North America Data Center Construction Market

Market Size in USD Billion

CAGR :

%

USD

19.22 Billion

USD

73.72 Billion

2025

2033

USD

19.22 Billion

USD

73.72 Billion

2025

2033

| 2026 –2033 | |

| USD 19.22 Billion | |

| USD 73.72 Billion | |

| % | |

|

North America Data Center Construction Market Size

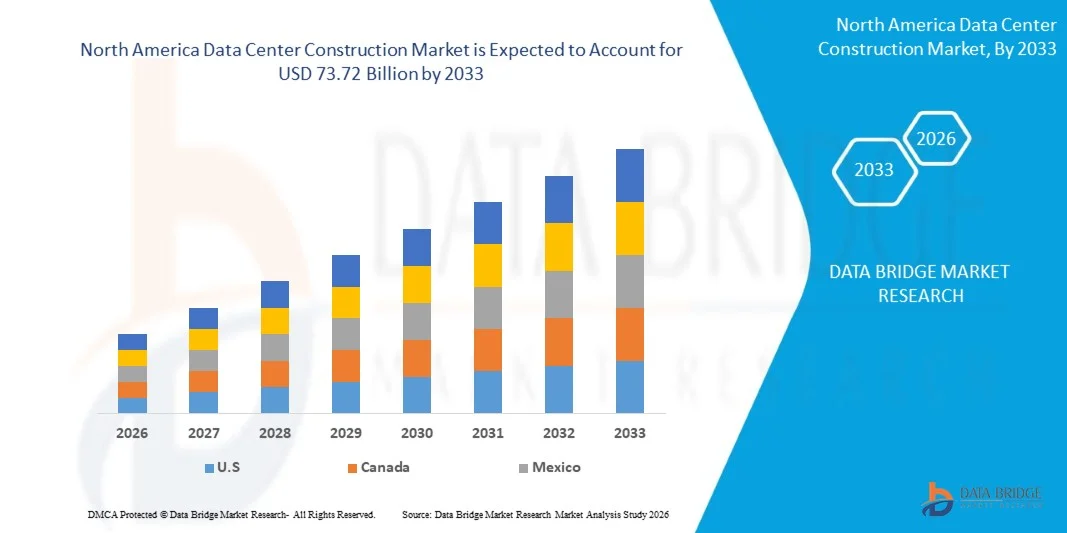

- The North America Data Center Construction Market size was valued at USD 19.22 billion in 2025 and is expected to reach USD 73.72 billion by 2033, at a CAGR of 18.30% during the forecast period

- The market growth is largely fueled by the rapid expansion of cloud computing, artificial intelligence, and big data analytics, which are significantly increasing the demand for high-capacity and scalable data center infrastructure across global enterprises and digital service providers

- Furthermore, rising investments in hyperscale and colocation facilities by technology companies and cloud service providers are accelerating the need for advanced construction solutions that support energy efficiency, high-density computing, and uninterrupted digital operations, thereby significantly boosting the industry's growth

North America Data Center Construction Market Analysis

- Data center construction refers to the planning, design, and building of specialized facilities that house IT infrastructure such as servers, storage systems, and networking equipment to support data processing, storage, and distribution across industries

- The escalating demand for data center construction is primarily fueled by the increasing digitization of businesses, rising internet traffic, expansion of 5G networks, and growing adoption of cloud-based services and AI-driven workloads across multiple end-user industries

- U.S. dominated the North America Data Center Construction Market with the largest share of 80.82% in 2025, due to rapid expansion of hyperscale data centers, strong cloud adoption, and continuous investments in AI-driven computing infrastructure across major technology hubs

- Canada is expected to be the fastest growing country in the North America Data Center Construction Market during the forecast period due to increasing investments in sustainable data center infrastructure, rising cloud adoption, and growing demand for data sovereignty and localized data storage solutions

- Tier 3 segment dominated the market with a market share of 42.14% in 2025, due to its balanced combination of high availability, redundancy, and cost efficiency suitable for enterprise and colocation facilities. Organizations prefer Tier 3 facilities due to their ability to provide concurrent maintainability without major downtime, making them ideal for mission-critical workloads

Report Scope and North America Data Center Construction Market Segmentation

|

Attributes |

Data Center Construction Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

North America Data Center Construction Market Trends

“Rapid Expansion of Hyperscale and AI-Driven Data Center Facilities”

- A significant trend in the North America Data Center Construction Market is the rapid expansion of hyperscale and AI-driven data center facilities, driven by the growing demand for high-performance computing, cloud services, and large-scale data processing capabilities across global enterprises. This expansion is reshaping construction strategies with a strong focus on scalable architecture, high-density rack systems, and advanced cooling and power infrastructure

- For instance, Microsoft Corporation and Amazon Web Services are continuously expanding hyperscale data center campuses across the U.S. and Europe to support increasing AI workloads and cloud computing demand. These developments are strengthening infrastructure scalability and enabling faster deployment of digital services across industries

- The rise of AI model training and generative AI applications is significantly increasing the need for specialized data centers designed to handle extreme computational loads. This is accelerating the shift toward AI-optimized infrastructure that integrates advanced GPUs, high-speed interconnects, and enhanced thermal management systems

- The expansion of cloud service providers such as Google Cloud is further driving demand for large-scale facilities capable of supporting global workloads with minimal latency. This is influencing construction firms to adopt modular and prefabricated designs for faster deployment and improved operational efficiency

- Industries including BFSI, healthcare, and telecommunications are increasingly relying on hyperscale facilities to manage growing data volumes and real-time processing requirements. This is reinforcing the importance of large, energy-efficient, and highly resilient data center infrastructures across markets

- The market is witnessing a structural shift toward AI-ready and hyperscale construction models that prioritize scalability, automation, and sustainability. This ongoing transformation is positioning hyperscale data centers as the backbone of global digital infrastructure expansion

North America Data Center Construction Market Dynamics

Driver

“Rising Demand for Cloud Computing, AI, and Big Data Workloads”

- The rising demand for cloud computing, artificial intelligence, and big data workloads is a key driver in the North America Data Center Construction Market, as enterprises increasingly depend on high-capacity digital infrastructure for data storage, processing, and analytics. This surge in digital workloads is accelerating investments in new data center facilities and expansion of existing infrastructure across global regions

- For instance, Oracle Corporation and Meta Platforms are expanding their data center infrastructure to support AI model training, cloud services, and large-scale data analytics. These investments are enabling improved computing performance and supporting growing enterprise demand for scalable digital ecosystems

- The increasing adoption of cloud-based enterprise solutions is driving the need for robust and geographically distributed data centers to ensure low latency and high availability of services. This is encouraging construction of advanced facilities equipped with high-speed networking and redundant systems

- The rapid growth of big data analytics across industries such as retail, BFSI, and healthcare is further fueling demand for high-performance computing environments. This is pushing data center developers to design facilities capable of handling massive data processing requirements efficiently

- The sustained growth in digital transformation initiatives across enterprises continues to strengthen this driver. The increasing reliance on cloud ecosystems and data-intensive applications is reinforcing the need for continuous data center construction and modernization

Restraint/Challenge

“High Capital Investment and Energy Consumption Constraints”

- The high capital investment and energy consumption constraints represent a major challenge in the North America Data Center Construction Market, as building and operating advanced facilities require substantial financial resources and long-term operational expenditure commitments. The rising complexity of infrastructure design further increases overall project costs and limits accessibility for smaller operators

- For instance, hyperscale projects by companies such as Google LLC and Microsoft Corporation involve multi-billion-dollar investments to develop energy-intensive facilities equipped with advanced cooling and power systems. These large-scale investments highlight the significant financial burden associated with modern data center development

- The continuous need for uninterrupted power supply, backup systems, and advanced cooling technologies leads to high energy consumption levels in data center operations. This creates pressure on operators to manage operational costs while maintaining efficiency and reliability

- The increasing adoption of AI and high-performance computing further intensifies energy demand, requiring more robust infrastructure to support thermal management and power distribution. This raises both construction complexity and long-term sustainability concerns

- The market continues to face constraints related to balancing infrastructure expansion with cost efficiency and environmental sustainability. These challenges are compelling stakeholders to focus on innovative design approaches and energy optimization strategies to support long-term growth

North America Data Center Construction Market Scope

The market is segmented on the basis of infrastructure type, data center type, organization size, and vertical.

•By Infrastructure Type

On the basis of infrastructure type, the North America Data Center Construction Market is segmented into electrical infrastructure, mechanical infrastructure, and general construction. The electrical infrastructure segment dominated the largest market revenue share in 2025, driven by the rising deployment of high-capacity power systems, backup solutions, and advanced power distribution units required to support energy-intensive data center operations. Growing demand for uninterrupted power supply, efficient load management, and integration of renewable energy sources further strengthens the dominance of this segment. Increasing investments in UPS systems, switchgear, and power monitoring solutions across hyperscale and enterprise data centers continues to support market expansion. The segment concludes strong growth due to its critical role in ensuring operational reliability and uptime in data center environments

The mechanical infrastructure segment is anticipated to witness the fastest growth rate from 2026 to 2033, driven by the rising need for advanced cooling systems to manage increasing heat loads from high-density computing environments. Rapid adoption of liquid cooling, precision air conditioning, and energy-efficient HVAC systems supports this growth. For instance, companies such as Schneider Electric are actively developing advanced thermal management solutions for modern data centers. Increasing focus on sustainability and reducing power usage effectiveness also accelerates the shift toward innovative mechanical infrastructure solutions.

•By Data Center Type

On the basis of data center type, the market is segmented into Tier 1, Tier 2, Tier 3, and Tier 4. The Tier 3 segment dominated the largest market revenue share of 42.14% in 2025, driven by its balanced combination of high availability, redundancy, and cost efficiency suitable for enterprise and colocation facilities. Organizations prefer Tier 3 facilities due to their ability to provide concurrent maintainability without major downtime, making them ideal for mission-critical workloads. Strong adoption across BFSI, IT, and telecom sectors further reinforces the dominance of this segment. The segment concludes its leadership as it offers an optimal balance between infrastructure investment and operational reliability.

The Tier 4 segment is anticipated to witness the fastest growth rate from 2026 to 2033, driven by increasing demand for ultra-high availability infrastructure supporting hyperscale cloud providers and mission-critical applications. These facilities offer fully fault-tolerant systems with maximum redundancy, ensuring near-zero downtime operations. Rising investments from global cloud service providers and AI-driven workloads further boost adoption. Growing emphasis on resilience and continuous uptime in digital-first enterprises accelerates the expansion of Tier 4 data center construction.

•By Organization Size

On the basis of organization size, the North America Data Center Construction Market is segmented into small size organizations, medium size organizations, and large size organizations. The large size organizations segment dominated the largest market revenue share in 2025, driven by extensive investments in hyperscale data centers and private cloud infrastructure. These organizations require large-scale computing capacity, advanced storage systems, and highly secure environments to support global operations. Strong financial capability and continuous expansion of digital ecosystems further strengthen this segment’s dominance. The segment concludes its leadership due to sustained investments in large, high-performance data center facilities.

The small size organizations segment is anticipated to witness the fastest growth rate from 2026 to 2033, driven by increasing adoption of cloud services and colocation facilities that reduce the need for in-house infrastructure. Growing digital transformation among SMEs and startups supports demand for scalable and cost-effective data center solutions. For instance, many emerging businesses are leveraging managed hosting services from providers such as Equinix to access enterprise-grade infrastructure. Rising awareness of data security and operational efficiency further accelerates growth in this segment.

•By Vertical

On the basis of vertical, the North America Data Center Construction Market is segmented into banking, financial services and insurance, IT and telecommunications, government and defense, healthcare, retail colocation, power and energy, manufacturing, and others. The BFSI segment dominated the largest market revenue share in 2025, driven by the increasing need for secure, high-performance, and low-latency data processing systems. Financial institutions require robust data centers to manage digital transactions, risk analytics, and regulatory compliance workloads. Strong emphasis on data security and uninterrupted service delivery further reinforces the dominance of this segment. The segment concludes its leading position due to continuous digital banking expansion and rising fintech adoption.

The IT and telecommunications segment is anticipated to witness the fastest growth rate from 2026 to 2033, driven by rapid expansion of cloud computing, 5G deployment, and data-intensive applications. Increasing demand for edge computing infrastructure and high-speed connectivity supports the growth of data center construction in this vertical. Rising investments from telecom operators and cloud service providers further accelerate infrastructure development. Growing digital consumption and real-time data processing requirements continue to drive strong expansion in this segment.

North America Data Center Construction Market Regional Analysis

- U.S. dominated the North America Data Center Construction Market with the largest revenue share of 80.82% in 2025, driven by rapid expansion of hyperscale data centers, strong cloud adoption, and continuous investments in AI-driven computing infrastructure across major technology hubs

- The demand for data center construction is further supported by continuous expansion initiatives and technological advancements by companies such as Microsoft Corporation and Amazon Web Services, focusing on large-scale hyperscale campuses and energy-efficient facility designs integrated with renewable energy and advanced cooling systems

- The presence of leading cloud service providers, strong digital transformation initiatives, and rising deployment of edge computing networks reinforce the U.S. leadership position in the North America market

Canada North America Data Center Construction Market Insight

Canada is projected to register the fastest CAGR in the North America Data Center Construction Market from 2026 to 2033, supported by increasing investments in sustainable data center infrastructure, rising cloud adoption, and growing demand for data sovereignty and localized data storage solutions. Favorable climate conditions for energy-efficient cooling and supportive government initiatives for green data center development are further accelerating market expansion. Growth is further supported by investments and expansion activities from companies such as Equinix Inc. and Digital Realty Trust, focusing on colocation facilities, low-carbon operations, and advanced connectivity infrastructure across key Canadian cities. Increasing focus on renewable energy integration, rising hyperscale cloud deployments, and strong demand from IT and telecom sectors position Canada as the fastest-growing country in the region during the forecast period.

Mexico North America Data Center Construction Market Insight

Mexico is expected to grow steadily from 2026 to 2033, driven by increasing foreign direct investments in digital infrastructure, expanding cloud service penetration, and rising demand for cost-effective data center facilities supporting regional enterprise operations. Growing digitalization across manufacturing, retail, and telecom sectors further supports the need for scalable data center capacity and improved connectivity infrastructure. Market development is further strengthened by infrastructure expansion initiatives and partnerships involving global players such as IBM Corporation and KIO Networks, focusing on colocation services, network expansion, and improved data handling capabilities across major urban and industrial regions. Rising adoption of cloud-based services, increasing data traffic, and continued investments in telecommunications infrastructure contribute to sustained growth of the North America Data Center Construction Market throughout the forecast period.

North America Data Center Construction Market Share

The data center construction industry is primarily led by well-established companies, including:

- Turner Construction Company (U.S.)

- DPR Construction (U.S.)

- AECOM (U.S.)

- Schneider Electric (France)

- M. A. Mortenson Company (U.S.)

- Arup (U.K.)

- Brasfield & Gorrie, L.L.C. (U.S.)

- CORGAN (U.S.)

- Currie & Brown Holdings Limited (U.K.)

- Fortis Construction (U.S.)

- Gensler (U.S.)

- Holder Construction Group, LLC (U.S.)

- Jacobs (U.S.)

- ROGERS-O’BRIEN CONSTRUCTION COMPANY, LTD (U.S.)

- Skanska (Sweden)

- Structure Tone Organization (U.S.)

- The Boldt Company (U.S.)

Latest Developments in North America Data Center Construction Market

- In February 2026, Compass Datacenters committed USD 10 billion to develop a 2 GW hyperscale data center campus in Mississippi integrated with on-site solar generation and battery storage systems, significantly strengthening the North America Data Center Construction Market by accelerating the shift toward sustainable and energy-resilient infrastructure. The large-scale investment is expected to enhance regional capacity for high-performance computing workloads while reducing dependency on conventional grid power, thereby improving operational efficiency and long-term cost stability for hyperscale operators

- In February 2026, Centersquare announced a 1 GW data center development project in Texas with an accelerated rollout plan for the first 200 MW phase within 24 months, reinforcing strong momentum in the North America Data Center Construction Market driven by rapid demand for scalable colocation and cloud infrastructure. The project highlights growing investor confidence in high-capacity facilities across key U.S. hubs, supporting improved latency performance, enhanced connectivity, and faster deployment of digital services for enterprise and cloud customers

- In February 2025, Cisco Systems Inc. announced an expanded strategic collaboration with NVIDIA to develop integrated AI infrastructure solutions for enterprise data centers, strengthening the North America Data Center Construction Market by enabling more efficient design of AI-ready facilities. The partnership focuses on combining advanced networking and AI computing platforms to deliver high-performance, low-latency, and energy-efficient infrastructure across hybrid environments, supporting the growing demand for scalable AI workloads and accelerating modernization of enterprise data center architectures

- In April 2025, Fujitsu announced a joint initiative with Supermicro and Nidec to reduce data center energy consumption through advanced cooling technologies, positively impacting the North America Data Center Construction Market by promoting the development of more energy-efficient facility designs. The collaboration integrates liquid-cooling monitoring software, high-performance GPU server platforms, and advanced cooling systems to lower power usage effectiveness, enabling operators to improve sustainability, reduce operational costs, and enhance thermal management in high-density computing environments

- In December 2025, ABB announced the acquisition of UK-based IPEC to enhance its digital power management capabilities, strengthening the North America Data Center Construction Market by advancing real-time monitoring and predictive maintenance of critical electrical infrastructure. The integration of AI-driven analytics for high-voltage asset monitoring is expected to improve operational reliability, reduce downtime risks, and prevent significant financial losses, thereby supporting more resilient and efficient power systems for data centers and other mission-critical industries

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

North America Data Center Construction Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its North America Data Center Construction Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as North America Data Center Construction Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.