North America Dental 3d Printing Market

Market Size in USD Billion

USD

1.81 Billion

USD

10.14 Billion

2025

2033

USD

1.81 Billion

USD

10.14 Billion

2025

2033

| 2026 - 2033 | |

| USD 1.81 Billion | |

| USD 10.14 Billion | |

| % | |

|

North America Dental 3-Dimensional (3D) Printing Market Overview

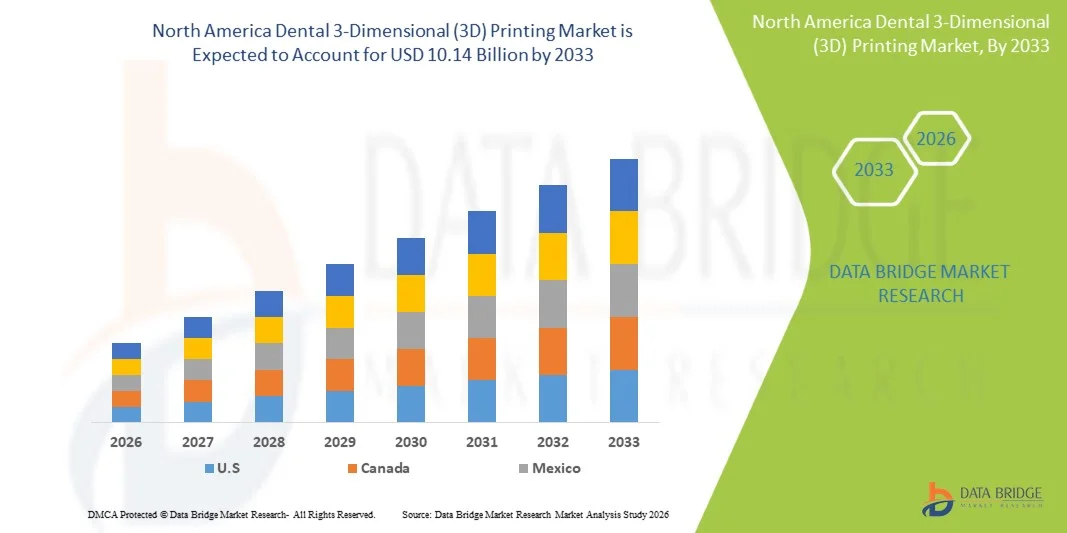

The North America Dental 3-Dimensional (3D) Printing market was valued at USD 1.81 billion in 2025 and is projected to reach USD 10.14 billion by 2033, growing at a CAGR of 24.04% from 2026 to 2033. The Dental 3-Dimensional (3D) Printing market is experiencing consistent growth driven by rising demand for customized dental solutions, rapid advancements in additive manufacturing technologies, and expanding applications across restorative dentistry, orthodontics, prosthodontics, and implantology.

The increasing adoption of digital dentistry workflows, combined with growing demand for personalized dental treatments and faster production of dental restorations, is encouraging dental clinics, laboratories, and manufacturers to integrate advanced 3D printing technologies. Resin-based printing, selective laser sintering (SLS), and digital light processing (DLP) technologies are replacing traditional manufacturing methods in many markets, offering cost-effective, accurate, and patient-specific solutions for crowns, bridges, aligners, surgical guides, and dental models. In addition, advancements in biocompatible materials, AI-enabled design software, and CAD/CAM integration are further accelerating the adoption of dental 3D printing solutions globally.

Key Market Trends & Insights

- The U.S. dominated the North America Dental 3-Dimensional (3D) Printing market with the largest revenue share of 62.74% in 2025, supported by strong adoption of digital dentistry workflows, advanced healthcare infrastructure, and increasing investments in dental additive manufacturing technologies. The country’s well-established dental care ecosystem, presence of leading dental technology companies, and rising demand for customized dental restorations, implants, aligners, and surgical guides are accelerating the adoption of 3D printing solutions across dental laboratories, clinics, and academic institutions. Furthermore, increasing integration of CAD/CAM systems, intraoral scanning, and advanced dental materials is strengthening market growth across prosthodontics, implantology, orthodontics, and oral & maxillofacial surgery applications.

- The System segment dominated the market with a 68.42% share in 2025, owing to the increasing adoption of advanced dental 3D printing systems across dental laboratories, hospitals, and clinics for manufacturing customized dental restorations, implants, surgical guides, and orthodontic devices.

- Canada is expected to be the fastest-growing market in North America at a CAGR of 8.3% from 2026 to 2033, fueled by increasing adoption of digital dentistry, rising investments in dental healthcare infrastructure, and growing demand for personalized dental treatment solutions. The country’s expanding dental laboratory network, increasing use of CAD/CAM technologies, and growing acceptance of additive manufacturing in restorative and implant dentistry are supporting market expansion. In addition, rising focus on advanced dental education, technology-driven treatment approaches, and collaboration with global dental technology providers is further accelerating the adoption of dental 3D printing technologies across Canada.

- Polymer materials dominated the material category with a 46.35% revenue share in 2025, supported by widespread use in dental models, aligners, temporary restorations, surgical guides, and prosthodontic applications due to cost-effectiveness, flexibility, and compatibility with digital dental workflows.

- Dental Laboratories represented the leading end-user segment with a 44.21% market share in 2025, owing to increasing adoption of digital manufacturing systems, faster turnaround times, and rising demand for customized dental products. Dental laboratories are increasingly integrating 3D printing into workflows to improve production efficiency and reduce material wastage.

- Direct Tenders remained a significant distribution channel with share in 2025, supported by procurement activities from large dental hospitals, academic institutions, and healthcare organizations seeking advanced dental 3D printing systems through direct manufacturer partnerships.

Market Size & Forecast

- North America Market Value (2025): USD 1.81 Billion

- Expected Market Value (2033): USD 10.14 Billion

- Forecast CAGR (2026–2033): 24.04%

- Leading Region in 2025: U.S.

- Fastest Growing Region: Canada

Report Scope and North America Dental 3-Dimensional (3D) Printing Market Segmentation

|

Attributes |

Dental 3-Dimensional (3D) Printing Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Mexico · Canada |

|

Key Market Players |

• 3D Systems Corporation (U.S.) |

|

Market Opportunities |

· Growing Adoption of Digital Dentistry and Customized Dental Solutions · Increasing Demand for Personalized Orthodontic and Implant Applications · Integration of Advanced Materials and AI-Based Dental Design Technologies |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

North America Dental 3-Dimensional (3D) Printing Market Trends

Trend: Growth in Digital Dentistry and Customized Dental Manufacturing

Dental laboratories, clinics, and academic institutions across North America are increasingly adopting Dental 3-Dimensional (3D) Printing technologies to improve the speed, accuracy, and customization of dental restorations and devices. The transition from traditional manufacturing methods toward digital dentistry workflows, including intraoral scanning, CAD/CAM design, and additive manufacturing, is accelerating the adoption of 3D printing for crowns, bridges, aligners, dentures, surgical guides, and implant planning. The growing demand for patient-specific dental solutions is encouraging the use of advanced materials such as dental polymers, resins, ceramics, and metals. Countries including the U.K., Germany, and Switzerland are witnessing increased integration of 3D printing systems within dental laboratories to reduce production time, improve precision, and enhance workflow efficiency. For instance, dental 3D printing is increasingly being used for orthodontic aligner production, where digital models allow manufacturers to rapidly produce customized treatment devices for individual patients.

North America Dental 3-Dimensional (3D) Printing Market Dynamics

Key Market Driver: Increasing Adoption of Digital Dentistry and Personalized Dental Solutions

The rising demand for customized dental treatments and minimally invasive procedures is a major driver for the North America Dental 3-Dimensional (3D) Printing market. Dental 3D printing enables faster production of highly accurate patient-specific products, including prosthetics, implants, orthodontic devices, and surgical planning models. The increasing prevalence of dental disorders, growing aging population, and rising demand for cosmetic dentistry are encouraging dental clinics and laboratories to invest in advanced digital manufacturing technologies. European countries are also benefiting from strong healthcare infrastructure and widespread adoption of CAD/CAM dentistry solutions. For instance, leading dental technology companies such as Straumann Group and 3D Systems have continued developing digital dental workflows and additive manufacturing solutions to support restorative dentistry, implantology, and orthodontic applications. The growing adoption of 3D printing in dental laboratories is helping reduce material waste, improve production efficiency, and shorten turnaround times.

Key Restraint/Challenge: High Equipment Costs and Limited Adoption Among Small Dental Practices

A significant challenge in the North America Dental 3-Dimensional (3D) Printing market is the high initial investment required for advanced printing systems, specialized dental materials, and supporting digital infrastructure. Professional dental 3D printers often require integration with scanners, design software, post-processing equipment, and skilled operators, increasing the overall cost of implementation. Small dental clinics and laboratories may face difficulties in adopting these technologies due to equipment costs, maintenance requirements, and the need for trained professionals capable of managing digital workflows. In addition, regulatory requirements for dental materials and medical-grade devices can increase product approval timelines and operational complexity. For instance, high-precision dental applications such as implant components and surgical guides require strict quality control, validated materials, and accurate printing processes, creating additional barriers for smaller organizations transitioning from conventional manufacturing methods.

Key Market Opportunity: Integration of AI, Automation, and Advanced Materials in Dental 3D Printing

The integration of artificial intelligence, automation, and advanced biomaterials presents significant growth opportunities for the North America Dental 3-Dimensional (3D) Printing market. AI-driven dental design platforms can improve treatment planning, automate restoration design, and enhance workflow efficiency by analyzing digital scans and patient-specific data. The development of advanced materials such as biocompatible polymers, ceramic composites, and metal alloys is expanding the application scope of dental 3D printing across implantology, prosthodontics, and oral surgery. In addition, cloud-based dental design platforms are enabling collaboration between dentists, laboratories, and manufacturers, improving access to digital dental solutions. The increasing focus on personalized healthcare, expansion of dental CAD/CAM adoption, and growing investments in digital healthcare infrastructure across North America are expected to accelerate the adoption of next-generation Dental 3-Dimensional (3D) Printing technologies.

North America Dental 3-Dimensional (3D) Printing Market Scope

The Dental 3-Dimensional (3D) Printing market is segmented on the basis of product, material, technology, application, end user, and distribution channel.

- By Product

On the basis of product, the North America Dental 3-Dimensional (3D) Printing market is segmented into systems and accessories. The System segment dominated the market with a 68.42% share in 2025, owing to the increasing adoption of advanced dental 3D printing systems across dental laboratories, hospitals, and clinics for manufacturing customized dental restorations, implants, surgical guides, and orthodontic devices. These systems provide high accuracy, faster production cycles, reduced material wastage, and improved workflow efficiency compared with conventional dental manufacturing methods. The increasing shift toward digital dentistry, CAD/CAM integration, and computer-aided treatment planning is significantly supporting the adoption of dental 3D printing systems. In addition, growing demand for personalized dental solutions, increasing prevalence of dental disorders, and rising investments in dental automation technologies are driving segment growth. Dental professionals are increasingly adopting advanced printing systems to improve treatment precision, enhance patient outcomes, and reduce turnaround time. The expansion of dental laboratories equipped with digital manufacturing capabilities across North America is further strengthening the dominance of this segment. Furthermore, continuous technological advancements, improved printer speed, and development of high-resolution printing systems are increasing adoption among professional users.

The Accessories segment is expected to witness the fastest CAGR of 9.1% from 2026 to 2033, driven by increasing demand for dental printing consumables, replacement components, software upgrades, and post-processing equipment required for continuous operation of 3D printing systems. The growing installation base of dental printers across laboratories and clinics is creating recurring demand for accessories such as printing materials, build platforms, cartridges, and maintenance components. Increasing utilization of multiple dental materials for different applications, including orthodontics, prosthodontics, and implantology, is further supporting segment expansion. In addition, manufacturers are focusing on developing advanced accessories that improve printing efficiency, accuracy, and workflow optimization. The rising adoption of digital dental workflows and increasing frequency of dental restoration procedures are creating significant growth opportunities. Furthermore, increasing demand for customized dental production and continuous innovation in accessory designs are expected to accelerate market growth during the forecast period.

- By Material

On the basis of material, the North America Dental 3-Dimensional (3D) Printing market is segmented into polymer, metal, ceramics, plastic, and others. The Polymer segment dominated the market with a 52.36% share in 2025, due to its widespread utilization in dental applications such as aligners, dental models, temporary crowns, surgical guides, and prosthetic components. Polymer materials are preferred because of their cost-effectiveness, lightweight properties, flexibility, and compatibility with advanced printing technologies including stereolithography (SLA) and digital light processing (DLP). The increasing adoption of customized dental solutions and rapid prototyping applications is significantly driving polymer material demand. In addition, the availability of various dental-grade resins with improved strength, durability, and biocompatibility is expanding their application scope. Dental laboratories and clinics are increasingly adopting polymer-based printing materials due to their ability to produce highly accurate and patient-specific dental products. The growing preference for affordable and efficient dental treatment solutions is further supporting segment dominance. Moreover, continuous advancements in resin formulations and improved material performance are enhancing adoption across Europe.

The Ceramics segment is expected to witness the fastest CAGR of 8.7% from 2026 to 2033, driven by increasing demand for aesthetic, durable, and biocompatible dental restoration solutions. Ceramic materials are gaining popularity in crowns, bridges, implants, and prosthetic applications due to their natural appearance and superior mechanical properties. The rising preference for long-lasting dental treatments and improved aesthetic outcomes is encouraging adoption of ceramic-based 3D printing materials. Advancements in ceramic printing technologies are enabling production of complex dental structures with higher precision and efficiency. In addition, increasing investments in research and development of advanced ceramic materials are creating new opportunities for manufacturers. The growing adoption of digital dentistry workflows and increasing demand for premium dental restorations are further accelerating market growth. Furthermore, improvements in ceramic processing techniques and reduced production limitations are expected to support rapid segment expansion.

- ByTechnology

On the basis of technology, the North America Dental 3-Dimensional (3D) Printing market is segmented into Light Curing, Powder Bed Fusion (PBF), and Fused Deposition Modelling (FDM). The Light Curing segment dominated the market with a 57.84% share in 2025, owing to its extensive application in producing dental models, aligners, crowns, bridges, and surgical guides. Light curing technologies such as SLA and DLP provide superior surface quality, high precision, and faster production compared with traditional dental manufacturing processes. The increasing adoption of digital dentistry solutions and integration of CAD/CAM technologies are supporting segment growth. Dental professionals prefer light curing technologies due to their ability to process advanced dental resins and produce highly detailed structures. In addition, growing demand for customized dental treatments and faster restoration production is increasing adoption across laboratories and clinics. The availability of affordable and efficient light curing printers is further expanding accessibility. Increasing investments by dental technology companies in improving printing accuracy and speed are strengthening segment leadership.

The Powder Bed Fusion (PBF) segment is expected to witness the fastest CAGR of 9.4% from 2026 to 2033, driven by increasing adoption in metal-based dental applications such as implants, frameworks, and complex prosthetic structures. PBF technology enables production of strong, durable, and highly customized dental components using advanced materials. Growing demand for personalized implant solutions and precision dental manufacturing is accelerating adoption. In addition, improvements in metal printing technologies and increased availability of dental-grade powders are supporting market expansion. The rising need for patient-specific solutions and advanced restorative procedures is creating significant opportunities for PBF technology providers. Furthermore, increasing investments in dental research and development activities are expected to enhance technology adoption during the forecast period.

North America Dental 3-Dimensional (3D) Printing Market Regional Analysis

The North America Dental 3-Dimensional (3D) Printing market remains a major contributor to the global dental additive manufacturing industry, driven by increasing adoption of digital dentistry workflows, advanced dental technologies, and rising demand for customized patient-specific dental solutions. The region benefits from well-established healthcare infrastructure, strong presence of dental technology providers, and widespread utilization of CAD/CAM systems, intraoral scanners, and additive manufacturing technologies across dental laboratories, hospitals, clinics, and academic research institutes. Increasing demand for customized dental restorations, orthodontic aligners, implant planning models, surgical guides, and prosthodontic solutions is supporting market expansion across North America. Furthermore, advancements in biocompatible materials, automation, artificial intelligence integration, and digital dental manufacturing processes are further strengthening the adoption of Dental 3D Printing technologies throughout the region.

U.S. Dental 3-Dimensional (3D) Printing Market Insight

The U.S. dominated the North America Dental 3-Dimensional (3D) Printing market with the largest revenue share of 62.74% in 2025, supported by strong adoption of digital dentistry workflows, advanced healthcare infrastructure, and increasing investments in dental additive manufacturing technologies. The country’s well-established dental care ecosystem, presence of leading dental technology companies, and rising demand for customized dental restorations, implants, aligners, and surgical guides are accelerating the adoption of 3D printing solutions across dental laboratories, clinics, and academic institutions. Furthermore, increasing integration of CAD/CAM systems, intraoral scanning technologies, and advanced dental materials is strengthening market growth across prosthodontics, implantology, orthodontics, and oral & maxillofacial surgery applications. The growing preference for faster treatment planning, improved accuracy, and personalized dental procedures is further supporting the expansion of dental 3D printing adoption across the U.S. market.

Canada Dental 3-Dimensional (3D) Printing Market Insight

The Canada Dental 3-Dimensional (3D) Printing market is expected to be the fastest-growing market in North America at a CAGR of 8.3% from 2026 to 2033, fueled by increasing adoption of digital dentistry, rising investments in dental healthcare infrastructure, and growing demand for personalized dental treatment solutions. The country’s expanding dental laboratory network, increasing use of CAD/CAM technologies, and growing acceptance of additive manufacturing in restorative and implant dentistry are supporting market expansion. Dental clinics and laboratories are increasingly adopting 3D printing solutions for customized prosthetics, crowns, bridges, orthodontic devices, and surgical planning applications to enhance efficiency and treatment outcomes. Additionally, rising focus on advanced dental education, technology-driven treatment approaches, and collaborations with global dental technology providers are further accelerating the adoption of dental 3D printing technologies across Canada.

North America Dental 3-Dimensional (3D) Printing Market Share

The Dental 3-Dimensional (3D) Printing industry is primarily led by well-established companies, including:

- 3D Systems Corporation (U.S.)

- Formlabs Inc. (U.S.)

- EnvisionTEC GmbH (Germany)

- Desktop Metal, Inc. (U.S.)

- Carbon, Inc. (U.S.)

- EOS GmbH (Germany)

- Renishaw plc (UK)

- Prodways Group (France)

- SprintRay Inc. (U.S.)

- Asiga (Australia)

- Roland DG Corporation (Japan)

- Dentsply Sirona Inc. (U.S.)

- Align Technology, Inc. (U.S.)

- Ivoclar Vivadent AG (Liechtenstein)

- Planmeca Oy (Finland)

- SHINING 3D Tech Co., Ltd. (China)

- Zortrax S.A. (Poland)

- Anycubic Technology Co., Ltd. (China)

- Ultimaker B.V. (Netherlands)

- Raise3D Technologies, Inc. (U.S.)

- GE Additive (U.S.)

- Materialise NV (Belgium)

- ExOne Company (U.S.)

- Nexa3D Inc. (U.S.)

- Voxeljet AG (Germany)

- Kulzer GmbH (Germany)

- 3Shape A/S (Denmark)

- Carestream Dental LLC (U.S.)

- Formlabs Dental (U.S.)

- Straumann Group (Switzerland)

- BEGO GmbH & Co. KG (Germany)

- Amann Girrbach AG (Austria)

- W2P Engineering GmbH (Germany)

- Rapid Shape GmbH (Germany)

Latest Developments in North America Dental 3-Dimensional (3D) Printing Market

- In March 2021, Stratasys Ltd., a leading provider of polymer 3D printing solutions, announced the launch of its J5 DentaJet 3D printer, a multi-material dental 3D printing system designed for dental laboratories. The system enables the production of highly detailed dental models, guides, and restorations using multiple materials in a single print cycle. The J5 DentaJet improves workflow efficiency, reduces manual processing requirements, and supports digital dentistry applications such as implantology, orthodontics, and prosthodontics, strengthening Stratasys’ position in the dental 3D printing market

- In April 2022, 3D Systems expanded its dental 3D printing capabilities through advancements in its NextDent portfolio, focusing on biocompatible dental materials and digital manufacturing solutions. The company continued enhancing its NextDent materials ecosystem to support applications including dentures, surgical guides, orthodontic models, and temporary restorations. These developments supported the increasing adoption of additive manufacturing technologies in dental laboratories seeking faster production and customized patient-specific solutions

- In January 2024, Formlabs introduced its Resin Pumping System and Premium Teeth Resin solutions for dental applications, aimed at improving workflow efficiency and supporting high-volume dental production. The resin delivery system was designed to reduce resin changeovers and packaging waste while enabling continuous printing operations, helping dental laboratories improve productivity and scalability in digital dentistry workflows

- In April 2024, Formlabs launched the Form 4 resin 3D printer featuring its Low Force Display (LFD) print engine, offering significantly faster printing speeds compared with previous generations. The system enabled dental professionals and laboratories to produce dental parts, models, and appliances more efficiently while maintaining accuracy and surface quality. This launch highlighted the growing shift toward faster, high-precision chairside and laboratory-based dental 3D printing solutions

- In June 2024, 3D Systems announced a major expansion in the dental market after securing a large-scale contract related to clear dental aligner production. The agreement supported the company’s strategy to advance direct 3D printing technologies for orthodontic applications and accelerate commercialization of next-generation dental manufacturing solutions. The development reflected increasing demand for customized orthodontic products produced through digital workflows and additive manufacturing

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.