Middle East And Africa Ultrasound Imaging Devices Market

Market Size in USD Billion

CAGR :

%

USD

1.59 Billion

USD

2.94 Billion

2025

2033

USD

1.59 Billion

USD

2.94 Billion

2025

2033

| 2026 –2033 | |

| USD 1.59 Billion | |

| USD 2.94 Billion | |

| % | |

|

Middle East and Africa Ultrasound Imaging Devices Market Size

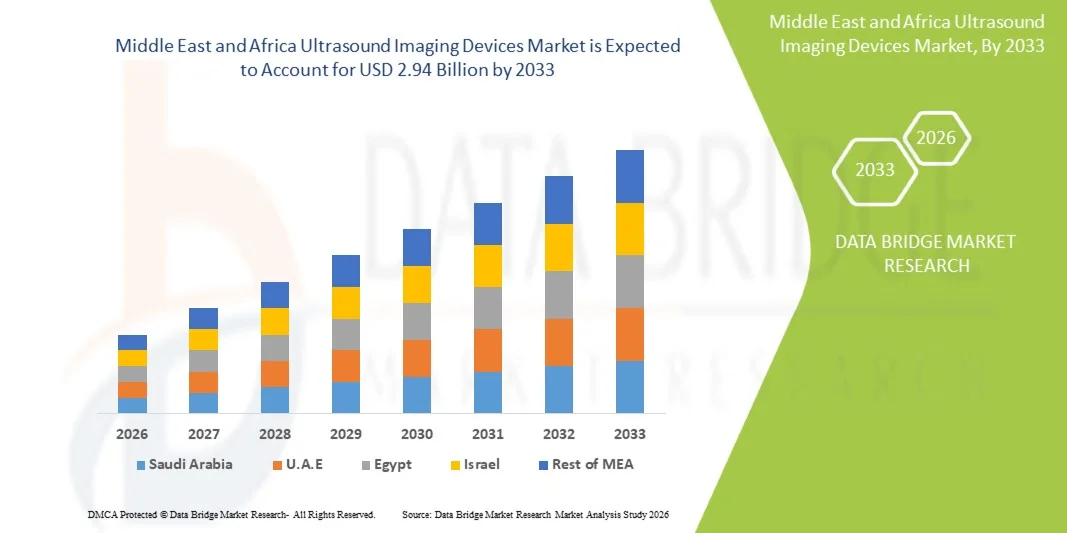

- The Middle East and Africa ultrasound imaging devices market size was valued at USD 1.59 billion in 2025and is expected to reach USD 2.94 billion by 2033, at a CAGR of 8.00% during the forecast period

- The market growth is primarily driven by the rising prevalence of chronic diseases, increasing maternal and fetal care needs, and expanding use of ultrasound systems in emergency and point-of-care diagnostics across hospitals and diagnostic centers

- Furthermore, growing healthcare infrastructure development, government initiatives to improve diagnostic imaging access, and the shift toward portable and AI-enabled ultrasound devices are significantly accelerating market adoption across the region

Middle East and Africa Ultrasound Imaging Devices Market Analysis

- Ultrasound imaging devices, offering non-invasive, real-time diagnostic imaging for a wide range of clinical applications, are becoming essential tools in modern healthcare systems across the Middle East and Africa due to their safety, portability, and expanding use in primary, emergency, and specialized care settings

- The increasing demand for ultrasound imaging devices is primarily driven by the rising burden of chronic and lifestyle-related diseases, growing maternal and neonatal healthcare needs, and expanding adoption of point-of-care ultrasound in hospitals and diagnostic centers

- Saudi Arabia dominated the ultrasound imaging devices market with the largest revenue share of 32.6% in 2025, supported by advanced hospital infrastructure, strong government healthcare investments under national transformation programs, and rapid adoption of high-end diagnostic imaging technologies

- Nigeria is expected to be the fastest growing country in the ultrasound imaging devices market during the forecast period due to improving healthcare access, rising investments in diagnostic infrastructure, and increasing deployment of portable and cost-effective ultrasound systems across urban and rural care settings

- The Trolley/Cart-Based Ultrasound Devices segment dominated the market with a substantial share of 54.1% in 2025, driven by its superior imaging performance, wide clinical applicability, and strong utilization in hospitals and advanced diagnostic facilities

Report Scope and Middle East and Africa Ultrasound Imaging Devices Market Segmentation

|

Attributes |

Middle East and Africa Ultrasound Imaging Devices Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa |

|

Key Market Players |

|

|

Market Opportunities |

· Expansion of portable and handheld ultrasound devices for point-of-care diagnostics in emergency, rural, and home healthcare settings · Increasing integration of AI-powered ultrasound imaging for automated diagnosis |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Middle East and Africa Ultrasound Imaging Devices Market Trends

“Growing Adoption of AI-Enabled and Portable Imaging Systems”

- A significant and accelerating trend in the Middle East and Africa ultrasound imaging devices market is the integration of artificial intelligence (AI) with advanced imaging systems and the rapid shift toward portable and handheld ultrasound devices for flexible diagnostic use

- For instance, GE HealthCare AI-enabled ultrasound platforms are being increasingly deployed in hospitals across Saudi Arabia and the UAE to enhance image interpretation accuracy and reduce scan time in critical care settings

- AI integration in ultrasound systems enables automated image analysis, improved lesion detection, and real-time clinical decision support, helping radiologists and clinicians achieve faster and more accurate diagnoses in high-volume healthcare environments

- Furthermore, the rising adoption of portable and handheld ultrasound devices allows physicians to perform bedside and point-of-care imaging in emergency rooms, ambulances, and remote clinics, significantly improving access to diagnostic care

- Increasing adoption of 3D and 4D ultrasound imaging technologies is further enhancing diagnostic precision in obstetrics, cardiology, and oncology, supporting more detailed and accurate clinical evaluations

- This trend toward intelligent, compact, and connected ultrasound systems is reshaping diagnostic workflows by enabling faster decision-making, improved workflow efficiency, and wider accessibility across urban and rural healthcare facilitie

- The demand for AI-powered and portable ultrasound imaging devices is growing rapidly across hospitals and diagnostic centers, as healthcare providers increasingly prioritize speed, accuracy, and accessibility in patient care delivery

Middle East and Africa Ultrasound Imaging Devices Market Dynamics

Driver

“Rising Burden of Chronic Diseases and Expanding Diagnostic Infrastructure”

- The increasing prevalence of chronic diseases such as cardiovascular disorders, cancer, and liver conditions, along with growing maternal and neonatal healthcare needs, is a major driver for ultrasound imaging device adoption in the Middle East and Africa

- For instance, in April 2025, Saudi Arabia expanded its national hospital network under Vision 2030, increasing procurement of advanced diagnostic imaging systems including ultrasound devices to strengthen early disease detection capabilities

- As patient awareness and screening programs improve, ultrasound imaging is increasingly being used for early diagnosis, monitoring, and treatment guidance, offering a safe and cost-effective imaging solution compared to other modalities

- Furthermore, government investments in healthcare infrastructure and the expansion of private diagnostic centers are significantly improving access to imaging services across urban and semi-urban populations

- The rising adoption of tele-ultrasound solutions is enabling remote diagnosis and specialist consultation in underserved areas, improving access to quality healthcare services

- Increasing use of ultrasound in preventive health screening programs for maternal care and cardiovascular assessment is further strengthening routine diagnostic demand across the region

- The growing preference for non-invasive, real-time imaging techniques and increasing integration of ultrasound systems in emergency and primary care settings are key factors propelling market growth across the region

Restraint/Challenge

“High Equipment Cost and Shortage of Skilled Radiology Professionals”

- Concerns related to the high cost of advanced ultrasound imaging systems and the limited availability of skilled radiologists and sonographers pose a significant challenge to broader market penetration in several Middle Eastern and African countries

- For instance, healthcare facilities in several African nations still rely on basic ultrasound systems due to budget constraints, limiting access to advanced imaging features such as AI-based diagnostics and 3D/4D imaging

- Addressing affordability issues through cost-effective portable devices and flexible financing models is crucial for expanding adoption, especially in public healthcare systems and rural medical centers

- Furthermore, the shortage of trained professionals capable of operating advanced ultrasound systems and interpreting complex imaging results limits the effective utilization of these technologies in many healthcare settings

- Limited availability of continuous medical training programs in rural healthcare systems further widens the skill gap, slowing down the adoption of advanced imaging technologies

- Dependence on imported high-end ultrasound equipment in many countries also increases maintenance and operational costs, creating additional financial pressure on healthcare providers

- Overcoming these challenges through affordable technology development, increased training initiatives, and government-supported healthcare workforce expansion will be vital for sustained market growth

Middle East and Africa Ultrasound Imaging Devices Market Scope

The market is segmented on the basis of array format, device display, device portability, technology, application, end-user, and distribution channel.

- By Array Format

On the basis of array format, the ultrasound imaging devices market is segmented into phased array, linear array, curved linear array, and others. The curved linear array segment dominated the market with the largest revenue share of 41.8% in 2025, driven by its extensive use in abdominal, obstetrics, and gynecology imaging across hospitals and diagnostic centers in the Middle East and Africa. Its ability to provide deeper tissue penetration and wide field-of-view makes it highly suitable for general imaging applications. Hospitals prefer curved array probes due to their versatility in routine examinations and emergency diagnostics. In addition, cost-effectiveness and widespread availability further strengthen its dominance across public healthcare systems. Strong adoption in maternal healthcare programs and prenatal screening initiatives also contributes significantly to its market leadership. The segment continues to benefit from rising demand for multipurpose imaging probes in resource-constrained healthcare settings.

The phased array segment is expected to witness the fastest growth rate of 8.6% from 2026 to 2033, driven by increasing use in cardiovascular and critical care applications. These probes are highly effective in imaging through narrow acoustic windows, making them ideal for cardiac assessments in emergency and ICU settings. Rising prevalence of cardiovascular diseases in countries such as Saudi Arabia and South Africa is accelerating demand. Their compact design and real-time imaging capability make them suitable for portable ultrasound systems. Increasing adoption in point-of-care diagnostics is further boosting growth across urban hospitals. Technological advancements enhancing image resolution are also supporting faster market penetration.

- By Device Display

On the basis of device display, the market is segmented into color ultrasound devices and black and white (B/W) ultrasound devices. The color ultrasound devices segment dominated the market with the largest revenue share of 76.3% in 2025, driven by superior imaging clarity and advanced diagnostic capabilities across multiple clinical applications. These systems are widely used in obstetrics, cardiology, and radiology departments across tertiary care hospitals. Growing demand for accurate real-time blood flow visualization using Doppler imaging is a major growth driver. Healthcare providers prefer color systems due to improved diagnostic confidence and reduced error rates. Government investments in modernizing hospital infrastructure are further boosting adoption. Increasing use in complex disease diagnosis also supports segment dominance. Continuous technological upgrades are reinforcing their leadership position in the market.

The black and white (B/W) ultrasound devices segment is expected to witness the fastest growth rate of 7.2% from 2026 to 2033, driven by rising demand in low-resource healthcare settings. These devices are widely used in rural clinics and small diagnostic centers due to their affordability. Increasing maternal healthcare screening programs in Africa are boosting demand for basic imaging solutions. Their low maintenance cost makes them attractive for budget-constrained healthcare systems. Expansion of primary healthcare infrastructure is further supporting growth. Despite limited advanced features, they remain essential for basic diagnostic applications.

- By Device Portability

On the basis of device portability, the market is segmented into trolley/cart-based ultrasound devices, compact/handheld ultrasound devices, stationary ultrasound devices, and point-of-care ultrasound devices. The trolley/cart-based ultrasound devices segment dominated the market with the largest revenue share of 54.1% in 2025, driven by their high imaging performance and widespread use in hospitals and diagnostic centers. These systems are preferred for detailed diagnostic imaging across radiology and cardiology departments. Their ability to support multiple transducers enhances clinical flexibility. Strong utilization in tertiary care hospitals across Saudi Arabia and UAE reinforces segment dominance. High reliability and advanced imaging features make them a standard choice in established healthcare facilities. Continuous hospital infrastructure upgrades further strengthen adoption.

The compact/handheld ultrasound devices segment is expected to witness the fastest growth rate of 9.3% from 2026 to 2033, driven by increasing demand for mobility and point-of-care diagnostics. These devices are widely used in emergency medicine, ambulatory care, and rural healthcare settings. Rising adoption in pre-hospital and ambulance-based care is significantly boosting demand. Their affordability and ease of use make them suitable for developing healthcare systems. Integration with smartphones and AI-based imaging is accelerating adoption. Growing preference for bedside diagnostics is further supporting rapid expansion.

- By Technology

On the basis of technology, the market is segmented into diagnostic ultrasound and therapeutic ultrasound. The diagnostic ultrasound segment dominated the market with the largest revenue share of 89.5% in 2025, driven by its extensive use in disease detection, pregnancy monitoring, and organ imaging across all healthcare settings. Hospitals rely heavily on diagnostic ultrasound for real-time, non-invasive imaging. Increasing burden of chronic diseases is fueling continuous demand. Strong adoption in obstetrics and emergency care further reinforces dominance. Government-led screening programs are also contributing significantly. Wide availability and cost-effectiveness strengthen its leadership position.

The therapeutic ultrasound segment is expected to witness the fastest growth rate of 8.1% from 2026 to 2033, driven by increasing use in physiotherapy and minimally invasive treatments. It is widely used for pain management, tissue healing, and musculoskeletal therapies. Rising orthopedic cases and sports injuries are boosting adoption. Growing awareness of non-surgical treatment options is supporting demand. Increasing integration in rehabilitation centers is further driving growth. Technological advancements in focused ultrasound therapies are enhancing clinical applications.

- By Application

On the basis of application, the market is segmented into radiology/general imaging, obstetrics and gynecology, cardiovascular, gastroenterology, vascular, urological, orthopedic and musculoskeletal, pain management, emergency department, critical care, and others. The radiology/general imaging segment dominated the market with the largest revenue share of 28.4% in 2025, driven by its broad diagnostic usage across hospitals and imaging centers. It serves as the primary application area for routine ultrasound examinations. Rising outpatient diagnostic volumes are strengthening demand. Increasing chronic disease screening programs further support dominance. Strong hospital infrastructure in GCC countries enhances adoption. Continuous upgrades in imaging technology are improving diagnostic efficiency.

The cardiovascular segment is expected to witness the fastest growth rate of 9.1% from 2026 to 2033, driven by rising prevalence of heart diseases across the region. Ultrasound is widely used for echocardiography and vascular assessment. Increasing lifestyle-related disorders are accelerating demand. Growing investment in cardiac care centers is boosting adoption. Expanding use in emergency cardiac diagnostics is further supporting growth. Technological advancements in cardiac imaging are enhancing accuracy and efficiency.

- By End-User

On the basis of end-user, the market is segmented into hospitals, surgical centers, research and academia, maternity centers, ambulatory care centers, diagnostic centers, and others. The hospitals segment dominated the market with the largest revenue share of 62.7% in 2025, driven by high patient inflow and availability of advanced imaging infrastructure. Hospitals serve as the primary point for diagnostic and emergency imaging services. Strong government investment in public hospitals is supporting dominance. Increasing chronic disease burden further boosts utilization. Availability of skilled radiologists enhances adoption of advanced systems. Continuous modernization of healthcare facilities strengthens market leadership.

The ambulatory care centers segment is expected to witness the fastest growth rate of 8.8% from 2026 to 2033, driven by rising demand for outpatient and decentralized healthcare services. These centers increasingly rely on portable ultrasound devices for rapid diagnostics. Growing preference for cost-effective outpatient care is boosting demand. Expansion of private healthcare networks is further supporting growth. Increasing focus on early diagnosis and preventive care strengthens adoption. Technological advancements in compact ultrasound systems are accelerating usage.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into direct tender, third-party distributors, and retail sales. The direct tender segment dominated the market with the largest revenue share of 58.9% in 2025, driven by bulk procurement by government hospitals and large healthcare institutions. Public healthcare systems prefer direct purchasing for cost efficiency and standardized equipment acquisition. Strong government-led healthcare expansion programs support dominance. Increasing hospital infrastructure investments further boost demand. Long-term service contracts with manufacturers enhance adoption. Centralized procurement policies strengthen market leadership.

The third-party distributors segment is expected to witness the fastest growth rate of 7.9% from 2026 to 2033, driven by expanding healthcare networks in emerging African markets. Distributors help bridge supply gaps in remote and rural regions. Growing demand for after-sales service and localized support is boosting adoption. Increasing presence of global manufacturers through distributor partnerships supports growth. Rising private healthcare expansion further accelerates demand. Ease of market entry for new technologies strengthens this channel.

Middle East and Africa Ultrasound Imaging Devices Market Regional Analysis

- Saudi Arabia dominated the ultrasound imaging devices market with the largest revenue share of 32.6% in 2025, supported by advanced hospital infrastructure, strong government healthcare investments under national transformation programs, and rapid adoption of high-end diagnostic imaging technologies

- Healthcare providers in the country increasingly prioritize ultrasound imaging devices due to their non-invasive nature, real-time diagnostic accuracy, and broad clinical applications across obstetrics, cardiology, radiology, and emergency care

- This strong adoption is further supported by government-led healthcare transformation initiatives such as Vision 2030, expansion of tertiary care hospitals, and increasing integration of AI-enabled and portable ultrasound systems, establishing ultrasound imaging as a core diagnostic modality across the healthcare ecosystem

The Saudi Arabia Ultrasound Imaging Devices Market Insight

Saudi Arabia dominated the Middle East and Africa ultrasound imaging devices market with the largest revenue share of 32.6% in 2025, driven by strong government healthcare spending and rapid expansion of advanced diagnostic infrastructure. The country is increasingly prioritizing ultrasound imaging due to its high accuracy, safety, and broad application across multiple clinical specialties. Hospitals and diagnostic centers are rapidly integrating AI-enabled and portable ultrasound systems to improve workflow efficiency and diagnostic precision. Moreover, Vision 2030 initiatives, expansion of tertiary care hospitals, and strong private sector participation are significantly strengthening market growth.

South Africa Ultrasound Imaging Devices Market Insight

South Africa is expected to witness strong growth in the ultrasound imaging devices market during the forecast period, driven by rising burden of chronic diseases and increasing demand for maternal and emergency care diagnostics. The country’s improving healthcare infrastructure and expansion of private diagnostic centers are supporting wider adoption of ultrasound systems. Portable and point-of-care ultrasound devices are gaining traction, particularly in rural and semi-urban healthcare facilities. In addition, government focus on improving access to diagnostic services is further accelerating market growth.

United Arab Emirates (UAE) Ultrasound Imaging Devices Market Insight

The United Arab Emirates (UAE) ultrasound imaging devices market is growing steadily, supported by advanced healthcare infrastructure and high adoption of cutting-edge medical technologies. Hospitals in the UAE are increasingly utilizing AI-integrated and high-resolution ultrasound systems for precise diagnostic imaging across cardiology, obstetrics, and radiology. Strong investments in smart hospitals and digital healthcare transformation are further driving demand. In addition, the presence of world-class healthcare facilities and medical tourism is boosting the uptake of advanced imaging technologies.

Nigeria Ultrasound Imaging Devices Market Insight

Nigeria is expected to register the fastest growth in the Middle East and Africa ultrasound imaging devices market during the forecast period, driven by expanding healthcare access and rising investments in diagnostic infrastructure. Increasing maternal and neonatal healthcare needs are significantly boosting demand for ultrasound imaging systems. The adoption of affordable portable ultrasound devices is improving diagnostic reach in rural and underserved regions. Furthermore, international aid programs and public-private partnerships are supporting the deployment of basic and mid-range ultrasound systems across healthcare facilities.

Middle East and Africa Ultrasound Imaging Devices Market Share

The Middle East and Africa Ultrasound Imaging Devices industry is primarily led by well-established companies, including:

- GE Healthcare (U.S.)

- Siemens Healthineers AG (Germany)

- Koninklijke Philips N.V. (Netherlands)

- Canon Medical Systems Corporation (Japan)

- FUJIFILM Holdings Corporation (Japan)

- Samsung Electronics Co., Ltd. (South Korea)

- Samsung Medison Co., Ltd. (South Korea)

- Shenzhen Mindray Bio-Medical Electronics Co., Ltd. (China)

- Hitachi, Ltd. (Japan)

- Esaote S.p.A. (Italy)

- Hologic, Inc. (U.S.)

- FUJIFILM Sonosite, Inc. (U.S.)

- Carestream Health, Inc. (U.S.)

- Konica Minolta, Inc. (Japan)

- Analogic Corporation (U.S.)

- Clarius Mobile Health Corp. (Canada)

- Butterfly Network, Inc. (U.S.)

- CHISON Medical Technologies Co., Ltd. (China)

- EDAN Instruments, Inc. (China)

- Trivitron Healthcare (India)

What are the Recent Developments in Middle East and Africa Ultrasound Imaging Devices Market?

- In March 2025, GE HealthCare expanded its AI-powered imaging and ultrasound portfolio across key Middle East and Africa markets, including Saudi Arabia, UAE, Egypt, and Türkiye. The expansion focuses on strengthening digital diagnostic ecosystems and improving workflow efficiency in hospitals and diagnostic centers. The initiative supports increasing demand for integrated imaging solutions that combine cloud connectivity and AI-assisted diagnostics

- In January 2025, GE HealthCare showcased its latest AI-enabled ultrasound and portable imaging solutions at Arab Health in Dubai, UAE, designed to enhance point-of-care diagnostics across cardiology, obstetrics, and emergency care. The solutions integrate advanced AI tools to assist clinicians in real-time image acquisition and interpretation, improving diagnostic speed and accuracy. The company emphasized the growing role of portable ultrasound systems in expanding access to imaging across the Middle East and Africa

- In June 2024, Siemens Healthineers strengthened its ultrasound presence in the Middle East and Africa by expanding availability of its ACUSON Sequoia platform in markets such as South Africa and the UAE. The system is designed to deliver high-resolution imaging for complex diagnostic applications, particularly in radiology and cardiology. The rollout supports growing demand for premium ultrasound systems in tertiary care hospitals

- In September 2023, Philips expanded its ultrasound innovation footprint in Africa through increased deployment of portable and point-of-care ultrasound systems for primary and emergency care settings. These systems are designed to improve access to diagnostic imaging in rural and underserved areas. The initiative focuses on maternal healthcare, infectious disease screening, and emergency diagnostics

- In May 2021, Mindray and other global ultrasound manufacturers expanded distribution networks across Middle East and Africa to strengthen access to cost-effective diagnostic imaging solutions. The expansion included broader availability of portable and mid-range ultrasound systems in hospitals and diagnostic clinics. The initiative aimed to address rising demand for affordable imaging in developing healthcare systems

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.