North America Clinical Trial Imaging Market

Market Size in USD Billion

CAGR :

%

USD

1.07 Billion

USD

2.02 Billion

2025

2033

USD

1.07 Billion

USD

2.02 Billion

2025

2033

| 2026 –2033 | |

| USD 1.07 Billion | |

| USD 2.02 Billion | |

| % | |

|

North America Clinical Trial Imaging Market Size

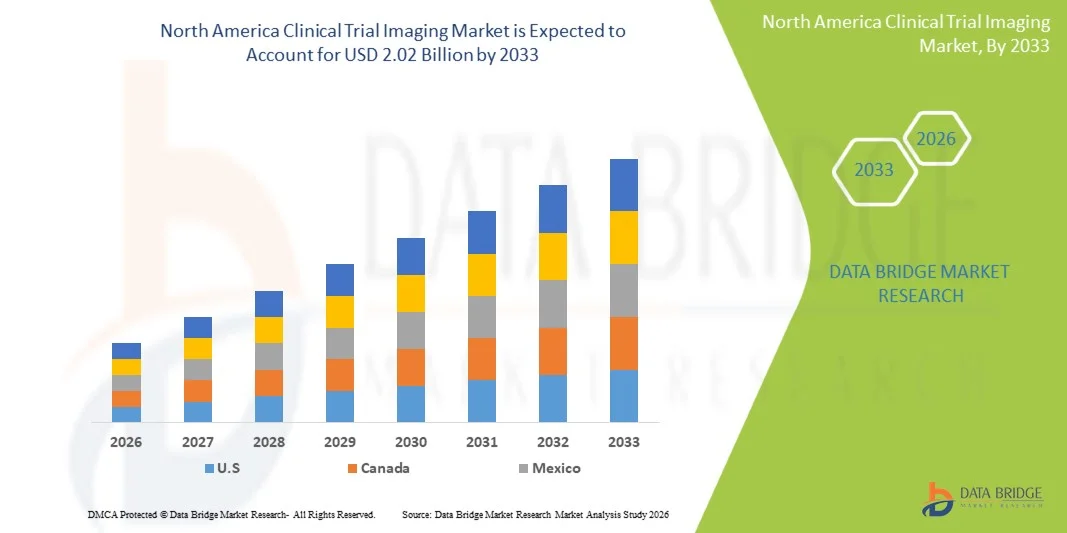

- The North America clinical trial imaging market size was valued at USD 1.07 billion in 2025 and is expected to reach USD 2.02 billion by 2033, at a CAGR of 8.3% during the forecast period

- The market growth is largely fueled by the increasing number of clinical trials, rising prevalence of chronic diseases, and continuous advancements in imaging technologies such as MRI, CT, and PET, leading to greater reliance on imaging endpoints in drug development and clinical research

- Furthermore, growing demand for accurate, standardized, and regulatory-compliant imaging data, along with the expansion of contract research organizations (CROs) and adoption of AI-driven imaging analysis, is establishing clinical trial imaging as a critical component in modern clinical research. These converging factors are accelerating the adoption of advanced imaging solutions, thereby significantly boosting the industry's growth

North America Clinical Trial Imaging Market Analysis

- Clinical trial imaging, involving the use of advanced imaging modalities such as MRI, CT, PET, and ultrasound to support diagnosis, monitoring, and endpoint evaluation in clinical research, has become an essential component of modern drug development and clinical trials due to its ability to provide precise, quantifiable, and reproducible data across study phases

- The escalating demand for clinical trial imaging is primarily fueled by the rising number of clinical trials, increasing prevalence of chronic and complex diseases such as cancer and neurological disorders, and growing reliance on imaging biomarkers for accurate assessment of therapeutic efficacy

- The United States dominated the North America clinical trial imaging with the largest revenue share of 85.2% in 2025, characterized by a well-established clinical research infrastructure, high R&D investments, and the strong presence of pharmaceutical companies and contract research organizations (CROs), with the country experiencing substantial growth in imaging-based trials driven by advancements in AI-powered image analysis and strong regulatory support for innovative therapies

- Canada is expected to be the fastest growing country in the North America clinical trial imaging during the forecast period due to expanding clinical trial activities, improving healthcare infrastructure, and increasing investments from global pharmaceutical companies

- Magnetic Resonance Imaging segment dominated the clinical trial imaging market with a market share of 35.9% in 2025, driven by its superior soft tissue contrast, non-invasive nature, and widespread application in oncology, neurology, and musculoskeletal clinical studies

Report Scope and North America Clinical Trial Imaging Market Segmentation

|

Attributes |

North America Clinical Trial Imaging Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

North America Clinical Trial Imaging Market Trends

“Rising Adoption of AI-Driven Imaging Analytics and Centralized Data Platforms”

- A significant and accelerating trend in the North America clinical trial imaging market is the increasing integration of artificial intelligence (AI) and advanced data analytics platforms with imaging technologies such as MRI, CT, and PET. This convergence is significantly enhancing the accuracy, efficiency, and standardization of imaging data in clinical trials

- For instance, AI-powered imaging platforms are being integrated by contract research organizations (CROs) to automate image analysis and improve endpoint assessment consistency across multi-center trials. Similarly, cloud-based imaging solutions are enabling centralized data storage and real-time collaboration among research teams

- AI integration in clinical trial imaging enables features such as automated lesion detection, quantification of disease progression, and predictive analytics for treatment response. For instance, some imaging software platforms utilize AI algorithms to improve diagnostic accuracy over time and provide intelligent alerts for anomalies in imaging data. Furthermore, advanced analytics capabilities offer researchers the ability to extract deeper insights from large imaging datasets

- The seamless integration of imaging systems with centralized clinical trial management platforms facilitates streamlined workflows and improved data interoperability. Through unified systems, stakeholders can manage imaging data alongside patient records, trial protocols, and regulatory documentation, ensuring efficient trial execution

- This trend towards more intelligent, data-driven, and interconnected imaging solutions is fundamentally reshaping clinical trial methodologies. Consequently, companies such as imaging CROs and technology providers are developing AI-enabled imaging platforms with features such as automated workflows, real-time data access, and enhanced regulatory compliance support

- The demand for clinical trial imaging solutions that offer advanced AI capabilities and seamless data integration is growing rapidly across pharmaceutical and biotechnology sectors, as organizations increasingly prioritize precision, efficiency, and faster drug development timelines

- Growing focus on personalized medicine and biomarker-driven research is encouraging the use of advanced imaging techniques to support patient stratification and targeted therapy development

North America Clinical Trial Imaging Market Dynamics

Driver

“Growing Demand Due to Increasing Clinical Trials and Need for Accurate Imaging Endpoints”

- The increasing number of clinical trials across therapeutic areas, coupled with the rising need for accurate and standardized imaging endpoints, is a significant driver for the heightened demand for clinical trial imaging solutions

- For instance, in March 2025, several clinical research organizations expanded their imaging capabilities to support oncology and neurology trials, focusing on advanced imaging modalities and centralized reading services. Such strategies by key companies are expected to drive the clinical trial imaging market growth in the forecast period

- As pharmaceutical and biotechnology companies intensify their drug development efforts, clinical trial imaging offers critical support through precise disease monitoring, efficacy evaluation, and safety assessment, providing a strong advantage over traditional assessment methods

- Furthermore, the growing complexity of clinical trials and the need for regulatory-compliant imaging data are making imaging solutions an integral component of modern research protocols, ensuring consistency across multi-site studies

- The ability to capture high-resolution images, perform quantitative analysis, and support remote collaboration among stakeholders are key factors propelling the adoption of clinical trial imaging in both academic and commercial research settings. The trend towards decentralized and hybrid clinical trials further contributes to market growth

- Increasing investments in pharmaceutical R&D and the expansion of clinical pipelines across oncology, cardiology, and neurology are further accelerating the demand for imaging services in clinical trials

- The rising role of contract research organizations (CROs) in managing end-to-end clinical trials is also boosting the adoption of outsourced imaging solutions, ensuring efficiency and scalability in trial execution

Restraint/Challenge

“Data Standardization Issues and Regulatory Compliance Hurdles”

- Concerns surrounding the lack of standardized imaging protocols and variability in data acquisition across trial sites pose a significant challenge to broader market adoption. As clinical trial imaging involves multiple stakeholders and technologies, inconsistencies can impact data reliability and trial outcomes

- For instance, differences in imaging equipment, protocols, and interpretation standards across regions have led to variability in imaging results, creating challenges in maintaining uniformity in multi-center trials

- Addressing these challenges through standardized imaging guidelines, advanced quality control measures, and harmonized protocols is crucial for ensuring data consistency and regulatory compliance. Companies are increasingly focusing on centralized reading and validation processes to mitigate variability

- In addition, the relatively high cost of advanced imaging technologies and associated infrastructure can be a barrier to adoption for smaller research organizations and emerging markets, particularly in cost-sensitive environments

- While technological advancements are gradually reducing operational complexities, the need for skilled professionals, compliance with stringent regulatory requirements, and investment in digital infrastructure can still hinder widespread adoption

- Data privacy concerns and strict regulations related to patient information handling, such as compliance with healthcare data protection frameworks, add complexity to imaging data management and sharing

- Limited availability of skilled radiologists and imaging specialists in certain regions can further constrain the efficient interpretation and analysis of complex imaging datasets

- Overcoming these challenges through technological standardization, regulatory alignment, and cost optimization strategies will be vital for sustained market growth

North America Clinical Trial Imaging Market Scope

The market is segmented on the basis of product and services, modality, application, end user, and distributor.

- By Product and Services

On the basis of product and services, the North America clinical trial imaging market is segmented into services and software. The services segment dominated the market with the largest revenue share in 2025, driven by the increasing outsourcing of imaging functions to contract research organizations (CROs) and specialized imaging service providers. Services such as image acquisition, central reading, data management, and quality control are critical for ensuring standardized and regulatory-compliant imaging data across multi-center trials. Pharmaceutical and biotechnology companies prefer outsourcing to reduce operational complexity and improve efficiency in trial execution. In addition, the growing number of global clinical trials and the need for consistent imaging protocols further support the dominance of services. The expertise offered by service providers in handling large imaging datasets and regulatory requirements also contributes to their strong market position.

The software segment is expected to witness the fastest growth rate during the forecast period, fueled by the rising adoption of AI-driven imaging analytics and cloud-based platforms. Advanced imaging software enables automated image processing, quantitative analysis, and real-time data sharing across stakeholders. The increasing use of artificial intelligence for image interpretation and predictive analytics is further accelerating software adoption. In addition, the shift toward decentralized and hybrid clinical trials is boosting demand for digital imaging platforms that support remote access and collaboration. Continuous advancements in imaging informatics and integration with clinical trial management systems are also contributing to the rapid growth of this segment.

- By Modality

On the basis of modality, the market is segmented into computed tomography, magnetic resonance imaging, echocardiography, nuclear medicine, positron emission tomography, X-ray, ultrasound, optical coherence tomography, and others. The magnetic resonance imaging (MRI) segment dominated the market in 2025 with a market share of 35.9%, driven by its superior soft tissue contrast and non-invasive nature. MRI is widely used in oncology, neurology, and musculoskeletal trials due to its ability to provide high-resolution and detailed images. The growing focus on precision medicine and biomarker-based studies further supports the adoption of MRI in clinical trials. In addition, the absence of ionizing radiation makes MRI a preferred choice for longitudinal studies and repeated imaging. Continuous technological advancements, such as functional MRI and advanced imaging sequences, further strengthen its dominance.

The positron emission tomography (PET) segment is expected to be the fastest growing during the forecast period, driven by its increasing use in oncology and neurology trials. PET imaging provides functional and metabolic information, enabling early detection and accurate assessment of disease progression. The rising adoption of PET in combination with CT and MRI for hybrid imaging is further enhancing its clinical value. In addition, the growing demand for imaging biomarkers and targeted therapies is boosting the use of PET in drug development. Technological advancements and increased availability of radiotracers are also contributing to the rapid growth of this segment.

- By Application

On the basis of application, the market is segmented into oncology, neurology, endocrinology, cardiology, dermatology, hematology, and others. The oncology segment dominated the market with the largest share in 2025, driven by the high volume of cancer-related clinical trials and the critical role of imaging in tumor detection, staging, and treatment monitoring. Imaging modalities such as MRI, CT, and PET are extensively used to evaluate therapeutic response and disease progression in oncology studies. The increasing global burden of cancer and rising investments in oncology drug development further support this segment’s dominance. In addition, the growing use of imaging biomarkers and precision medicine approaches is enhancing the importance of imaging in oncology trials. Continuous advancements in imaging technologies are also improving diagnostic accuracy and trial outcomes.

The neurology segment is expected to witness the fastest growth during the forecast period, fueled by the increasing prevalence of neurological disorders such as Alzheimer’s disease and Parkinson’s disease. Imaging plays a crucial role in understanding brain structure and function, supporting early diagnosis and monitoring disease progression. The growing focus on central nervous system (CNS) drug development is driving the demand for advanced imaging techniques. In addition, the adoption of functional imaging and AI-based analysis tools is enhancing the efficiency of neurology trials. Increasing research funding and clinical trial activity in neurology are further contributing to the rapid growth of this segment.

- By End User

On the basis of end user, the market is segmented into pharmaceutical & biotechnology companies, contract research organizations, medical device manufacturers, academic and government research institutes, and others. The pharmaceutical & biotechnology companies segment dominated the market in 2025, driven by their extensive involvement in clinical trials and drug development activities. These companies rely heavily on imaging technologies for evaluating drug efficacy, safety, and disease progression. The increasing number of pipeline drugs and rising R&D investments further contribute to their leading position. In addition, the need for regulatory-compliant imaging data and standardized protocols supports the adoption of imaging services among these companies. Their strong financial capabilities and focus on innovation also drive market growth.

The contract research organizations (CROs) segment is expected to be the fastest growing during the forecast period, fueled by the increasing trend of outsourcing clinical trial operations. CROs offer specialized imaging services, including data management, central reading, and advanced analytics, which enhance trial efficiency and reduce costs. The growing complexity of clinical trials and the need for expertise in imaging further drive the demand for CRO services. In addition, CROs are increasingly adopting AI and digital platforms to improve service delivery. The expansion of global clinical trials and partnerships with pharmaceutical companies are also contributing to the rapid growth of this segment.

- By Distributor

On the basis of distributor, the market is segmented into direct sales and tender sales. The direct sales segment dominated the market in 2025, driven by the strong relationships between imaging solution providers and pharmaceutical companies or CROs. Direct sales allow companies to offer customized imaging solutions and maintain better control over service quality and delivery. In addition, direct engagement facilitates better understanding of client requirements and regulatory needs. The increasing demand for integrated imaging services and long-term contracts further supports the dominance of this segment. Companies also benefit from higher profit margins and improved customer retention through direct sales channels.

The tender sales segment is expected to witness the fastest growth during the forecast period, driven by increasing procurement activities by government institutions and large research organizations. Tender-based procurement ensures transparency and cost-effectiveness, making it a preferred approach for large-scale clinical trials. In addition, the expansion of public-funded research initiatives and collaborations is boosting demand through tender channels. The growing participation of multiple vendors in competitive bidding processes is also driving innovation and cost optimization. Increasing investments in healthcare infrastructure and research facilities further contribute to the rapid growth of this segment.

North America Clinical Trial Imaging Market Regional Analysis

- The United States dominated the North America clinical trial imaging with the largest revenue share of 85.2% in 2025, characterized by a well-established clinical research infrastructure, high R&D investments, and the strong presence of pharmaceutical companies

- Organizations in the country highly value the accuracy, standardization, and regulatory compliance offered by clinical trial imaging solutions, along with their ability to integrate seamlessly with clinical data management systems and trial workflows

- This widespread adoption is further supported by substantial R&D investments, well-established healthcare infrastructure, and a technologically advanced research ecosystem, establishing clinical trial imaging as a critical component for efficient and data-driven drug development across both academic and commercial research settings

U.S. Clinical Trial Imaging Market Insight

The U.S. clinical trial imaging market captured the largest revenue share of 85.2% in 2025 within North America, fueled by the high concentration of clinical trials and the strong presence of pharmaceutical and biotechnology companies. Organizations are increasingly prioritizing accurate and standardized imaging for drug development and regulatory approvals. The growing preference for outsourcing imaging services to specialized providers, combined with robust demand for AI-driven imaging analytics and centralized data platforms, further propels the market. Moreover, the increasing integration of advanced imaging modalities such as MRI, CT, and PET with clinical trial management systems is significantly contributing to the market's expansion.

Canada Clinical Trial Imaging Market Insight

The Canada clinical trial imaging market is projected to expand at a notable CAGR throughout the forecast period, primarily driven by the growing number of clinical trials and supportive government initiatives for healthcare research. The increasing adoption of advanced imaging technologies and the presence of well-established research institutions are fostering market growth. Canadian organizations are also emphasizing high-quality and standardized imaging data to ensure regulatory compliance. The country is witnessing steady growth in oncology and neurology trials, with imaging solutions being widely incorporated across various phases of clinical research.

Mexico Clinical Trial Imaging Market Insight

The Mexico clinical trial imaging market is anticipated to grow at a steady CAGR during the forecast period, driven by the expanding clinical research landscape and increasing investments from global pharmaceutical companies. The country offers cost advantages and a diverse patient population, making it an attractive destination for clinical trials. In addition, improving healthcare infrastructure and rising adoption of digital imaging solutions are supporting market growth. The growing involvement of contract research organizations and increasing focus on regulatory alignment are further contributing to the adoption of clinical trial imaging in Mexico.

North America Clinical Trial Imaging Market Share

The North America Clinical Trial Imaging industry is primarily led by well-established companies, including:

- ICON plc (Ireland)

- Parexel International Corporation (U.S.)

- Medpace Holdings, Inc. (U.S.)

- IXICO plc (U.K.)

- Radiant Sage LLC (U.S.)

- WorldCare Clinical, LLC (U.S.)

- Cardiovascular Imaging Technologies LLC (U.S.)

- Resonance Health Ltd (Australia)

- Navitas Life Sciences (India)

- Imaging Endpoints (U.S.)

- Pharma Imaging Group (U.S.)

- WCG Clinical (U.S.)

- Invicro LLC (U.S.)

- Perspectum Diagnostics Ltd (U.K.)

- Mint Medical GmbH (Germany)

- Medidata Solutions, Inc. (U.S.)

- Prism Clinical Imaging (U.S.)

- Biomedical Systems Corporation (U.S.)

- VirtualScopics, Inc. (U.S.)

- Intrinsic Imaging LLC (U.S.)

What are the Recent Developments in North America Clinical Trial Imaging Market?

- In September 2025, Tempus AI announced that the U.S. Food and Drug Administration (FDA) cleared its AI-powered cardiac imaging platform, Tempus Pixel, designed to enhance cardiac MRI analysis by converting raw imaging data into detailed tissue characterization maps. This advancement enables more precise detection of conditions such as fibrosis and inflammation that are often missed in conventional imaging

- In January 2025, the U.S. Food and Drug Administration (FDA) released draft guidance on the use of artificial intelligence in clinical trials, including imaging-based decision-making. The framework outlines a structured approach for validating AI models used in clinical research, emphasizing transparency, reliability, and regulatory compliance. This development is significant for imaging trials, as AI is increasingly used for image analysis, endpoint assessment, and predictive modeling in drug development

- In September 2024, GE HealthCare received FDA approval for its PET imaging agent Flyrcado, designed for improved detection of coronary artery disease through myocardial perfusion imaging. The diagnostic agent enhances imaging accuracy and workflow efficiency, supporting its use in clinical trials evaluating cardiovascular therapies. Its improved imaging performance and broader accessibility mark a key advancement in imaging-based clinical research in North America

- In April 2023, Proprio, a U.S.-based medical technology company, received FDA 510(k) clearance for its Paradigm surgical imaging platform, which utilizes AI and light-field technology to create real-time 3D visualizations during procedures. This innovation enhances imaging precision and intraoperative decision-making, supporting advanced imaging applications in clinical research and trials. The development underscores the growing integration of AI-enabled imaging technologies in the U.S. healthcare and clinical trial ecosystem

- In October 2021, Medidata, a company of Dassault Systèmes, announced that its Rave Imaging platform surpassed a major milestone by supporting over 1,000 clinical imaging studies globally. The cloud-based platform processes more than 100 million images annually and provides real-time visibility into imaging workflows across trials. This development highlights the growing reliance on centralized imaging platforms to improve efficiency, data consistency, and decision-making in clinical trials

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.