North America Ambulatory Infusion Pumps Market

Market Size in USD Billion

CAGR :

%

USD

6.97 Billion

USD

15.71 Billion

2025

2033

USD

6.97 Billion

USD

15.71 Billion

2025

2033

| 2026 –2033 | |

| USD 6.97 Billion | |

| USD 15.71 Billion | |

| % | |

|

North America Ambulatory Infusion Pumps Market Size

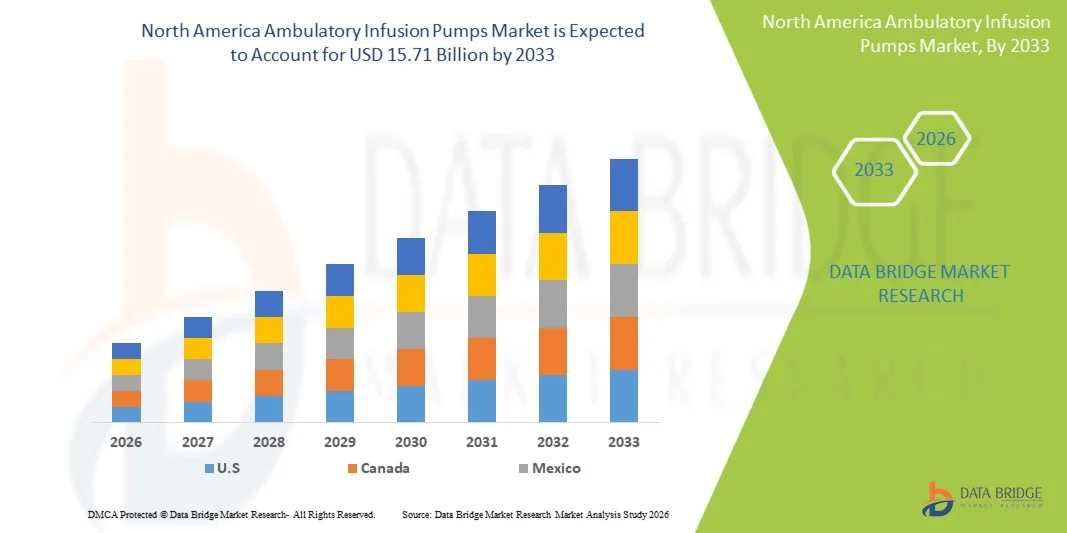

- The North America ambulatory infusion pumps market size was valued at USD 6.97 billion in 2025 and is expected to reach USD 15.71 billion by 2033, at a CAGR of 10.7% during the forecast period

- The market growth is primarily driven by the rising prevalence of chronic diseases such as cancer, diabetes, and pain-related disorders, which are increasing the demand for precise and continuous drug delivery solutions in outpatient and home healthcare settings

- Furthermore, growing adoption of home-based and ambulatory care models, along with advancements in portable and smart infusion pump technologies, is enhancing treatment convenience, improving patient compliance, and significantly accelerating the uptake of ambulatory infusion pump systems across North America

North America Ambulatory Infusion Pumps Market Analysis

- Ambulatory infusion pumps, which are portable medical devices designed to deliver controlled and continuous doses of medications such as insulin, chemotherapy agents, and pain management drugs, are increasingly vital in modern healthcare settings due to their ability to support outpatient care, improve patient mobility, and enhance treatment precision

- The growing demand for ambulatory infusion pumps is primarily driven by the rising prevalence of chronic diseases such as cancer, diabetes, and cardiovascular disorders, along with the increasing shift toward home healthcare, outpatient treatment, and technologically advanced drug delivery systems that improve safety and dosage accuracy

- The United States dominated the North America ambulatory infusion pumps market with the largest revenue share of 88.5% in 2025, supported by advanced healthcare infrastructure, high adoption of innovative medical devices, and strong utilization of home infusion therapies, with increasing integration of smart pump technologies in hospitals and home care settings

- Canada is expected to be the fastest growing country during the forecast period due to expanding home healthcare services, increasing government support for remote monitoring solutions, and rising adoption of advanced infusion technologies across clinical and ambulatory care environments

- The oncology segment dominated the North America ambulatory infusion pumps market with a market share of 42.9% in 2025, driven by the high cancer burden and the increasing use of ambulatory infusion systems for chemotherapy administration, enabling precise drug delivery, reduced hospitalization, and improved patient comfort during long treatment cycles

Report Scope and North America Ambulatory Infusion Pumps Market Segmentation

|

Attributes |

North America Ambulatory Infusion Pumps Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

North America Ambulatory Infusion Pumps Market Trends

“Advancement of Smart, Connected, and Portable Drug Delivery Systems”

- A significant and accelerating trend in the North America ambulatory infusion pumps market is the integration of smart connectivity features such as Bluetooth, Wi-Fi, and cloud-based monitoring systems, improving real-time dosage tracking and patient management in home and hospital settings

- For instance, Baxter’s Sigma Spectrum infusion systems and ICU Medical’s Plum 360 platform are increasingly being enhanced with connectivity features that allow clinicians to remotely monitor infusion parameters and improve medication safety outcomes

- Digital integration in ambulatory infusion pumps enables features such as automated dose tracking, programmable delivery schedules, and real-time alerts for occlusions or dosage errors, thereby improving clinical precision and reducing medication risks in long-term therapies

- The seamless integration of infusion pumps with electronic health records (EHR) and hospital information systems is enabling centralized patient data management, allowing healthcare providers to make faster and more informed treatment decisions across care settings

- The growing use of AI-enabled predictive analytics in infusion systems is further enhancing early detection of infusion failures and improving personalized treatment adjustments for chronic disease patients in home care settings

- This trend towards more intelligent, portable, and interconnected infusion systems is reshaping expectations for outpatient care delivery, with companies such as BD and Fresenius Kabi developing next-generation pumps with enhanced mobility and digital compatibility

- The demand for smart ambulatory infusion pumps is growing rapidly across oncology, diabetes, and pain management applications, as healthcare providers increasingly prioritize safety, remote monitoring, and patient-centric home infusion therapy

North America Ambulatory Infusion Pumps Market Dynamics

Driver

“Rising Chronic Disease Burden and Expansion of Home Infusion Therapy”

- The increasing prevalence of chronic diseases such as cancer, diabetes, and cardiovascular disorders, coupled with the growing shift toward home-based healthcare, is a major driver for the rising demand for ambulatory infusion pumps

- For instance, in April 2025, Baxter International Inc. expanded its home infusion service initiatives in the United States, aiming to improve outpatient chemotherapy and antibiotic administration through advanced portable infusion systems

- As patients and healthcare systems seek to reduce hospital stays and associated costs, ambulatory infusion pumps offer precise, continuous drug delivery that supports safe and effective treatment in non-hospital environments

- Furthermore, the growing adoption of outpatient care models and increasing reimbursement support for home healthcare services are making ambulatory infusion therapy more accessible across North America

- The increasing focus on patient-centric care models and value-based healthcare delivery is further encouraging hospitals to adopt ambulatory infusion systems for improved long-term treatment outcomes

- Expansion of specialty pharmacy networks and home infusion service providers is also strengthening distribution channels and improving patient access to infusion therapies across urban and rural areas

- The convenience of portable drug delivery systems, combined with improved patient compliance and reduced clinical workload, are key factors accelerating the adoption of ambulatory infusion pumps in both hospital discharge and chronic care settings

- Overcoming this demand through continuous innovation in pump miniaturization, improved battery life, and enhanced safety features will be vital for sustained market expansion

Restraint/Challenge

“High Device Costs and Risk of Medication Errors and Technical Failures”

- Concerns regarding high initial device costs and the complexity of operation pose a significant challenge to broader adoption of ambulatory infusion pumps, particularly in smaller healthcare facilities and home care settings

- For instance, reports of programming errors and device malfunctions in electronic infusion pumps have raised concerns among clinicians about potential risks of underdosing or overdosing during long-term therapies

- Ensuring patient safety through advanced alarm systems, automated dosage controls, and user-friendly interfaces is critical to minimizing medication errors and improving clinical confidence in these devices

- Additionally, the relatively high maintenance costs and need for regular calibration and technical support can limit adoption, especially in cost-sensitive healthcare environments and developing care infrastructure

- Increasing cybersecurity vulnerabilities in connected infusion pumps also raise concerns about unauthorized access and potential disruption of drug delivery systems in critical care scenarios

- Limited technical training among home healthcare providers and patients can further increase the risk of misuse or incorrect pump programming in ambulatory settings

- While advanced smart pumps from companies such as B. Braun and ICU Medical offer improved safety features, their higher price point remains a barrier for widespread use in smaller outpatient clinics

- Addressing these challenges through cost optimization, improved device reliability, enhanced cybersecurity, and better user training programs will be essential for sustained market penetration

North America Ambulatory Infusion Pumps Market Scope

The market is segmented on the basis of product type, usage, route of administration, application, end user, and distribution channel.

- By Product Type

On the basis of product type, the market is segmented into devices, and accessories and consumables. The devices segment dominated the market with the largest revenue share of 65% in 2025, driven by the high upfront demand for advanced ambulatory infusion pump systems used across hospitals and home care settings. These devices are essential for precise and programmable drug delivery, making them the core component of infusion therapy. Strong adoption of smart and portable pump technologies, along with frequent upgrades in hospital infrastructure, further supports the dominance of this segment. The increasing use of electronic pumps for chronic disease management and oncology care also reinforces steady demand for devices. Additionally, hospitals prefer investing in durable pump systems due to long-term cost efficiency and improved patient safety outcomes.

The accessories and consumables segment is expected to witness the fastest growth rate of 12% CAGR during 2026–2033, driven by recurring demand for infusion sets, catheters, tubing, and cartridges used in continuous therapy. Growth is strongly supported by the rising number of home infusion patients requiring regular replacement of consumables. Increasing oncology and diabetes treatment cycles further contribute to high repeat purchases. Expansion of outpatient care services and specialty pharmacy distribution channels is also accelerating consumables demand. Moreover, technological advancements in disposable infusion components are improving safety and reducing infection risks, boosting adoption.

- By Usage

On the basis of usage, the market is segmented into disposable and reusable systems. The reusable segment dominated the market with a revenue share of 60% in 2025, due to widespread hospital preference for cost-effective, durable infusion pump systems that can be used across multiple patients with proper sterilization. Reusable pumps offer advanced programmability, better accuracy, and long operational life, making them suitable for high-volume clinical environments. Hospitals and surgical centers prefer reusable systems for their reliability in complex therapies such as oncology and pain management. Strong procurement by healthcare institutions and long-term infrastructure investments further support this dominance. Additionally, reusable systems are often integrated with digital monitoring platforms, enhancing their clinical utility.

The disposable segment is expected to witness the fastest growth rate of 13% CAGR from 2026 to 2033, driven by rising demand for home healthcare and infection control concerns. Disposable infusion pumps are increasingly used in outpatient chemotherapy and short-term pain management therapies. Their ease of use, elimination of cross-contamination risks, and no requirement for sterilization make them highly suitable for home care settings. Increasing preference for patient-friendly, single-use medical devices is further accelerating adoption. Growth in ambulatory surgical procedures and decentralized care delivery models is also boosting demand for disposable systems.

- By Route of Administration

On the basis of route of administration, the market is segmented into subcutaneous, intravenous, and epidural. The intravenous segment dominated the market with the largest revenue share of 52% in 2025, driven by its widespread use in hospitals for chemotherapy, antibiotics, and fluid delivery in critical care and chronic disease treatment. IV infusion pumps offer precise control over drug administration, making them essential for high-risk therapies. Strong adoption in oncology and emergency medicine further strengthens this segment’s dominance. Hospitals prefer intravenous delivery due to its rapid drug absorption and high clinical efficiency. Continuous improvements in IV pump safety features also support widespread usage across care settings.

The subcutaneous segment is expected to witness the fastest growth rate of 12% CAGR during 2026–2033, driven by increasing adoption in diabetes management and home-based insulin delivery. Subcutaneous infusion pumps offer improved patient comfort and enable long-term self-administration of medication. Rising preference for minimally invasive drug delivery methods is further supporting growth. Expansion of home healthcare services and wearable infusion technologies is accelerating adoption. Additionally, increasing use in pain management and hormonal therapies is boosting demand for this route.

- By Application

On the basis of application, the market is segmented into emergency medicine, general anaesthesia, pain management, oncology, diabetes, gastroenterology, neonatology, and others. The oncology segment dominated the market with a revenue share of 42.9% in 2025, driven by the high prevalence of cancer and the widespread use of infusion pumps for chemotherapy administration. Ambulatory infusion pumps enable controlled, long-duration drug delivery, improving treatment accuracy and patient comfort. Strong hospital-based oncology infrastructure and rising cancer incidence in North America further support dominance. Increasing adoption of home-based chemotherapy is also boosting demand. Technological advancements in portable infusion systems are improving treatment continuity outside hospital settings.

The diabetes segment is expected to witness the fastest growth rate of 14% CAGR from 2026 to 2033, driven by the rising diabetic population and increasing use of insulin infusion pumps. Continuous subcutaneous insulin infusion systems are gaining traction for better glycemic control and reduced complications. Growth is supported by increasing awareness of advanced diabetes management technologies. Expanding home healthcare adoption and wearable pump innovations are further accelerating growth. Additionally, strong reimbursement support in the U.S. is encouraging wider adoption.

- By End User

On the basis of end user, the market is segmented into hospitals, specialty clinics, ambulatory surgical centers, home care settings, and others. The hospitals segment dominated the market with the largest revenue share of 48% in 2025, due to high patient inflow requiring infusion therapies for acute and chronic conditions. Hospitals extensively use ambulatory infusion pumps for oncology, emergency medicine, and post-surgical care. Strong procurement budgets and advanced healthcare infrastructure further support dominance. Integration of smart infusion systems with hospital IT networks enhances efficiency. Additionally, hospitals remain the primary setting for initiating infusion-based treatments before transitioning patients to home care.

The home care settings segment is expected to witness the fastest growth rate of 15% CAGR during 2026–2033, driven by the shift toward decentralized healthcare and patient preference for at-home treatment. Ambulatory infusion pumps enable safe and continuous drug delivery outside hospital environments. Rising chronic disease burden and aging population are key growth drivers. Increasing availability of user-friendly portable pumps is further accelerating adoption. Expansion of home infusion service providers and reimbursement support is also boosting this segment.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into direct tender and retail sales. The direct tender segment dominated the market with a revenue share of 75% in 2025, driven by large-scale procurement of infusion pumps by hospitals, healthcare systems, and government institutions. Direct contracts ensure cost efficiency, bulk purchasing, and long-term supply agreements with manufacturers. Hospitals prefer this channel for high-value devices requiring service and maintenance support. Strong presence of key manufacturers engaging in institutional sales further supports dominance. Additionally, regulatory procurement frameworks in North America favor direct tendering for medical equipment.

The retail sales segment is expected to witness the fastest growth rate of 13% CAGR from 2026 to 2033, driven by increasing adoption of home healthcare and online medical device distribution. Retail channels are gaining traction for consumables and portable pump systems used in outpatient care. Rising consumer awareness and ease of access through medical supply stores and e-commerce platforms are supporting growth. Growth in self-administered therapies such as insulin delivery is further boosting retail demand. Additionally, expansion of specialty pharmacies is strengthening this channel significantly.

North America Ambulatory Infusion Pumps Market Regional Analysis

- The United States dominated the North America ambulatory infusion pumps market with the largest revenue share of 88.5% in 2025, supported by advanced healthcare infrastructure, high adoption of innovative medical devices, and strong utilization of home infusion therapies, with increasing integration of smart pump technologies in hospitals and home care settings

- Healthcare providers in the country highly value the precision, safety features, and seamless integration of ambulatory infusion pumps with electronic health records and digital monitoring platforms for improved treatment outcomes and patient safety

- This widespread adoption is further supported by a high burden of chronic diseases, strong reimbursement support, rapid adoption of home infusion therapies, and the presence of leading medical device manufacturers, establishing the United States as the key growth hub for ambulatory infusion pump technologies

U.S. Ambulatory Infusion Pumps Market Insight

The U.S. ambulatory infusion pumps market captured the largest revenue share of 88.5% in 2025 within North America, fueled by the high burden of chronic diseases and the rapid adoption of advanced drug delivery systems across healthcare settings. Healthcare providers are increasingly prioritizing precision-based, programmable, and portable infusion systems to enhance treatment outcomes in oncology, diabetes, and pain management. The growing preference for home healthcare and outpatient infusion therapy, combined with strong reimbursement support, further propels market expansion. Moreover, the increasing integration of smart infusion pumps with EHR systems, remote monitoring platforms, and connected healthcare infrastructure is significantly contributing to the market’s growth.

Canada Ambulatory Infusion Pumps Market Insight

The Canada ambulatory infusion pumps market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by rising adoption of home healthcare services and increasing demand for cost-effective outpatient treatment solutions. The country’s growing aging population and increasing prevalence of chronic conditions are fostering the use of ambulatory infusion systems across hospitals and home care settings. Canadian healthcare providers are also focusing on improving patient convenience and reducing hospital stays through advanced portable infusion technologies. Furthermore, government support for digital health initiatives and remote patient monitoring is expected to accelerate market adoption.

Mexico Ambulatory Infusion Pumps Market Insight

The Mexico ambulatory infusion pumps market is anticipated to grow at a steady CAGR during the forecast period, driven by improving healthcare infrastructure and increasing awareness of advanced drug delivery systems. Rising cases of chronic diseases such as diabetes and cancer are encouraging greater use of infusion-based therapies in both public and private healthcare sectors. Additionally, expanding access to specialty care services and gradual adoption of modern medical technologies are supporting market growth. However, cost sensitivity and uneven healthcare access may moderately restrain widespread adoption compared to developed North American countries.

North America Ambulatory Infusion Pumps Market Share

The North America Ambulatory Infusion Pumps industry is primarily led by well-established companies, including:

- B. Braun SE (Germany)

- Fresenius Kabi AG (Germany)

- Baxter (U.S.)

- ICU Medical, Inc. (U.S.)

- BD (U.S.)

- Smiths Group plc (U.K.)

- Terumo Corporation (Japan)

- Medtronic (Ireland)

- NIPRO Corporation (Japan)

- Vygon SA (France)

- Micrel Medical Devices S.A. (Greece)

- Caesarea Medical Electronics Ltd. (Israel)

- Eitan Medical Ltd. (Israel)

- Moog Inc. (U.S.)

- Zyno Medical LLC (U.S.)

- Arcomed AG (Switzerland)

- Fresenius Kabi Deutschland GmbH (Germany)

- Tricumed Medizintechnik GmbH (Germany)

- Mindray Medical International Limited (China)

What are the Recent Developments in North America Ambulatory Infusion Pumps Market?

- In December 2025, Baxter highlighted smart infusion pump–EMR integration improving safety and workflow efficiency. Baxter presented real-world clinical evidence showing that its smart infusion pumps integrated with electronic medical records (EMR) can improve medication safety and nursing productivity

- In July 2025, Baxter reported weak demand and operational disruptions, including voluntary actions related to its infusion pump systems after safety concerns. The company also adjusted its financial outlook due to supply constraints and hospital usage changes

- In October 2024, Following Hurricane Helene, Baxter began importing IV and infusion products into the U.S. from international facilities to stabilize supply. The disruption affected a major portion of U.S. IV fluid production, leading to hospital shortages and procedural delays

- In May 2024, Baxter announced improved financial performance driven by strong demand for infusion pumps and other medical devices. The company reported increased sales in its medical products segment, supported by post-pandemic recovery in hospital procedures

- In February 2023, Becton Dickinson (BD) received FDA clearance for its updated BD Alaris infusion system, incorporating enhanced cybersecurity and safety improvements. The system supports multiple infusion types, including ambulatory and hospital-based therapies

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.