Middle East And Africa Used Car Market

Market Size in USD Billion

CAGR :

%

USD

110.06 Billion

USD

162.17 Billion

2025

2033

USD

110.06 Billion

USD

162.17 Billion

2025

2033

| 2026 –2033 | |

| USD 110.06 Billion | |

| USD 162.17 Billion | |

| % | |

|

What is the Middle East and Africa Used Car Market Size and Growth Rate?

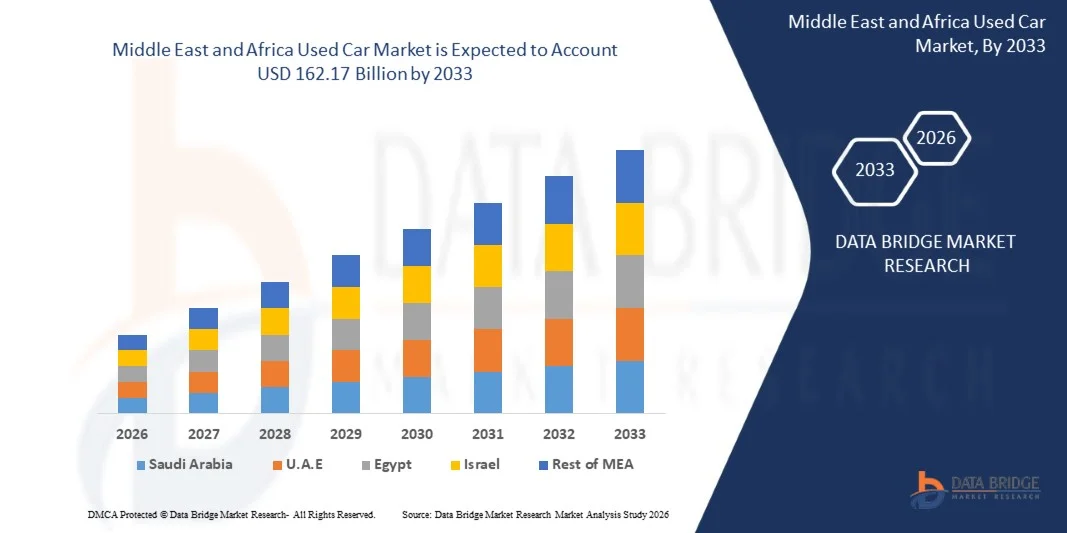

- The Middle East and Africa used car market size was valued at USD 110.06 billion in 2025 and is expected to reach USD 162.17 billion by 2033, at a CAGR of 4.90% during the forecast period

- Factors, such as high cost of new vehicles, concerns about affordability, and an increase in demand for off-lease automobiles and subscription services by the franchise, leasing offices, and car dealers, are expected to boost the growth of the Middle East & Africa used car market

What are the Major Takeaways of Used Car Market?

- The used-to-new vehicle ratio has risen dramatically in the recent years in both developed as well as emerging countries. Furthermore, franchised dealers with OEM engagement in certification and marketing programs, online inventory pooling, and access to high-quality contracts are helping the used car market to expand significantly

- South Africa dominated the Middle East & Africa Used Car market with the largest revenue share of 33.6% in 2025, supported by the strong presence of established automotive dealerships, growing consumer demand for affordable mobility solutions, and increasing vehicle replacement cycles

- U.A.E is witnessing the fastest growth rate of 11.52% in the Middle East & Africa region, driven by strong growth in digital automotive marketplaces, rising demand for luxury pre-owned vehicles, and the country’s dynamic expatriate population

- The Unorganized segment dominated the market with a 58.4% share in 2024, primarily due to the large presence of independent dealers, small local traders, and informal vehicle resale networks across emerging economies

Report Scope and Used Car Market Segmentation

|

Attributes |

Used Car Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Middle East and Africa

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

What is the Key Trend in the Used Car Market?

“Digital Transformation and Online Marketplace Expansion in Used Car Sales”

- A key trend transforming the Used Car market is the rapid shift toward digital platforms and online vehicle marketplaces, enabling consumers to browse, compare, finance, and purchase vehicles remotely. This transformation is improving convenience, transparency, and accessibility across the used vehicle buying process

- For instance, companies such as CarMax, AutoNation, and Vroom have expanded their digital retail platforms, allowing customers to complete entire vehicle purchases online, including financing approvals, vehicle inspections, and home delivery services

- The integration of AI-powered vehicle valuation tools, digital inventory management, and virtual showroom experiences allows buyers to access detailed pricing comparisons, vehicle history reports, and high-resolution inspections before making purchasing decisions

- These digital solutions are widely adopted by dealerships and online automotive platforms to streamline inventory turnover, reduce operational costs, and reach a wider customer base across regional and international markets

- Manufacturers and automotive retailers are increasingly investing in end-to-end digital ecosystems, including mobile apps, real-time vehicle tracking, and integrated payment systems to simplify used car transactions

- This trend toward digital-first car buying experiences is redefining consumer behavior and accelerating innovation across automotive retail, positioning online platforms as a critical component of the future Used Car markets

What are the Key Drivers of Used Car Market?

- The rising demand for affordable personal mobility is a major driver of the Used Car market, as consumers increasingly opt for pre-owned vehicles due to lower purchase costs compared to new vehicles

- For instance, in 2024, major automotive retailers such as Lithia Motors, CarMax, and Group 1 Automotive expanded their used vehicle inventories and digital retail platforms to capture growing demand across North America and Europe

- Increasing vehicle ownership costs, including insurance, taxes, and financing for new cars, are encouraging consumers to choose certified pre-owned (CPO) vehicles, which offer reliability and lower upfront investment

- Growth in ride-hailing, car-sharing services, and small fleet operations is also increasing demand for used vehicles, particularly fuel-efficient compact cars and commercial vehicles

- Expansion of vehicle inspection technologies, transparent pricing models, and vehicle history databases has improved buyer confidence, making used cars a safer and more attractive purchasing option

- Supported by rising urbanization, expanding automotive financing options, and growing consumer awareness, the Used Car market is expected to witness sustained global growth

Which Factor is Challenging the Growth of the Used Car Market?

- One of the major challenges affecting the Used Car market is the lack of standardized vehicle quality and pricing transparency, which can create uncertainty among buyers regarding vehicle condition and fair market value

- For instance, variations in maintenance history, accident records, and mileage manipulation in some regions continue to affect consumer trust and purchasing decisions

- Fluctuations in vehicle supply and pricing, particularly during semiconductor shortages and new vehicle production disruptions between 2022 and 2024, significantly impacted used car inventories and resale prices globally

- Limited access to reliable financing options and insurance coverage in developing markets can also restrict the purchasing capacity of potential buyer

- In addition, competition from certified pre-owned programs offered by automobile manufacturers is creating pricing pressure for independent used car dealers and online marketplaces

- To address these issues, companies are increasingly investing in AI-driven vehicle inspections, digital documentation systems, and transparent pricing models, which will be essential for strengthening buyer trust and ensuring long-term market expansion

How is the Used Car Market Segmented?

The market is segmented on the basis of vendor type, propulsion, engine capacity, dealership, sales channel, and vehicle type.

• By Vendor Type

On the basis of vendor type, the Used Car market is segmented into Organized and Unorganized. The Unorganized segment dominated the market with a 58.4% share in 2024, primarily due to the large presence of independent dealers, small local traders, and informal vehicle resale networks across emerging economies. These sellers offer competitive pricing, flexible negotiations, and faster transaction processes, which attract cost-sensitive buyers seeking affordable mobility solutions. In many developing markets, consumers often rely on local dealer networks and peer-to-peer sales for used vehicle purchases due to easier documentation processes and lower operational costs.

However, the Organized segment is expected to register the fastest CAGR from 2025 to 2032, driven by the increasing presence of certified dealerships, online automotive marketplaces, and professional vehicle inspection services. Organized platforms offer benefits such as warranty coverage, certified pre-owned (CPO) programs, financing options, and transparent vehicle history reports. Growing consumer preference for reliability, standardized pricing, and digital purchasing platforms is encouraging the expansion of organized used car dealerships globally.

• By Propulsion

On the basis of propulsion, the Used Car market is segmented into Petrol, Diesel, CNG, LPG, Electric, and Others. The Petrol segment dominated the market with a 46.7% share in 2024, driven by the widespread availability of petrol vehicles, lower maintenance costs, and strong demand for compact passenger cars in urban areas. Petrol-powered vehicles are often preferred for city driving due to smoother engine performance, lower upfront costs, and reduced servicing requirements compared to diesel-powered vehicles. The strong presence of petrol vehicles in entry-level and mid-range segments further contributes to their dominance in the used car market.

The Electric vehicle (EV) segment is projected to witness the fastest CAGR from 2025 to 2032, fueled by the rapid adoption of electric mobility and increasing resale availability of early-generation EV models. Government incentives, stricter emission regulations, and rising fuel prices are encouraging consumers to explore used electric vehicles as an affordable entry point into sustainable mobility.

• By Engine Capacity

On the basis of engine capacity, the Used Car market is segmented into Full Size (Above 2500 CC), Mid-size (Between 1500–2499 CC), and Small (Below 1499 CC). The Small engine capacity segment dominated the market with a 49.3% share in 2024, driven by strong consumer demand for fuel-efficient and affordable vehicles, particularly in densely populated urban markets. Vehicles with smaller engines typically offer lower fuel consumption, reduced maintenance costs, and easier maneuverability in congested cities. These cars are widely preferred by first-time buyers, budget-conscious consumers, and urban commuters seeking economical transportation.

The Mid-size engine capacity segment is expected to grow at the fastest CAGR from 2025 to 2032, supported by rising consumer demand for balanced performance, comfort, and fuel efficiency. Mid-size vehicles offer greater power, improved highway performance, and enhanced interior space compared to small-engine cars, making them attractive to families and long-distance commuters.

• By Dealership

On the basis of dealership, the Used Car market is segmented into Franchised and Independent dealerships. The Independent dealership segment dominated the market with a 55.8% share in 2024, supported by a vast network of local dealers offering a wide range of vehicle brands, flexible pricing structures, and diverse inventory options. Independent dealers often operate with lower overhead costs and provide competitive pricing compared to franchised dealerships, making them popular among value-focused buyers.

However, the Franchised dealership segment is anticipated to witness the fastest CAGR from 2025 to 2032, driven by increasing demand for certified pre-owned vehicles, standardized inspection processes, and manufacturer-backed warranties. Franchised dealerships are expanding their used vehicle programs, offering improved after-sales services, financing options, and trade-in programs to attract consumers seeking higher reliability and assurance in vehicle quality.

• By Sales Channel

On the basis of sales channel, the Used Car market is segmented into Online and Offline. The Offline segment dominated the market with a 63.2% share in 2024, as traditional dealership visits remain the preferred purchasing method for many consumers who want to physically inspect vehicles, conduct test drives, and negotiate prices directly with sellers. Physical dealerships also provide immediate vehicle delivery and personalized assistance, which strengthens consumer trust in the buying process.

The Online segment is expected to register the fastest CAGR from 2025 to 2032, driven by the rapid growth of digital automotive marketplaces and mobile-based vehicle purchasing platforms. Online platforms enable buyers to compare prices, view vehicle specifications, access history reports, and complete financing applications remotely, significantly improving convenience and transparency in the used car purchasing process.

• By Vehicle Type

On the basis of vehicle type, the Used Car market is segmented into Passenger Car, LCV, and HCV & Electric Vehicle. The Passenger Car segment dominated the market with a 67.5% share in 2024, primarily due to the high demand for affordable personal transportation across urban and suburban regions. Used passenger cars provide a cost-effective alternative to new vehicles while offering sufficient comfort, fuel efficiency, and practicality for everyday commuting.

The Electric Vehicle segment within HCV & Electric Vehicle category is projected to grow at the fastest CAGR from 2025 to 2032, driven by rising environmental awareness, expanding EV charging infrastructure, and government incentives promoting electric mobility. As more electric vehicles enter the secondary market, consumers are increasingly considering used EVs as a lower-cost entry point into sustainable transportation.

Which Region Holds the Largest Share of the Used Car Market?

- South Africa dominated the Middle East & Africa Used Car market with the largest revenue share of 33.6% in 2025, supported by the strong presence of established automotive dealerships, growing consumer demand for affordable mobility solutions, and increasing vehicle replacement cycles. The country has a well-developed automotive retail ecosystem, including certified pre-owned vehicle programs, independent dealerships, and expanding digital vehicle marketplaces that simplify the buying and selling of used cars. Rising urbanization, improved financing availability, and increasing consumer preference for cost-effective vehicle ownership continue to support strong market demand across major metropolitan areas such as Johannesburg, Cape Town, and Durban

- In the country, increasing adoption of online vehicle listing platforms, transparent pricing mechanisms, and certified inspection programs are strengthening consumer confidence in the used car purchasing process. Expanding automotive retail networks and improved vehicle trade-in programs further enhance accessibility to used vehicles across diverse income groups

- In South Africa, the growing middle-class population, rising demand for personal transportation, and strong dealership networks further reinforce the country’s leadership position within the Middle East & Africa Used Car market

U.A.E Used Car Market Insight

U.A.E is witnessing the fastest growth rate of 11.52% in the Middle East & Africa region, driven by strong growth in digital automotive marketplaces, rising demand for luxury pre-owned vehicles, and the country’s dynamic expatriate population. The presence of well-established online platforms, certified dealerships, and transparent vehicle inspection services is transforming the used car purchasing experience. Consumers increasingly prefer online vehicle browsing, digital documentation, and quick financing approvals, which significantly accelerate transaction processes in the market.

Nigeria Used Car Market Insight

In Nigeria, the Used Car market is expanding steadily, supported by rising demand for affordable transportation and strong reliance on imported pre-owned vehicles. The country remains one of the largest markets for used vehicles in Africa, with a significant share of vehicles sourced from Europe, the U.S., and Asia. Growing urban populations, increasing ride-hailing services, and the need for cost-effective mobility solutions continue to stimulate demand for used cars across major cities such as Lagos and Abuja.

Which are the Top Companies in Used Car Market?

The used car industry is primarily led by well-established companies, including:

- Group1 Automotive, Inc. (U.S.)

- AutoNation, Inc. (U.S.)

- CarMax Business Services, LLC (U.S.)

- eBay Inc. (U.S.)

- Maruti Suzuki India Limited (India)

- Hellman & Friedman LLC (U.S.)

- Pendragon (U.K.)

- Manheim (U.S.)

- The Hertz Corporation (U.S.)

- Cox Automotive (U.S.)

- Sun Toyota (U.S.)

- TrueCar, Inc. (U.S.)

- Vroom (U.S.)

- Asbury Automotive Group (U.S.)

- Lithia Motors, Inc. (U.S.)

- Hendrick Automotive Group (U.S.)

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.