growth.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into direct tender and third-party distributors. The Direct Tender segment dominated the market with a 58.4% share in 2025, driven by large-scale procurement by government hospitals and major private healthcare systems. Direct purchasing allows institutions to secure advanced surgical energy systems at negotiated pricing while ensuring standardized equipment across hospital networks. Strong government involvement in healthcare procurement, particularly in GCC countries, further strengthens this segment.

The Third-Party Distributors segment is expected to witness the fastest growth at a CAGR of 6.5% from 2026 to 2033, supported by expanding healthcare infrastructure in emerging African markets and increasing reliance on local distribution networks. Distributors play a critical role in providing equipment access, maintenance support, and technical services in regions with limited direct manufacturer presence. Growing demand for aftermarket services and rapid expansion of private healthcare providers are further driving this segment’s growth.

Middle East and Africa Orthopedic Surgical Energy Devices Market Regional Analysis

Saudi Arabia dominated the Middle East and Africa orthopedic surgical energy devices market with the largest revenue share of 33.12% in 2025, supported by advanced hospital infrastructure, strong government healthcare investments, and increasing adoption of minimally invasive orthopedic procedures. The country also benefits from a rapidly expanding network of tertiary care hospitals, rising medical tourism, and high prevalence of osteoarthritis and trauma-related injuries. Increasing focus on healthcare modernization, adoption of advanced surgical energy platforms, and growing investment in orthopedic specialty centers continue to strengthen Saudi Arabia’s leadership position in the regional market.

The UAE Orthopedic Surgical Surgical Energy Devices Market Insight

The UAE orthopedic surgical energy devices market is expanding steadily, supported by strong government initiatives in healthcare modernization, rising medical tourism, and increasing demand for advanced orthopedic procedures. The country’s highly developed private healthcare sector and adoption of cutting-edge surgical technologies are driving utilization of energy-based devices across hospitals and ambulatory surgical centers. In addition, growing investments in smart hospitals and integration of minimally invasive surgical systems are further strengthening market growth across the region.

South Africa Orthopedic Surgical Energy Devices Market Insight

The South Africa orthopedic surgical energy devices market is growing due to rising burden of trauma cases, sports injuries, and degenerative bone disorders. Increasing investments in public and private healthcare infrastructure, along with gradual adoption of advanced surgical technologies, are supporting market expansion. However, limited access to high-cost surgical systems in rural and underfunded hospitals continues to create disparities in adoption. Despite these challenges, rising awareness of minimally invasive procedures and growing expansion of private hospital networks are driving steady demand for orthopedic energy devices in the country.

Egypt Orthopedic Surgical Energy Devices Market Insight

The Egypt orthopedic surgical energy devices market is experiencing steady growth driven by a large patient population, increasing prevalence of osteoarthritis, and rising demand for orthopedic surgical interventions. Expansion of public healthcare facilities and gradual modernization of hospital infrastructure are supporting adoption of advanced surgical energy systems. In addition, growing investment in specialty orthopedic centers and increasing awareness of minimally invasive procedures are contributing to market development. However, cost constraints in public hospitals still limit widespread adoption of high-end surgical technologies.

Saudi Arabia Orthopedic Surgical Energy Devices Market Insight

The Saudi Arabia orthopedic surgical energy devices market is the most dominant in the region, supported by large-scale healthcare investments under national transformation programs and rapid expansion of tertiary care and specialty orthopedic hospitals. Increasing prevalence of obesity, osteoarthritis, and road traffic accidents is significantly driving surgical volumes. Strong adoption of advanced technologies such as radiofrequency, ultrasound, and radiation-based systems is enhancing surgical precision and efficiency. In addition, rising medical tourism and availability of highly skilled orthopedic surgeons are further strengthening market growth and positioning Saudi Arabia as the regional leader.

Middle East and Africa Orthopedic Surgical Energy Devices Market Share

The Middle East and Africa Orthopedic Surgical Energy Devices industry is primarily led by well-established companies, including:

- Stryker (U.S.)

- Medtronic (Ireland)

- Johnson & Johnson Services, Inc. (U.S.)

- Smith & Nephew (U.K.)

- Olympus Corporation (Japan)

- B. Braun SE (Germany)

- CONMED Corporation (U.S.)

- Zimmer Biomet. (U.S.)

- Boston Scientific Corporation (U.S.)

- Karl Storz SE & Co. KG (Germany)

- Erbe Elektromedizin GmbH (Germany)

- KLS Martin Group (Germany)

- Aesculap AG (Germany)

- Applied Medical Resources Corporation (U.S.)

- Integra LifeSciences Holdings Corporation (U.S.)

- Richard Wolf GmbH (Germany)

- Apyx Medical Corporation (U.S.)

- BOWA-electronic GmbH & Co. KG (Germany)

- Misonix, Inc. (Bioventus Inc.) (U.S.)

- De Soutter Medical (U.K.)

Latest Developments in Middle East and Africa Orthopedic Surgical Energy Devices Market

- In March 2025, Stryker announced the expansion of its orthopedic and powered surgical instruments distribution network across the Middle East region, strengthening access to advanced surgical energy devices used in minimally invasive orthopedic procedures. The company highlighted growing demand from hospitals in Gulf countries for high-precision surgical tools used in trauma and joint replacement surgeries. This expansion supports improved availability of electrosurgical and powered orthopedic systems across key healthcare facilities in the region

- In September 2024, UAE healthcare authorities reported increased investment in trauma care infrastructure following a rise in road traffic accident cases, leading to higher adoption of advanced orthopedic surgical technologies in public and private hospitals. Hospitals increasingly integrated energy-based surgical systems to manage fracture fixation and reconstructive orthopedic procedures. This development reflects growing reliance on minimally invasive orthopedic surgery solutions in the country

- In June 2023, Saudi Arabia’s Ministry of Health expanded orthopedic specialty services across major tertiary hospitals under healthcare modernization initiatives, increasing the use of advanced surgical energy devices in hip and knee replacement procedures. The initiative aimed to improve surgical outcomes and reduce recovery time through minimally invasive techniques. This expansion significantly strengthened demand for radiofrequency and electrosurgical systems in the country

- In April 2022, South African public hospitals increased adoption of modern electrosurgical systems in orthopedic trauma units, driven by rising accident-related injuries and growing demand for cost-effective surgical solutions. Hospitals upgraded surgical infrastructure to improve efficiency in bone cutting and coagulation procedures. This development highlights gradual modernization of orthopedic surgical capabilities in public healthcare facilities

- In February 2021, major global medical device companies including Medtronic and Zimmer Biomet expanded their distributor partnerships across African markets, improving access to orthopedic surgical energy devices in emerging healthcare systems. These partnerships helped strengthen supply chains for advanced surgical tools used in orthopedic trauma and reconstructive surgeries. The expansion supported broader adoption of minimally invasive orthopedic procedures across the region

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.