North America Hernia Mesh Repair Devices Market

Market Size in USD Billion

CAGR :

%

USD

5.60 Billion

USD

7.74 Billion

2025

2033

USD

5.60 Billion

USD

7.74 Billion

2025

2033

| 2026 –2033 | |

| USD 5.60 Billion | |

| USD 7.74 Billion | |

| % | |

|

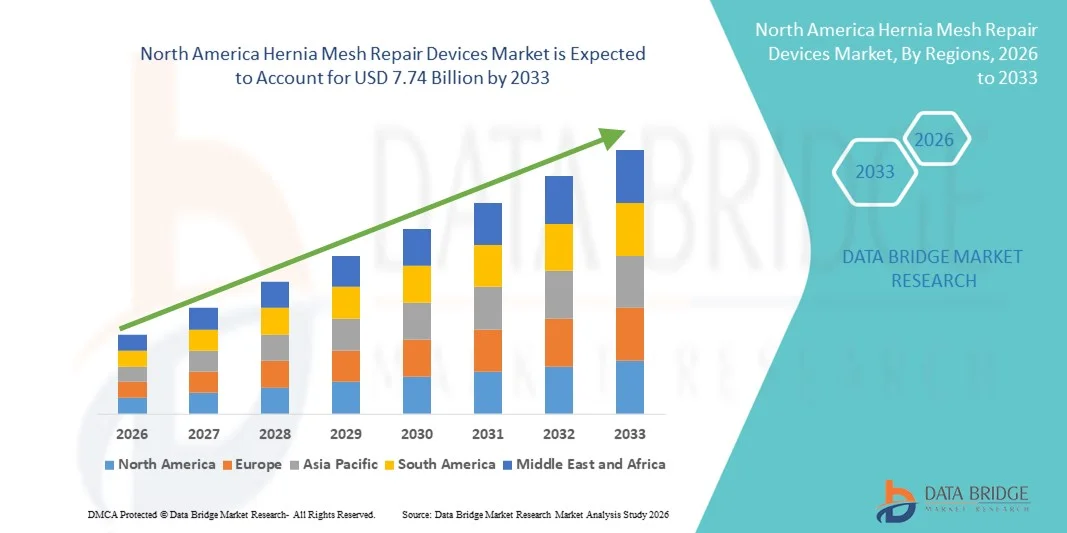

North America Hernia Mesh Repair Devices Market Size

- The North America hernia mesh repair devices market size was valued at USD 5.60 billion in 2025 and is expected to reach USD 7.74 billion by 2033, at a CAGR of 4.13% during the forecast period

- The market growth is largely driven by the rising prevalence of hernia cases, increasing awareness of minimally invasive surgical techniques, and advancements in biocompatible mesh materials that improve patient outcomes and reduce postoperative complications

- Furthermore, growing adoption of laparoscopic and robotic-assisted hernia repair procedures, along with rising investments by healthcare providers to enhance surgical infrastructure, is positioning hernia mesh repair devices as a preferred solution in both hospitals and specialized surgical centers. These factors are collectively boosting demand, thereby propelling the industry’s growth

North America Hernia Mesh Repair Devices Market Analysis

- Hernia mesh repair devices, including meshes, fixation devices, and surgical instruments, are increasingly vital components of modern surgical procedures in both hospitals and ambulatory surgery centers due to their ability to reduce recurrence rates, enhance patient recovery, and support minimally invasive techniques

- The escalating demand for hernia mesh repair devices is primarily fueled by the growing prevalence of hernia cases, increasing adoption of minimally invasive surgical procedures, and innovations in meshes and fixation devices that improve surgical outcomes and reduce postoperative complications

- The U.S. dominated the North America hernia mesh repair devices market with the largest revenue share of 65.7% in 2025, characterized by advanced surgical infrastructure, high healthcare spending, and a strong presence of key industry players, with substantial growth in laparoscopic and tension-free open repair surgeries, driven by innovations from both established medical device manufacturers and startups focusing on safer and more effective mesh solutions

- Canada is expected to be the fastest-growing country in the North America hernia mesh repair devices market during the forecast period due to increasing healthcare investments, rising adoption of laparoscopic surgeries, and expanding access to advanced hernia repair devices across hospitals and ambulatory surgery centers

- Meshes segment dominated the North America hernia mesh repair devices market with a market share of 55.2% in 2025, driven by its proven effectiveness, widespread clinical acceptance, and ease of integration into various surgical procedures

Report Scope and North America Hernia Mesh Repair Devices Market Segmentation

|

Attributes |

North America Hernia Mesh Repair Devices Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

North America Hernia Mesh Repair Devices Market Trends

Advancements in Minimally Invasive and Robotic-Assisted Surgeries

- A significant and accelerating trend in the North America hernia mesh repair devices market is the growing adoption of minimally invasive and robotic-assisted surgical techniques, improving precision, reducing recovery time, and enhancing patient outcomes

- For instance, the robotic-assisted hernia mesh repair procedures allow surgeons to perform complex inguinal and ventral hernia repairs with enhanced dexterity and visualization, resulting in fewer complications and shorter hospital stays

- Advanced meshes and fixation devices are being developed to support laparoscopic and robotic-assisted procedures, providing better biocompatibility and reducing recurrence rates compared with traditional materials

- The integration of pre-shaped, lightweight, and biologically engineered meshes with modern surgical techniques enables surgeons to tailor procedures for patient-specific needs, enhancing procedural efficiency and clinical outcomes

- This trend towards more precise, less invasive, and patient-specific surgical solutions is fundamentally reshaping surgeon and patient expectations for hernia repair procedures

- Consequently, companies such as Medtronic and Ethicon are developing robotic-compatible and laparoscopic-friendly meshes and instruments to support the evolving demand for minimally invasive hernia repair solutions

- For instance, emerging startups are introducing 3D-printed meshes customized for patient anatomy, further advancing personalized surgical care

North America Hernia Mesh Repair Devices Market Dynamics

Driver

Increasing Prevalence of Hernia Cases and Awareness of Advanced Surgical Techniques

- The rising prevalence of hernia cases, combined with growing awareness of minimally invasive surgical options, is a significant driver for the heightened demand for hernia mesh repair devices

- For instance, in March 2025, Ethicon launched an advanced laparoscopic mesh system in the U.S., designed to improve patient recovery and reduce postoperative complications, driving adoption in key hospitals

- As patients and surgeons seek safer, faster, and more effective repair options, advanced meshes and fixation devices provide improved outcomes and lower recurrence rates, creating strong demand

- Furthermore, the expanding number of ambulatory surgery centers and adoption of laparoscopic and tension-free procedures are making hernia mesh repair devices an essential part of surgical infrastructure

- Growing investments in healthcare infrastructure, increasing insurance coverage, and rising patient awareness are further supporting the uptake of hernia mesh repair devices across both hospitals and outpatient surgical centers

- For instance, hospitals in Canada are upgrading operating rooms to support laparoscopic and robotic-assisted hernia repairs, boosting mesh adoption

- Increasing clinical research and training programs for surgeons on advanced mesh applications are also promoting higher adoption rates across North America

Restraint/Challenge

Postoperative Complications and Regulatory Compliance

- The risks of postoperative complications such as mesh rejection, infection, or adhesion formation pose a significant challenge to broader market penetration

- For instance, reports of mesh-related adverse events have made some surgeons and patients cautious about certain mesh types, impacting adoption rates in some hospitals

- Addressing these clinical concerns through improved mesh design, biocompatible materials, and surgeon training is crucial for building trust and encouraging adoption

- In addition, stringent regulatory requirements by the FDA for new mesh products and surgical instruments can delay product approvals, adding time and cost hurdles for manufacturers

- While innovations are reducing complication rates and expanding the safety profile of hernia meshes, these challenges require continuous clinical evidence, monitoring, and education to maintain market growth

- For instance, delays in FDA clearance for new robotic-compatible mesh instruments can slow adoption in leading U.S. hospitals

- High costs of advanced biologic and robotic-compatible meshes compared to traditional meshes can limit accessibility in price-sensitive regions or smaller healthcare centers

North America Hernia Mesh Repair Devices Market Scope

The market is segmented on the basis of product, surgery type, hernia type, and end user.

- By Product

On the basis of product, the market is segmented into meshes, fixation devices, and surgical instruments. The meshes segment dominated the market with the largest revenue share of 55.2% in 2025, driven by their established effectiveness in reinforcing weakened tissue and reducing hernia recurrence rates. Meshes are widely preferred in both laparoscopic and tension-free open surgeries due to their biocompatibility, lightweight design, and ease of integration into various surgical procedures. Surgeons prioritize synthetic and biologic meshes for their proven clinical performance and ability to minimize postoperative complications. The strong presence of key medical device manufacturers in North America ensures the availability of high-quality meshes, further reinforcing their market dominance. In addition, patient awareness and hospital preference for reliable surgical outcomes are increasing the adoption of advanced mesh types.

The fixation devices segment is anticipated to witness the fastest growth from 2026 to 2033, fueled by rising adoption of laparoscopic surgeries and robotic-assisted procedures. Fixation devices, including tacks, sutures, and adhesives, enhance the stability of implanted meshes and improve procedural efficiency. Surgeons increasingly prefer these devices for their precision, reduced operative time, and ability to secure meshes effectively in minimally invasive surgeries. The growing number of ambulatory surgery centers and investments in advanced surgical infrastructure are also contributing to the accelerated uptake of fixation devices. In addition, innovation in absorbable and ergonomic fixation tools is attracting hospitals seeking safer and more user-friendly options.

- By Surgery Type

On the basis of surgery type, the market is segmented into tension-free open repair surgery and laparoscopic surgery. The tension-free repair surgery segment dominated the market in 2025 due to its long-standing clinical acceptance and ability to reduce tension on repaired tissue, which minimizes recurrence rates. Surgeons often prefer tension-free techniques for inguinal and umbilical hernia repairs, especially in traditional hospital settings. High familiarity among healthcare professionals, extensive clinical evidence, and proven patient outcomes drive its continued preference. The segment benefits from wide availability of compatible meshes and fixation devices, making it the default choice in many North American hospitals. In addition, insurance coverage and standardized surgical protocols support the sustained dominance of this segment.

The laparoscopic surgery segment is expected to witness the fastest growth from 2026 to 2033, fueled by the rising demand for minimally invasive procedures that reduce recovery time, postoperative pain, and hospital stays. Laparoscopic surgery allows surgeons to perform hernia repairs with smaller incisions and greater precision, which is increasingly preferred in both hospitals and ambulatory surgical centers. Technological advancements in laparoscopic instruments and meshes compatible with robotic-assisted systems further enhance its adoption. Growing patient awareness of faster recovery and reduced complications is also supporting the segment’s accelerated growth.

- By Hernia Type

On the basis of hernia type, the market is segmented into inguinal, incisional, umbilical, and femoral hernia. The inguinal hernia segment dominated the market with the largest revenue share in 2025 due to the high prevalence of this condition in the U.S. and Canada. Surgical intervention for inguinal hernias often requires mesh implantation, which drives product demand. Both laparoscopic and tension-free open repair procedures are widely used for inguinal hernia repairs, contributing to the segment’s dominance. The clinical familiarity among surgeons, proven procedural outcomes, and patient preference for effective repair solutions further support its leading market position. In addition, hospital protocols and insurance coverage for inguinal hernia repairs ensure sustained demand for surgical meshes and fixation devices.

The incisional hernia segment is expected to witness the fastest growth from 2026 to 2033, driven by the increasing number of abdominal surgeries and rising postoperative hernia incidence. Incisional hernias often require complex repair procedures using advanced meshes and fixation devices, creating high-value opportunities for manufacturers. The adoption of laparoscopic techniques for incisional hernia repairs, coupled with growing awareness of minimally invasive options, is accelerating segment growth. Hospitals and ambulatory surgery centers are increasingly equipped to handle complex incisional repairs, further supporting this trend.

- By End User

On the basis of end user, the market is segmented into hospitals and ambulatory surgery centers. The hospitals segment dominated the market in 2025 with the largest revenue share due to the high volume of hernia surgeries performed in these settings and the availability of advanced surgical infrastructure. Hospitals have greater access to trained surgeons, robotic-assisted systems, and high-quality meshes, making them the primary choice for complex and high-risk hernia procedures. Strong partnerships with leading medical device manufacturers and adherence to standardized surgical protocols also drive hospital preference. In addition, hospitals benefit from insurance reimbursements and clinical research support, reinforcing their dominance in the market.

The ambulatory surgery centers segment is expected to witness the fastest growth from 2026 to 2033, fueled by the increasing preference for outpatient procedures, minimally invasive surgeries, and shorter recovery times. Ambulatory centers are expanding capabilities for laparoscopic hernia repairs using advanced meshes and fixation devices. Patient demand for faster discharge and reduced hospitalization costs supports the rapid adoption of hernia mesh repair devices in these centers. Innovations in portable laparoscopic instruments and user-friendly fixation devices further enhance the segment’s growth potential.

North America Hernia Mesh Repair Devices Market Regional Analysis

- The U.S. dominated the North America hernia mesh repair devices market with the largest revenue share of 65.7% in 2025, characterized by advanced surgical infrastructure, high healthcare spending, and a strong presence of key industry players

- Patients and surgeons in the region highly value minimally invasive techniques, advanced meshes, and fixation devices that reduce recurrence rates and postoperative complications, improving overall surgical outcomes

- This widespread adoption is further supported by strong healthcare spending, growing awareness of laparoscopic and tension-free repair procedures, and a robust network of hospitals and ambulatory surgery centers, establishing hernia mesh repair devices as a preferred solution across both public and private healthcare settings

U.S. Hernia Mesh Repair Devices Market Insight

The U.S. hernia mesh repair devices market captured the largest revenue share of 65.7% in 2025 within North America, fueled by widespread adoption of minimally invasive procedures and advanced surgical technologies. Patients and surgeons increasingly prioritize safer, faster, and more effective hernia repairs using laparoscopic and tension-free open surgeries. The growing preference for biologic and synthetic meshes, combined with innovative fixation devices and robotic-assisted solutions, further propels market growth. High healthcare spending, advanced medical infrastructure, and the presence of key medical device manufacturers are significantly contributing to expansion. Moreover, hospitals and ambulatory surgery centers are upgrading capabilities to perform complex inguinal and incisional hernia repairs efficiently.

Canada Hernia Mesh Repair Devices Market Insight

The Canada hernia mesh repair devices market is expected to grow at the fastest CAGR during the forecast period due to increasing healthcare investments and rising adoption of laparoscopic and robotic-assisted surgeries. Hospitals and ambulatory surgery centers are expanding access to advanced meshes and fixation devices to meet growing patient demand. Surgeons increasingly prefer minimally invasive procedures due to faster recovery, reduced postoperative complications, and enhanced procedural precision. In addition, growing awareness of newer mesh technologies and the expansion of surgical training programs are supporting market growth. The country’s strong healthcare infrastructure and regulatory support for medical innovations are further accelerating adoption.

Mexico Hernia Mesh Repair Devices Market Insight

The Mexico hernia mesh repair devices market is projected to grow steadily during the forecast period, driven by increasing hernia prevalence, expanding hospital infrastructure, and rising awareness of advanced surgical options. Minimally invasive procedures, including laparoscopic surgeries, are gaining traction in major urban centers. Hospitals are increasingly adopting high-quality meshes and fixation devices to improve surgical outcomes and reduce complications. Government initiatives to improve healthcare access and investments in medical technology are further supporting market expansion. The growing patient population seeking faster recovery and safer hernia repair solutions also contributes to increased adoption

North America Hernia Mesh Repair Devices Market Share

The North America Hernia Mesh Repair Devices industry is primarily led by well-established companies, including:

- Boston Scientific Corporation (U.S.)

- Cook (U.S.)

- TELA Bio, Inc. (U.S.)

- Integra LifeSciences Corporation (U.S.)

- BD (U.S.)

- Ethicon Inc. (U.S.)

- C.R. Bard, Inc. (U.S.)

- Medtronic (Ireland)

- W. L. Gore & Associates, Inc. (U.S.)

- Zimmer Biomet. (U.S.)

- Smith+Nephew plc (U.K.)

- Stryker (U.S.)

- Olympus Corporation (Japan)

- Karl Storz SE & Co. KG (Germany)

- Getinge AB (Sweden)

- Medline Industries, LP (U.S.)

- Cardinal Health, Inc. (U.S.)

- Teleflex Incorporated (U.S.)

- CONMED Corporation (U.S.)

- Arthrex, Inc. (U.S.)

What are the Recent Developments in North America Hernia Mesh Repair Devices Market?

- In December 2025, Tela Bio Inc. filed an antitrust lawsuit against Becton Dickinson, alleging monopolistic practices in the U.S. hernia mesh market that restricted competition and increased costs for hospitals and healthcare providers, reflecting legal and competitive dynamics shaping the industry

- In June 2025, breakthrough hernia mesh technology developed by researchers at NC State University and Duke University was selected for the AUTM Better World Project, highlighting its potential to improve patient outcomes and reduce complications, and underscoring academic innovation in hernia mesh development

- In April 2025, Becton, Dickinson and Company (BD) received FDA 510(k) clearance and launched the Phasix™ ST Umbilical Hernia Patch, the first fully bioabsorbable hernia mesh designed specifically for umbilical hernia repair, offering surgeons a resorbable alternative to traditional permanent mesh while using familiar placement techniques

- In April 2024, TELA Bio, Inc. announced the U.S. commercial launch of its OviTex IHR (Inguinal Hernia Repair) Reinforced Tissue Matrix, a robotic‑compatible surgical mesh available in multiple configurations designed for laparoscopic and robotic‑assisted inguinal hernia procedures, addressing the need for more natural tissue repair options in common hernia surgeries

- In July 2021, Becton, Dickinson and Company acquired Tepha, Inc., a developer of proprietary resorbable polymer technology, strategically integrating key resorbable material technology (GalaFLEX P4HB) into its hernia mesh product portfolio to support development of advanced absorbable meshes

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.