North America Medical Waste Management Market

Market Size in USD Billion

CAGR :

%

USD

1.23 Billion

USD

1.97 Billion

2025

2033

USD

1.23 Billion

USD

1.97 Billion

2025

2033

| 2026 –2033 | |

| USD 1.23 Billion | |

| USD 1.97 Billion | |

| % | |

|

North America Medical Waste Management Market Size

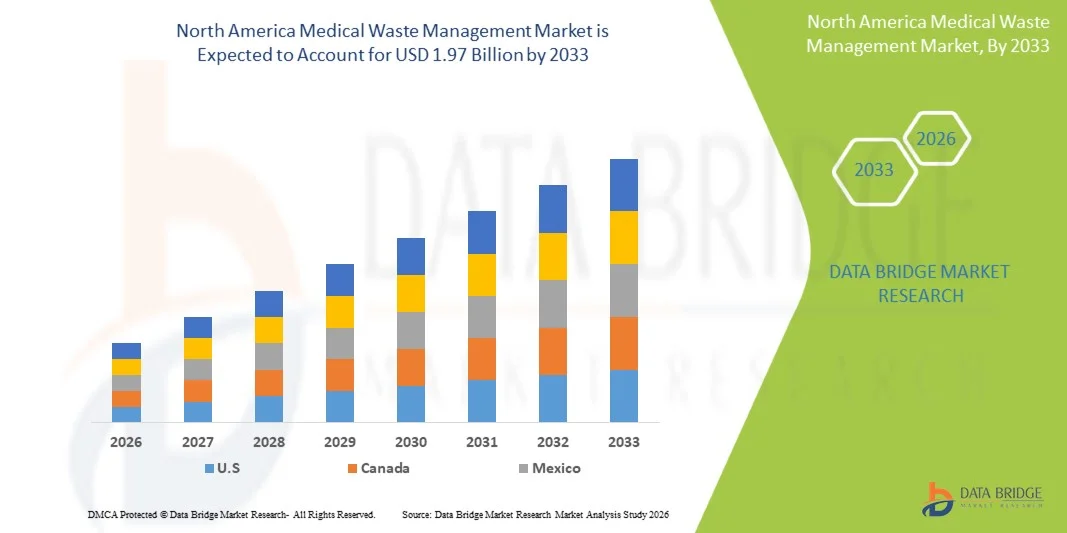

- The North America Medical Waste Management Market size was valued at USD 1.23 billion in 2025 and is expected to reach USD 1.97 billion by 2033, at a CAGR of 6.07% during the forecast period

- The market growth is largely fueled by the increasing generation of medical and healthcare waste, coupled with technological advancements in waste treatment and disposal solutions, leading to safer and more efficient management practices across hospitals, clinics, laboratories, and pharmaceutical facilities

- Furthermore, rising regulatory requirements, growing awareness about environmental sustainability, and increasing emphasis on public health safety are establishing medical waste management solutions as an essential component of modern healthcare infrastructure. These converging factors are accelerating the uptake of medical waste management solutions, thereby significantly boosting the industry's growth

North America Medical Waste Management Market Analysis

- Medical waste management solutions, encompassing the collection, treatment, and disposal of hazardous healthcare waste, are increasingly vital components of modern healthcare systems in hospitals, clinics, laboratories, and pharmaceutical facilities due to their role in ensuring public safety, regulatory compliance, and environmental protection

- The escalating demand for medical waste management is primarily fueled by increasing healthcare activities, stringent regulatory requirements, rising awareness of environmental sustainability, and the need for safe and efficient waste handling solutions

- U.S. dominated the North America Medical Waste Management Market with the largest revenue share of 41.5% in 2025, characterized by advanced healthcare infrastructure, strong enforcement of waste management regulations, and high adoption of modern treatment technologies, with significant growth driven by large hospitals, clinics, and diagnostic laboratories implementing comprehensive waste management systems

- Canada is expected to be the fastest growing region in the North America Medical Waste Management Market during the forecast period due to increasing healthcare investments, expansion of medical facilities, rising awareness about safe disposal practices, and adoption of innovative waste treatment technologies

- The controlled segment dominated the largest market revenue share of 65.1% in 2025, driven by strict government regulations and monitoring requirements for medical waste management

Report Scope and North America Medical Waste Management Market Segmentation

|

Attributes |

Medical Waste Management Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

|

|

Key Market Players |

• Stericycle, Inc. (U.S.) |

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

North America Medical Waste Management Market Trends

“Increasing Adoption of Advanced Waste Management Solutions”

- A significant trend in the global North America Medical Waste Management Market is the rapid adoption of advanced waste segregation, collection, and disposal technologies to meet stringent healthcare regulations

- For instance, in 2025, Apollo Hospitals in India implemented an automated biomedical waste tracking system to monitor segregation and disposal across multiple facilities, ensuring compliance with local regulatory guidelines and improving operational efficiency

- This trend is further fueled by hospitals, diagnostic laboratories, and pharmaceutical companies seeking safer and more environmentally responsible disposal methods

- The integration of environmentally sustainable practices into waste management processes is becoming increasingly prevalent. For instance, in Germany, the University Hospital Heidelberg adopted microwave-based waste treatment to sterilize infectious waste before disposal, reducing environmental impact while meeting EU waste disposal standards

- This trend highlights the global shift toward eco-friendly technologies that balance compliance with sustainability

- Healthcare providers are increasingly adopting digital monitoring and reporting systems for waste management, enabling real-time data collection and process optimization. For instance, in the U.S., Kaiser Permanente introduced digital dashboards to track the quantity and type of waste generated across its facilities, allowing for better decision-making and cost control

- These systems are shaping the modern approach to medical waste management worldwide

North America Medical Waste Management Market Dynamics

Driver

“Rising Healthcare Activities and Regulatory Compliance”

- The growth of healthcare services globally, including the expansion of hospitals, outpatient clinics, and diagnostic laboratories, is a key driver for the North America Medical Waste Management Market

- For instance, in 2025, the Mayo Clinic in the U.S. expanded its outpatient services and simultaneously upgraded its waste management infrastructure to handle increased biomedical waste, ensuring adherence to OSHA and EPA regulations. Increased patient inflow, diagnostic testing, and surgical procedures directly contribute to higher waste volumes, driving demand for effective management solutions

- Government regulations and strict compliance requirements for biomedical waste disposal are accelerating investments in certified medical waste management systems. For instance, in the U.K., NHS Trusts have implemented centralized waste management protocols following the Hazardous Waste Regulations, compelling healthcare facilities to adopt advanced disposal methods and monitoring systems

- Regulatory oversight ensures a safer and more controlled waste management ecosystem, stimulating market growth

- Outbreaks of infectious diseases and heightened awareness of public health risks are pushing healthcare institutions to modernize their waste management practices

- For instance, during the COVID-19 pandemic, hospitals in Italy introduced segregated collection and treatment systems for infectious PPE and clinical waste, highlighting the importance of efficient waste disposal for infection control. This ongoing focus on safety and compliance continues to drive market demand globally

Restraint/Challenge

“High Operational Costs and Infrastructure Limitations”

- The high initial investment and ongoing operational expenses associated with advanced medical waste management systems remain a significant barrier, especially for smaller healthcare facilities in developing regions

- For instance, several clinics in sub-Saharan Africa rely on manual disposal methods due to the prohibitive costs of autoclaves or microwave treatment systems, limiting adoption despite growing awareness of proper waste management practices

- Limited infrastructure and lack of trained personnel in certain regions restrict the effective implementation of advanced waste disposal systems

- For instance, rural hospitals in Southeast Asia often face challenges in transporting biomedical waste to certified treatment facilities, leading to delays or unsafe disposal practices. These infrastructure constraints highlight a critical barrier to global market growth

- Inconsistent enforcement of regulations and low awareness in some countries can also hinder investments in medical waste management

- For instance, small clinics in parts of Latin America may not comply fully with national waste guidelines due to inadequate monitoring and support, reducing the overall effectiveness of existing systems

- Addressing these challenges through training programs, government incentives, and scalable, cost-efficient solutions is essential to sustain market growth

North America Medical Waste Management Market Scope

The North America Medical Waste Management Market is segmented on the basis of type of waste, service type, treatment type, treatment site, category, and source of generation.

• By Type of Waste

On the basis of type of waste, the market is segmented into hazardous waste and non-hazardous waste. The hazardous waste segment dominated the largest market revenue share of 57.4% in 2025, driven by stringent regulatory requirements for infectious, pharmaceutical, chemical, and sharps waste generated in hospitals, laboratories, and clinics. Hazardous waste management ensures safety for healthcare workers and prevents environmental contamination. Hospitals prioritize safe disposal solutions to comply with OSHA, WHO, and EPA guidelines. The growing number of healthcare facilities and increase in surgical procedures globally further supports dominance. Advanced technologies like autoclaving, chemical treatment, and low-emission incineration strengthen the segment. Training programs for proper handling and segregation, coupled with certified service providers, enhance adoption. Regulatory compliance and government monitoring programs are major drivers. Increasing awareness about the risks associated with improper disposal also fuels segment growth. Hazardous waste accounts for the majority of medical waste generated, ensuring sustained market demand. Hospitals, laboratories, and clinics are key contributors to this segment.

The non-hazardous waste segment is expected to witness the fastest CAGR of 19.8% from 2026 to 2033, driven by the growing volumes of general and biodegradable waste in hospitals, laboratories, and outpatient facilities. Rising adoption of waste-to-energy initiatives, recycling programs, and sustainable disposal practices supports growth. IoT-enabled monitoring and cloud-based tracking systems improve operational efficiency and ensure proper segregation of non-hazardous waste. Increasing environmental awareness, government incentives for sustainable waste management, and initiatives promoting circular economy practices further accelerate adoption. Non-hazardous waste includes packaging materials, paper, plastics, and non-infectious laboratory waste. Hospitals and diagnostic centers are increasingly implementing organized management systems. Recycling of plastics and metals reduces landfill impact and environmental footprint. Onsite and centralized processing technologies are being expanded for efficient handling. Public-private partnerships and corporate sustainability programs contribute to faster adoption. Overall, non-hazardous waste is rapidly growing due to focus on environmental sustainability and operational efficiency.

• By Service Type

On the basis of service type, the market is segmented into collection, transportation and storage, treatment and disposal, recycling, and others. The treatment and disposal segment dominated the largest market revenue share of 52.6% in 2025, due to the critical need for safe elimination of hazardous and infectious waste. Hospitals, clinics, and laboratories rely on incineration, autoclaving, chemical, and biological methods for sterilization. Regulatory oversight and accreditation requirements are major drivers. Treatment and disposal services include handling of sharps, pharmaceutical residues, and infectious materials. Technological advancements in sterilization, volume reduction, and emissions control support market dominance. Centralized facilities provide economies of scale, reducing operational costs. Continuous training for healthcare staff enhances proper waste handling. Strict adherence to environmental and health standards ensures reliability. Adoption of modern treatment systems in emerging markets is increasing. Awareness programs on infection prevention promote professional treatment adoption. Increasing medical procedures and testing volume further boost market growth.

The recycling segment is expected to witness the fastest CAGR of 21.4% from 2026 to 2033, driven by increasing focus on sustainability and resource recovery. Recycling of plastics, metals, and non-hazardous materials helps reduce landfill pressure and promotes circular economy practices. Hospitals, laboratories, and reverse distributors are adopting specialized recycling programs. Integration of sterilization and reuse of certain medical materials reduces operational costs. Government incentives and policies promoting green healthcare support growth. Expansion of dedicated recycling infrastructure enhances capacity. Awareness campaigns and ESG initiatives in healthcare facilities accelerate adoption. Adoption of automated waste segregation technologies ensures efficiency. Recyclable medical waste is increasingly monitored through IoT and cloud platforms. The segment benefits from rising regulatory encouragement and environmental awareness. Public-private partnerships further strengthen adoption.

• By Treatment Type

On the basis of treatment type, the market is segmented into incineration, autoclaving, chemical treatment, irradiative, biological, and others. The incineration segment dominated the largest market revenue share of 48.7% in 2025, due to its ability to destroy infectious and pharmaceutical waste effectively. Hospitals and laboratories rely on incineration for sharps and high-risk hazardous waste. Energy-efficient and low-emission incinerators ensure compliance with environmental regulations. The segment is supported by growing healthcare infrastructure and surgical procedures. Incineration reduces waste volume significantly while eliminating pathogens. Technological improvements enhance throughput and reduce operating costs. Regulatory oversight ensures safe emissions and process control. Staff training for proper loading and handling is a key requirement. Centralized facilities improve operational efficiency. Incineration remains the preferred choice for high-risk medical waste. Government monitoring and enforcement further strengthen adoption.

The autoclaving segment is expected to witness the fastest CAGR of 20.6% from 2026 to 2033, driven by increasing adoption of environmentally friendly non-incineration technologies. Autoclaving is widely used for infectious waste, reusable instruments, and laboratory waste. Mobile and onsite autoclave units provide flexibility for small and medium-sized healthcare facilities. Technological advancements improve energy efficiency and sterilization cycles. Rising awareness of emissions from incineration encourages adoption. Compliance with environmental standards and regulatory encouragement support growth. Hospitals, laboratories, and ambulatory centers are adopting autoclaving for sustainability. Training and certification programs increase efficiency. Integration with digital tracking systems ensures proper waste monitoring. Expansion of outpatient care centers further drives demand.

• By Treatment Site

On the basis of treatment site, the market is segmented into offsite and onsite. The offsite segment dominated the largest market revenue share of 60.2% in 2025, driven by centralized treatment facilities handling large volumes of medical waste from multiple hospitals and laboratories. Offsite treatment ensures compliance with stringent environmental regulations and allows for advanced sterilization and disposal methods. It reduces operational burden on healthcare facilities. Centralized sites provide economies of scale and cost advantages. Advanced incineration, chemical treatment, and autoclaving technologies are concentrated at offsite facilities. Regulatory oversight ensures safe handling, transport, and disposal. Growing hospital networks and increased medical procedures drive demand. Advanced logistics and tracking systems improve operational efficiency. Offsite treatment ensures safe emissions control and biohazard risk reduction. Continuous quality monitoring and certification programs support adoption.

The onsite segment is expected to witness the fastest CAGR of 18.9% from 2026 to 2033, driven by the rising adoption of mobile and decentralized treatment technologies. Onsite autoclaves, mobile incinerators, and sterilization units enable hospitals, clinics, and laboratories to process waste on-site. This reduces transportation risks, improves biohazard safety, and ensures regulatory compliance. Increasing demand from small and medium-sized healthcare facilities accelerates adoption. Sustainability initiatives encourage reuse and proper segregation. Integration with digital monitoring platforms ensures operational efficiency. Onsite treatment also reduces turnaround times for high-risk waste. Cost-effective mobile solutions support widespread adoption. Emerging markets with regulatory developments favor onsite implementation. Training programs enhance staff capabilities. Growth in outpatient and ambulatory centers further drives the segment.

• By Category

On the basis of category, the market is segmented into controlled and uncontrolled. The controlled segment dominated the largest market revenue share of 65.1% in 2025, driven by strict government regulations and monitoring requirements for medical waste management. Controlled systems ensure proper documentation, segregation, collection, and disposal of hazardous and non-hazardous waste. Hospitals, laboratories, and manufacturers rely on controlled practices to comply with WHO, EPA, and local regulations. Advanced monitoring, digital tracking, and staff training strengthen adoption. Risk mitigation and infection prevention programs further drive growth. Controlled systems enable safe handling and environmental protection. Certification programs for service providers ensure compliance. Government incentives encourage adoption of controlled waste management practices. Growing hospital infrastructure increases demand. Technological adoption improves efficiency and safety.

The uncontrolled segment is expected to witness the fastest CAGR of 17.8% from 2026 to 2033, driven by increasing adoption in small clinics, rural healthcare centers, and emerging markets with developing regulatory frameworks. Awareness campaigns, training programs, and capacity-building initiatives support growth. Healthcare providers are gradually adopting partial controlled practices. Non-compliant waste disposal practices are being replaced with improved protocols. Cost-effective management solutions drive adoption in small facilities. Integration of mobile monitoring systems accelerates uptake. Local authorities increasingly provide support for compliance. Environmental and safety awareness boosts adoption. Non-hospital facilities contribute significantly to growth. Technological adoption further improves efficiency and reduces risks.

• By Source of Generation

On the basis of source of generation, the market is segmented into hospitals, physician offices, clinical laboratories, manufacturers, and reverse distributors. The hospitals segment dominated the largest market revenue share of 61.5% in 2025, due to the high volume of hazardous and non-hazardous waste generated daily. Hospitals require full-scale collection, transport, treatment, and disposal services to maintain compliance. Increasing surgical procedures, diagnostic tests, and patient volumes contribute to waste generation. Strict regulatory compliance, accreditation requirements, and risk mitigation programs drive adoption. Centralized treatment facilities and advanced disposal technologies are widely used. Training, staff awareness, and monitoring programs strengthen adoption. Hospitals produce sharps, pharmaceutical residues, infectious, and general waste. Growing healthcare infrastructure globally further boosts the segment. Advanced waste management services are increasingly integrated. Continuous monitoring and regulatory compliance remain critical drivers.

The clinical laboratories segment is expected to witness the fastest CAGR of 22.1% from 2026 to 2033, fueled by increasing diagnostic testing, research activities, and biotechnology applications. Laboratories generate infectious, chemical, and sharps waste requiring specialized management solutions. Outsourcing waste management and adoption of environmentally friendly technologies boost growth. Expansion of testing facilities and government regulations for biohazard waste drive demand. Integration of IoT-enabled tracking, digital monitoring, and automation enhances operational efficiency. Clinical labs in emerging markets increasingly adopt professional waste management services. Safety protocols and training programs further support adoption. Rising prevalence of infectious diseases increases laboratory testing. Research institutions contribute significantly to growth. Technological innovations in sterilization and recycling accelerate segment adoption. Overall, clinical laboratories represent the fastest-growing source of medical waste due to expanding research and testing activities.

North America Medical Waste Management Market Regional Analysis

- North America dominated the North America Medical Waste Management Market with the largest revenue share in 2025, driven by increasing healthcare activities, stringent regulatory enforcement, and the growing adoption of modern waste treatment technologies. For instance, several U.S. hospital networks implemented centralized autoclave and incineration systems in 2025 to efficiently manage biomedical and hazardous waste, ensuring compliance with federal and state regulations

- The region’s advanced healthcare infrastructure, high hospital density, and focus on patient safety are key factors supporting market growth. Hospitals and diagnostic laboratories are increasingly adopting microwave-based treatment units and chemical sterilization methods to safely process infectious waste, reflecting a strong emphasis on environmentally responsible disposal practices

- North American healthcare facilities are investing in integrated waste management systems to streamline segregation, collection, and disposal processes, thereby improving operational efficiency while minimizing environmental impact. Many hospitals in the U.S. have also implemented digital tracking systems to monitor waste streams in real-time, showcasing the growing trend toward modernized, compliant, and sustainable medical waste management practices

U.S. North America Medical Waste Management Market Insight

The U.S. North America Medical Waste Management Market accounted for the largest revenue share of 41.5% in 2025 within North America, driven primarily by large hospitals, clinics, and diagnostic laboratories that are implementing comprehensive waste management systems. For instance, the Mayo Clinic deployed an advanced biomedical waste management program across its multi-campus facilities, including on-site sterilization and centralized monitoring, to ensure compliance with OSHA and EPA regulations. Advanced healthcare infrastructure, high regulatory enforcement, and the adoption of modern treatment technologies, such as autoclaves, chemical disinfection units, and microwave sterilization systems, have played a key role in market growth. The adoption of digital dashboards to track waste volume, type, and treatment methods is becoming increasingly common, enabling hospitals to optimize operational efficiency while maintaining safety and sustainability standards. Furthermore, urban hospitals are increasingly integrating eco-friendly and automated waste handling solutions to meet both compliance requirements and growing environmental awareness among stakeholders.

Canada North America Medical Waste Management Market Insight

Canada North America Medical Waste Management Market is expected to be the fastest-growing region in North America during the forecast period, propelled by increasing healthcare investments, expansion of medical facilities, and rising awareness about safe disposal practices. In Ontario, hospitals have adopted mobile incineration units to treat infectious waste safely in remote and high-demand areas, ensuring effective compliance and minimizing environmental hazards. The expansion of outpatient care centers, diagnostic laboratories, and specialized clinics has heightened the demand for efficient waste management solutions. Several Canadian provinces have introduced incentive programs to encourage hospitals to implement eco-friendly sterilization technologies, promoting the adoption of advanced waste treatment methods. Innovative solutions, such as the combination of chemical and thermal treatments for pharmaceutical and infectious waste deployed in pilot programs in Quebec, exemplify Canada’s commitment to safe, compliant, and environmentally conscious medical waste management practices.

North America Medical Waste Management Market Share

The Medical Waste Management industry is primarily led by well-established companies, including:

• Stericycle, Inc. (U.S.)

• Daniels Health (Australia)

• Veolia Environmental Services (France)

• Clean Harbors, Inc. (U.S.)

• MedPro Disposal (U.S.)

• Shred-it (Stericycle) (Canada)

• Suez Environment (France)

• Biffa plc (U.K.)

• Republic Services, Inc. (U.S.)

• MedWaste Management, Inc. (U.S.)

• SterilMed (U.S.)

• BioMedical Waste Solutions (India)

• Healthcare Waste Solutions (U.K.)

• Waste Management, Inc. (U.S.)

• EnviroWaste Services (Australia)

• MedX Environmental Services (U.S.)

• BioMedical Waste Disposal Co. (India)

• CleanMed Waste Management (U.S.)

• Veolia North America (U.S.)

• Advanced Disposal Services, Inc. (U.S.)

Latest Developments in North America Medical Waste Management Market

- In June 2023, Cabinet Health launched a nationwide recycling program for pill bottles in the U.S., extending its sustainable medicine system to tackle pharmaceutical plastic waste and improve recycling for healthcare products

- In February 2023, EcoSteris opened a state‑of‑the‑art medical waste treatment and disposal facility in Summerville, U.S., enhancing its capabilities in handling and innovating healthcare waste solutions

- In June 2024, Waste Management, Inc. (WM) and Stericycle, Inc. announced a definitive agreement for WM to acquire Stericycle for approximately USD 7.2 billion, representing one of the largest strategic moves in the medical waste services sector to expand comprehensive waste solutions

- In April 2024, Sterilis Solutions partnered with Polycarbin to drive sustainable laboratory waste management practices through innovation and improved recycling techniques in waste streams

- In February 2024, MYGroup entered a partnership with Johnson & Johnson aimed at recycling packaging materials from diagnostic and surgical products, showcasing cross‑industry collaboration for sustainable waste reduction

- In November 2024, after WM’s acquisition, Waste Management completed the purchase of Stericycle, making it a wholly owned subsidiary and signaling consolidation and scale expansion in global medical waste services

- In February 2025, Triumvirate Environmental sold a significant stake to private equity firm Berkshire Partners, valuing the company at about USD 1.8 billion, reflecting major investment and interest in advanced medical waste and environmental services

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.