North America Geotechnical Instrumentation And Monitoring Market

Market Size in USD Billion

CAGR :

%

USD

4.54 Billion

USD

12.70 Billion

2025

2033

USD

4.54 Billion

USD

12.70 Billion

2025

2033

| 2026 –2033 | |

| USD 4.54 Billion | |

| USD 12.70 Billion | |

| % | |

|

North America Geotechnical Instrumentation and Monitoring Market Size

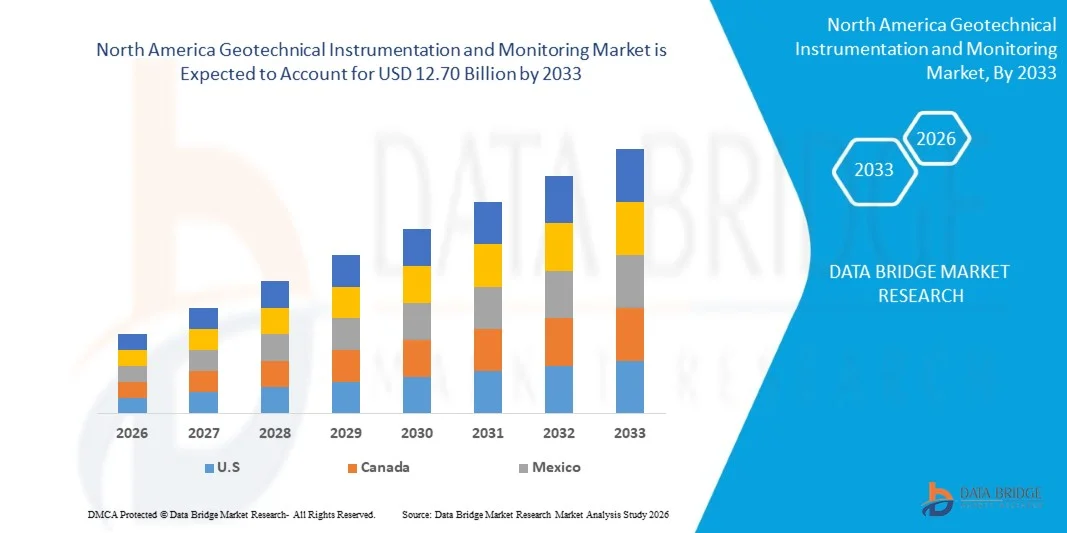

- The North America geotechnical instrumentation and monitoring market size was valued at USD 4.54 billion in 2025 and is expected to reach USD 12.70 billion by 2033, at a CAGR of 13.7% during the forecast period

- The market growth is largely fueled by the increasing demand for infrastructure safety and risk mitigation across construction, mining, and energy sectors, leading to greater adoption of advanced geotechnical instrumentation and monitoring systems for real-time data collection and analysis

- Furthermore, rising investments in large-scale infrastructure projects and the growing need for continuous monitoring of structural stability and ground conditions are establishing geotechnical monitoring solutions as critical tools for ensuring operational safety and regulatory compliance. These converging factors are accelerating the deployment of advanced monitoring technologies, thereby significantly boosting the market growth

North America Geotechnical Instrumentation and Monitoring Market Analysis

- Geotechnical instrumentation and monitoring systems are used to measure, track, and analyze parameters such as soil movement, deformation, pressure, and groundwater conditions in infrastructure and environmental projects. These systems integrate sensors, data acquisition units, and software platforms to provide real-time insights, enhancing decision-making and safety across construction, mining, and energy applications

- The escalating demand for geotechnical instrumentation and monitoring is primarily driven by increasing infrastructure development activities, growing emphasis on safety regulations, and the rising need for early detection of structural and geological risks, which is encouraging widespread adoption of advanced monitoring solutions across various end-use industries

- U.S. dominated the geotechnical instrumentation and monitoring market in 2025, due to extensive infrastructure development, strict regulatory frameworks for construction safety, and increasing investments in transportation, energy, and urban development projects requiring continuous monitoring systems

- Canada is expected to be the fastest growing country in the geotechnical instrumentation and monitoring market during the forecast period due to rising investments in mining activities, infrastructure modernization, and increasing demand for environmental and structural monitoring solutions

- Wired network technology segment dominated the market with a market share of 62.95% in 2025, due to its reliability, stability, and ability to deliver continuous data transmission in critical monitoring environments. Wired systems are widely preferred in long-term infrastructure projects where uninterrupted data flow is essential for safety and compliance

Report Scope and North America Geotechnical Instrumentation and Monitoring Market Segmentation

|

Attributes |

North America Geotechnical Instrumentation and Monitoring Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

North America Geotechnical Instrumentation and Monitoring Market Trends

“Growing Adoption of IoT-Enabled and Real-Time Monitoring Solutions”

- A significant trend in the geotechnical instrumentation and monitoring market is the increasing adoption of IoT-enabled and real-time monitoring systems, driven by the need for continuous data collection and proactive risk management across infrastructure and environmental projects. This trend is transforming traditional monitoring approaches into intelligent systems capable of delivering instant insights and improving decision-making accuracy

- For instance, Geokon offers IoT-based wireless monitoring systems that enable real-time data transmission and remote access for infrastructure and mining applications. These solutions enhance operational efficiency and allow engineers to detect anomalies early, reducing the risk of structural failures

- The integration of cloud-based platforms with geotechnical sensors is expanding the ability to store, analyze, and visualize large volumes of monitoring data. This advancement is improving project transparency and enabling stakeholders to access critical information from remote locations

- The rising complexity of infrastructure projects such as tunnels, bridges, and high-rise buildings is increasing the reliance on automated monitoring systems that provide accurate and continuous measurements. This is strengthening the importance of advanced instrumentation in ensuring structural safety and long-term performance

- Industries are increasingly focusing on predictive maintenance strategies supported by real-time monitoring data, which helps in identifying potential risks before they escalate. This approach is reducing maintenance costs and minimizing downtime across critical infrastructure assets

- The growing emphasis on smart infrastructure and digital construction practices is reinforcing the adoption of connected monitoring systems. This ongoing shift toward intelligent monitoring solutions is supporting safer, more efficient, and data-driven project management across the market

North America Geotechnical Instrumentation and Monitoring Market Dynamics

Driver

“Increasing Infrastructure Development and Safety Regulations”

- The increasing scale of infrastructure development projects across transportation, energy, and urban construction sectors is driving the demand for geotechnical instrumentation and monitoring systems that ensure structural integrity and safety compliance. Governments and private stakeholders are prioritizing monitoring solutions to reduce risks associated with ground movement and structural instability

- For instance, Fugro provides advanced site investigation and monitoring solutions for offshore wind and large infrastructure projects, supporting safe construction practices and regulatory compliance. These services enable accurate subsurface analysis and continuous monitoring, which are critical for project success

- Stringent safety regulations and guidelines are encouraging the deployment of monitoring systems to track parameters such as deformation, pressure, and groundwater levels. These requirements are increasing the adoption of advanced instrumentation across various infrastructure projects

- The rapid urbanization and expansion of smart cities are creating a strong need for reliable monitoring systems that ensure the stability and longevity of buildings and utilities. This is driving investments in geotechnical technologies that support safe construction practices

- The consistent focus on infrastructure safety and compliance is reinforcing the role of geotechnical instrumentation as a critical component in modern engineering projects. This sustained demand is significantly contributing to overall market growth

Restraint/Challenge

“High Installation and Maintenance Costs Limiting Widespread Adoption”

- The geotechnical instrumentation and monitoring market faces challenges due to the high costs associated with the installation and maintenance of advanced monitoring systems, which can limit adoption, particularly in cost-sensitive projects. These systems require specialized equipment, skilled personnel, and continuous calibration to ensure accurate performance

- For instance, Sisgeo S.r.l develops high-precision monitoring instruments that involve complex installation and calibration processes, increasing overall project costs. These cost factors can act as barriers for small and medium-scale projects seeking to implement advanced monitoring solutions

- The deployment of monitoring systems in remote or harsh environments further increases installation complexity and operational expenses. This adds to the overall cost burden and limits scalability in certain regions

- Maintenance requirements, including periodic inspections, data validation, and system upgrades, contribute to long-term operational costs. These ongoing expenses can impact the return on investment for project stakeholders

- The challenge of balancing high-performance monitoring capabilities with cost efficiency continues to influence market dynamics. Addressing these cost-related constraints is essential for expanding the adoption of geotechnical instrumentation and monitoring solutions across diverse applications

North America Geotechnical Instrumentation and Monitoring Market Scope

The market is segmented on the basis of offering, technology, structure, instrumentation, and end user.

•By Offering

On the basis of offering, the geotechnical instrumentation and monitoring market is segmented into hardware, software, and service. The hardware segment dominated the largest market revenue share in 2025, driven by the essential role of physical instruments such as sensors, inclinometers, and data loggers in real-time ground and structural monitoring. These components form the backbone of any monitoring system, ensuring accurate data collection across infrastructure and mining projects. The increasing number of large-scale construction and infrastructure development projects has further strengthened demand for reliable hardware solutions. In addition, advancements in sensor durability and precision have enhanced their deployment in harsh environmental conditions. The integration of hardware with digital platforms continues to improve operational efficiency and safety outcomes across projects.

The software segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by the rising adoption of data analytics, cloud-based monitoring platforms, and automation tools. Software solutions enable real-time data visualization, predictive analysis, and remote monitoring, which are becoming critical for decision-making in complex infrastructure projects. The growing emphasis on digitization and smart infrastructure is accelerating demand for advanced monitoring software. In addition, integration with IoT and AI technologies enhances anomaly detection and risk mitigation capabilities. The scalability and flexibility of software platforms make them increasingly attractive across diverse end users.

•By Technology

On the basis of technology, the geotechnical instrumentation and monitoring market is segmented into wired network technology and wireless technology. The wired network technology segment held the largest market revenue share of 62.95% in 2025, driven by its reliability, stability, and ability to deliver continuous data transmission in critical monitoring environments. Wired systems are widely preferred in long-term infrastructure projects where uninterrupted data flow is essential for safety and compliance. Their resistance to signal interference and ability to operate in extreme conditions further support their dominance. In addition, established infrastructure and familiarity among engineers contribute to continued adoption. These systems remain a preferred choice for high-precision and mission-critical monitoring applications.

The wireless technology segment is expected to witness the fastest growth rate from 2026 to 2033, driven by its flexibility, ease of installation, and cost-effectiveness in remote or hard-to-access locations. Wireless systems reduce the need for extensive cabling, enabling faster deployment and scalability across projects. The increasing adoption of IoT-enabled monitoring solutions is further accelerating this segment’s growth. In addition, advancements in battery life and communication protocols are improving reliability and performance. The growing focus on smart infrastructure and real-time remote monitoring is strengthening demand for wireless solutions.

•By Structure

On the basis of structure, the geotechnical instrumentation and monitoring market is segmented into tunnels and bridges, buildings and utilities, dams, and others. The tunnels and bridges segment dominated the largest market revenue share in 2025, driven by the critical need for continuous monitoring of structural integrity and safety in transportation infrastructure. These structures are highly susceptible to environmental stress, load variations, and geological shifts, necessitating advanced monitoring systems. Governments and private entities are increasingly investing in infrastructure upgrades and expansions, further boosting demand. The complexity and risk associated with tunnels and bridges require high-precision instrumentation solutions. Continuous monitoring helps prevent failures and ensures long-term operational safety.

The dams segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by increasing concerns over dam safety, aging infrastructure, and rising investments in water management systems. Monitoring systems play a crucial role in detecting seepage, deformation, and structural weaknesses in dams. Regulatory mandates and safety compliance requirements are further driving adoption. In addition, climate change impacts and fluctuating water levels are increasing the need for advanced monitoring solutions. The integration of real-time data systems is enhancing risk management and operational efficiency in dam infrastructure.

•By Instrumentation

On the basis of instrumentation, the market is segmented into monitoring pore water pressures, magnetic extensometers, vertical deformation measurement, measurement of lateral deformation, rainfall gauges, settlement gauges, settlement plates and survey markers, and horizontal profile gauge. The monitoring pore water pressures segment held the largest market revenue share in 2025, driven by its critical importance in assessing soil stability and groundwater conditions. Accurate measurement of pore water pressure is essential for preventing slope failures, landslides, and structural instability in construction and mining projects. The widespread application of these instruments across infrastructure and geotechnical projects supports their dominance. In addition, increasing focus on safety and risk mitigation has strengthened their adoption. Continuous monitoring capabilities further enhance project reliability and performance.

The vertical deformation measurement segment is expected to witness the fastest growth rate from 2026 to 2033, driven by rising demand for precise tracking of ground and structural settlement. These instruments are increasingly used in high-rise construction, tunneling, and infrastructure projects to ensure stability and safety. The growing complexity of urban construction projects is accelerating demand for advanced deformation monitoring solutions. In addition, technological advancements are improving measurement accuracy and data integration capabilities. The need for early detection of structural issues is further supporting the growth of this segment.

•By End User

On the basis of end user, the geotechnical instrumentation and monitoring market is segmented into buildings and infrastructure, energy and power, oil and gas, and mining. The buildings and infrastructure segment dominated the largest market revenue share in 2025, driven by rapid urbanization and increasing investments in large-scale construction projects. Monitoring systems are essential for ensuring the safety, durability, and compliance of infrastructure such as highways, railways, and commercial buildings. The growing adoption of smart city initiatives is further supporting demand for advanced monitoring solutions. In addition, stringent safety regulations are encouraging the integration of geotechnical instrumentation. Continuous monitoring helps reduce risks and enhances long-term structural performance.

The mining segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by increasing exploration activities and the need for enhanced safety in mining operations. Geotechnical monitoring plays a crucial role in detecting ground movement, slope instability, and underground hazards. The rising focus on worker safety and regulatory compliance is accelerating adoption. In addition, the use of advanced monitoring technologies is improving operational efficiency and risk management. The expansion of mining activities in emerging economies is further contributing to segment growth.

North America Geotechnical Instrumentation and Monitoring Market Regional Analysis

- U.S. dominated the geotechnical instrumentation and monitoring market with the largest revenue share in 2025, driven by extensive infrastructure development, strict regulatory frameworks for construction safety, and increasing investments in transportation, energy, and urban development projects requiring continuous monitoring systems

- The demand for geotechnical instrumentation and monitoring solutions is supported by continuous technological advancements and service expansion by companies such as Geokon and Fugro, offering advanced sensors, real-time monitoring systems, and data-driven solutions designed to enhance structural safety, improve risk assessment, and support efficient project management

- The presence of established infrastructure, increasing adoption of digital monitoring technologies, and strong focus on risk mitigation and compliance standards reinforce the U.S. leadership position in the North America market

Canada Geotechnical Instrumentation and Monitoring Market Insight

Canada is projected to register the fastest CAGR in the North America geotechnical instrumentation and monitoring market from 2026 to 2033, supported by rising investments in mining activities, infrastructure modernization, and increasing demand for environmental and structural monitoring solutions. Government initiatives promoting infrastructure safety and collaborations with companies such as RST Instruments Ltd. and Keller Group plc for advanced monitoring technologies are accelerating market growth. The expansion of smart infrastructure and increasing focus on sustainable resource management position Canada as the fastest-growing country in the region during the forecast period.

Mexico Geotechnical Instrumentation and Monitoring Market Insight

Mexico is expected to grow steadily from 2026 to 2033, driven by expanding infrastructure and construction activities, increasing investments in energy and transportation projects, and rising adoption of geotechnical monitoring systems to ensure structural stability and safety. Improvements in construction practices and growing awareness of risk management are supporting the integration of advanced instrumentation solutions. Partnerships with global service providers such as Fugro and Sisgeo S.r.l are strengthening technical capabilities. These developments contribute to sustained growth of the North America geotechnical instrumentation and monitoring market throughout the forecast period.

North America Geotechnical Instrumentation and Monitoring Market Share

The geotechnical instrumentation and monitoring industry is primarily led by well-established companies, including:

- Nova Ventures (U.S.)

- American Geotechnical (U.S.)

- Geotech Services Pvt. Ltd. (India)

- Cascade Geotechnical (U.S.)

- Petra Geosciences, Inc. (U.S.)

- GEOKON (U.S.)

- RST Instruments Ltd. (Canada)

- Deep Excavation LLC (U.S.)

- Fugro (Netherlands)

- Geotechnics Limited (U.K.)

- James Fisher and Sons plc (U.K.)

- Keller Group plc (U.K.)

- Sisgeo S.r.l (Italy)

- M.A.E. Srl. (Italy)

- WJ Groundwater Limited (U.K.)

- Wardle Drilling & Geotechnical Ltd. (U.K.)

- Land-Drill (U.K.)

- MGS (U.S.)

- Quantum Geotechnic (Australia)

Latest Developments in North America Geotechnical Instrumentation and Monitoring Market

- In April 2026, Geokon introduced an advanced wireless monitoring system integrating IoT-enabled sensors and cloud-based analytics, which is strengthening the geotechnical instrumentation and monitoring market by enhancing real-time data accuracy and enabling continuous remote monitoring across critical infrastructure projects. This development is accelerating the shift toward digital and automated monitoring solutions, reducing manual intervention and improving operational efficiency. It is further supporting predictive maintenance capabilities and early risk detection, which are becoming essential for large-scale and complex engineering projects

- In June 2025, Fugro opened a new geotechnical laboratory in Jakarta, increasing testing capacity by 20% and reducing turnaround time by 30%, which is supporting the market by improving project timelines and enabling faster geotechnical data analysis. This expansion is addressing the growing demand for infrastructure development in Southeast Asia, where timely soil and material testing is critical for project execution. It is also enhancing service efficiency and strengthening Fugro’s regional presence, contributing to higher adoption of advanced testing and monitoring solutions

- In June 2025, Fugro secured an offshore site characterization contract with RWE and TotalEnergies for upcoming wind farm projects, which is contributing to market growth by expanding the role of geotechnical monitoring in offshore renewable energy developments. This contract highlights the increasing reliance on precise subsurface data and monitoring technologies for safe and efficient wind farm installation. It is further driving demand for advanced offshore instrumentation and strengthening the integration of geotechnical solutions in sustainable energy infrastructure

- In May 2025, Michigan Department of Environment, Great Lakes, and Energy allocated USD 14.9 million under its Dam Risk Reduction Grant Program for monitoring-focused dam upgrades, which is driving the market by increasing government investments in infrastructure safety and resilience. This initiative is promoting the adoption of advanced monitoring systems to detect structural weaknesses, seepage, and deformation in aging dams. It is also reinforcing regulatory compliance requirements and encouraging the use of real-time monitoring technologies for effective risk mitigation and disaster prevention

- In January 2025, SOCOTEC acquired Ninyo and Moore, adding 16 offices and 600 professionals across the U.S., which is strengthening the market by expanding technical expertise and service capabilities in geotechnical and environmental monitoring. This acquisition is enhancing SOCOTEC’s ability to deliver integrated solutions across large infrastructure and environmental projects. It is also supporting market consolidation and increasing competition, leading to improved service quality and innovation in geotechnical instrumentation and monitoring solutions

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

North America Geotechnical Instrumentation And Monitoring Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its North America Geotechnical Instrumentation And Monitoring Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as North America Geotechnical Instrumentation And Monitoring Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.