North America Analytical Laboratory Services Market

Market Size in USD Billion

CAGR :

%

USD

4.44 Billion

USD

12.75 Billion

2025

2033

USD

4.44 Billion

USD

12.75 Billion

2025

2033

| 2026 - 2033 | |

| USD 4.44 Billion | |

| USD 12.75 Billion | |

| % | |

|

North America Analytical Laboratory Services Market Overview

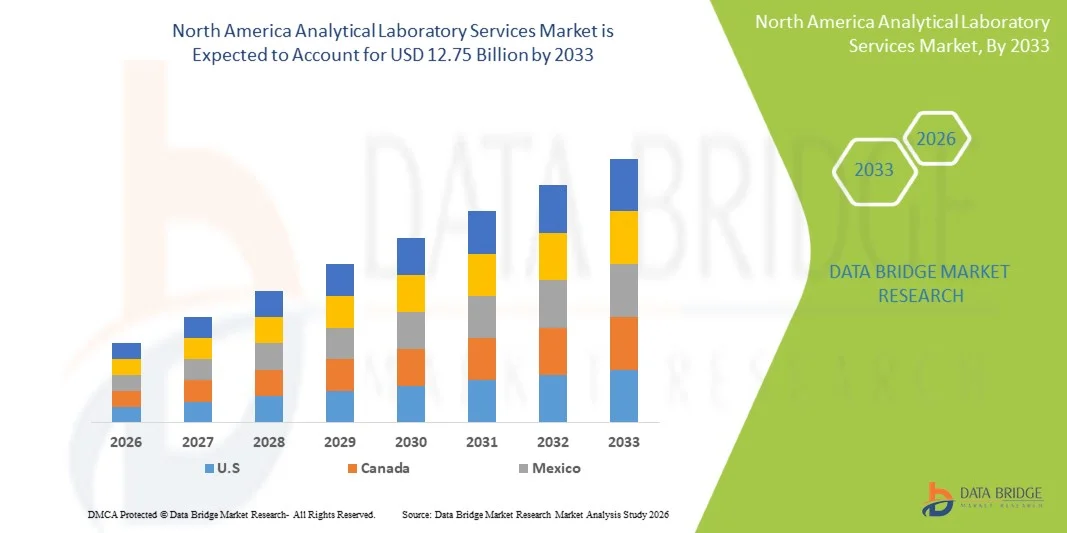

The North America analytical laboratory services market was valued at USD 4.44 billion in 2025 and is projected to reach USD 12.75 billion by 2033, growing at a CAGR of 14.1% from 2026 to 2033. The market is witnessing steady expansion driven by increasing demand for high-precision testing services, growing pharmaceutical and biotechnology R&D activities, and rising regulatory requirements for quality assurance across healthcare, food & beverage, and environmental sectors.

The growing emphasis on drug discovery, personalized medicine, and biologics development is significantly boosting the need for advanced analytical testing capabilities across contract research organizations and independent laboratories. In addition, stringent regulatory frameworks imposed by agencies such as the FDA, combined with increasing outsourcing of laboratory services by pharmaceutical and biotech companies, are accelerating market adoption. The integration of advanced technologies such as chromatography, mass spectrometry, and automation-enabled laboratory platforms is further enhancing efficiency, accuracy, and turnaround time in analytical testing workflows across North America.

Key Market Trends & Insights

- The United States dominated the North America analytical laboratory services market with the largest revenue share of 79.64% in 2025, supported by a highly advanced pharmaceutical R&D ecosystem, strong presence of CROs, and extensive FDA-regulated testing requirements across drug development pipelines.

- The Bioanalytical Testing segment led the market with a 34.67% share in 2025, driven by extensive demand from clinical trials, drug development programs, and regulatory submissions across pharmaceutical and biotechnology industries.

- Canada is expected to be the fastest-growing country in the market, registering a CAGR of 7.2% from 2026 to 2033, driven by expanding biopharmaceutical research activities, increasing clinical trial outsourcing, and rising investments in advanced analytical testing infrastructure across healthcare and life sciences sectors.

- Method Validation are the fastest-growing test type, projected to register a CAGR of 6.9%, reflecting the surge in regulatory requirements for ensuring accuracy, reliability, and reproducibility of analytical methods.

- The Stand-Alone Laboratories segment dominated the service type category with a 58.12% revenue share in 2025, led by strong infrastructure, advanced instrumentation capabilities, and high-volume testing capacity.

- Pharmacokinetic Testing accounted for 32.45% of the market, preferred by its critical role in evaluating drug absorption, distribution, metabolism, and excretion profiles.

- The Biomarker Testing segment is the fastest-growing method type category, with a CAGR of 7.3%, driven by the rising adoption of precision medicine and targeted therapies.

Market Size & Forecast

- Global Market Value (2025): USD 4.44 Billion

- Expected Market Value (2033): USD 12.75 Billion

- Forecast CAGR (2026–2033): 14.1%

- Leading Country in 2025: United States

- Fastest Growing Country: Canada

Report Scope and North America Analytical Laboratory Services Market Segmentation

|

Attributes |

North America Analytical Laboratory Services Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico |

|

Key Market Players |

· Eurofins Scientific SE (Luxembourg) · SGS S.A. (Switzerland) · Bureau Veritas S.A. (France) · SYNLAB AG (Germany) · Charles (U.S.) · IQVIA Holdings Inc. (U.S.) · Thermo Fisher Scientific Inc. (U.S.) · PRA Health Sciences (U.S.) · Labcorp. (U.S.) · Evotec SE (Germany) · Almac Group (U.K.) · Medpace Holdings, Inc. (U.S.) · Envigo (U.K.) · Intertek Group plc (U.K.) · Recipharm AB (Sweden) · WuXi AppTec (China) · Pharmaron PLC (U.K.) · Celerion (U.S.) · Frontage Laboratories (U.S.) · Cerba HealthCare (France) |

|

Market Opportunities |

· Expansion of biosimilar and biologics development pipelines · Increasing regulatory complexity under EMA guidelines · Growth of decentralized and virtual clinical trials |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

North America Analytical Laboratory Services Market Trends

Trend: Expansion of Biopharmaceutical & Precision Testing Services

Pharmaceutical and biotechnology companies are increasingly relying on advanced analytical laboratory services to support biologics development, precision medicine, and complex clinical trial analysis. The integration of high-resolution techniques such as mass spectrometry, chromatography, and molecular diagnostics is enabling deeper molecular-level insights and improving regulatory compliance outcomes. Laboratories are also adopting automation and digital laboratory information management systems to enhance throughput, reduce human error, and improve turnaround time for critical testing workflows. For instance, the increasing use of advanced LC-MS/MS platforms by CROs and biopharma companies in the United States to support biologics characterization and clinical bioanalysis reflects this growing trend.

North America Analytical Laboratory Services Market Dynamics

Key Market Driver: Rising Outsourcing of Analytical Testing Services

The growing complexity of drug development pipelines and increasing regulatory scrutiny are driving pharmaceutical and biotechnology companies to outsource analytical testing services to specialized laboratories. This shift enables cost optimization, faster time-to-market, and access to highly specialized instrumentation and scientific expertise. The expansion of clinical trials and biologics research is further strengthening demand for scalable and compliant third-party laboratory solutions across North America. For instance, the increasing outsourcing of stability testing, method validation, and bioanalytical services by U.S.-based pharmaceutical companies to contract research organizations highlights this structural market shift.

Key Restraint/Challenge: High Operational and Instrumentation Costs

A major restraint in the North America analytical laboratory services market is the high cost associated with acquiring and maintaining advanced analytical instruments such as high-resolution mass spectrometers, nuclear magnetic resonance systems, and automated chromatography platforms. In addition, ongoing expenses related to skilled workforce requirements, regulatory compliance, and frequent technology upgrades significantly increase overall operational costs, limiting accessibility for smaller laboratories and research institutions. For instance, the deployment and maintenance of fully automated GLP-compliant analytical laboratories in Canada often require substantial capital investment, making it challenging for mid-sized service providers to scale operations efficiently.

Key Market Opportunity: Integration of AI-Driven Data Analytics and Automation

The integration of artificial intelligence and advanced data analytics into laboratory workflows presents a significant opportunity for market expansion. AI-powered platforms can accelerate data interpretation, enhance predictive analytics in drug development, and optimize laboratory resource utilization. The growing adoption of cloud-based laboratory systems and digital twin technologies is further enabling real-time data sharing and improving collaboration across research networks in North America. For instance, the use of AI-enabled laboratory information management systems in U.S. clinical research laboratories to automate data validation and accelerate regulatory reporting demonstrates the expanding role of intelligent technologies in the sector.

North America Analytical Laboratory Services Market Scope

The North America analytical laboratory services market is segmented on the basis of test type, service type, method type, application, technology, and end user channel.

- By Test Type

On the basis of test type, the North America analytical laboratory services market is segmented into bioanalytical testing, batch release testing, stability testing, raw material testing, physical characterization, method validation, microbial testing, and environmental monitoring. The Bioanalytical Testing segment dominated the market with a 34.67% share in 2025, driven by extensive demand from clinical trials, drug development programs, and regulatory submissions across pharmaceutical and biotechnology industries. This segment is critical for evaluating drug concentration, metabolism, and pharmacokinetic behavior in biological systems. Increasing complexity of biologics and biosimilars is further strengthening demand for advanced analytical techniques. High outsourcing rates to CROs and specialized laboratories are also supporting growth. Continuous regulatory pressure from agencies such as the FDA is reinforcing the need for accurate and reproducible bioanalytical data. Expansion of personalized medicine pipelines is further consolidating its dominance.

The Method Validation segment is expected to register the fastest growth at a CAGR of 6.9% from 2026 to 2033, driven by increasing regulatory requirements for ensuring accuracy, reliability, and reproducibility of analytical methods. Pharmaceutical companies are increasingly investing in validation services to support global drug approvals and compliance with evolving quality standards. Rising complexity of multi-component drug formulations is further increasing demand for robust validation protocols. Growth in biologics and gene therapy pipelines is also contributing to segment expansion. Outsourcing of validation services to specialized laboratories is improving efficiency and reducing internal workload. Continuous updates in regulatory frameworks are further accelerating adoption across North America.

- By Service Type

On the basis of service type, the market is segmented into hospital-based laboratories, stand-alone laboratories, and clinic-based laboratories. The Stand-Alone Laboratories segment dominated the market with a 58.12% share in 2025, supported by strong infrastructure, advanced instrumentation capabilities, and high-volume testing capacity. These laboratories serve pharmaceutical companies, CROs, and academic institutions with specialized analytical services. They offer broader test portfolios and faster turnaround times compared to hospital-based facilities. Increasing outsourcing of complex analytical workflows is further strengthening their position. High investment in automation and digital lab systems is improving efficiency and scalability. Their independence from hospital systems enables flexible service delivery and global regulatory compliance.

The Hospital-Based Laboratories segment is expected to be the fastest growing at a CAGR of 6.5% from 2026 to 2033, driven by rising demand for integrated diagnostic and research services within healthcare institutions. Increasing clinical trial activity in hospital settings is boosting in-house analytical capabilities. Growing focus on translational research is also supporting adoption of advanced laboratory technologies. Expansion of precision medicine programs within hospitals is further increasing demand for specialized testing. Investments in upgrading hospital laboratory infrastructure are improving service quality and capacity. Strong collaboration between hospitals and pharmaceutical companies is accelerating growth across North America.

- By Method Type

On the basis of method type, the market is segmented into cell-based assays, virology testing, biomarker testing, pharmacokinetic testing, immunogenicity, and serology. The Pharmacokinetic Testing segment dominated the market with a 32.45% share in 2025, driven by its critical role in evaluating drug absorption, distribution, metabolism, and excretion profiles. It is widely used in clinical trials and regulatory submissions to ensure drug safety and efficacy. Increasing development of complex biologics is further boosting demand for advanced pharmacokinetic analysis. High reliance on outsourcing to specialized CRO laboratories is strengthening market penetration. Continuous expansion of oncology and infectious disease drug pipelines is also contributing to growth. Regulatory emphasis on comprehensive PK profiling is reinforcing its dominance.

The Biomarker Testing segment is expected to register the fastest growth at a CAGR of 7.3% from 2026 to 2033, driven by rising adoption of precision medicine and targeted therapies. Biomarker-based diagnostics are increasingly used for patient stratification and treatment monitoring. Growth in oncology and immunology research is significantly accelerating demand. Advances in high-throughput screening technologies are improving testing efficiency. Pharmaceutical companies are increasingly integrating biomarker analysis into clinical development pipelines. Expansion of companion diagnostics is further supporting rapid adoption across North America.

- By Application

On the basis of application, the market is segmented into oncology, neurology, infectious disease, gastroenterology, cardiology, and other applications. The Oncology segment dominated the market with a 38.76% share in 2025, driven by the rising global cancer burden and strong pipeline of oncology drugs. Analytical laboratory services are extensively used in tumor profiling, biomarker identification, and clinical trial monitoring. Increasing adoption of personalized cancer therapies is further boosting demand. High investment in oncology R&D by pharmaceutical companies is strengthening market dominance. Advanced molecular diagnostic techniques are improving accuracy in cancer research. Regulatory focus on precision oncology is further supporting segment growth.

The Neurology segment is expected to be the fastest growing at a CAGR of 7.1% from 2026 to 2033, driven by increasing prevalence of neurological disorders such as Alzheimer’s and Parkinson’s disease. Rising research activity in neurodegenerative disease pathways is accelerating demand for analytical testing services. Growth in CNS drug development pipelines is further supporting expansion. Advances in biomarker discovery are improving diagnostic capabilities. Increasing collaboration between research institutes and pharmaceutical companies is boosting innovation. Expansion of clinical trials in neurotherapeutics is driving strong growth across North America.

- By Technology

On the basis of technology, the market is segmented into mass spectroscopy (LC-MS/MS), immunochemistry, UPLC technology, turbulent flow technology, and others. The Mass Spectroscopy (LC-MS/MS) segment dominated the market with a 41.92% share in 2025, driven by its high sensitivity, accuracy, and ability to analyze complex biological samples. It is widely used in bioanalysis, pharmacokinetics, and drug metabolism studies. Increasing demand for biologics and biosimilars is further strengthening adoption. Continuous technological advancements are improving detection limits and throughput. High compatibility with regulatory requirements is enhancing its use in clinical studies. Strong outsourcing demand from pharmaceutical companies is further supporting dominance.

The UPLC Technology segment is expected to be the fastest growing at a CAGR of 6.8% from 2026 to 2033, driven by demand for faster and more efficient chromatographic separation techniques. UPLC offers higher resolution and reduced analysis time compared to traditional HPLC systems. Increasing need for high-throughput screening in drug development is boosting adoption. Integration with automated laboratory systems is further enhancing efficiency. Expanding applications in quality control and stability testing are driving growth. Rising focus on cost and time optimization in laboratories is supporting rapid uptake across North America.

- By End User Channel

On the basis of end user channel, the market is segmented into pharmaceutical and biopharmaceutical companies, contract development and manufacturing organizations (CDMOs), contract research organizations (CROs), and others. The Pharmaceutical and Biopharmaceutical Companies segment dominated the market with a 46.83% share in 2025, driven by high investment in drug discovery, clinical trials, and regulatory testing requirements. These companies rely heavily on analytical laboratories for ensuring drug safety, efficacy, and compliance. Increasing development of biologics and personalized therapies is further boosting demand. Strong R&D pipelines are reinforcing the need for advanced testing capabilities. Expansion of global clinical trials is also contributing to segment dominance. Continuous innovation in drug development is strengthening long-term market leadership.

The Contract Research Organizations (CROs) segment is expected to be the fastest growing at a CAGR of 7.4% from 2026 to 2033, driven by increasing outsourcing of clinical development and analytical testing services. CROs offer cost efficiency, scalability, and regulatory expertise to pharmaceutical companies. Rising complexity of clinical trials is further increasing reliance on specialized service providers. Expansion of biologics and specialty drug pipelines is boosting demand for CRO capabilities. Technological advancements are improving data accuracy and turnaround times. Growing globalization of clinical research is further accelerating CRO adoption across North America.

North America Analytical Laboratory Services Market Regional Analysis

The United States dominated the North America analytical laboratory services market with the largest revenue share of 79.64% in 2025, supported by a highly advanced pharmaceutical R&D ecosystem, strong presence of CROs, and extensive FDA-regulated testing requirements across drug development pipelines. The country also benefits from stringent FDA regulatory requirements, high R&D investment in drug discovery and clinical trials, and rapid adoption of advanced analytical technologies such as LC-MS/MS, UPLC, and molecular diagnostics. Increasing demand for biologics, precision medicine, and large-scale clinical research activities continues to strengthen the United States’ leadership position in the North America analytical laboratory services market.

U.S. Analytical Laboratory Services Market Insight

The U.S. analytical laboratory services market is witnessing strong growth due to rising investments in pharmaceutical R&D, expanding clinical trial activity, and increasing demand for advanced bioanalytical testing services. The country’s highly developed biotechnology and life sciences ecosystem, along with the strong presence of CROs and independent laboratories, is driving demand across drug development, regulatory testing, and quality control applications. In addition, stringent FDA compliance requirements and rapid adoption of advanced technologies such as LC-MS/MS, UPLC, and molecular diagnostics are accelerating analytical testing adoption across healthcare and pharmaceutical industries.

Canada Analytical Laboratory Services Market Insight

The Canada analytical laboratory services market is experiencing steady growth due to increasing investments in biopharmaceutical research, expanding clinical trial outsourcing, and rising demand for advanced diagnostic and analytical testing services. The country’s strong academic–industry collaboration ecosystem, along with growing presence of specialized contract research organizations, is supporting market expansion across drug development and healthcare research applications. In addition, increasing adoption of high-precision technologies such as mass spectrometry and chromatography, combined with strict Health Canada regulatory standards, is driving demand for high-quality, compliant laboratory services across pharmaceutical and environmental testing sectors.

Mexico Analytical Laboratory Services Market Insight

The Mexico analytical laboratory services market is growing steadily, driven by rising pharmaceutical manufacturing activities, increasing clinical research participation, and expanding demand for cost-effective laboratory testing solutions. The country is benefiting from growing outsourcing trends as global pharmaceutical companies shift analytical workflows to lower-cost regions. In addition, improving healthcare infrastructure, increasing regulatory alignment with international standards, and gradual adoption of advanced analytical technologies are supporting market expansion. Furthermore, growing investments in biotechnology and expanding contract laboratory services are positioning Mexico as an emerging hub for analytical testing services in Latin America.

North America Analytical Laboratory Services Market Share

The North America analytical laboratory services industry is primarily led by well-established companies, including:

- Eurofins Scientific SE (Luxembourg)

- SGS S.A. (Switzerland)

- Bureau Veritas S.A. (France)

- SYNLAB AG (Germany)

- Charles (U.S.)

- IQVIA Holdings Inc. (U.S.)

- Thermo Fisher Scientific Inc. (U.S.)

- PRA Health Sciences (U.S.)

- (U.S.)

- Evotec SE (Germany)

- Almac Group (U.K.)

- Medpace Holdings, Inc. (U.S.)

- Envigo (U.K.)

- Intertek Group plc (U.K.)

- Recipharm AB (Sweden)

- WuXi AppTec (China)

- Pharmaron PLC (U.K.)

- Celerion (U.S.)

- Frontage Laboratories (U.S.)

- Cerba HealthCare (France)

Latest Developments in North America Analytical Laboratory Services Market

- In October 2025, Thermo Fisher Scientific announced the acquisition of Clario for up to USD 9.4 billion, significantly strengthening its clinical research, data analytics, and integrated laboratory services capabilities across North America. The acquisition enhances end-to-end support for pharmaceutical clinical trials by combining advanced data management solutions with laboratory testing services. It also expands Thermo Fisher’s presence in decentralized and hybrid clinical trial ecosystems, where integrated analytics and lab workflows are increasingly critical. This move reflects growing consolidation in the analytical laboratory services space and rising demand for unified trial-to-lab platforms

- In August 2024, Quest Diagnostics completed the acquisition of LifeLabs, one of Canada’s largest diagnostic laboratory networks, expanding its analytical and clinical testing footprint across North America. The acquisition enhances access to high-volume diagnostic services, including specialized testing in infectious diseases, oncology, and chronic conditions. It strengthens Quest’s cross-border laboratory infrastructure and improves service integration between the United States and Canada. The deal also supports rising demand for outsourced and advanced clinical laboratory services

- In August 2024, Labcorp completed the acquisition of select Invitae assets, expanding its capabilities in genetic, oncology, and rare disease testing services across North America. The acquisition strengthens Labcorp’s position in high-complexity analytical laboratory services and precision medicine applications. It enhances support for pharmaceutical and biotechnology companies conducting biomarker-driven clinical trials. The integration improves access to advanced genomic and molecular testing platforms

- In March 2024, Labcorp expanded its clinical diagnostics network through the acquisition of select BioReference Health laboratory assets in the United States. The acquisition enhances testing capacity in reproductive health, women’s health, and general clinical diagnostics services. It strengthens Labcorp’s nationwide laboratory infrastructure and improves operational efficiency for high-throughput testing. The move supports rising demand for outsourced analytical services from healthcare providers and life sciences companies

- In April 2023, Quest Diagnostics completed the acquisition of laboratory service assets from NewYork-Presbyterian, expanding its hospital-based analytical testing network in the United States. The acquisition enhances access to advanced clinical diagnostics and strengthens integrated laboratory service offerings within hospital systems. It increases Quest’s testing capacity and improves turnaround time for high-complexity diagnostic services. The deal supports growing demand for hospital-integrated analytical laboratory solutions

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.